Written by: Sebastien Davies, Partner at Primal Capital

Translated by: Luffy, Foresight News

For nearly a decade, the global financial sector has been obsessed with building tracks like payment and transactional infrastructure. Discussions around digital assets have primarily focused on: the throughput of blockchain, the cryptographic security of decentralized applications, and the theoretical elegance of smart contract logic. This is the era of infrastructure, a time of crazily constructing "containers." From 2020 to 2024, the industry frantically built pipelines, vaults, and gateways, attempting to modernize the flow of value.

During this period, the development of the cryptocurrency market has been highly focused on infrastructure, as institutional participation would be impossible without it. We have built enterprise-grade custody platforms, standardized exchange APIs, on-chain compliance services, and addressed five core gaps: custody, trading, execution, utility of stablecoins, and regulatory reporting.

However, the industry now faces a fundamental truth of financial history: infrastructure is a necessary prerequisite for financial activity, but balance sheets determine who can capture economic value.

Simply having faster and more transparent tracks alone will not change the gravitational center of the market. Infrastructure solves the technical question of "how institutions participate," yet ignores a more critical issue: who captures the value.

In the heavy infrastructure era, value distribution still relies on traditional models: centralized market makers earn spreads, early holders enjoy appreciation, and validators receive transaction fees. This stage failed to create new balance sheet structures, thereby changing where deposits are held or fundamentally altering the structure of credit creation.

A common rebuttal to this is: "Tracks" are the core driving force of value because they lower entry barriers and achieve financial democratization, naturally pushing economic power to the margins. Supporters argue that open-source and permissionless technologies are themselves transformative forces. This is an intriguing narrative for the retail-dominated crypto-native world, but it does not withstand the test of institutional reality.

In mature financial markets, institutions care more about capital efficiency and risk-adjusted returns than cost efficiency. An institution will not move a billion dollars simply because of lower fees; it transfers funds because the balance sheet where that money resides can provide better returns or more efficient collateral utility.

Infrastructure merely makes entry possible; the balance sheet is the strategic asset that determines winner of the spread.

Financial history repeatedly proves that infrastructure is not the key to determining market power; balance sheets are. The rise of the Eurodollar market in the 1960s did not require new payment tracks or financial technologies, just the outflow of dollar deposits from the US banking system. Once these balance sheets migrated, a parallel dollar system emerged that was enormous and largely untethered from domestic US regulations.

We are now entering a new phase beginning in 2025: the reconstruction period of institutional balance sheets. The battlefield has shifted from the protocol layer to the liquidity allocation layer. The previous phase focused on building platforms, while the next phase focuses on the movements of participants and the flow of funds.

In 2024, a CFO, when choosing where to hold cash, could technically use mature custody facilities to hold USDC, but economically, traditional bank deposits with FDIC insurance and attractive interest rates would be more appealing. The infrastructure is ready, but balance sheets have not yet migrated. As the regulatory environment moves from abstract policy designs to concrete implementations, this reallocation becomes possible.

The next stage of cryptocurrency adoption is not determined by infrastructure, but by the flow of balance sheets.

The Gateway to Implementation

For most of the past decade, institutional participation has been limited, not due to a lack of imagination or technology, but because it has been impossible to integrate digital assets into regulated balance sheets. Institutions require more than just a usable wallet; legal clarity, specific accounting treatments, and strict governance structures are minimum requirements.

Without a recognized definition of "custody," and no clear compliance pathways, no regulated entity can bear the risk of a contaminated balance sheet. Large-scale adoption has fallen into a "waiting game": banks and asset management institutions are waiting for clear signals to confirm they can deploy funds without incurring fatal legal risks.

The era of policy debate has finally come to an end, replaced by the operational landing phase. The GENIUS Act, passed in May 2025, has become a decisive catalyst, establishing a national regulatory framework for stablecoin payments and ultimately providing legal basis for balance sheet allocation.

The act sets up a federal licensing process and requires stablecoins to provide 100% reserves backed by government-approved instruments, transforming digital assets from speculative curiosities into recognized financial instruments. In August 2025, the SEC concluded the long-running investigation into the Aave protocol without taking enforcement action, completely eliminating the regulatory shadow that suppressed institutional participation in DeFi.

