Written by: DD Didi./

In a bear market, many people choose to invest their money.

However, in the current environment, the collapse of DEFI projects has become the norm.

If you do not understand what kind of magic the project team is playing, you are just meat on their chopping board.

Therefore, this time I want to start from the very basic logic, and we will learn about the underlying options in DEFI.

Table of Contents

1. How humans first bought a choice for the future

2. A piece of paper, how can it trade the future

3. When do people need options

4. Call, Put, Buyer, Seller

5. From Wall Street to the crypto world: IV, Greeks and the true core of option risk

1. How humans first bought a choice for the future

Imagine this, time goes back thousands of years to the ancient Middle Eastern desert.

The protagonist of the story is named Jacob. He traveled long distances to his uncle Laban's house and fell in love at first sight with Laban's youngest daughter Rachel. Jacob really wanted to marry Rachel, but at that time he was a broke fugitive and couldn't come up with the hefty bride price required by society.

If following the usual spot trading (paying in cash for immediate delivery), Jacob had no qualification to discuss this marriage. Moreover, if he spent a few years saving money, the beautiful Rachel might already be promised to other wealthy suitors.

Faced with the huge risk of "the future full of uncertainty," what should Jacob do?

He proposed to Laban: "I am willing to work for you for free for seven years to earn the right to marry Rachel in seven years."

15 One day, Laban said to him: "Although we are relatives, I can't let you work for me for nothing. Tell me, what do you want as your reward?" 16 Laban had two daughters, the older was named Leah, and the younger was named Rachel. 17 Leah had weak eyes[a], while Rachel was beautiful and attractive. 18 Jacob loved Rachel, so he said to Laban: "I will work for you for seven years, please give Rachel to me." 19 Laban said: "It is better to give her to you than to another man; you stay here!" 20 Jacob worked for Laban for seven years for Rachel. Because he loved Rachel, those seven years seemed like just a few days to him.

Laban agreed. Both parties entered into a contract against time and the future.

This is actually the four core elements of an option

Buyer: Jacob.

He is the one who wants to control the future.

Seller: Laban.

He received benefits and promised to fulfill obligations in the future.

Underlying Asset:

The right to marry Rachel. In modern times, this can be stocks of Bank of America, Bitcoin, or gold.

Premium:

Seven years of free labor. In order to "buy this right," Jacob had to pay the cost upfront. This is like the premium we pay for insurance; once paid, it cannot be returned, but what we gain is future protection.

Expiration Date:

In seven years. The contract specifies the exact time for fulfilling the promise.

What problem did Jacob solve through this contract?

He used his current labor (premium) to lock in a future price and right, eliminating the risk of Rachel marrying someone else during those seven years. This is the most charming aspect of options:

It gives people the ability to fight against the uncertainty brought by time. The earliest DEFI collapse: Counterparty Risk

The interesting part of this story is that it also includes the most primitive DEFI collapse event, where the project party secretly switched people.

When the seven-year term was up (the expiration date arrived), Jacob was ready to exercise his right (to marry Rachel). However, the sly seller Laban actually defaulted on the wedding night! He secretly swapped Leah for Rachel to marry Jacob.

25 The next morning, Jacob found out that he married Leah and said to Laban: "What have you done to me! Did I not serve you for Rachel? Why did you deceive me?" 26 Laban said: "According to local customs, the younger sister cannot be married before the older sister. 27 After the seven-day marriage period is over, I will give you Rachel too, and you will work for me for another seven years."

This is counterparty risk, where the other party to the contract does not honor their commitment, resulting in the contract not being fulfilled on time. This is the earliest DEFI collapse.

2. A piece of paper, how can it trade the future

In Jacob's case, he locked in a future commitment with seven years of labor. The mechanism of modern financial markets is to convert this verbal commitment into standardized contracts, which is a string of code in computer systems. As for why a contract can be used to trade the future and even cause prices to fluctuate wildly, we can understand it through the everyday action of putting down a deposit on a house.

Understanding the essence of options through house deposits

Suppose someone is interested in a downtown property worth 10 million. There are rumors that a subway station might be announced in the area next month. If the subway station is confirmed, the property price may soar to 15 million; if the rumor is false, the price may drop to 8 million.

The buyer lacks sufficient funds or is unwilling to bear the risk of a price drop. Therefore, he proposes to the homeowner: first pay 100,000, which is non-refundable. In exchange, the homeowner must provide a contract promising that within three months, regardless of how much the price rises, the buyer has the right to purchase the property for 10 million.

The homeowner considers the current market situation and believes that 100,000 is guaranteed cash income. Even if the buyer decides not to purchase after three months, the house still remains and the 100,000 is already in pocket, so he agrees to sign. This model is a standard call option transaction in the financial market.

