A piece of news about Meta "selling computing power" heavily impacted the AI hardware sector, CoreWeave dropped 13% in a single day, Nebius fell 15%, and the narrative of "excess computing power" rapidly spread.

However, well-known semiconductor research organization SemiAnalysis believes that the market's interpretation of Meta "renting out computing power = cutting expenses" is incorrect. On July 3, the organization released an interpretive report stating:

“We believe that both interpretations are wrong; Meta's data center and computing power procurement will accelerate rather than slow down. Capital expenditure in 2027 will be astonishingly high.”

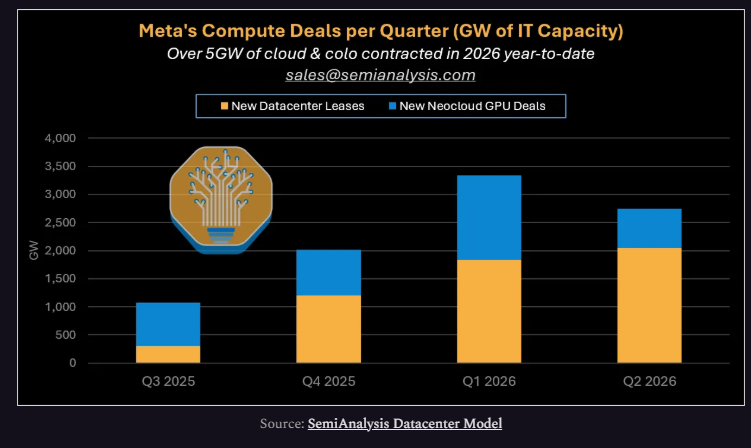

To support this judgment, SemiAnalysis provided a set of specific numbers: in the first half of 2026 alone, Meta signed contracts for over 5 GW of data center capacity, covering cloud leasing and co-location, not including the full progress of self-built projects.

Meta's two largest under-construction data center campuses—satellite/aerial images—these two campuses have a combined construction capacity of 2.5 GW.

The report also countered another widely circulated market narrative—“half of the US data center projects are delayed, with only 5 GW under construction nationwide.” SemiAnalysis stated: just Meta's two campuses are already equivalent to half of that number; “these headlines are completely wrong.”

Four Paths: Why Meta Can Continuously Bet on Computing Power

SemiAnalysis believes that the market misjudges because it only sees the action of "selling computing power" but fails to understand why Meta has the confidence to continue expanding.

The report outlines four high-value monetization directions, each fundamentally different from the typical Neocloud's "bare metal IaaS" model.

First, cutting-edge AI models (MSL) remain core.

SemiAnalysis explicitly states that Meta has not abandoned training cutting-edge models. Meta Superintelligence Labs (MSL) is still the largest destination for incremental computing power. The report states that the team is currently "excited" about their progress and will issue a deep report assessing MSL’s chances of catching up with Anthropic and OpenAI.

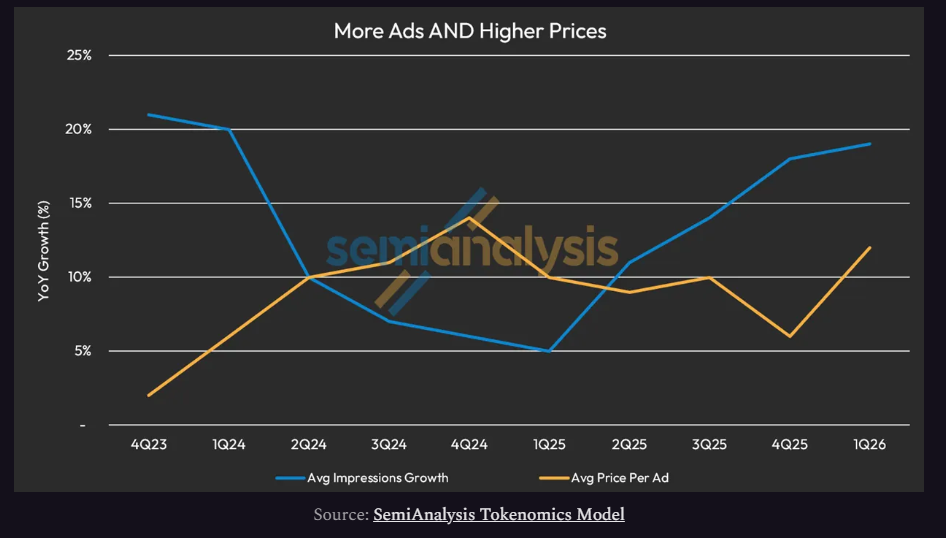

Second, the advertising recommendation system (RecSys): a 10x expansion space.

SemiAnalysis believes Meta believes it can expand the complexity of the advertising recommendation system by more than 10 times to accelerate revenue growth. This requires investment in both reasoning and training computing power. Larger and more expensive RecSys models drive advertisers to pay higher prices while maintaining strong advertising return rates (ROAS), and they also encourage users to spend more time on Meta's applications, expanding the addressable advertising inventory.

