Author: Zheng Jie

Translation: Deep Tide TechFlow

Deep Tide Introduction: Artemis is a leading data analytics institution in the cryptocurrency industry, and this report comes from its analyst Zheng Jie. Strategy (formerly MSTR) has seen its mNAV drop from 6 times to 1.15 times, and the DAT sector has been collectively demystified, but the author believes that PURR should not be treated equally: Strategy spends $2.3 million daily to service debt, while the ETH and SOL purchased by BMNR and Forward Industries are already locked up, while the HYPE held by PURR comes from a real profit machine that earns $857 million a year, with 99% of its revenue used for repurchases and destruction.

Conclusion

The market is pricing PURR under the framework of another MSTR: issuing shares at a premium, buying more tokens, and increasing the number of tokens per share. We believe this pricing is wrong. Strategy spends $2.3 million daily to pay interest on $780,897 worth of Bitcoin, $835 million in preferred stock, and convertible bonds annually, while Bitcoin itself does not generate a cent; its mNAV has already dropped from a peak of over 6 times to today's 1.15 times. PURR has no debt, no preferred stock, no recurring expenses, and the 18.8 million HYPE tokens it holds are backed by the only mainstream protocol generating positive returns in 2025: $857 million in service fees (with $797 million from perpetual contracts at a 2.72 basis points fee), with 99% flowing into the Assistance Fund, $837 million used for repurchasing and destruction, and operating costs almost zero. The token structure is deflationary: approximately 19 million are bought back and destroyed each year, while about 7 million are released from the staking reserve. The stock's current price is 1.12 times mNAV. Our baseline assumption is that HYPE reaches $76 by 2030, corresponding to an expected revenue of $1.71 billion and a 20 times price-to-earnings ratio, with PURR maintaining 1.1 times mNAV, corresponding to a stock price of $10.59, offering about 63% upside over five years. In an optimistic scenario, HYPE reaches $127, 1.3 times mNAV, corresponding to $20.84, +220%. In a pessimistic scenario, HYPE compresses to $27, with a 16 times price-to-earnings ratio and 0.95 times mNAV, corresponding to -49%.

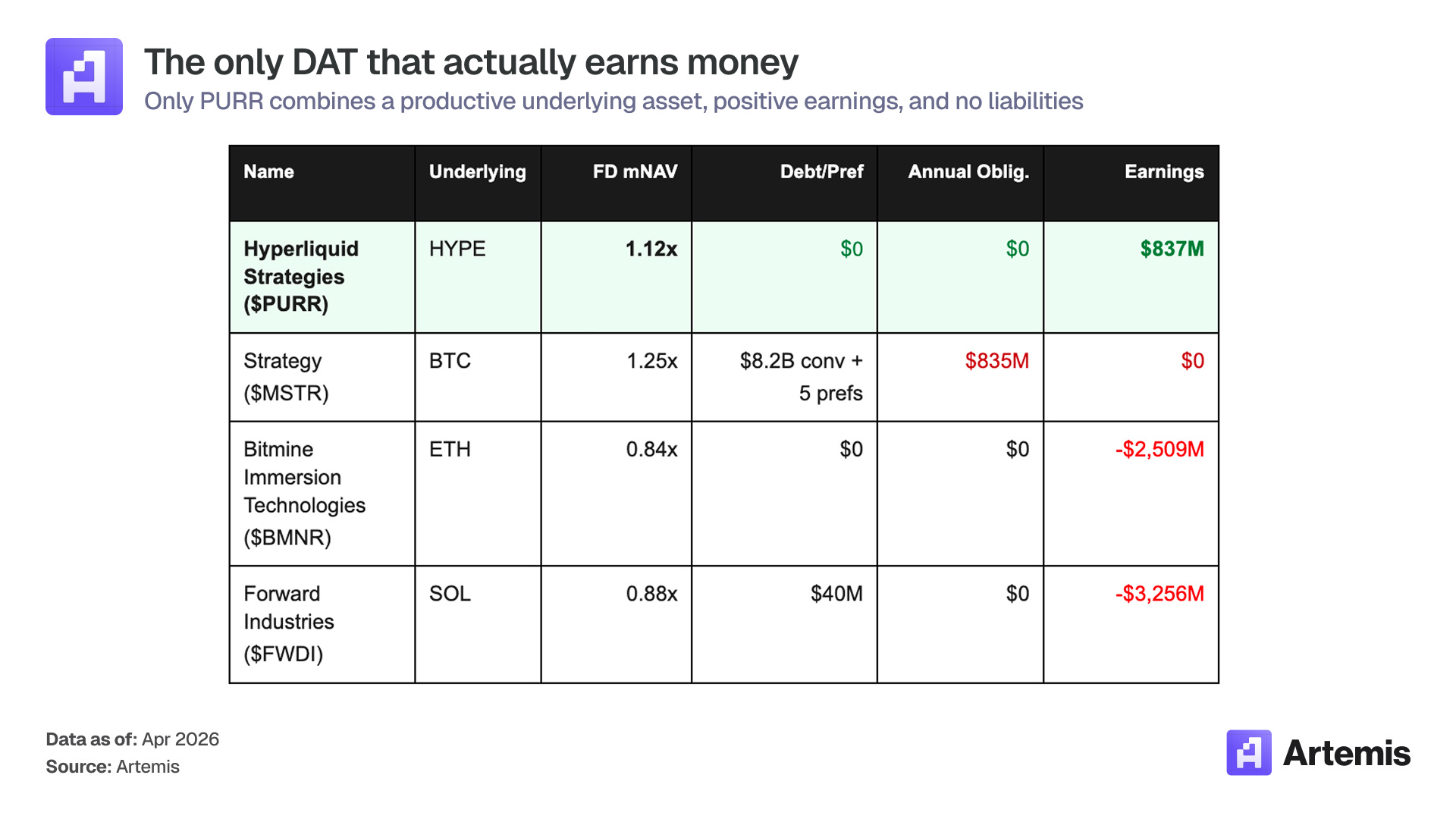

Comparison: PURR's Special Position in the Digital Asset Treasury Sector

Caption: Among all Digital Asset Treasury (DAT) companies, only PURR meets three criteria: underlying assets generate cash flow, recorded profits, and zero debt.