Why does this contract have value?

Suppose a month later the subway station is confirmed to start construction, and the property price skyrockets to 15 million. At this point, this contract undergoes a radical change. According to the contract, the buyer has the right to purchase the property, which is now worth 15 million, for 10 million. As long as he executes the contract and resells the property, he can make a net profit of 5 million. This means that the value of this contract itself is at least 5 million.

This reflects two core features of options:

First, it separates rights and obligations.

Ordinary contracts have mutual obligations, but options are unilateral. The buyer has the right but no obligation, while the seller has the obligation but no right. If the subway is not built and the price drops to 8 million, the buyer can freely choose not to execute the contract, with a maximum loss of just the initial premium of 100,000. The buyer bears limited loss risk while retaining potential profit space.

Second, it allows participation in price fluctuations without holding the asset, creating leverage.

The buyer did not actually use 10 million to buy the property, but instead controlled the price increase of a 10 million asset with a 100,000 contract. The actual return rate of buying the property for a profit of 5 million is 50%, but through options, using 100,000 to earn 5 million yields a return of 50 times. This illustrates why options have the remarkable characteristic of high leverage with a small investment.

3. When do people need options

Continuing the previous question, since the buyer enjoys limited losses and unlimited profits, why are there still people willing to assume the potential infinite risks of being a seller in the market? The answer lies in participants having distinctly different financial plans and needs when facing market uncertainty.

The operation of the options market is primarily driven by three motivations: hedging, speculation, and creating extra income.

The first demand is hedging, which is essentially the concept of buying insurance.

Suppose you hold a large amount of cryptocurrency spot in the exchange. You are optimistic about the long-term development of these assets but worried that short-term changes in the overall economy or regulations may lead to a sharp market pullback. Directly selling the spot would miss the long-term increase, but holding on bears the risk of significant asset depreciation.

At this time, you can choose to buy a put option. This contract grants you the right to sell your assets at an agreed price at a future point in time. If the market crashes, while your current assets may show a paper loss, the put option you hold will greatly appreciate, just enough to compensate for the loss on the spot. Conversely, if the market continues to rise, your maximum loss will only be the premium paid for the contract, while your current holdings still enjoy the benefits of the rise. This is like buying a price decline insurance for your investment portfolio, using a fixed cost to secure downside protection.

The second demand is speculation, which is to amplify potential returns through leverage with manageable risk.

For traders who do not want to invest a large principal to buy spot, options provide extremely high capital efficiency. For example, if they observe that a certain blockchain network (such as the Base ecosystem) is about to undergo a major upgrade, which they expect the associated tokens will experience explosive growth. Going directly into the spot market requires substantial capital investment, whereas through buying a call option, they only need to pay a relatively small premium to control equivalent assets and participate in the upside profit.

If the market judgment is correct, the increase in contract value may be several times that of the spot; if the judgment is wrong, the maximum loss is limited to the initial premium paid. Unlike futures contracts, the option buyer does not face the pressure of a margin call due to insufficient margin, making it a powerful tool for defining absolute risk boundaries.

The third demand is to create income, which is the main reason why sellers are willing to assume obligations.

In the financial market, acting as an option seller is akin to running an insurance company. Statistically, the vast majority of options contracts expire worthless, ultimately going to zero. The seller's business model is to continuously collect premiums paid by buyers by taking on small probabilities of extreme risk.

Additionally, many large institutions or long-term holders use covered call strategies. If they already hold a substantial amount of spot and assess that the price will only stabilize in the short term without spiking, they will choose to sell call options. As long as the asset price does not exceed the agreed exercise price at expiration, the seller will earn this premium reliably. In a sideways market phase, this practice effectively creates additional cash flow from idle assets.

The options market is woven together by these three demands. Hedgers seek protection, speculators seek leverage, while sellers provide liquidity and earn value from the passage of time. Understanding the fundamental motives of the participants allows us to further unpack the four basic aspects of trade in the contract, along with their rights and obligations.

4. Call, Put, Buyer, Seller: The rights and obligations of options

Entering the options market, the four basic quadrants often confuse people. In fact, as long as we separate the types of contracts and the roles of participants, the underlying logic becomes very clear. The entire options market's endless variety is formed by the combinations of two types of contracts and two types of identities.

First, distinguish the types of contracts. Calls are call options, granting the holder the right to "buy" the underlying asset at the agreed price in the future. This can be seen as a pre-purchase order. Puts are put options, granting the holder the right to "sell" the underlying asset at the agreed price in the future. This can be seen as a policy or a price protection acquisition certificate.

Next, distinguish the roles of the participants. The buyer pays the premium to obtain the rights conferred by the contract. The buyer holds absolute initiative, and when the time comes, can decide whether or not to execute the contract. The seller receives the premium and bears the obligations set forth in the contract. The seller is in a passive position, and once the buyer decides to execute, the seller must comply unconditionally.