The focus now shifts to regulatory details. In February 2026, the Office of the Comptroller of the Currency (OCC) published comprehensive proposed rules implementing the GENIUS Act, establishing a framework for "compliant payment stablecoin issuers." This is significant as it provides specific prudential standards covering reserve composition, capital adequacy ratios, and operational resilience, allowing Chief Risk Officers or asset-liability management committees to formally approve digital asset strategies. The GENIUS Act has embedded blockchain regulation into the governance structures of the largest financial institutions globally.

However, to understand why this transformation is occurring now, one must also recognize the inertia of balance sheets that defines institutional behavior. Banks operate under strict regulatory capital adequacy requirements; every dollar of risk-weighted assets must be backed by capital. If bank deposits flow into stablecoins, lending must be proportionally reduced to maintain those capital adequacy ratios. This is a painful and costly contraction, leading to a chain reaction throughout the economy. This also explains why the adoption speed of stablecoins has been so slow. Comprehensive technical integration takes six to eighteen months, while governance cycles like audits and board reviews take even longer to complete.

The current environment is entering a compounded acceleration period. Pioneers like JPMorgan, Citigroup, and Bank of America are beginning to roll out stablecoin settlement solutions, sending a clear signal to the market: the risk of getting left behind has replaced the risk of being early.

We are in a phase of competitive pressure; inter-industry participation has lowered the adoption risk for the entire sector. As these institutional constraints relax, pathways for liquidity to migrate from traditional systems to the programmable containers of the digital age have been opened. This transformation forces us to rethink the intrinsic ownership of capital, shifting attention to the "containers" that will underpin the next generation of global liquidity.

Where Liquidity Resides

To understand the magnitude of this transformation, it's essential to recognize the historical stability of financial "containers." In every monetary era, liquidity ultimately needs a home. This is not only a technical storage demand but also a long-term essential need for global safe short-term assets.

For centuries, liquidity has been highly concentrated within a few clearly defined structures: commercial bank balance sheets, central bank reserves, and money market funds. Each type of traditional container serves as an intermediary, capturing the economic value generated by the capital it holds.

This determines that the existence of financial intermediaries is to solve mismatches: the cash generated from global operations far exceeds the funds that can be immediately put to productive use, creating a permanent liquidity surplus that seeks a safe haven.

Traditionally, commercial banks absorb this surplus in the form of deposits, investing in long-term assets like mortgages and corporate loans to earn significant interest spreads. This net interest margin is a core indicator for commercial banks. Bank shareholders are the primary beneficiaries of this spread, while depositors receive only a small portion of the returns in exchange for liquidity and government-backed insurance.

Digital asset infrastructure has introduced a new type of "container" that directly competes for this capital. This economic reconstruction goes far beyond mere technical upgrades. As liquidity shifts from banks to stablecoin reserve pools or tokenized government bond funds, the entities capturing that yield undergo a fundamental change.

For instance, in the stablecoin reserve pool, issuers (like Circle and Tether) earn the spread between the yields of the underlying government bonds and the interest paid to token holders (typically zero). This essentially shifts the "housing of economic value" from the commercial banking sector to digital asset issuers.

Additionally, these new containers possess transparency and programmability that traditional structures cannot match. By March 2026, the market capitalization of tokenized government bond funds surpassed $11.5 billion, representing a structural evolution where the yields of underlying assets belong directly to the holders.

This creates a powerful economic incentive: senior finance executives no longer have to choose between the safety of banks and the returns of funds; they can hold tokenized funds that serve as yield-generating assets and fast settlement mediums. By redefining liquidity direction, digital infrastructure is not only building new tracks but is also creating a competitive market for the balance sheets that support the global economy.

Stablecoins Driving Capital Reallocation

Stablecoins represent the first large-scale migration of liquidity to new financial balance sheets, marking the transition of digital currency from a novelty to a core component of financial infrastructure.

The market size of stablecoins is nearing historical peaks, reaching $311 billion with annual growth rates of 50%-70%. This growth shatters the narrative of "just a speculative phenomenon." We are witnessing a genuine "reallocation of dollars": funds are moving away from traditional banking infrastructure and into programmable settlement systems.

