Author: Zuo Ye on Crooked Neck Mountain

The media surrounding altcoins has calmed down, and the saints of the crypto world have found their own beloved children.

It seems nothing has happened; the media does not need to take responsibility for the massive dumping of altcoins, and exchanges do not need to pay for the complete destruction of the industry image.

Reflected in the public opinion market, KOLs are generally extreme and united. Behind Kaito's withdrawal and the implicit harvesting by agencies, the BNB players and everyone else clashed together, ultimately triggering a nonsensical internal conflict.

Only Noise Remains

Beyond the information gap and consensus, only noise remains.

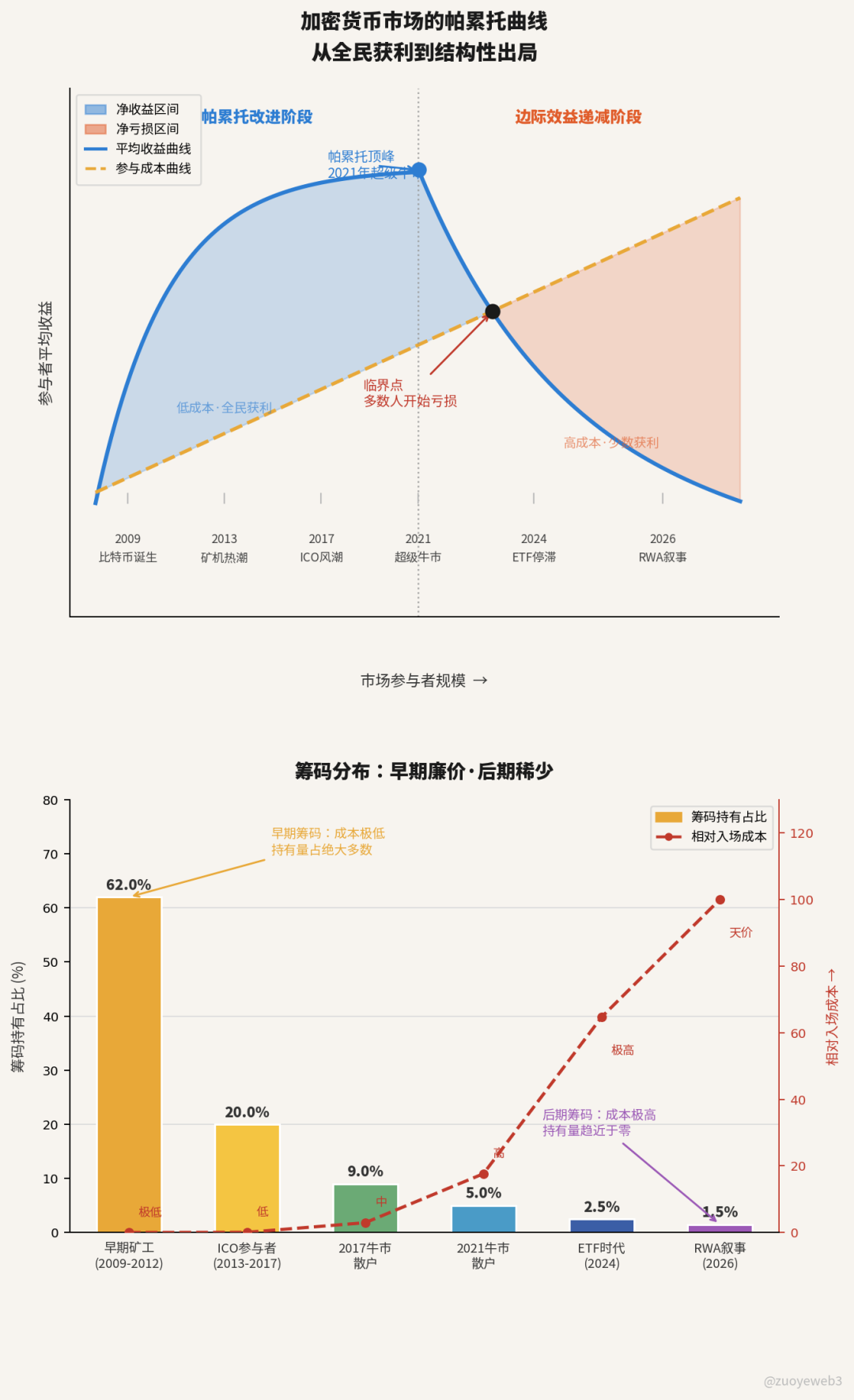

Since the advent of Bitcoin in 2009, the history of cryptocurrency is a perfect Pareto curve, where early lucky individuals accumulated immeasurable wealth, and all subsequent actions revolve around them in cyclical movements.

Image caption: The bull and bear cycles are completely over

Image source: @zuoyeweb3

Pandering to Binance or complaining about unfair OKX lotteries is merely a childish act; exchanges are the ceiling for KOLs, project parties and big players subtly imply scarcity, only crouching to learn when hot topics arise or conducting one-off marketing before issuing tokens.

