Original Authors: DaiDai, Frank, MaiTong MSX Research Institute

Q1 just concluded, and the market presented a rather challenging report card.

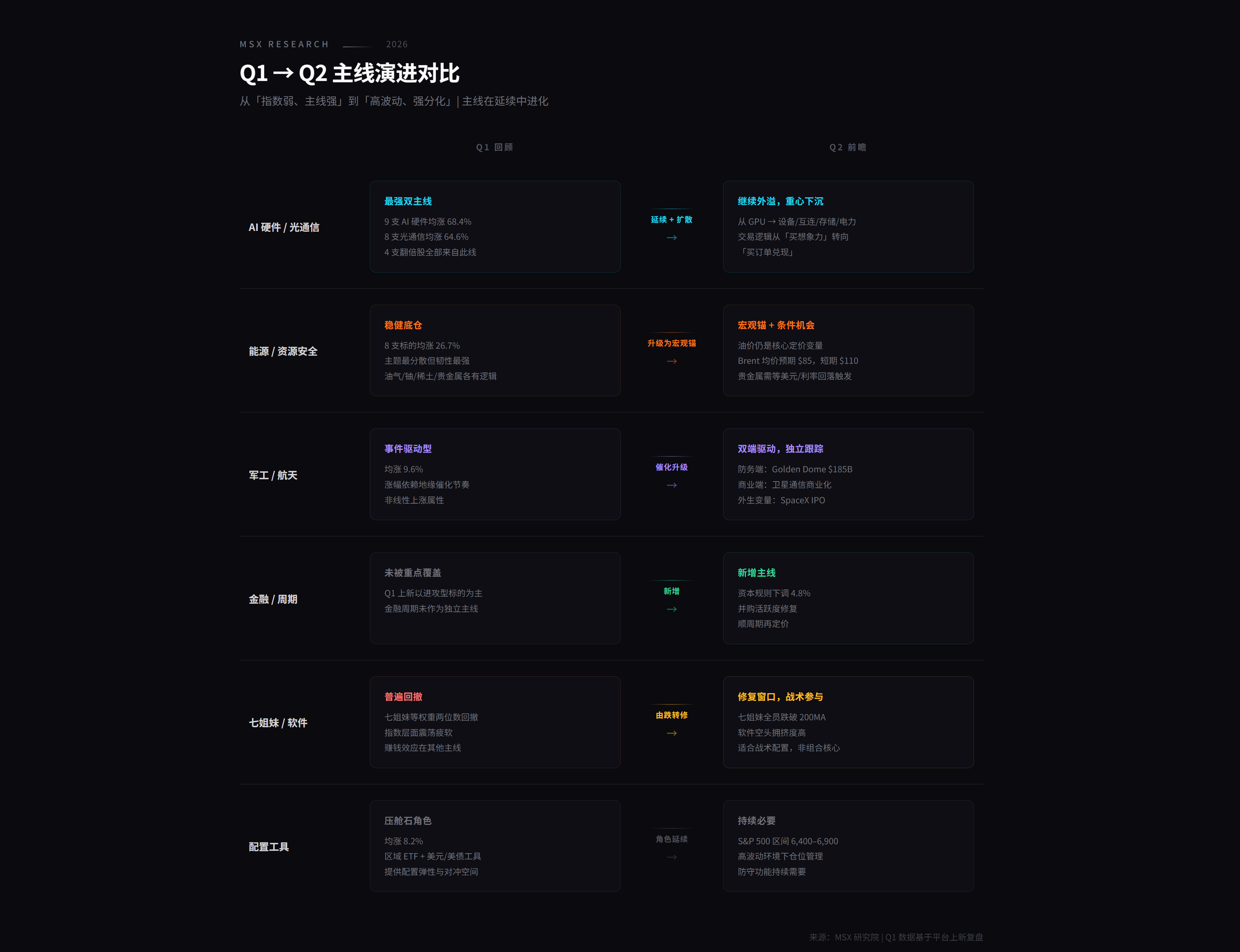

Seven sisters fell across the board, and the index was overall weak, but if you had investments in optical communications, AI hardware, and energy resources, the earnings in Q1 were actually not bad. MaiTong MSX launched 39 targets in Q1, of which 4 targets increased by over 100% were concentrated in the main lines of AI hardware and optical communications (see also: What kind of temperature difference code for US stocks in 2026 is hidden in a "top student's" Q1 new list?).