What is PURR?

Hyperliquid Strategies Inc (NASDAQ: PURR) is a Digital Asset Treasury (DAT) company whose sole mission is to hoard and hold HYPE, the native token of the Hyperliquid protocol. The company was founded in December 2025 through an $888 million merger with Sonnet BioTherapeutics, the SPAC company Rorschach I LLC under Paradigm, and a new entity set up by Atlas Merchant Capital.

Its balance sheet is the cleanest in the entire DAT sector: 18.8 million HYPE, $112.6 million cash, zero debt, zero preferred stock, zero convertible bonds. In January 2026, the company authorized a $30 million stock repurchase plan. As of February 3, 2026, $10.5 million has been used to repurchase about 3 million shares, fully diluted total equity reduced to 150.8 million shares. There is also a $1 billion equity line available outside of cash, serving as backup ammunition during HYPE pullbacks.

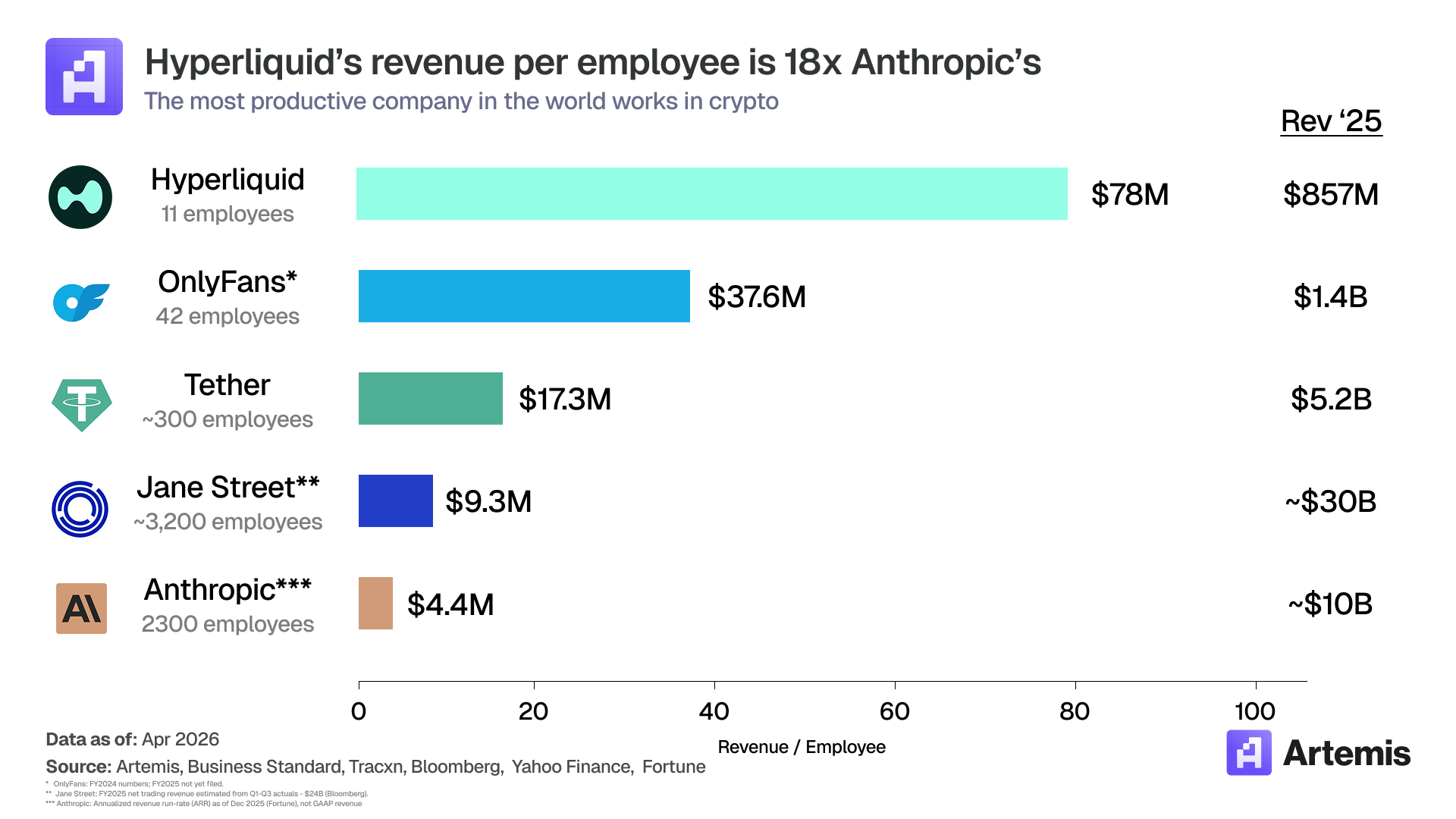

What makes this structure unique is the underlying assets. HYPE is equivalent to a Hyperliquid equity token, a perpetual contract exchange that generated $857 million in service fees in 2025, with only 11 employees (annual revenue per employee of about $78 million, the highest among all companies worldwide).