The economic impact of this migration is particularly pronounced under the deposit substitution effect.

When a corporation or institutional investor transfers $100 billion from traditional bank deposits to stablecoin containers like USDC, the profitability of the banking system will suffer greatly. Under traditional models, this $100 billion can support bank lending, generating approximately $3 billion in net interest each year. When funds migrate to Stablecoin issuers' reserves, these earnings become disintermediated. Banks lose deposits, lending capacity contracts, and the spreads are instead captured by stablecoin issuers.

This shift has profound implications for credit creation and financial stability.

Research by Federal Reserve economists published at the end of 2025 emphasizes that high adoption scenarios for stablecoins could lead to a reduction in bank deposits by $65 billion to $1.26 trillion. This could reshape how credit supply is provided in the economy. Regional banks, which heavily rely on stable deposits to support local lending, are the most vulnerable to this migration. As depositors pursue the 24/7 settlement advantages of stablecoins, the appeal of the "in-transit funding spread" that banks have long relied on diminishes rapidly.

In response, the banking sector has shifted from skepticism to participation.

JPMorgan, Citigroup, and Bank of America announced the launch of their own stablecoin settlement infrastructure from late 2025 to early 2026, not to "disrupt" their own businesses but to maintain their importance as liquidity containers. These institutions recognize that future economic value will shift towards issuers of digital containers. By issuing stablecoins themselves, banks hope to capture the reserve yields that would otherwise flow to new entrants.

Of course, this large-scale cash reallocation is just the prologue. As new liquidity containers stabilize, the battlefield is shifting toward more complex collateral domains, as well as the leverage systems that underpin global finance.

Programmable Collateral

If the cash migration brought about by stablecoins is the first wave of change, then the migration of collateral represents a more fundamental reconstruction of the core leverage mechanisms in the financial system.

Modern financial markets essentially comprise a vast network of collateralized debt. In the U.S. repo market alone, the daily scale of securities lending reaches $2-4 trillion. However, this critical infrastructure remains hampered by traditional banks' "discrete settlement windows." In the current environment, collateral can only move during bank business hours, and the fragmentation of custody means that securities held by one bank cannot be used immediately to meet another bank's margin requirements. This friction results in capital being locked up inefficiently, unable to respond to real-time market fluctuations.

Tokenization transforms collateral from static, geographically constrained assets into programmable, highly liquid tools.