This reflects an important idea: when the index no longer easily provides Beta, market money will flow more concentratedly towards a few directions that can realize industrial logic.

So the question arises, entering Q2, will this structure of "weak index, strong main lines" continue? Where should money be placed?

Based on this, this article provides a systematic outlook on the macro environment, main sector lines, and trading logic for Q2. The core judgment can be summarized in one sentence—Q2 resembles a quarter of high volatility, strong differentiation, primarily characterized by structural opportunities. The Beta returns at the index level are limited, but Alpha has not disappeared; instead, it will be more concentrated, more selective, and more reliant on understanding the evolution of the main lines.

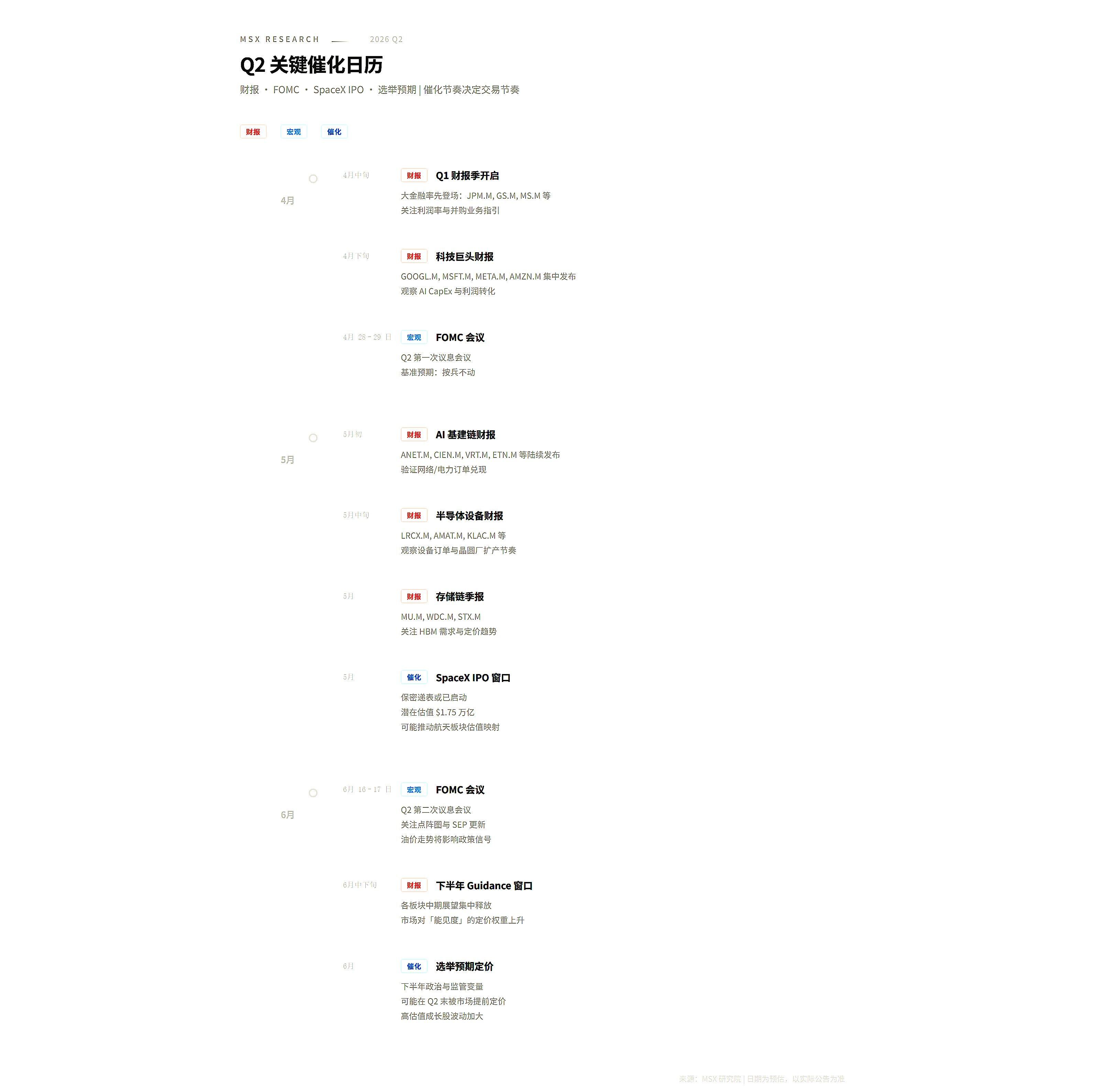

1. Macro Background: Oil Prices as Anchor, Interest Rates as Wall

To understand the market rhythm in Q2, one must see the two layers of ceilings that currently press down on risk assets: one layer is oil prices, and the other is interest rates.