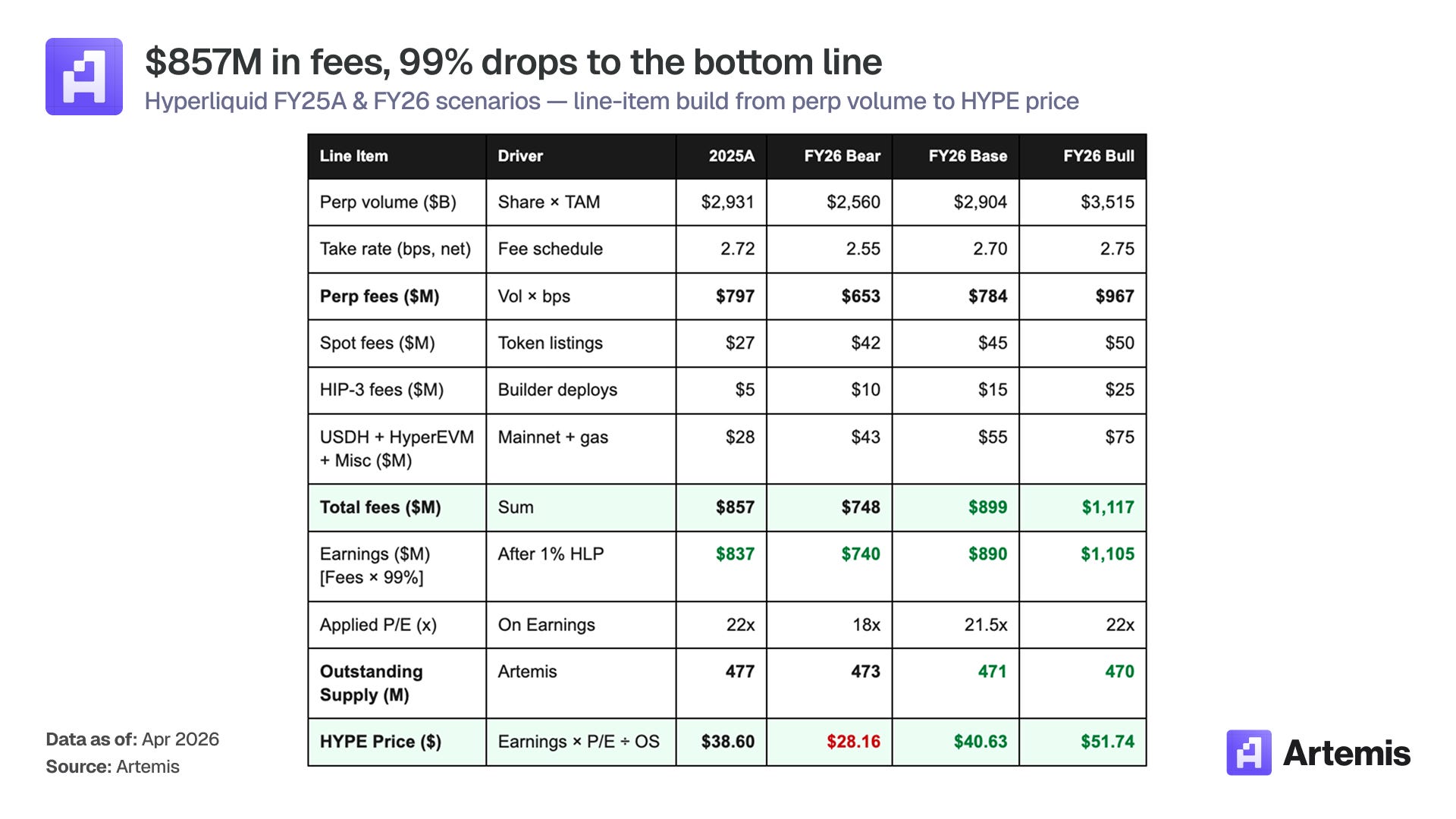

Caption: Fundamental data of the Hyperliquid protocol: $857 million in service fees in 2025, with 99% flowing into the Assistance Fund for repurchasing and destruction of HYPE.

Fee-Making Machine

Hyperliquid is an exchange.

The model is a business of "trading volume × fees," with marginal costs close to zero.

The fee distribution mechanism is divided into six projects:

Caption: Hyperliquid fee distribution waterfall chart: spot/perpetual fees, HLP sharing, Assistance Fund repurchase, staking release, etc.

Argument One: The Only Profitable Underlying Asset

Every DAT company listed on US exchanges today has packaged assets that either generate no returns (BTC) or actually lose money once you account for the dilution from tokens issued to maintain chain operations. Ethereum generated $526 million in fees in 2025 but paid out $3.035 billion in staked issuance; Solana generated $680 million while paying $3.936 billion. Hyperliquid generated $857 million in fees.

The definition of "revenue" here needs to be clarified. For Hyperliquid, revenue = service fees minus 1% HLP treasury share (3% before August 30, 2025), with 99% flowing into the Assistance Fund for repurchase and destruction: $857 million in fees corresponds to $837 million in revenue. For Ethereum and Solana, the comparable metric is fees minus staked issuance, as these chains cannot operate without staked issuance; validators must pay with tokens. This is a real operating cost, and both chains are negative at the time of writing. Hyperliquid's $312 million staked issuance comes from pre-allocated reserves, not from exchange revenue, so it does not count in this metric. On an adjusted basis ($545 million), Hyperliquid is the only protocol with positive cash flow.

This gap is directly reflected in the asset and liability statements of DAT companies. BMNR's average buy-in cost for ETH is $2826, while Forward Industries’ cost for SOL is $232. Both are currently stuck.