Third, Bedrock-like model API services.

SemiAnalysis reveals that Meta is in the final negotiation stage of signing an agreement with Anthropic, which will grant it private deployment rights for Claude, similar to how Amazon gains access to Claude through Bedrock, with the distinction being that it operates within Meta's own data centers. This means that in the future, Meta will not only sell its own models but also bundle Claude with its computing power and platforms to provide external services.

SemiAnalysis listed three monetization paths:

- Internal use: Meta itself needs tokens for Claude, but Anthropic's supply cannot keep up with the demand; private instances can also provide stronger security and privacy protection.

- Selling Claude services externally: Similar to the Bedrock model, Meta controls the complete technology stack from CPU to GPU to network, which is highly secure; however, as a new entrant, establishing relationships with enterprise clients is a challenge.

- Vertical integration to create application layers: Meta is one of the largest advertising platforms globally, with paths to build AI Agent products in sales and marketing, deeply integrating cutting-edge models.

SemiAnalysis also pointed out that distributing models to free social media users and Meta's hardware ecosystem (like smart glasses) is also a potential option, which holds high strategic value for OpenAI and Anthropic, “They are likely willing to make concessions in exchange for the opportunity to enter this distribution channel.”

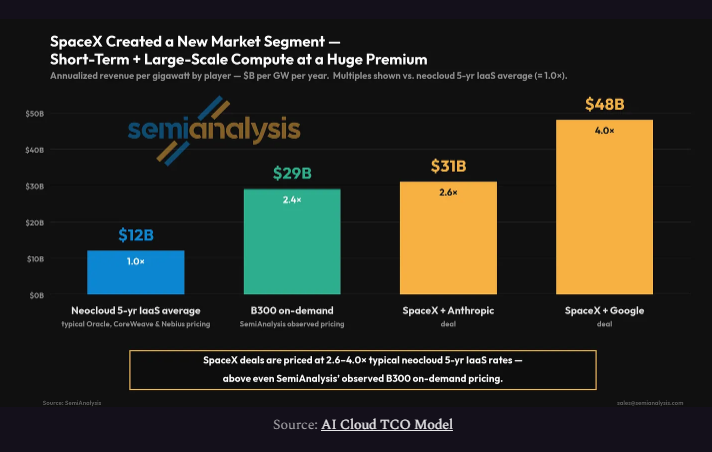

Third, "SpaceX-style" bulk computing power leasing. Musk created a new market, and Meta wants to share in it.

This is the most striking judgment in the report.

The computing power leasing agreement signed between SpaceX and Google shocked the entire AI infrastructure circle—its pricing is four times that of similar industry products, and its pricing with Anthropic is also three times that of peers.

SemiAnalysis's AI Cloud TCO team tracks hundreds of GPU cloud transactions annually, possessing the most complete global GPU pricing database. Their conclusion is: “We have never seen agreements of such scale and such short duration. This contract nominally has a three-year term, but both parties can cancel within 90 days—effectively, it is a 3-month contract that automatically renews.”

Why hasn't anyone done this before? Because very few companies can. Typical Neoclouds require long-term contracts to cover financing costs and simply cannot provide a 90-day cancellation option. The three major hyperscale cloud providers (Microsoft, Amazon, Google) have the technical capabilities, but each has higher-value long-term binding strategies—Microsoft has equity and IP in OpenAI, Amazon focuses on promoting Bedrock and Trainium, and Google does TPU and Vertex.

The result is that only two companies can truly replicate the SpaceX model: Oracle and Meta.

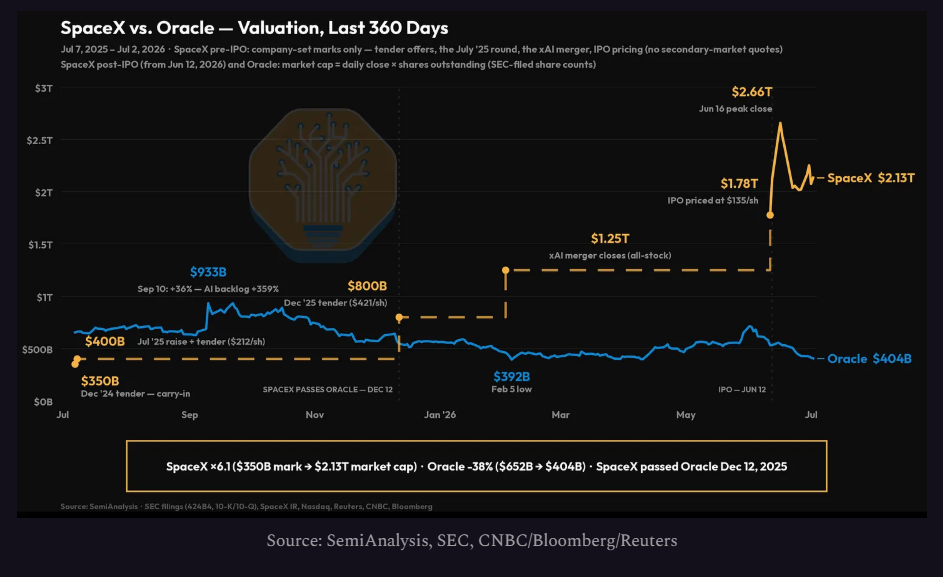

SemiAnalysis’s evaluation of Oracle is blunt: “This is a significant blow to Oracle. They could have monetized their few GW of computing power better.” The report illustrates how significant this differentiation is by comparing the valuation trends between Oracle and SpaceX.