Recently, market expectations for the oil price center have clearly risen, with Brent prices briefly trading in a higher range. At the same time, US inflation data continues to show strong stickiness, and the Fed's stance has not truly shifted towards easing. In this combination, the most important reality the market needs to accept is that rate cuts may come, but they won’t arrive quickly or smoothly enough.

This means Q2 is unlikely to be a quarter that relies on "expansion at the denominator end" to lift overall valuations. After all, if interest rates do not decline, long-duration assets are naturally under pressure; if oil prices rise, it becomes difficult for corporate costs and inflation expectations to easily recede, leading to high oil prices → inflation stickiness → delayed rate cuts → compressed valuation expansion space.

For the market, this almost delineates the trading boundaries in advance, making it increasingly difficult for directions relying on valuation imagination to thrive, while those relying on orders, income, profits, and cash flows find it easier to gain market recognition.

However, constraints do not mean that there are no opportunities. A significant point worth noting at the macro level is that the current environment does not treat all industries equally:

- For example, changes like marginal improvements in regulation, revisions in capital rules, and revived M&A activity are likely to initially benefit the financial sector and certain cyclical industries;

- Meanwhile, the expansion of AI infrastructure, the release of defense budgets, and rising energy and resource prices will channel opportunities into more specific segments of the industrial chain;

Therefore, Q2 is destined not to be a quarter of "overall upward movement," but rather a quarter where "profit visibility determines premiums and the speed of industrial realization determines resilience."

2. Five Main Lines for Q2: Where Will Money Flow?

If we summarize the current environment as "high oil prices + high interest rates + difficulty for the index to trend upwards," then the excess returns in Q2 are likely still to come from a few clear main lines.

