Author: Yuuki&Jill, LD Capital

Introduction

Since the beginning of this year, DWF has gained a reputation, attracting large investments, and tokens associated with it have seen significant price increases. How has DWF achieved this during the current bear market in the crypto market? And how should primary market investors participate in related targets?

Conclusion

DWF is a product of the bear market under weak regulation, using the dilemma of project teams and the psychology of retail investors to achieve dual profits. During the bear market, project teams generally face difficulties in realizing assets and financing, and directly selling tokens would undermine fragile market confidence, significantly impacting token prices and project ecosystems. In this scenario, DWF acts as a bridge for project teams to sell tokens, helping them unload through OTC or other marketing means. Describing the behavior of obtaining OTC tokens from project teams as strategic investment, in reality, it does not provide substantial help for the long-term development of the project and instead sells the tokens; by disguising the nature of the project team's indirect selling through publicity, DWF also profits from both the project team and the market in this process.

As secondary market investors, after seeing information about a project's cooperation with DWF, it is necessary to first distinguish what business DWF is involved in (secondary investment, OTC, market making, marketing) and use different strategies for different businesses. Based on past market performance: 1. It is important to pay close attention to targets directly involved in secondary market investment by DWF, which are usually newly listed coins with good chip structures or meme coins; 2. Targets in which DWF buys tokens OTC from project teams (packaged as strategic investment) often initially show a few months of decline in the secondary market, followed by a rapid price surge, ending after DWF deposits tokens into exchanges (the surge usually lasts no more than 1 week); 3. Genuine market-making projects by DWF do not have doubling market trends, but usually attract speculative capital, providing a brief window for establishing positions, which can be seized in advance; 4. Market trends triggered by DWF-related marketing news have a poor success rate and risk-reward ratio, as stakeholders use DWF's current market influence to attract liquidity and dump tokens. After determining DWF's intention to boost prices, the sharp increase in contract holdings and spot trading volume is a signal of the market's initiation; DWF's on-chain address interacting with exchange addresses (at high prices), decreasing holdings, and extreme negative funding rates often signal the end of the market trend.

Main Body

DWF Labs is a subsidiary of Digital Wave Finance (DWF), a global cryptocurrency high-frequency trading company that has been trading spot and derivatives on over 40 top trading platforms since 2018. When DWF Labs first appeared in the crypto market, it presented itself as a market maker. The real attention to DWF in the market began with the explosive rise of Hong Kong concept coins such as CFX and ACH in the first quarter, followed by meme coins like PEPE and LADYS with tens of times increase in the second quarter, and more recently, the several-fold increase in listed targets like YGG and CYBER. Among these, CFX, ACH, and YGG were obtained OTC, while PEPE (MEME), LADYS (MEME), and CYBER (Binance Launch Pool) were directly purchased through the secondary market by DWF due to their good chip structures.

Some tokens related to DWF have attracted market attention with several-fold increases

The reasons DWF has attracted market attention are not only due to the significant price fluctuations of the currencies it handles but also due to its discord with other peers. Well-known market makers like Wintermute and GSR have publicly expressed dissatisfaction with DWF, considering it a poor-quality market maker and a bad actor.

Deconstructing the business scope of DWF:

In the crypto market, investment and market making are usually two distinct concepts. Investment usually refers to injecting funds into a project before the issuance of tokens to support project development, operations, and marketing, and receiving token shares with a lock-up period as a reward after the project goes live; while market making aims to provide good liquidity for already issued tokens, reduce trading costs, and attract more traders. The source of returns for investment activities comes from the token returns of the invested project, while the source of returns for market making activities comes from the market making fees paid by the project and the spreads earned during market making (the price difference between buying and selling). Well-known investment institutions in the crypto market include A16Z and Paradigm, while well-known market makers include Wintermute and GSR.

DWF has been criticized by participants in the crypto market for often confusing the concepts of investment and market making. On its official website, it positions itself as a Web3 venture capital and market maker, with three types of businesses: investment, OTC, and market making.

Based on the past performance of DWF-related targets, it primarily selects targets with emotional themes for market making, including CFX, MASK, YGG, C98, WAVES, and others. However, it is found that in its past market making cases, it rarely genuinely supports the long-term development of projects. DWF typically chooses to inject funds at a discount into "struggling" projects that have already issued tokens, and then sells for profit in the secondary market. Moreover, during this process, it often aggressively boosts the prices of the projects it "invested" in, not only selling tokens at high prices but also establishing a money-making image in the minds of retail investors, and then continues to sell this image advantage to the project as a product; for example, by jointly disclosing large investment information with the project to create market optimism and attract liquidity for better selling of tokens.