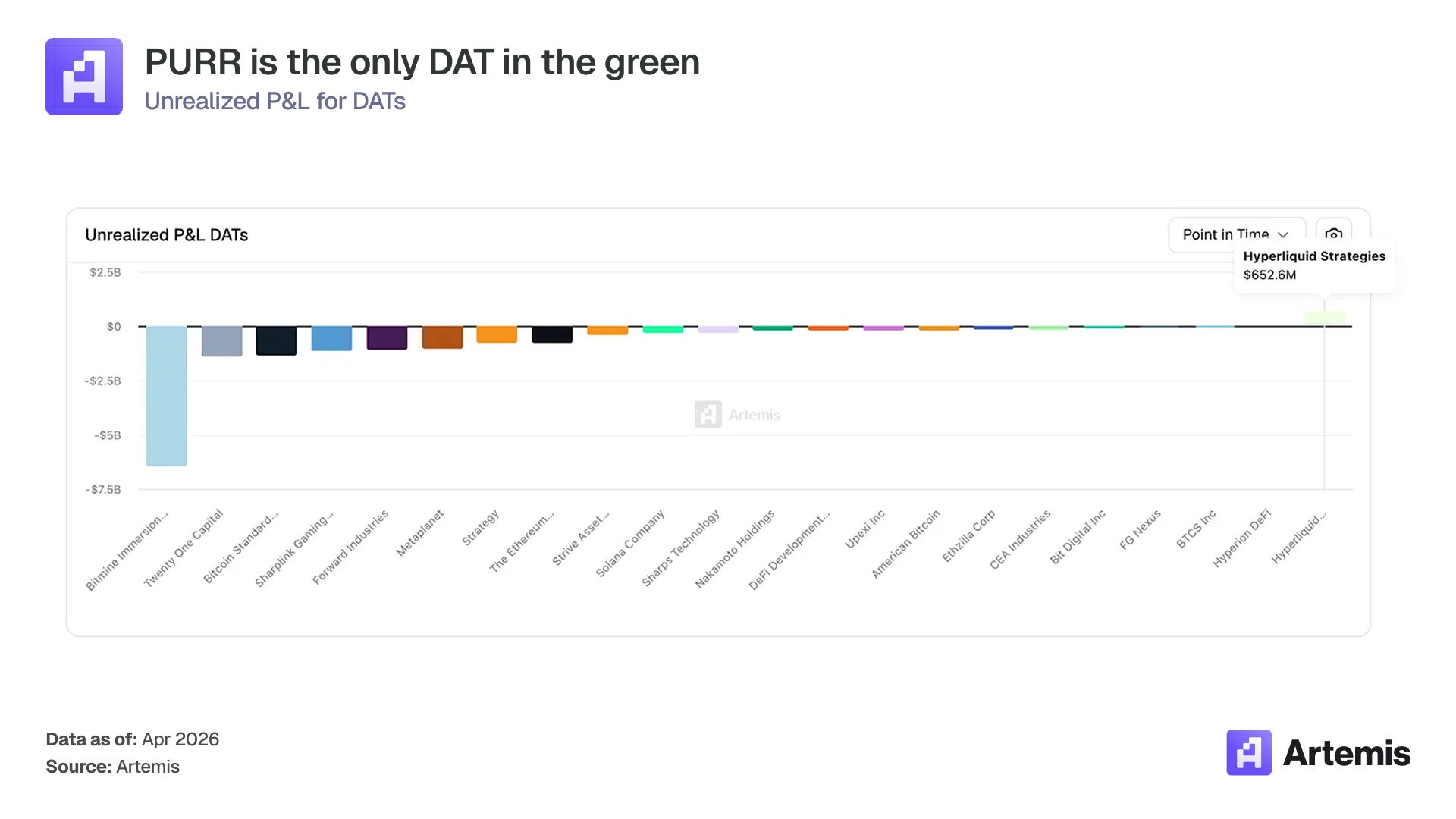

Caption: Comparison of unrealized gains and losses among various cryptocurrency treasury companies: Only PURR's HYPE holdings have substantial unrealized gains, around $600 million.

PURR is the only DAT company with substantial unrealized gains, with HYPE holdings approximately earning $600 million. The underlying assets not only generate profits but are also appreciating.

Five Growth Factors Amplifying This Advantage:

- HIP-3: Turning Hyperliquid into a token listing platform. After launching in October 2025, any developer can deploy permissionless perpetual contracts on any asset by staking 500,000 HYPE: commodities, stocks (China, South Korea, Japan), forex, alternative assets are all acceptable. This transforms HL from a cryptocurrency marketplace into a universal token listing layer. During the Hormuz Strait crisis, TradeXYZ's crude oil market deployed on HIP-3 processed a nominal trading volume of $305 million over a weekend; the correlation coefficient R² between cross-asset weekend prices and traditional market reopening prices was 0.785 (Blockworks' Shaunda calculated). The total addressable market (TAM) of available listing targets expands from $3 to $5 trillion in crypto derivatives to over $100 trillion in the global derivatives market. Each HIP-3 deployment requires a permanent stake of 500,000 HYPE, same for HIP-4. Once scaled, 20 markets will lock up approximately 10 million HYPE (2.1% of the circulating supply).

- DAT as a developer partner. At current prices, 500,000 HYPE is about $23 million. Most building teams cannot afford this. Large holders like PURR (18.8 million HYPE) are natural counter-parties: providing funding or jointly deploying for HIP-3/HIP-4 in exchange for market fee sharing. This creates an income line and ecological influence that cannot be replicated by individual HYPE holders.