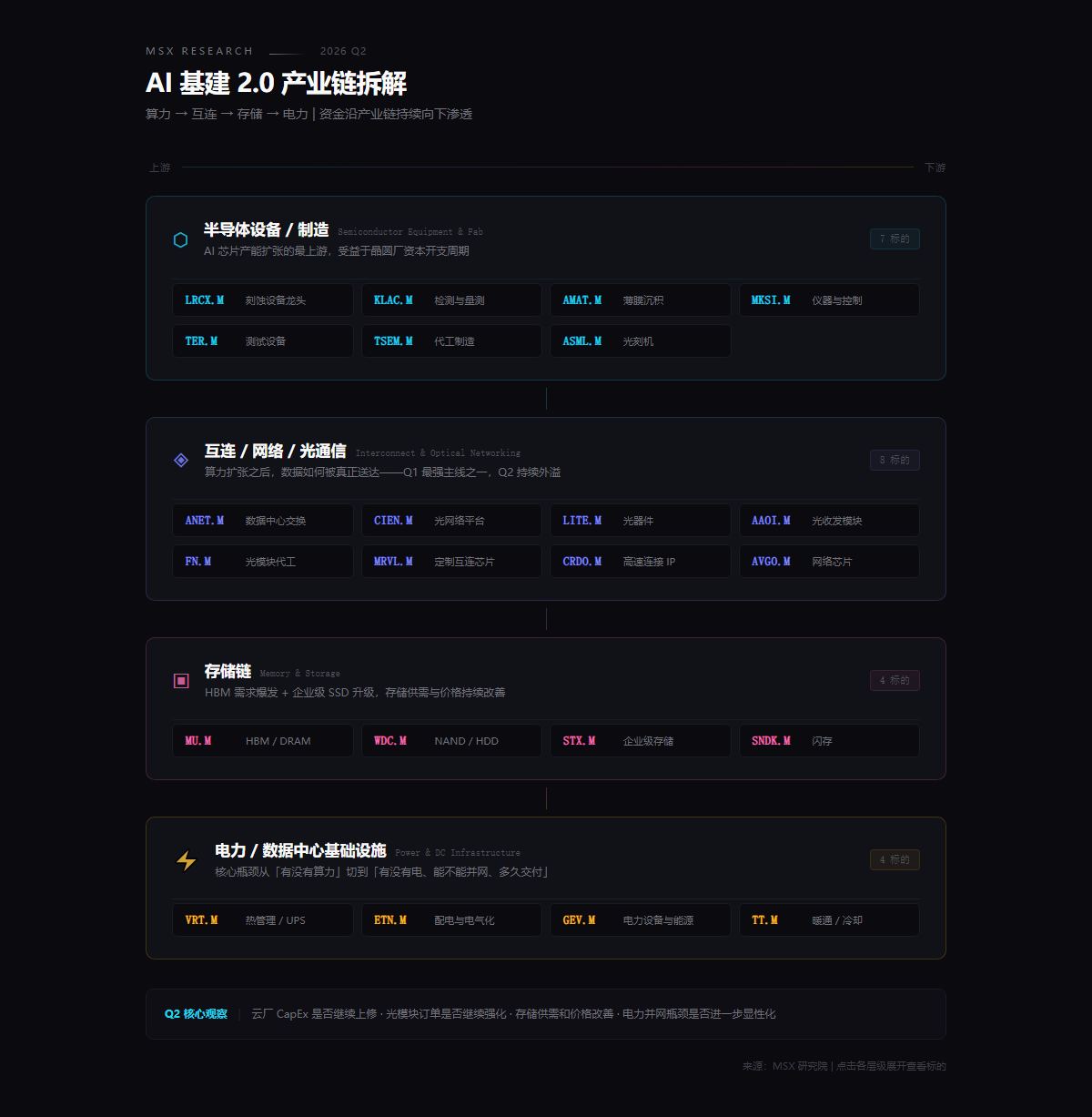

1. AI Infrastructure 2.0: From GPU to Networks, Storage, and Power

The story of AI is far from over, but the market's trading focus has noticeably shifted downwards.

Over the past two years, the market has been particularly focused on trading GPUs, platform companies, and the narrative of large models; as we enter 2026, funds are increasingly questioning more realistically: how is the capital expenditure of large companies that continue to expand actually being transmitted downwards? Who converts this money into orders first, and who converts the orders into revenue and profits?

This is why the AI main line in Q2 aligns more with a "spillover of infrastructure" logic, specifically pointing to four more concrete directions.

These include Lam Research (LRCX.M), KLA (KLAC.M), Applied Materials (AMAT.M), among others. The logic of this line has already begun to materialize in Q1, and Q2 will need to continue observing whether cloud providers revise CapEx upward and whether equipment orders are persistent, marking the most front-end and hard-core capacity expansion logic.

Next, interconnects, networks, and optical communications correspond to the comprehensive amplification of high-density connectivity demands within data centers, including Arista Networks (ANET.M), Ciena (CIEN.M), Lumentum (LITE.M), Applied Optoelectronics (AAOI.M), Fabrinet (FN.M), Marvell Technology (MRVL.M), etc. The average increase of 8 optical communication targets launched by MSX in Q1 was 64.6%, which essentially reflects the explosion in demand for optical interconnects coming from AI data centers, making this line worth continuous tracking in Q2.

Looking further, the beneficiaries of the storage chain are also becoming clearer, including Micron Technology (MU.M), Western Digital (WDC.M), Seagate Technology (STX.M), etc., with the core observation point being whether storage supply and demand and prices can continue to improve.

Lastly, regarding power and data center infrastructure, including Vertiv (VRT.M), Eaton (ETN.M), GE Vernova (GEV.M), etc. The core bottleneck of data center expansion is shifting from "is there computing power" to "is there electricity, can it be connected to the grid, and how long can it be delivered". Power and grid connection capabilities are becoming the most realistic constraints on AI infrastructure, making this a variable worth tracking separately in Q2.

In other words, the AI main line in Q2 is no longer simply about "buying AI," but closer to "infrastructure spillover," meaning funds will continue to penetrate down the industry chain along computing power → interconnects → storage → power. The market must answer a more specific question, namely, to whom are AI investments ultimately reflected in the financial statements? The clearer this question, the easier it becomes for transactions to transition from thematic speculation to systematic opportunity.