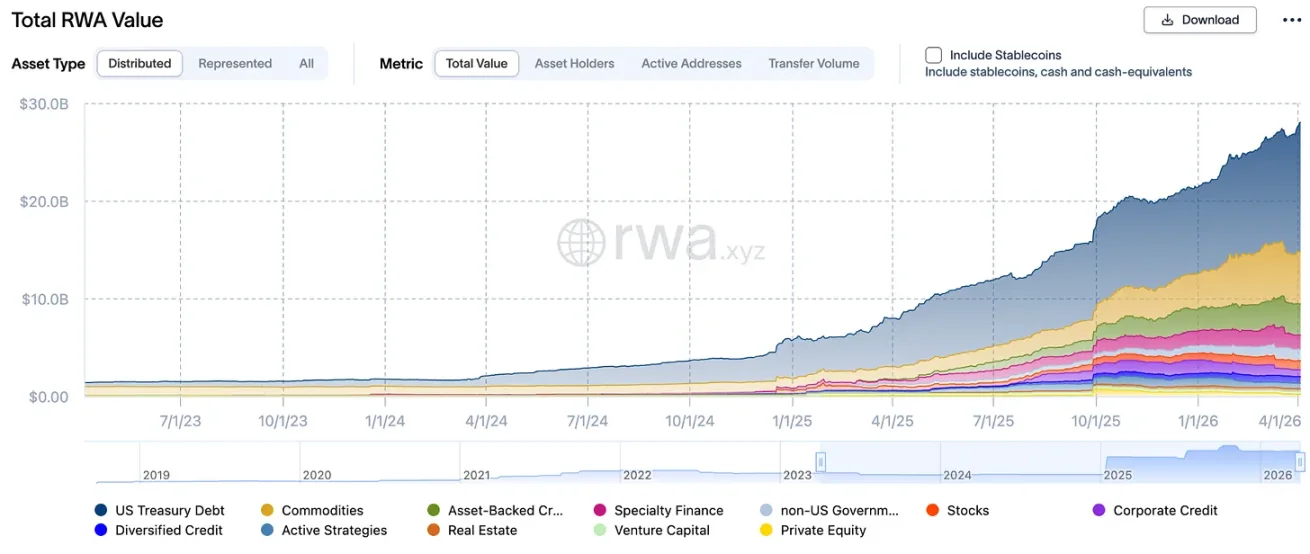

By converting real-world assets (RWAs) like U.S. Treasury bonds into on-chain tokens, institutions can transfer and settle these assets around the clock. The market is growing rapidly: as of April 1, 2026, the tokenized RWA market was approximately $28 billion in size, with tokenized government bonds accounting for nearly half. This growth is driven by institutional-grade products like BlackRock's BUIDL and Franklin Templeton's BENJI, allowing holders to earn a 5% yield from the underlying government securities while maintaining the liquidity and deployability of the tokens.

RWA Asset Value, Source: RWA.xyz

True innovation lies in collateral efficiency.

In traditional repo transactions, investors may need to accept significant discounts or wait several days to unlock and transfer securities between custodian banks. In contrast, tokenized collateral possesses composability. An institutional investor holding $100 million in BUIDL tokens can instantly borrow stablecoins at a 95% ratio on protocols like Aave, capturing tactical opportunities. The collateral does not need to leave the digital environment and is continuously revalued through automated price feeds, with any margin calls processed via real-time, automatic liquidations.

This shift transitions the "dealer economy" to the "protocol economy."

In traditional repo markets, large dealer banks act as intermediaries, borrowing at one rate and lending at another, earning spreads of around 50 basis points. In a tokenized ecosystem, collateral holders can match themselves in DeFi lending markets, using software as intermediaries to capture the entire spread. Although scaling to reach mass adoption will still take several years, this transformation could potentially shift billions of dollars in earnings from traditional trading dealers to protocol governance and asset holders.

The mechanism of tokenized collateral, through atomic settlement, dismantles the liquidity moats of large dealers. The institutional process broadly unfolds as follows:

- Tokenization: Highly liquid assets like U.S. Treasuries are digitally packaged (e.g., BUIDL), becoming 24/7 movable tokens.

- Instant Submission: Finance teams can submit tokenized collateral to lending protocols by 10 PM on Sunday night, without having to wait for wire transfer on Monday morning.

- Real-Time Valuation: Smart contracts revalue collateral market prices every few seconds through oracles rather than once a day, significantly enhancing loan-to-value ratios.

- Yield Retention: Investors continue to earn the yields of underlying government securities while their assets are occupied as collateral, achieving "yield stacking."

For corporate finance or asset management teams, this represents a fundamental revaluation of idle asset value.

Under traditional models, finance executives must hold significant amounts of low-interest cash buffers to deal with unexpected margin calls and operational needs. With tokenized collateral, this buffer can consistently be invested in yield-generating government bonds, as these assets can be liquidated in seconds instead of days. This eliminates the "liquidity discount" that has long been present in long-term assets.

The implications for the banking sector are equally profound.

Banks have long relied on the "in-transit funds" and intermediary spreads of the repo market for profit. As collateral becomes programmable and self-matching, this toll will vanish. This is also why institutional-grade pipelines like Anchorage Atlas Network and JPMorgan's internal tokenization project are so critical; they are attempts by financial institutions to build new barriers before facing competition from old barriers.

The transition from cash to collateral marks a shift in the financial system from a series of "discrete events" to a "continuous flow." Institutions that fail to adapt their balance sheets to this new flow rate will find their held capital increasingly static and increasingly costly.

What appears on the surface as an improvement in settlement speed is, in essence, a comprehensive reconstruction of capital allocation, valuation, and intermediation methods.

