Recently, the Securities and Futures Commission (SFC) of Hong Kong issued a notice regarding the tokenization of authorized investment products, detailing the types of investment tokenization products that can be sold to the public in Hong Kong, further opening up the connection between Hong Kong and virtual assets. This article will analyze the notice in detail.

Authored by: Crypto Big Brother, Meta Era

Introduction

Recently, the Securities and Futures Commission (SFC) of Hong Kong issued a notice regarding the tokenization of authorized investment products, detailing the types of investment tokenization products that can be sold to the public in Hong Kong, further opening up the connection between Hong Kong and virtual assets. This article will analyze the notice in detail.

Content of the Notice

A. Based on the following market research, the Securities and Futures Commission has decided to further open up the convenience of virtual asset trading.

- The Commission understands that tokenization represents the investment shares of investors, all of which will be recorded on the blockchain and ultimately belong to the investors. However, these products must be distributed by intermediaries licensed by the SFC, or traded among blockchain participants under permitted circumstances.

- Potential benefits of tokenization include improving product efficiency by reducing reliance on intermediaries and lowering operational costs, as well as accessing end investors through new channels.

- To meet market demand, the SFC has further regulated the trading of tokenized products (i.e., subscription and redemption) and the platforms on which tokenized products can be sold.

For secondary trading of virtual assets, the SFC explicitly stipulates that the level of investor protection should be equivalent to that of non-tokenized products. Considerations include maintaining appropriate and immediate token ownership records, preparing trading infrastructure and market participants to support liquidity, and ensuring fair pricing of tokenized products, among others.

B. In light of the above, the SFC has issued the following trading terms

- Providers of tokenized SFC-authorized investment products (product providers) must ensure that the underlying products comply with the applicable requirements of relevant regulations and product codes (including the eligibility of product providers, product structure, investment and operational requirements, disclosure, and ongoing compliance obligations).

It is evident that while the SFC maintains an open attitude towards virtual assets, it is no less stringent than traditional financial assets in terms of compliance. Whether in terms of trading compliance or fair pricing, investors in Hong Kong can confidently choose their preferred virtual financial assets for trading. In this environment, Hong Kong may indeed be the preferred location for the issuance or trading of virtual assets in the future.

C. Tokenization Arrangements

Product providers are responsible for maintaining and ultimately managing the soundness of the adopted tokenization arrangements and ownership records, regardless of any outsourcing arrangements. This eliminates the risk of shifting responsibility to third-party organizations. For example, if technical outsourcing is provided to a foreign technical team and a "disaster" occurs resulting in significant asset losses for investors, this provision requires product providers to focus on operational oversight. Therefore, the following operational regulations have been issued:

- Product providers must ensure appropriate records of token holders' ownership interests in the products, and the tokenization arrangements are compatible with the involved service providers.

- Product providers must take appropriate measures to manage and mitigate network security risks, data privacy, system failures and recovery, and maintain comprehensive and robust business continuity plans.

- Product providers should not use public or unlicensed blockchain networks without additional and appropriate controls. For example, product providers can use permissioned tokens to impose additional controls, and all operations must be transparent without any backdoors.

- Product providers must, at the request of the SFC, confirm and demonstrate the soundness of the management and operation of the tokenization arrangements, ownership records, and the integrity of smart contracts. The SFC may obtain third-party audits or verifications of the soundness of the management and operation of the tokenization arrangements, ownership records, and smart contracts.

D. Disclosure Matters

- Before purchasing, it should be clearly disclosed whether settlement is offline or on-chain.

- Representation of token ownership (e.g., legal and beneficial ownership of tokens, ownership/equity in the product).

- Risks associated with the tokenization arrangements, such as network security, system failures, potential undiscovered technical defects, the evolution of regulatory environments, and challenges posed by the application of existing laws.

These terms should also be disclosed to consumers before purchase, and consumers must be aware of the risks.

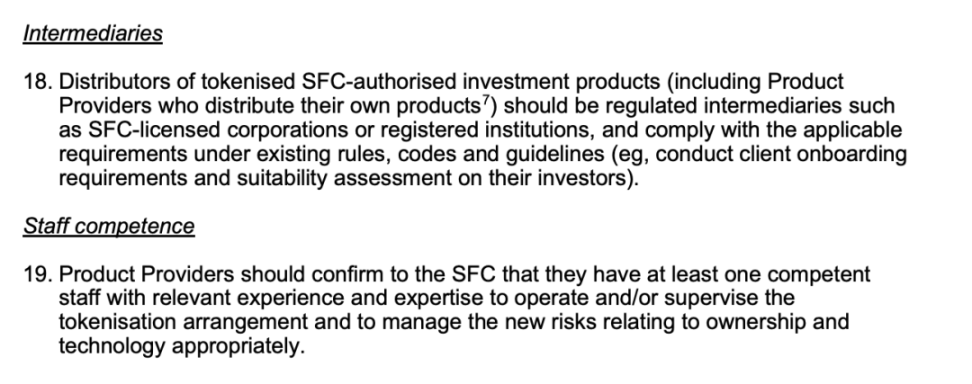

E. Intermediaries

In terms of tokenization, distributors of SFC-authorized investment products (including product providers distributing their own products) should be regulated intermediaries, such as companies or registered institutions licensed by the SFC, and comply with the applicable requirements of current rules, guidelines, and directives (e.g., fulfilling customer onboarding requirements and conducting suitability assessments of their investors).

After a product is licensed by the SFC, the product provider also needs to confirm to the SFC that they have at least one competent employee with relevant experience and expertise who can operate or supervise the tokenization arrangements and appropriately manage new risks related to ownership and technology.

This is similar to traditional securities exams, where traditional financial practitioners need to pass exams and obtain licenses before they can work. However, there are currently no specific exams related to virtual currencies, and the specific standards are based on internal regulations of the SFC.

F. Prior Consultation or Approval

In addition to new investment products with tokenization features seeking SFC authorization, prior consultation with the SFC is required for the tokenization of existing SFC-authorized investment products, and such changes may require prior approval.

Conclusion

The conclusion drawn from the new regulations issued above is that the SFC has allowed intermediaries and institutions to open tokenized financial products to the public. However, the premise for all of this must be compliance and legality, and Hong Kong absolutely does not allow any illegal situations to occur. By maintaining existing policies and continuously advancing and improving them, it is believed that in the future, Hong Kong will become a safe haven for the development of virtual assets and related industries, as well as a new home that allows them to grow in compliance.

Original Notice:

[1] SFC's latest release of the "Notice on SFC-authorized Investment Products with Tokenization Features" in Chinese

https://www.metaera.hk/gw_detail?id=164770

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。