Surface business: Investment, market making, OTC, marketing

Business essence: Injecting funds into "struggling" projects, obtaining tokens at a discount through OTC, selling for profit in the secondary market; aggressively boosting prices to establish a brand image and then selling this image advantage as a product to the project. Specific cases are as follows:

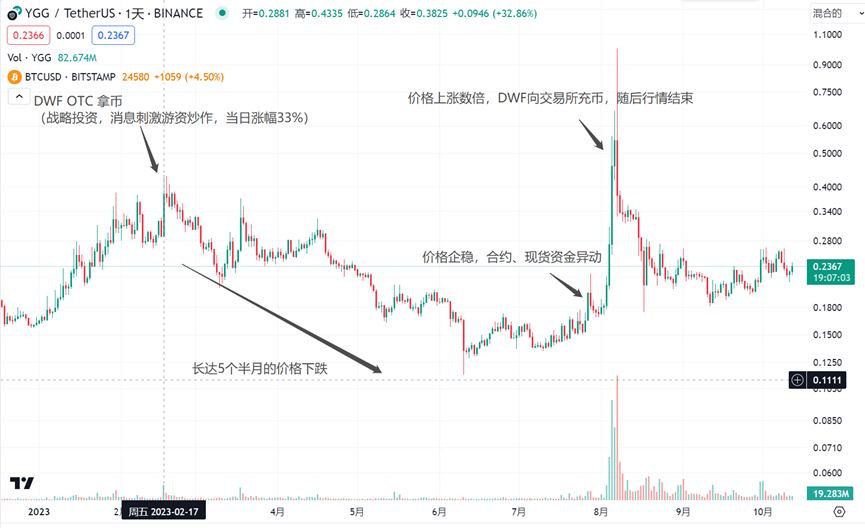

1. YGG & C98: OTC Purchase, Secondary Market Price Boost

On February 17, 2023, the blockchain gaming guild Yield Guild Games (YGG) raised $13.8 million through the sale of tokens, with DWF Labs and A16Z leading the investment (YGG had already issued tokens in 2021).

It is worth noting that DWF Labs had already received 8 million YGG tokens from YGG's treasury on February 10, and then transferred 700,000 tokens to Binance on February 14. On February 17, media reports on the investment information were followed by DWF making two more transfers, 3.65 million tokens on June 19 and 3.65 million tokens on August 6. Considering YGG's price performance: on February 17, influenced by the investment information, YGG saw a maximum increase of 50% and closed with a 33% increase; it then began a decline lasting for 5 and a half months until the start of a price surge in early August, with YGG rising over 7 times from its previous low, and the market trend ended when DWF made the final transfer of YGG tokens to Binance.

As a secondary market investor, at the beginning of the YGG market trend, anomalies in contract data can be observed. YGG's contract data initially showed a sharp increase in holdings and stable rates; in the middle term, it showed a slowdown in holding growth and a decrease in rates, and in the later term, it showed a decrease in holdings due to long positions being closed.

Similar trading tactics can also be observed in targets such as CYBER: On August 22, DWF withdrew 170,000 CYBER tokens from Binance, when the price of CYBER was approximately $4.5. Subsequently, the price continuously declined, reaching a low of $3.5. Seven days later, a price surge for CYBER began, reaching a high of $16.2, approximately 3.6 times higher than the price at the time of DWF's withdrawal, and about 4.6 times higher than the previous low. As a Binance Launch Pool project, CYBER had a good chip structure early on, with minimal selling pressure in the secondary market. DWF's involvement in the CYBER project is inferred to be buying tokens in the secondary market to boost prices, with minimal involvement with the project team. (Similar to DWF's involvement in meme coins such as PEPE and LADYS in the second quarter of this year)

In terms of funding data, CYBER's performance is similar to YGG: the contract data initially showed a sharp increase in holdings and stable rates; in the middle term, it showed a slowdown in holding growth and a decrease in rates, and in the later term, it showed a decrease in holdings due to long positions being closed.

On February 2, 2023, the DWF on-chain address received a transfer of approximately 4.12 million tokens from the official Coin98 address, equivalent to about $1.11 million at the market price on that day (the secondary market price of C98 was approximately $0.27 on that day), and immediately transferred to Binance. On August 8, Coin98 announced a seven-figure investment from DWF Labs to drive the widespread adoption of Web3. On October 12, according to media reports, DWF transferred 1 million USDT to C98. Considering C98's price performance, after DWF received and transferred the tokens to the exchange, C98 briefly rose before entering a 5-month decline. On August 8, the media reported a 58% increase in price in two days compared to the previous low, followed by a rapid decline. In retrospect, the essence of this event may be DWF obtaining tokens from the C98 project at a discount, and then selling for profit in the secondary market.

The data performance of C98 before the price surge showed a significant increase in holdings, and the end of the market trend was marked by a decrease in holdings due to long positions being closed, accompanied by a return of rates.

Similar targets with price surges include LEVER, WAVES, CFX, MASK, ARPA, and others.