2. Finance and Cyclicals: Not Waiting for Rate Cuts, But for Capital Release

Finance and cyclicals are worth reevaluating in Q2, but the logic is not just about "waiting for the Fed to turn dovish."

The more noteworthy changes are that marginal improvements in regulation, adjustments in capital rules, and a warming in M&A activity are providing new profit elasticity for some financial stocks. For large investment banks and comprehensive financial institutions, the real benefits may not come from an immediate decline in interest rates, but more likely from a relief in capital occupation, the restoration of repurchase space, the warming of M&A financing, and the overall resurgence of financial activity.

Therefore, leading financial institutions like Goldman Sachs (GS.M), Morgan Stanley (MS.M), JPMorgan Chase (JPM.M) are watching closely whether they can earlier convert policy improvements into performance expectation recovery in Q2.

As for the industrial and manufacturing sector, for example, Caterpillar (CAT.M), Deere (DE.M), Parker-Hannifin (PH.M), etc. are better understood under the framework of "high nominal growth + cyclical revaluation." As long as industrial orders, equipment investments, and capital expenditure expectations can be maintained, funds will still be willing to provide them with some revaluation space.

Thus, the focus for this line is not on who is the cheapest, but rather who can earliest demonstrate the complete chain of policy marginal improvement → enhanced profit visibility → valuation recovery.

3. Aerospace: From Theme to Commercial Realization

Aerospace is the line in Q2 that is easiest to underestimate but also the most likely to be traded repeatedly.

On one end, there is stronger certainty in defense budgets. For example, forecasts for the costs related to the US "Golden Dome" have been raised to $185 billion, and the capabilities for space and defense are shifting from thematic narratives to real budget support, corresponding to targets including Lockheed Martin (LMT.M), Northrop Grumman (NOC.M), RTX (RTX.M), among others, reflecting a high degree of certainty regarding defense spending logic. Moreover, Kratos (KTOS.M), AeroVironment (AVAV.M), and other defense stocks with greater elasticity take on the market's re-evaluation expectations of unmanned systems, cost-effective combat capabilities, and new defense needs.

On the other end, commercial aerospace is gradually moving away from the vision narrative stage and entering a selection phase of "who can realize, who can commercialize." Companies like AST SpaceMobile (ASTS.M), Rocket Lab (RKLB.M), Planet Labs (PL.M) actually correspond to different paths like satellite communications, launch services, space data, and the market is increasingly willing to reorder them based on realization progress, order quality, and business models (see also: As SpaceX IPO approaches, what really needs to be re-evaluated in the MSX space sector is not just "SpaceX").

Additionally, potential capital market actions surrounding SpaceX, even if still at the expectation level, could serve as significant emotional catalysts for the entire sector. Its real significance lies not just in bringing attention but in potentially pulling the market back to a question: if commercial aerospace is transitioning from a dreamy industry to a cash flow industry, which existing public companies are most qualified to enjoy valuation reflection?

This is why the main line in aerospace for Q2 is likely not a single surge but rather a direction that is traded repeatedly alongside event catalysts, budget advancements, and performance validation.