Where is Meta's advantage? Lots of computing power, fast construction, and the ability to cancel contracts at any time.

At a pricing of $50 billion in annual revenue per GW, just allocating 200 MW to external clients could bring in over $10 billion annually, with extremely high profit margins. The 90-day cancellation clause means that if the Meta Superintelligence Labs needs more computing power, it can reclaim it at any time.

The report also mentioned Meta's rapid "tent-style" data center construction strategy—SemiAnalysis was the first to track this design last year, and such facilities are rapidly landing across the United States. Quick deployment and monetization align closely with the SpaceX model.

SemiAnalysis expects that Meta will soon announce a large customer computing power leasing agreement similar to SpaceX, with the most likely target being Anthropic.

"CFO's Dream": High Optionality Makes Meta More Comfortable Buying

This is one of the core logics of the entire SemiAnalysis report.

The existence of four monetization paths means that each GW of Meta's computing power has multiple high-value outlets. This is not “having too much to lose” but rather “having options with more purchase.”

The report's wording is: “This is basically the CFO's dream, making all-in computing power very easy. We would bet that Susan (Meta CFO Susan Li) had a complete turnaround after seeing the SpaceX computing power agreement pricing!”

The logic is straightforward: if Meta Superintelligence Labs succeeds, all computing power will be used in-house, yielding the highest ROI; if Meta Superintelligence Labs faces setbacks, a portion of the computing power can be put into the SpaceX model or Bedrock model, generating high-margin revenue immediately; if the RecSys expansion is below expectations, there are still other outlets to digest the capacity.

This high optionality also brings another effect: Meta can fully continue to procure computing power from third-party Neoclouds like CoreWeave and Nebius, because even if they “sublet” this computing power, the profit margin is still sufficient to cover costs.

SemiAnalysis has provided reassurance for Neocloud investors here—“Meta will not be a bare metal IaaS supplier with only a 30% gross margin; all its monetization options are high value. This gives it enough profit margin to provide computing power to external customers while continuing to procure capacity from Neoclouds to accelerate expansion.”

In other words, Meta is more likely to be an important source of RPO growth for companies like CoreWeave rather than a competitor.

RecSys: The Most Overlooked Computing Power Monetization Engine

Another dimension is the advertising recommendation system.

From the end of 2022 to the beginning of 2023, the market generally believed that Meta had entered a mature growth phase. However, in the following years, Meta's revenue growth significantly accelerated. SemiAnalysis's judgment is: GPU investment is a key trigger factor.

The logical chain is: larger and more expensive RecSys models → more precise advertising placements → advertisers willing to pay higher prices → advertisers’ ROAS (advertising spending return rate) remains strong → forming a positive cycle.

At the same time, the upgrading of content recommendation systems has boosted user retention on Meta’s applications, further expanding the advertising inventory.

So, how far can the AI expansion of RecSys go? SemiAnalysis believes Meta itself thinks it can increase model complexity by over 10 times.

SemiAnalysis’s core conclusion is clear: Meta renting out computing power is not because it over-purchased computing power but rather because it has enough computing power to support multiple high-value strategies simultaneously, and each option is profitable enough.

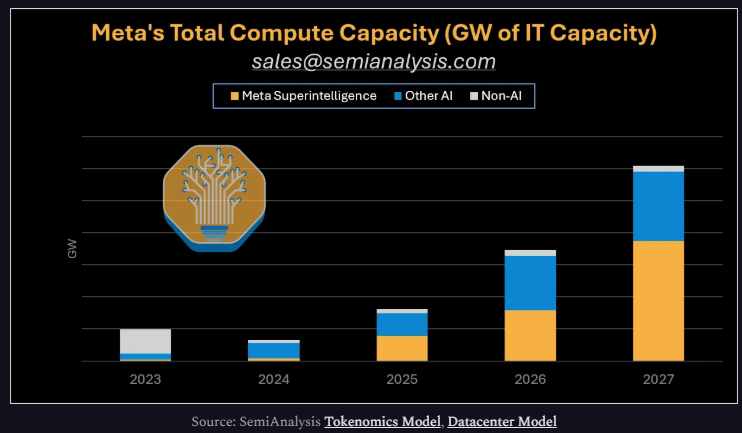

Capital expenditure in 2027 will exceed market expectations by a large margin.

For investors, this report is essentially saying: that wave of sell-offs may have been a misjudgment. But SemiAnalysis also leaves an important footnote: whether MSL can truly catch up with Anthropic and OpenAI remains the biggest uncertain variable.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。