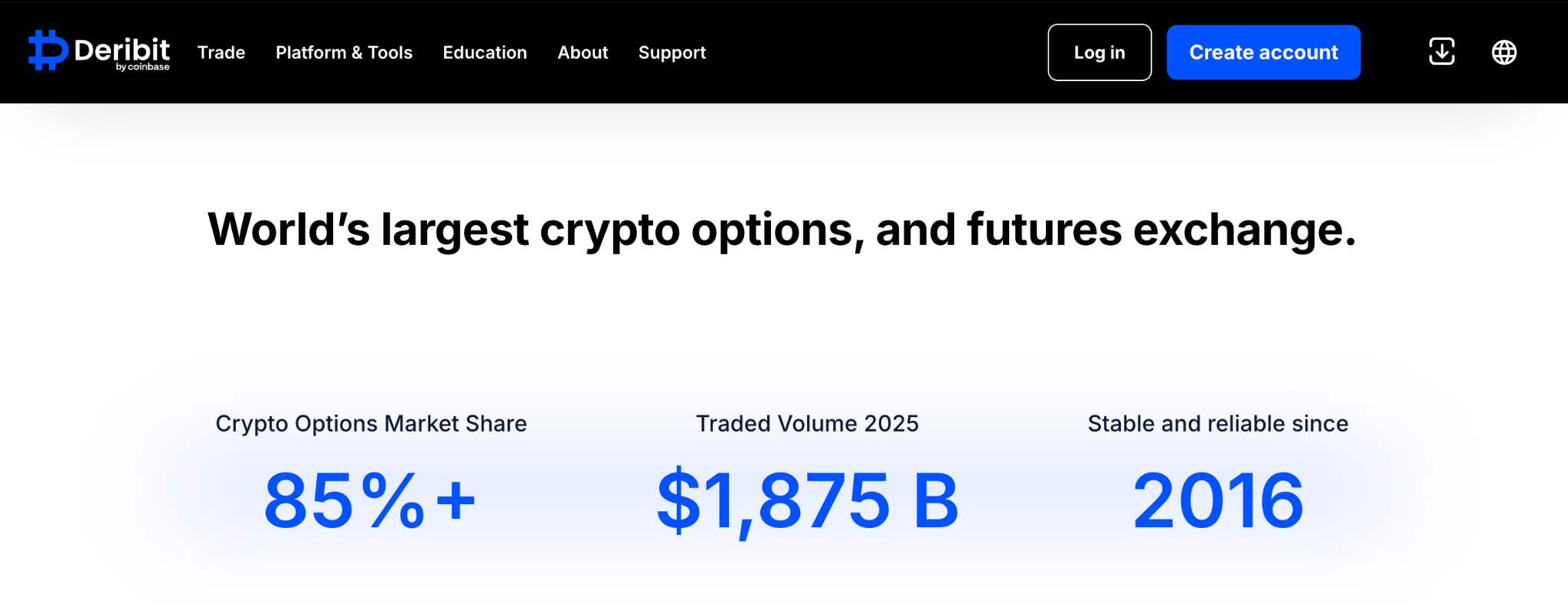

- HIP-4: Options and event contracts. The testnet will launch in March 2026, with the mainnet aimed for Q4 2026. Deribit, acquired by Coinbase, reported nominal options trading volume exceeding $18.75 trillion in 2025, accounting for over 85% of the entire market (about $22 trillion). Options currently account for only 3% of crypto derivatives (Coinglass data indicates the total for crypto derivatives is $85.7 trillion). If on-chain options can achieve a penetration rate of 15%, with HL capturing half, that's $165 billion in trading volume × approximately 8 basis points (options spread is wider than perpetual contracts, Deribit charges 12 basis points) = $135 million in annual service fees. The baseline model assumes starting at $50 million in 2026, rising to $130 million by 2030. The prediction market's event contracts will open the second income stream for HIP-4 (Polymarket's annual service fees are approaching $700 million).

Caption: Deribit options market data: 2025 total nominal options trading volume exceeds $18.75 trillion (source: Deribit)

- Builder Codes: A distribution channel with negative customer acquisition costs. Currently, about 40% of HL's daily active users are accessed through third-party front ends (Phantom being the largest). For every transaction routed through third-party front ends, developers receive a share of the fees, totaling over $40 million paid (data from Dwellir). Compared to Coinbase's customer acquisition cost of $400 to $600 per deposit account, HL has negative acquisition costs. This is why the model anticipates perpetual trading volume will rise from $29 trillion in 2025 to $52 trillion in the 2030 baseline scenario. The distribution layer is outsourced.

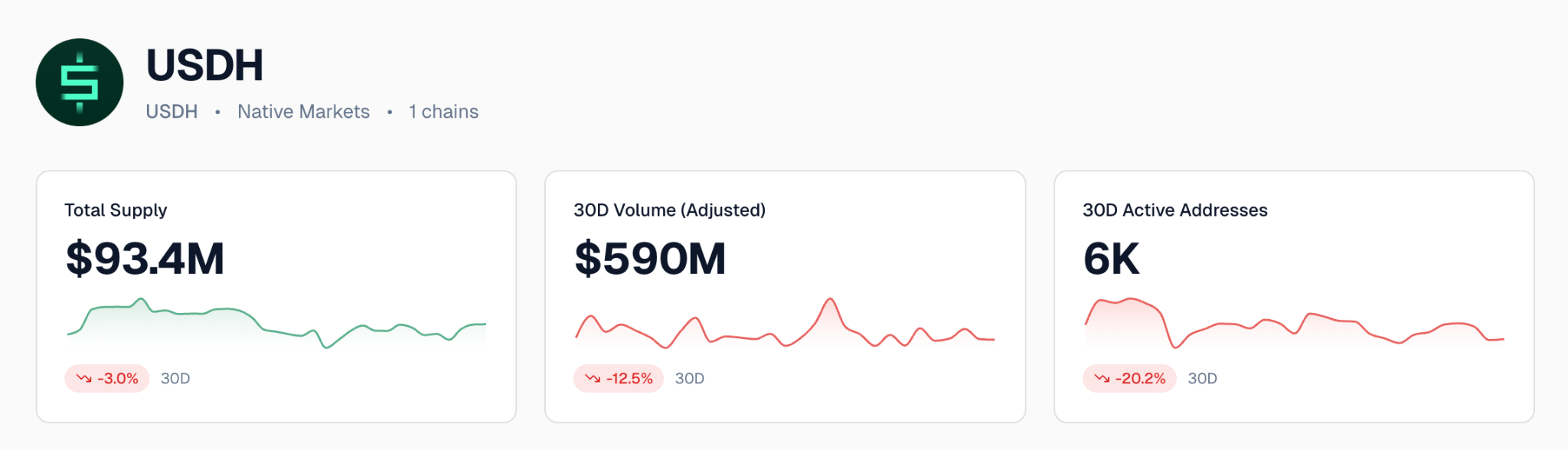

- USDH: Native stablecoin carrying fee-sharing. Native Markets obtained the issuance rights for USDH in September 2025. The reserves are managed in a fund by BlackRock, with 50% of reserve income flowing into the Assistance Fund.