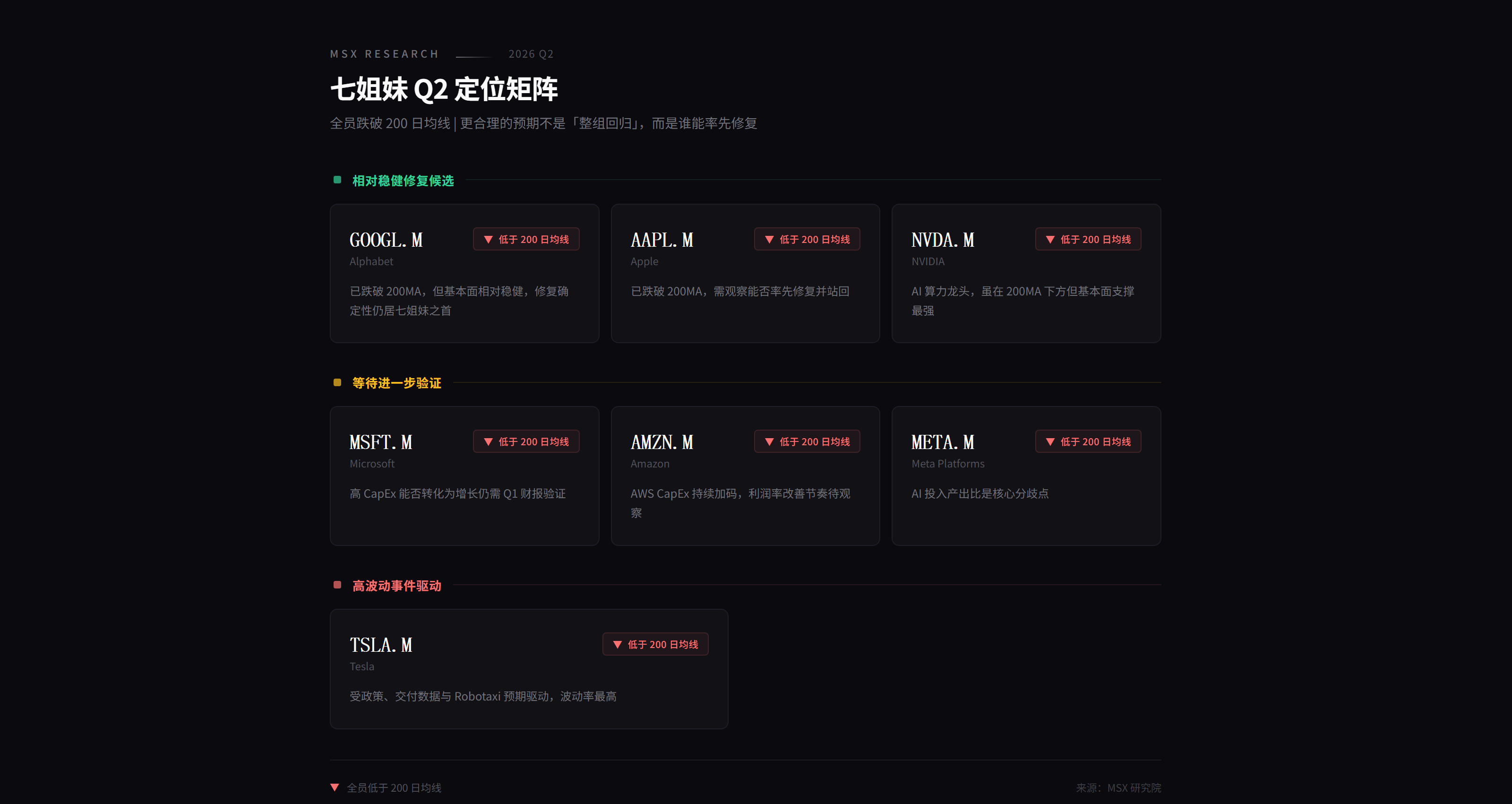

4. Seven Sisters and Software: Repair Window, Not Indiscriminate Return

The Seven Sisters remain important in Q2, but more like a "style signal" rather than a "sole main line."

The value of this group of assets does not lie in whether they will lead the index in a single-sided market but in who can prove first that high capital expenditure is not merely consuming profits but paving the way for future growth and profitability.

From this perspective, Alphabet (GOOGL.M), Apple (AAPL.M), and NVIDIA (NVDA.M) are relatively robust, while Microsoft (MSFT.M), Amazon (AMZN.M), and Meta (META.M) still require more validation from profitability and monetization efficiency. Tesla (TSLA.M) is likely to remain within the framework of high volatility and strong event-driven scenarios.

The software sector is similar. In Q1, many SaaS and software service companies bore a clear implication of "first killing the sentiment, then examining the fundamentals." The market first compressed growth stocks at high valuations, then gradually distinguished who was wrongly punished and who was genuinely decelerating. By Q2, as software and IT services had become overcrowded shorts in institutional holdings, this sector might see partial repair opportunities.

However, what’s truly worth watching is not a generalized rebound in software but which companies possess sturdier cash flows, higher customer stickiness, and clearer segmented barriers. Defensive software (PANW.M, CRWD.M) and enterprise platform leaders with relatively stable cash flows (ORCL.M, CRM.M) will typically find it easier to attract repair capital than purely story-driven SaaS.

Thus, this direction is more suitable to grasp as a tactical repair opportunity rather than being elevated to a new absolute main line.

5. Precious Metals and Resource Security: Conditional Opportunities, But Should Not Be Ignored

Precious metals and resource security should still be kept on the watch list in Q2, but it resembles more a direction of "waiting for triggers."