No long-term cooperation with large tech companies exists here, nor the fertile ground for the birth of industry-level KOLs; you must choose your camp.

More seriously, public chains and USDC/USDT stablecoins no longer require media relations in the crypto space; lobbying, capital operations, and political relationships are more critical than KOLs.

Mr. Beast is advancing into the FinTech industry, while crypto KOLs can only awkwardly learn from the US stock market.

Why?

Because the commodity of information only holds economic value when the information gap and consensus overlap.

- Early miners faced highly controllable investment and holding costs compared to buying and selling Bitcoin and Ethereum; likened to early participants in a pyramid scheme, they could always exit in time. During the stamp and currency card era, CZ was already adept.

- Later-stage assets all believe that everything traditional finance does will go on-chain, but without the expectations of The Merge and BTC spot ETFs, those who invested everything in altcoins wait in vain for capital overflow.

You either became a miner early on to act as a producer, or became a big player later to earn interest. If you entered in between, you could only desperately shout that the bull market will come again; as more KOLs emerge, few can leave with dignity.

Industry-recognized Binance-affiliated KOLs are being bitten back by their main supporters, just like Binance discards its close coin, token editors, and listing brokers; giants have begun to tear away their margins, maintaining a mechanical existentialism.

Moreover, the introduction of AI will only spell disaster for the crypto public opinion market.

In the face of SEC policy interpretations, qualifications review of stablecoin issuers, and project parties' due diligence, the interpretative ability KOLs require closely approaches the professionalism of traditional consulting, auditing, or legal industries.

Then, these industries themselves are in the historical process of being replaced by AI, so why not just learn AI directly?

The problem is that AI is a great professional assistant; professional programmers can leverage AI as a productivity multiplier, but most people can only create a flashy little tool.

In reality, AI has never improved KOLs' ability to interpret and disseminate professional problems; for example, you can see many independent developer KOLs, but you rarely use products made by independent developers; you will see many crypto KOLs' short tweets, but personal IP recognition is increasingly diminished.

Selling the information gap, from the technical advantages of Solana/Aptos and other Ethereum killers, has already collapsed to the Agent needing stablecoins, repeatedly telling themselves that Agents needing stablecoins equate to crypto having a spring again.

Whether stablecoins or RWA, they are merely tools in the crypto industry; without the value of presenting oneself as an asset for sale, the final outcome is SaaS valuations.

In contrast to native crypto assets, a vast sense of bewilderment surrounds us; everyone knows MegaETH will follow in the footsteps of Monad/Scroll, but gamblers have taken up licenses, and everyone must cooperate to perform this play.

In the post-truth era, it's not KOLs and media exploiting AI to create false information, nor is it recommendation algorithms flooding "digital waste"; it’s that the pain index of ordinary people is too high, forcing them to embrace emotional K-line moments of peace.

There is no so-called post-truth era, only garbage time rejecting the truth.

Does Du Jun not know that BTCFi is a joke? Yet he still insists on selling BTC/ETH L2 projects, turning to hide in the room of Bitcoin.

The Super Liquidity of Opinions

Who is our enemy? Who is our friend?

The crypto circle inevitably enters the second half of the Pareto curve; the arrow of time cannot turn back, and under diminishing marginal returns, zero-sum games (my gain is your loss) are unavoidable, so don’t harbor any illusions.

The free market of opinions offers value in finding the next asset with attributes of "upward momentum." Researching whether Google can maintain its position or whether Bitcoin will fall to $50,000 is meaningless; these assets have proven themselves over long cycles.

The solidified market structure, for the public opinion market, anchors on abandoning the foreign concept of KOLs; information market makers are most appropriate.