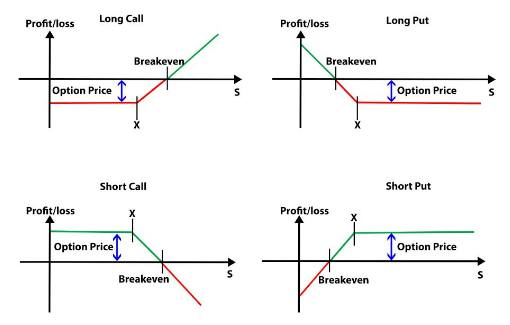

Crossing these two aspects leads to the four basic strategies of options:

Buy Call (Long Call)

The investor pays the premium, obtaining the "right" to buy the underlying asset at the agreed price at some future time, with a bullish market outlook.

Sell Call (Short Call)

The investor sells call options, collects the premium, and assumes the "obligation" to possibly "sell" the asset at the agreed price in the future.

Buy Put (Long Put)

The investor pays the premium, acquiring the "right" to sell the underlying asset at the agreed price in the future, typically used when expecting a market drop or hedging against asset depreciation risk.

Sell Put (Short Put)

The investor sells put options, collects the premium, and bears the "obligation" to potentially "buy" the asset at the agreed price in the future.

1. Buy Call: Strategy for expecting a significant rise

This is the most intuitive way to go long. When a trader is very optimistic that an asset will surge in the future but does not want to invest the full amount, they will buy a Call. For example, expecting an asset will rise from the current price of 100 to 150. The trader can pay a premium of 5 to buy a Call with an exercise price of 110. If the price indeed rises to 150, the trader has the right to buy at 110, accounting for the 5 premium, to net a profit of 35. If the price falls below 110, the trader can forgo execution, with a maximum loss of only 5. This is a typical scenario of limited risk and unlimited profit.

2. Buy Put: Strategy for expecting a substantial drop or hedging

This is akin to insuring an asset. When a trader expects the market to crash or wants to protect their current spot assets, they will buy a Put. Suppose they hold assets worth 100, worried about a significant drop next month. The trader pays 5 to buy a Put with an exercise price of 90. If the market crashes to 50, they still have the right to sell the assets for 90. The value of the Put will soar as the price of the underlying asset declines. This too is a strategy with limited risk and extremely high profit potential.

3. Sell Call: Strategy expecting no rise

This is one of the premium-earning strategies, typically used in a market where prices are anticipated to stabilize or gently decline. The seller collects the premium paid by the buyer and commits to selling the asset to the buyer at the agreed price if the price exceeds that exercise price. If they sell a Call without holding the underlying asset (known as naked selling), once the asset price skyrockets, the seller faces an infinite loss risk. Therefore, institutional investors usually combine it with owning the spot, using a covered call strategy to enhance additional income during sideways markets.

4. Sell Put: Strategy expecting no significant drop or targeting an entry price

This is a commonly overlooked strategy but widely applied by many value investors or quantitative traders. When they expect prices to not drop significantly or want to buy an asset at a lower target price, they will sell a Put. For example, if the current asset price is 100, a trader believes that 80 is an excellent entry point. They can sell a Put with an exercise price of 80 and immediately collect the premium. If by expiration the price does not drop below 80, the contract expires worthless, making the premium profit. If the price falls below 80, the trader must fulfill the obligation to buy the asset at 80, which aligns perfectly with their original plan to build a position at 80, and since they have already received the premium, the actual purchase cost will be lower than 80.

These four quadrants form the foundation of all complex derivative financial products. Buyers exchange limited risk for leverage and choice freedom; sellers trade extreme risk for fixed income from the passage of time.

However, in the real trading world, the pricing of contracts is not simply about rising or falling prices. The value of an option also involves the degree of market panic and the passage of time. This introduces the core elements of quantitative models in Wall Street and crypto, which are critical and often a threshold that many advanced traders must cross.

5. From Wall Street to the crypto world: IV, Greeks and the true core of option risk

When the sophisticated financial tools of options were transitioned from Wall Street trading floors to the crypto market, which operates year-round with extreme price fluctuations, the game rules changed fundamentally.

In a traditional stock market, investors may wait a season for a company’s earnings report, with market volatility being relatively predictable. However, in crypto, sudden news over a weekend can lead to Bitcoin or Ethereum experiencing volatility of more than ten percent. In such extreme environments, merely guessing price direction is insufficient for executing quantitative arbitrage or building defensive positions.

If you imagine yourself standing in front of a massive blackboard trying to dissect all the variables that affect option prices, you would find that the pricing model for options is essentially a set of multi-dimensional calculus equations. To analyze these variables, financial scholars invented a system of indicators known as the "Greeks."