If the dollar and real interest rates fall at some stage, coupled with ongoing geopolitical uncertainties, then gold, silver, and certain resource stocks are likely to regain trading heat easily. Gold ETF tokens, silver ETF tokens, and leading mining companies will naturally become significant expressions on this line.

More importantly, the significance of this line within the portfolio is not solely about seeking short-term elasticity but rather about its lower correlation to technological growth, possessing certain defensive value. For a portfolio that needs to balance offense and stability, resource security might not always rise the fastest, but it can often provide a different kind of support at critical moments.

3. What to Watch in Q2 from an Earnings Perspective?

MaiTong MSX Research Institute believes that in an environment of high oil prices and high interest rates, Q2's most important focus should not just be on income growth itself but on whether profit margins can be maintained and whether Guidance can be provided more clearly.

The reason is simple. Patience for high investments is declining in the market. If companies can only keep talking about capital spending, future space, and industry vision without gradually converting investments into revenue, profits, or clearer visibility, then valuation pressure will grow increasingly significant; conversely, those companies that can both align with industrial trends and realize growth in their financial statements will naturally achieve higher premiums.

Therefore, the two main things to track in Q2 are:

- First, whether AI has truly led to real efficiency improvements, rather than simply driving up capital expenditure;

- Second, whether cost transmission is smooth, especially given high oil prices, which industries can more easily pass on costs, and which industries will be squeezed by raw material, transportation, and financing costs;

In this sense, segments like equipment, networks, storage, and power are favored at this stage not because they are more "attractive," but because they align better with the current market's aesthetic for realizability.

Therefore, rather than focusing on who slightly exceeds expectations in a single quarter, Q2 should pay more attention to who dares to provide clearer guidance for the second half of the year. The market's tolerance for "high investment" is decreasing, while preferences for "order fulfillment" and "visibility enhancement" are rising. This is also the fundamental reason why these segments are favored at this stage.

Nevertheless, risks still need to be noted. The biggest external variable in Q2 remains the situation in the Middle East and its impact on oil prices and global inflation expectations. If inflation continues to rise and oil prices remain high, the Fed could be forced to maintain a more hawkish path, even reigniting market discussions on "rate hike risks."

Furthermore, the upcoming US midterm elections and regulatory variables for the second half of the year could also be priced in by the market in Q2, leading to greater volatility in high-valuation growth stocks.

Overall, starting from the beginning of Q2, many investors will ask: should we lean more towards offense or defense? MaiTong MSX Research Institute prefers to reinterpret this question: in the current macro environment, a truly effective strategy is not just to simply answer "all offense" or "all defense," but about how to, in a high-volatility environment, establish core positions based on certainty, with marginal positions based on elasticity, while retaining necessary low-correlated defensive exposure.

In other words, the most reasonable strategy for Q2 is not to place all bets on high-elasticity tech stocks, nor to comprehensively retreat out of fear of volatility, but to "bring defense into offense." Core positions can still revolve around AI infrastructure and aerospace supply chains, as they remain the clearest main lines regarding current orders, income, and industrial transmission. At the same time, a portion of exposure less correlated with the tech cycle, such as finance, software, precious metals, and resource security, should be retained to enhance the portfolio's resilience and ability to respond to sudden events.

In Conclusion

When connecting Q1 and Q2, an increasingly clearer trend is that the US stock market in 2026 is transitioning from an era of "buying indices, buying narratives" to "buying main lines, buying realizations."

Q1 has already validated this point. The uniform decline of the seven sisters and the pressure on the index does not mean there is no profit effect; what has truly emerged are the structural directions standing on the transmission chain of industrial trends.

Entering Q2, this pattern is unlikely to disappear, only becoming more differentiated, more rhythmic, and more testing for the understanding of industrial realization paths. Thus, the Beta returns at the index level are limited (with the S&P 500 benchmark expected to oscillate in the range of 6400-6900), but structural Alpha opportunities are abundant.

For investors, the most critical upcoming aspect is no longer to gamble on whether the index can trend upward again but to clearly see which main lines capital will repeatedly migrate along, and which directions can continue to gain market pricing in an environment of high oil prices, high interest rates, and high volatility.

From this perspective, Q2 may not be an easy quarter to "win by lying down," but it could still be a quarter where money can be earned through structural understanding.

Let’s encourage each other.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。