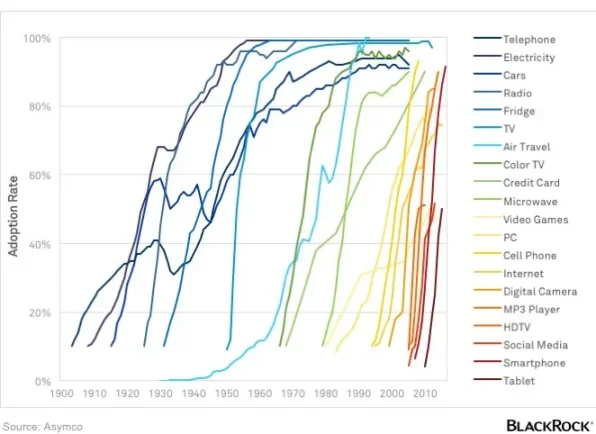

Adoption Rate S-Curve

The migration of institutional balance sheets is not an overnight disruption but a gradual absorption, ultimately accelerating into an explosion. This is a "Web 2.5" reality: blockchain technology is integrated into existing financial architectures rather than replacing them.

Institutional adoption is currently constrained by balance sheet inertia: regulatory capital requirements, risk committee approvals, and traditional technology systems are significant drag factors. Banks cannot simply flip a switch to transfer assets; they must maintain strict tier-one capital ratios to ensure that deposits moving into digital containers do not force a contraction in lending.

Despite these obstacles, the proliferation of digital asset infrastructure is progressing along a clear S-curve, similar to the decades-long adoption period of credit cards and the internet.

Between 2015 and 2024, the market was in a phase of experimentation and regulatory confusion, with growth suppressed by uncertainty. We have now entered a period of competitive pressure (2025-2026), with clearer regulations and standardized infrastructure. "You are not the first, but you cannot be the last" has become the core motivation for institutional CFOs. As more banks see peers participating in stablecoin settlements and tokenized government bond funds, the perceived risk of adoption has sharply decreased.

The current market size provides a foundation for accelerating growth: Fireblocks reached a yearly digital asset transfer volume of over $5 trillion, the institutional tokenized asset market is growing rapidly, and new system pipelines have reached production readiness. Infrastructure standardization allows banks to build on mature systems without needing to redevelop proprietary systems.

Looking forward to 2027 and beyond, several "policy levers" remain to further accelerate migration. If stablecoin issuers can access Federal Reserve master accounts directly, or if the interest restrictions on payment stablecoins under the GENIUS Act are relaxed through alliance "reward" mechanisms, the speed of deposits shifting from traditional bank books to digital containers could significantly accelerate.

The system is prepped to enter a positive feedback loop: more stablecoin liquidity attracts more DeFi applications, which in turn attract more institutional capital, ultimately forming a restructured financial landscape. The "competition of tracks" has ended, and the focus has fully shifted to the strategic management of balance sheets.

The Final Winners

The transition from the infrastructure era to the balance sheet era signifies that discussions of digital assets have moved from the technological margins to the core of the global macroeconomy.

For years, the industry assumed that building better tracks would inevitably lead to a better system. Now we understand: tracks are merely invitations; transformation only truly occurs when capital itself migrates.

The "race for tracks" has, in fact, been won by a standardized, institutional-grade technology stack: MPC custody, tokenized government bond funds, federal-regulatory stablecoin frameworks.

The new battlefield is: balance sheets holding global liquidity and collateral.

As we move towards 2027-2030, structural advantages will belong to those entities that can most efficiently manage these new "digital containers." As depositors increasingly value the 24/7 settlement and higher yield utility of stablecoins, commercial bank net interest margins will remain under pressure. Large corporations and institutional investors may shift their primary savings and finance functions towards DeFi and RWA markets, maximizing transparency of protocols to compress intermediary spreads.

This is not the end of traditional banks, but it marks the end of an era in which banks served as cheap capital warehouses that were static and unchallenged.

The winners of the new era will be "Web 2.5" hybrids; those institutions that realize they are no longer merely lenders but programmable liquidity managers. By 2030, the stablecoin market is expected to approach $2 trillion, and the boundaries between cryptocurrency and finance will largely disappear. The system will fully integrate track efficiency with balance sheet stability.

In this reconstructed landscape, financial power does not belong to technological innovators but to the entities controlling the ultimate containers of global liquidity and collateral.

Over the past decade, cryptocurrency has been building the infrastructure for institutional participation. The next decade will determine where institutional balance sheets ultimately reside.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。