The above are recent typical examples of DWF's trading targets. It can be seen that DWF usually participates in both the futures and spot markets. In the early stages of a market trend, a large amount of funds can be observed entering the futures market. Due to the early long positions in the futures market, the increase in holdings does not affect the rates. In the middle term, it typically shows a spot market price surge, with the main long positions in the futures market starting to close, often resulting in a sharp increase in spot prices, severe negative futures rates, stagnant or decreasing growth in holdings. Some targets may also have a final surge to create liquidity, allowing the main spot market to obtain better selling prices and liquidity. After the main futures long positions profit, the market trend may end directly. It is crucial to determine whether the benefits of continuing the surge in the spot market for the main players in the final stage will outweigh the costs. (For example, whether there is a key resistance level, and whether there is a large amount of selling pressure in the market)

2. "Marketing-style" Investment, On-Chain Transfers, Using Brand Image to Create Optimism to Conceal Selling Nature

As a new investment institution, DWF has been active in the bear market, with over 260 projects in collaboration. According to media reports, DWF has invested in over 100 projects, many of which involve large investments. Some projects in which DWF has invested over $5 million include:

DWF co-founder Grachev stated that DWF Labs has no external investors, but its high-frequency and large-scale investments have raised questions about the source of its funds. Many of the projects it has invested in are not industry trend projects, but rather mostly older projects with average or poor fundamentals (such as EOS, ALGO, etc.). After announcing investments, there has been no improvement in product development, marketing, or community cooperation for these projects. Some of DWF's actions may be aimed at creating "marketing-style" investments to attract retail investors and repeatedly speculate on token prices in the secondary market, facilitating the team's token sales. (FET announced a $40 million investment, but DWF has only received approximately $3 million in tokens so far)

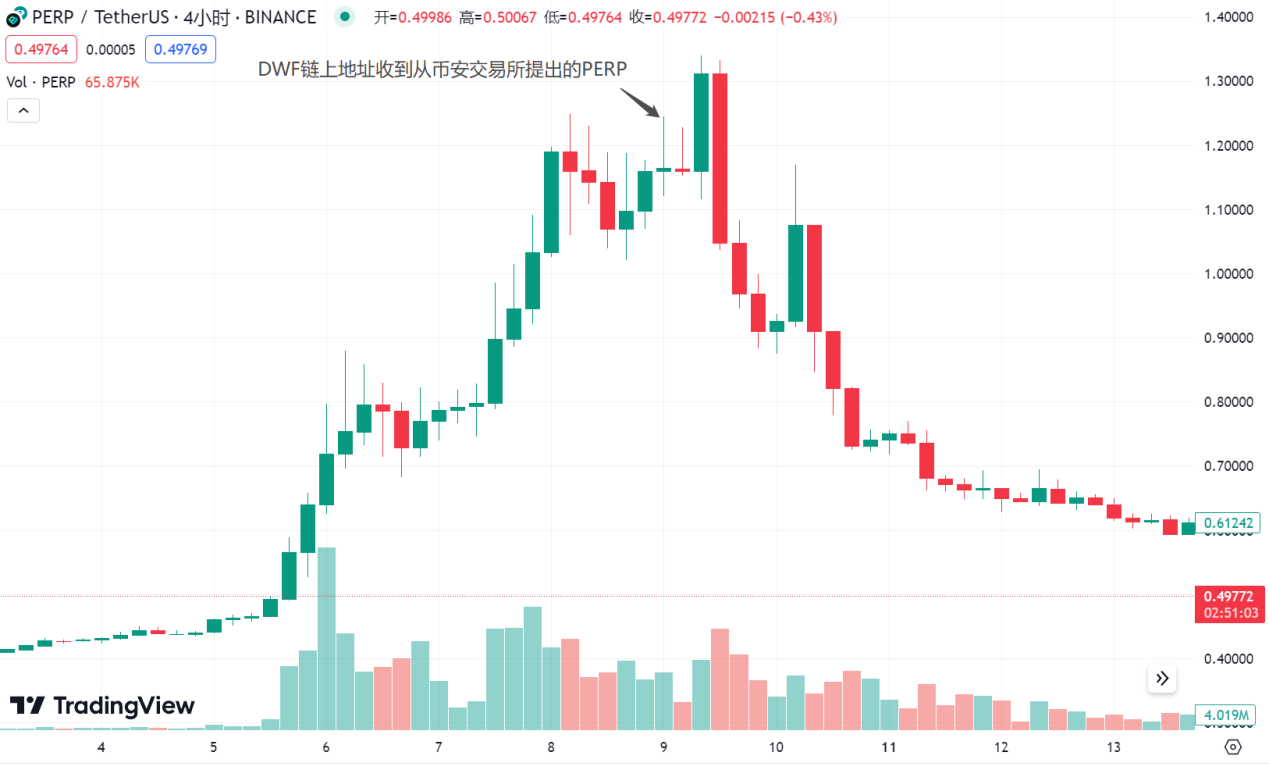

Additionally, on September 8, the DWF on-chain address received a transfer of PERP from Binance. Prior to this, PERP had already seen a significant increase in price. After DWF's withdrawal from the exchange, there was a noticeable increase in buying pressure for PERP, leading to a brief price surge followed by a significant sell-off and a downward trend.