At current supply levels (around $93 million) and a 3.7% US Treasury yield, USDH contributes approximately $1 million annually to the Assistance Fund for repurchase. When supply reaches $2 billion to $5 billion, this corresponds to $4 million to $10 million annually. Moreover, HIP-4 options may only support trading with USDH, which is a significant tailwind for Native Markets' stablecoin.

Caption: Comparison of stablecoin supply scales (source: Artemis Stablecoin Dashboard)

All these expansions do not require Hyperliquid to hire more staff. Every growth line (HIP-3 token listings, HIP-4 options, Builder distribution, USDH liquidity) is outsourced to external teams, allowing them to bear the risks of token listings and distribution in exchange for fee-sharing. The eleven-member core team is only responsible for writing protocols and fee pipelines. This is a platform scaling model: throughput, token listing targets, and frontend all grow without increasing headcount.

Argument Two: Buying This Shell at Cost Price

Strategy’s playbook is to issue shares at a premium, exchanging cash for BTC, and calling it financial engineering. The issue is that once the premium disappears, the mechanism reverses, and today the entire DAT sector is in this position (Strategy's price has dropped from 6 times to 1.15 times). PURR operates in the opposite direction: its stock price is around 1.12 times NAV, and the $30 million repurchase plan is only activated when the market prices PURR below the net asset value of its held tokens. For every dollar spent on repurchasing below NAV, it mechanically raises the corresponding number of HYPE tokens per share. This mechanism works in both directions. Below NAV, management repurchases stock, increasing the number of HYPE represented by the remaining shares. Above NAV, they can issue new shares at a premium, using the money to buy more HYPE, which similarly increases the number of HYPE per share. Both directions accumulate value for existing shareholders.

Other DAT companies do not have this mechanism. Strategy, BMNR, and Forward Industries all issue shares to buy tokens, but when premiums compress, they do not execute any repurchase actions. Shareholders are diluted when the price rises, and get nothing back when it falls.

Buying HYPE directly also has several advantages: no management fees at the company level, no dilution risks from equity financing, no regulatory risks targeting PURR's management, enjoying 100% of the token's upside. The options of staking and airdrops are only available to direct holders.

However, PURR offers four things that direct purchases of HYPE do not provide:

- Automatic appreciation without extra risks: The aforementioned repurchase is paid by existing cash on the balance sheet, with no margin calls, no liquidation risks, and holders do not have to take any action. Direct holders can leverage through perpetual contracts or lending but introduce counterparty and liquidation exposure.

- Regulatory moat: PURR and HYPD are currently the only two publicly listed NASDAQ vehicles with HYPE exposure. Any enforcement actions against Hyperliquid's no KYC operations will only push institutional demand toward this shell.

- Zero obligations: no debt repayments, no forced sales, no preferred stock.

- Tax efficiency: PURR is taxed as a regular stock. Those holding for more than a year are taxed at long-term capital gains (federal maximum 20%), can be placed into IRA and 401(k) accounts for deferred or tax-free growth, and can harvest tax losses alongside other stock positions. Direct HYPE holders must tax each time they receive staking rewards as ordinary income (maximum 37%), with no tax-advantaged retirement accounts available, and IRS guidance on airdrop cost basis remains undecided. For investors in the highest US tax brackets, this shell roughly halves the tax burden.

Each "circulating HYPE" generates $1.76 in revenue from the underlying exchange ($837 million ÷ 477 million circulating supply. This metric was introduced by Artemis in August 2025 in collaboration with Pantera Capital).

Valuation and Scenarios

Valuation is derived in two steps: first, pricing HYPE based on fundamentals (2030 expected revenue × price-to-earnings ratio ÷ circulating supply), then translating the target mNAV into the price of each PURR share.

HYPE Valuation Scenarios

HYPE is priced based on revenue (fees × 99% after HLP is deducted) multiplied by the terminal price-to-earnings ratio:

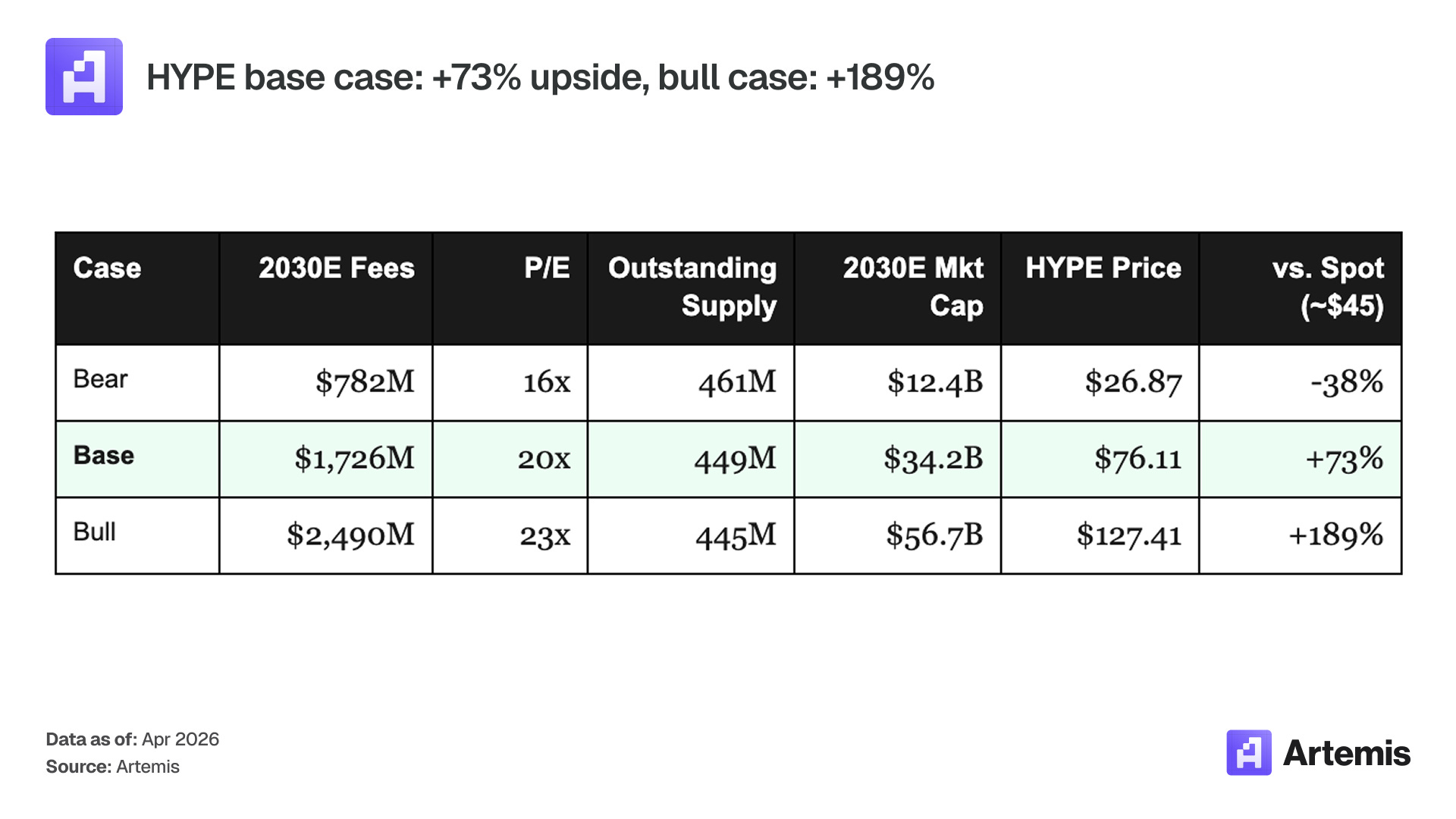

Caption: Three scenarios for HYPE valuation in 2030: Baseline $76 (20 times price-to-earnings ratio), optimistic $127, pessimistic $27 (16 times price-to-earnings ratio).

PURR Valuation Scenarios

The formula to translate HYPE scenarios into PURR is: Adjusted NAV per share = (18.8 million HYPE × price + $112.6 million cash − $95.8 million deferred tax burden + $4.5 million adjustments) ÷ 150.8 million fully diluted shares, then multiplied by target fully diluted mNAV. Historically, DAT stocks with productive underlying assets have seen their NAV multiples reprice in up cycles to 1.1 to 2.0 times, with the sector norm being 1.0 times.

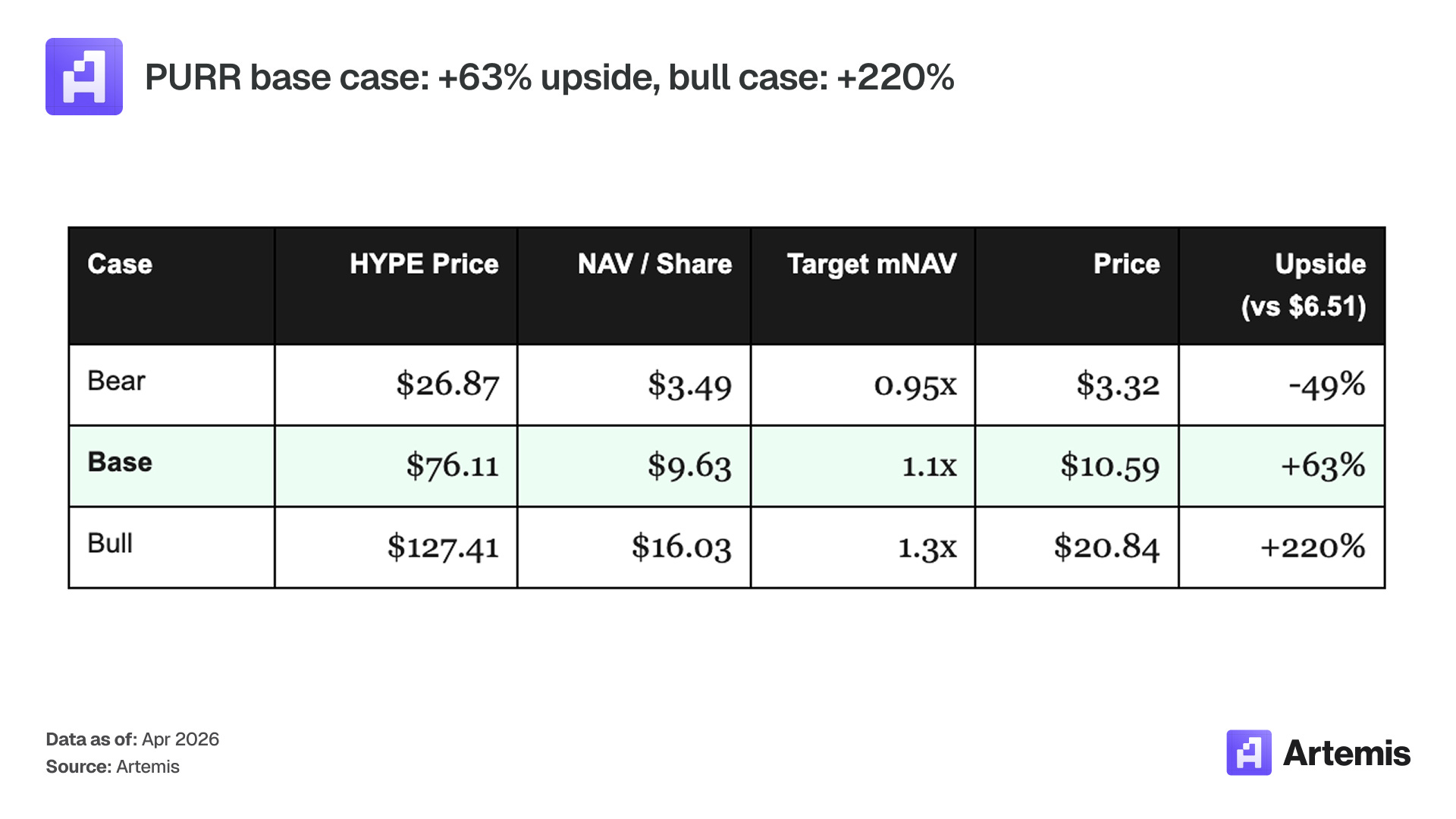

Caption: Three scenarios for PURR's valuation in 2030: Baseline $10.59 (+63%), optimistic $20.84 (+220%), pessimistic $3.32 (-49%).