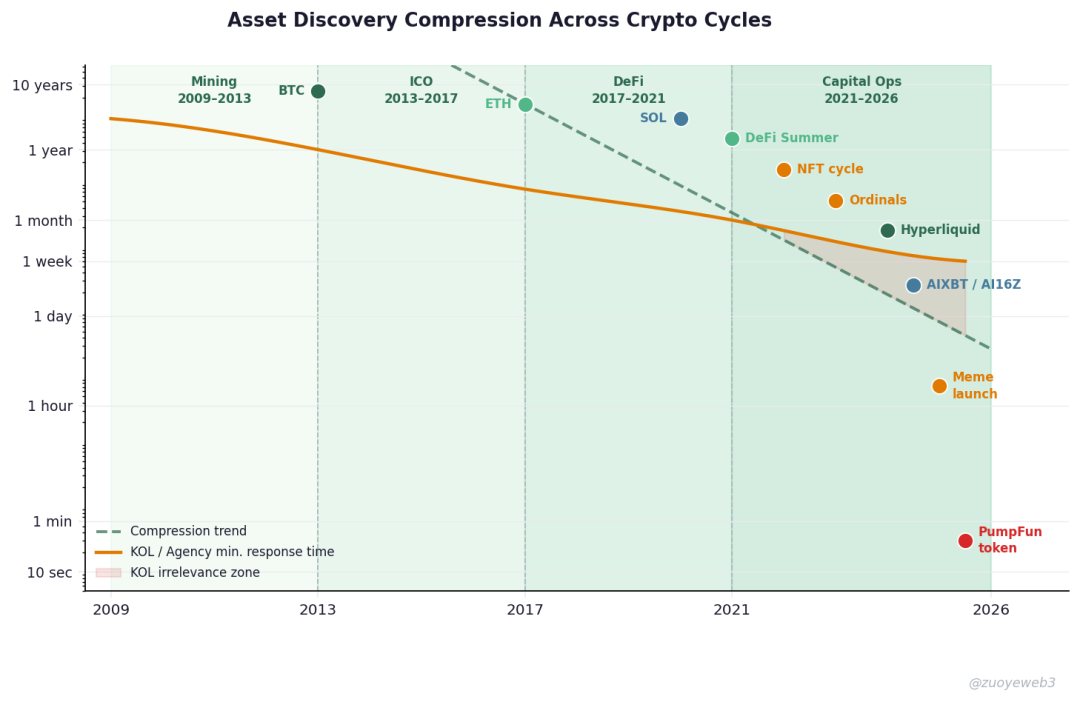

Image caption: Asset discovery and information expression cycles

Image source: @zuoyeweb3

After the end of technical narratives, the narrative of assets and retail purchasing power becomes fractured; US stocks and bonds need to go through stablecoins and Ondo to introduce on-chain narratives. The existing viewpoints of LPs are insufficient to explain this complexity; AMM or CLOB perspectives must be introduced.

Hyperliquid doesn’t do marketing, but traditional algorithms of Twitter (X), WeChat, and Xiaohongshu create barriers; PumpFun treats coins like joy beans, ultimately colliding into extreme probability market tickers.

Gone are the days; compared to these asset issuance paradigms, the opinion market has only evolved into a handmade cooperative like Agency, which does not fit the upcoming asset discovery narratives; it’s not about discovering crypto assets or AI assets, but the next era and the next generation's assets.

If everyone carefully observes the trends in exchanges, a tendency toward central registration (中登化) is already inevitably emerging.

Their goal is to maneuver between major project parties and exchange position arbitrage, not wanting to start a business to get rich, just wanting executives to engage in struggles; they cannot understand the impact of AI on the industry externally, nor can they enhance user experience internally.

Central Registration: A being that fantasizes about commanding others to realize ideas due to its age and the structured superiority granted by its organization.

Asset holders become centralized, opinion spreaders become centralized, leaving only the small ones left in disarray in the wind.

If Perp DEX replacing CEX is already on the way, then to replace the current information market, information market makers must know where to exert their efforts.

- Eliminate the old; the ones to be eliminated are the Binance parents, children, and Xu Mingxing; retreat to the second line, holding coins for interest to earn industry beta returns.

- Introduce newcomers; using the overseas embrace of RWA as an opportunity is critical for financial professionals to step in and facilitate information and funding.

- Transform mechanisms; clinging to Easy Mode for distributing project information will not bring in incremental growth; either have the capability to discover new assets or transition to offline pyramid schemes.

In the face of the helplessness of AI, and the confusion felt in the industry, we need to establish a sense of mission among founders; merely facilitating business transaction information between exchanges and project parties holds no meaning for transaction volumes.

Friends of altcoins (crypto media people) do not possess superior information analysis capabilities; what they have is the inertia of a media brand. Early wealth accumulators possess absolute capital advantages yet do not necessarily have stronger capital operation capabilities; the scale of capital has masked their clumsiness.

Beneath Yi Lihua, whales cut losses and exit; Peter Thiel exited during the low tide of DAT; both are proving that early advantages are more critical. You can continue to make mistakes, but early low-cost accumulation will save you time and time again.

Under the framework of information market makers, any content surrounding current hotspots and individuals is merely a clue; the undercurrents below are the media's exploration range. If the media lacks this discovery capability, it’s recommended to check out Douyin for girls.

Moving forward along the great road paved by DeFi, professional market makers must first be AMM-ified to evolve into more advanced professional CLOB Perp DEX.

In other words, every individual should treat the media as their supporting business, not that KOLs should study for CPA, but that CPA holders should pursue KOL work; the next step in information facilitation is capital facilitation.

Conclusion

The crypto circle is an economic history at light-year scales.

In just over a decade, everyone has gone from profiting to extremity, and riches have yet to be accumulated; the shame of those in the industry is growing daily.

As money is engineered into stablecoins, and AI is engineered into computing power, information should not remain in manual operation stages; everyone’s participation must be mobilized to trigger capital involvement.

The hierarchical pattern of a few big KOLs and many small retail investors cannot bring about the incremental growth that exchanges yearn for; may 2026 see the emergence of a super information market maker.

For Mom and Dad to love me once more is truly abstract; it’s not the child that is abstract, the child merely imitates, the parents are the primary responsibility bearers.

Do not become Wang Lin or Epstein; strive to be the Peter Thiel or Lü Buwei of the new era, hoarding the rare goods of the next stage.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。