On October 17, BNX announced a strategic partnership with DWF. Prior to the announcement, BNX had experienced a significant increase in price for a week. After the information was disclosed, there was a rapid sell-off, likely involving insider trading, using DWF's brand effect to release news and create liquidity for selling.

Examples of project teams and DWF using their brand influence to create optimism and attract liquidity for selling are common. Secondary market participants need to carefully discern when they see information related to DWF. Many targets related to DWF have experienced continuous price declines, such as EOS, CELO, FLOW, BICO, and others.

3. Seeking "Struggling" Projects, Using the Difficulty of Financing in the Bear Market to Maximize Bargaining Power and Profits

Abracadabra (SPELL) is a stablecoin project collateralized by interest-bearing asset certificates (such as stablecoin LP in Curve, stablecoin deposit certificates in Yearn, etc.). After experiencing the UST default (UST was once an important underlying asset for Abracadabra, and after the UST default, Abracadabra accumulated a large number of bad debts) and a prolonged bear market, the protocol's TVL, token price, and overall development have been struggling. On September 14, it passed Proposal AIP#28, which introduced DWF as the market maker for SPELL. The market making terms included: 1. Abracadabra providing a $1.8 million SPELL loan to DWF for 24 months; 2. DWF purchasing $1 million worth of tokens from the DAO at a 15% discount to the market price, with this portion locked for 24 months; 3. Abracadabra paying DWF a European call option as market making fees after the loan period ends.

In this market-making agreement, the cost paid by the Abracadabra project team is significantly higher compared to other market-making projects in the industry, including discounted token purchases and European options. Due to the inclusion of market-price discounted token purchases in the market-making terms, from DWF's perspective, a short-term reduction in token price is beneficial for maximizing its interests. Combined with the market performance, the price of SPELL has been declining steadily since DWF's entry. Specifically:

The proposal was voted on from September 11th and passed on September 14th. In response to this information, the price of SPELL rose from a low of 0.0003716 on September 11th to a high of 0.0006390 on September 19th, a maximum increase of 72% (speculative trading in the market).

On September 19th, Abracadabra provided a $3.3 million SPELL loan to DWF, which was then transferred to Binance. SPELL entered a downward trend, with the current price at 0.0004416, a 31% decrease from the previous high point.

From the funding data, it can also be seen that in the short-term market trend of SPELL, there is poor consistency in funding, with 70% of the increase involving multiple fund relays, indicating strong uncertainty.

In summary: DWF initially created a wealth effect and built its brand image through price manipulation. It is a product of the bear market under weak regulation, using the development difficulties of project teams and the psychology of retail investors to achieve profits from both ends. Project teams in the bear market generally face difficulties in realizing their assets and obtaining financing, and directly selling tokens will undermine fragile market confidence, severely impacting token prices and project ecosystems. In this situation, DWF acts as a bridge for project teams to sell tokens, helping them with OTC or other marketing methods. The behavior of obtaining tokens from project teams through OTC is described as strategic investment, but in reality, it does not provide substantial help to the long-term development of the project and instead involves selling the tokens. By using promotional packaging to conceal the nature of the project's indirect selling, DWF also achieves profits from both the project team and users in this process.

As a secondary market investor, when seeing information about a project's collaboration with DWF, it is important to first distinguish what kind of business it is for DWF (secondary investment, OTC, market-making, marketing) and use different strategies for different businesses. In previous market performances:

Targets directly involved in the secondary market investment by DWF need to be closely monitored. These targets are typically new coins listed on exchanges with a good chip structure or meme coins.

Targets in which DWF buys tokens OTC from project teams (packaged as strategic investments) often initially show a few months of decline in the secondary market, followed by a rapid price surge, and the market trend ends after DWF deposits tokens into the exchange (the surge usually lasts no more than 1 week).

Truly market-making projects by DWF do not typically have a doubling market trend, but they often attract speculative trading and have a brief window for establishing positions, so being proactive is key.

Market trends triggered by DWF-related marketing news have a poor win rate and risk-reward ratio. The underlying logic is that stakeholders use DWF's current market influence to attract liquidity and sell off tokens. When there is an intention for price manipulation by DWF, a surge in contract holdings and spot trading volume is a signal of the market trend starting; interactions between DWF's on-chain address and exchange addresses (at high prices), a decrease in holdings, and extremely negative funding rates often signal the end of the market trend.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。