The true starting point of this system is Implied Volatility (IV).

Implied Volatility: Pricing fear and greed

Before understanding the Greeks, one must first grasp IV. IV is not the historical volatility from the past, but rather the collective consensus among market participants regarding future volatility.

When the market anticipates upcoming large movements (for example, a major upgrade on a Layer 2 network is about to happen, or the Federal Reserve is preparing to announce rate cuts), everyone rushes to buy options for speculation or hedging. This buying behavior drives up the prices of the contracts. The elevated price calculated in the inverse pricing formula yields the IV.

In simple terms, IV is the fear and greed index of the options market. The higher the IV, the more the market believes the future will be unstable, thus making the premiums more expensive; the lower the IV, the cheaper the premiums.

The first level risk dashboard: Delta, Theta, Vega

With the concept of IV, we can now open the dashboard for controlling options risk. The three core indicators correspond to price, time, and volatility.

Delta represents price sensitivity, or directional risk. It describes how much the price of the option will change when the price of the underlying asset changes by 1 unit. You can think of Delta as the speedometer in a car. If your call option's Delta is 0.5, that means for every 1 dollar increase in Bitcoin, the value of your contract will increase by 0.5 dollars.

Theta represents time decay, or time risk. Options have a storage period, and Theta measures how much value your contract will lose over a day, holding other factors constant. For buyers, Theta is like a merciless meter running down every day, just like holding a melting ice block; but for sellers, Theta is automatic interest credited every day.

Vega represents volatility sensitivity, or emotional risk. It gauges how much the price of the contract will change when the implied volatility (IV) changes by 1%. In the crypto sphere, Vega's impact often overrides Delta. Sometimes you are correct in your directional view, and Bitcoin does rise, but due to market sentiment calming from extreme euphoria to stability, the decline in IV caused by Vega can eat into the profits brought by Delta, which is known as "volatility crush" in Wall Street jargon.

Advanced tuning gears: Speed, Color, Ultima

If the financial market were affected only by the three variables mentioned, quantitative trading would be much too simple. The reality is that when market prices change, Delta, Theta, and Vega themselves also change. To address this dynamic variation, higher-order Greeks were developed.

To understand these higher-order letters, we first need to mention Gamma. Gamma is the acceleration of Delta. It measures how much Delta itself will change when the price of the asset moves by 1 unit.

Speed is the rate of change of Gamma. In physics, if Delta is speed and Gamma is acceleration, then Speed is jerk, measuring how fast Gamma itself changes as the price of the underlying asset continues to fluctuate. This is particularly important for managing extremely short-term positions subject to wild price jumps.

Color measures the impact of time on Gamma. As the expiration date of the contract draws closer, the value of Gamma will change. Color tells traders how their acceleration (Gamma) will change as each day passes.

Ultima is the third derivative concerning volatility. When IV changes, Vega will change, and the indicator measuring the rate of change of Vega is called Vomma. Ultima further measures how Vomma will change when IV changes again. These extremely small values are typically used only by institutions managing hundreds of millions of dollars, engaging in precise arbitrage of volatility curves.

Cross-dimensional ghosts: Vanna and Charm

In modern quantitative research, what truly captivates advanced traders are the cross-dimensional interactive effects of Greek letters, among which Vanna and Charm are the most famous.

Vanna measures the effect of changes in volatility (IV) on Delta. This may sound counterintuitive: why does a change in volatility affect my sensitivity to price direction? Because when the market panics (IV rises), those originally unattainable, extremely out-of-the-money options suddenly become "potentially realizable." This expansion of possibility pulls the entire Delta distribution of the investment portfolio. In extreme market conditions in crypto where liquidations occur in succession, Vanna often drives market makers to frantically buy and sell underlying assets to hedge risk.

Charm measures the effect of time passing on Delta, also known as Delta decay. As days pass, the chances of an out-of-the-money option that has no intrinsic value turning around diminish. Charm describes how this option's Delta will approach zero over time.

The true core of option risk

From the basic Delta to the complex Vanna, these letters reveal the ultimate truth of options trading: what you are trading is never a single-dimensional asset, but a four-dimensional space interwoven by price, time, volatility, and probability.

Novices die by direction (misreading Delta), veterans die by time (worn down by Theta), while experts often die by volatility (retaliated against by Vega and Vanna).

Of course, writing this article is not just about teaching everyone to hedge.

It is more about hoping to equip everyone with the ability to understand the deceptive plays of DEFI projects.

You want their interest.

They want your principal.

How to see through those complex structured products

and protect yourself

is the way to self-preservation in a bear market.

Of course, the complexity of options is hard to explain in just one article.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。