Baseline scenario: HYPE reaches $76 by 2030, each adjusted NAV $9.63, valued at 1.1 times NAV corresponds to a stock price of $10.59, five years +63%.

Optimistic scenario: HYPE reaches $127 by 2030, adjusted NAV $16.03, revalued at 1.3 times, corresponding to $20.84, +220%.

Pessimistic scenario: HYPE compresses to $27, adjusted NAV falls to $3.49, mNAV slides to 0.95 times, corresponding to $3.32, -49%. The baseline scenario has an annualized return of about 10%, but the distribution is asymmetric: the downside is supported by zero debt and a protocol still capable of generating $782 million in service fees, while the upside benefits simultaneously from HYPE appreciation and mNAV revaluation.

Management and Share Structure

PURR is a balance sheet company. Its sole job is capital allocation: when to buy HYPE, when to repurchase shares, when to utilize equity lines, and when to do nothing at all. The team responsible for making these decisions collectively has over 80 years of experience in capital markets, bank balance sheet management, and exchange infrastructure. Paradigm is the cornerstone investor in this SPAC, the largest crypto-native fund in the world (managing $12.7 billion). D1, Galaxy, and Pantera complete a shareholder roster that bridges traditional finance and crypto. Bob Diamond’s institutional connections also serve as a distribution channel, catering to those who want HYPE exposure but cannot handle digital token custody or complex crypto taxes.

- Bob Diamond (Chairman): former CEO of Barclays, co-founder of Atlas Merchant Capital

- David Schamis (CEO): co-founder of Atlas Merchant Capital, former partner at JC Flowers

- Eric Rosengren (Director): former President of the Boston Fed (2007-2021)

- Larry Leibowitz (Director): former COO of NYSE, operating partner at Atlas Merchant Capital

Cornerstone investors include Paradigm, D1, Galaxy, Pantera.

Risk Factors

1. HYPE Price Retracement

PURR is a leveraged position on HYPE's price. A crypto bear market would compress trading volume, fees, and repurchase pools. The pessimistic scenario mimics this situation: TAM is stagnant at $85 trillion, HL’s market share is steady at 3%, fee rates slide to 2.3 basis points, price-to-earnings ratio drops to 16 times, corresponding to HYPE at $27 and PURR at $3.32 (-49%). The circulating supply is approximately 477 million; the pessimistic scenario assumes that the team's token liquidation rate is 35% from 2026 to 2027.

Mitigation: Zero debt means no forced sell-off. Even in a pessimistic scenario, Hyperliquid can still generate $782 million in fees and $774 million in profits, while the amount repurchased and destroyed continues to exceed the staking issuance, making the token remain deflationary (net destruction of about 23 million tokens annually). The $1 billion equity line is optional, not mandatory.

2. Regulatory Enforcement Against Hyperliquid

Hyperliquid operates without KYC. The Futures Industry Association has formally complained to US regulators, demanding enforcement against offshore perpetual contracts accessed by US residents. Any adverse enforcement actions would directly compress HYPE. Extending HIP-3 to traditional financial assets (silver, crude oil, stocks) would increase regulatory exposure, and commodity perpetual contracts may attract CFTC scrutiny, exceeding the currently observed scope of crypto-special enforcement.

Mitigation: PURR itself is a fully compliant NASDAQ listed entity. Regulatory actions may instead push US institutional demand toward PURR as the approved way to hold economic rights to HYPE.

3. Equity Financing Line Dilution

The $1 billion equity line can be activated when HYPE drops, but issuing shares at the wrong price would dilute existing shareholders. In the pessimistic scenario where HYPE is $27, PURR's adjusted NAV is $3.49, and issuing shares would mean pricing below $6.51 of the current price.

Mitigation: This line is optional and completely decided by management. The current posture is to repurchase rather than to issue new shares. By early February 2026, the $30 million repurchase plan had already executed $10.5 million, repurchasing approximately 3 million shares, reducing the fully diluted equity to 150.8 million shares. The shareholder structure led by Paradigm has no incentive to dilute itself.

4. DAT Premium Compression

Any premium relative to NAV that appears in a rising market will quickly compress once sentiments reverse. Strategy's 6 times mNAV premium fell to 1.15 times in less than 12 months. In an optimistic scenario, PURR could be revalued to 1.3 times NAV ($20.84); if sentiment reverses and the multiple compresses to 1.1 times, the upper loss would be the difference in mNAV.

Mitigation: PURR's mNAV today is 1.12 times. Compared to Strategy's peak premium of over $5 per dollar, PURR's premium is 12 cents. The asymmetry is upward: a 1.3 times valuation in a bull market is merely moderate, as historically, DAT stocks with productive underlying assets have approached 2.0 times or more. At 1.0 to 1.1 times, the value of this shell is simply the underlying asset itself.

Disclaimer: This article is for informational purposes only and does not constitute investment advice, financial advice, trading advice, or any form of recommendation. The views expressed are solely the author's opinion and should not be regarded as a recommendation to buy, sell, or hold any asset. The author or related entities may hold positions in the assets discussed. You should conduct your own research and consult appropriate financial professionals before making any investment decisions.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。