Author: Zhi Wu Bu Yan

Around 2006, a group of small foreign trade bosses began exploring how to open stores on eBay in Guangdong and Fujian. They sat in small offices next to factories, doing business with strangers on the other side of the world using broken English.

The hardest part was not the language, not the logistics, but money—how to ensure that an American buyer could safely send money to a Chinese seller?

Making this possible was a blue button. That button was called PayPal.

At that time, PayPal represented the forefront of financial democratization and the most advanced productivity. According to the "Website Payments Standard Integration Guide," global small and medium-sized merchants only needed to input a piece of HTML code to collect payments worldwide.

This technological equality, combined with the foundation laid by eBay's only officially recommended payment method, made PayPal the undisputed global payment leader. To this day, if you open any overseas checkout page, PayPal is sure to have a place.

Twenty years have passed. Many of those small foreign trade bosses have grown from small eBay stores into cross-border merchants flourishing on independent sites, Amazon stores, TikTok, and Temu. The scale of China’s cross-border e-commerce exports has exceeded 2 trillion yuan, and payment tools have evolved from a blue button to a diverse array including Stripe, Wise, Lianlian, and Wanlihui.

The industry has matured, but PayPal has somewhat fallen behind.

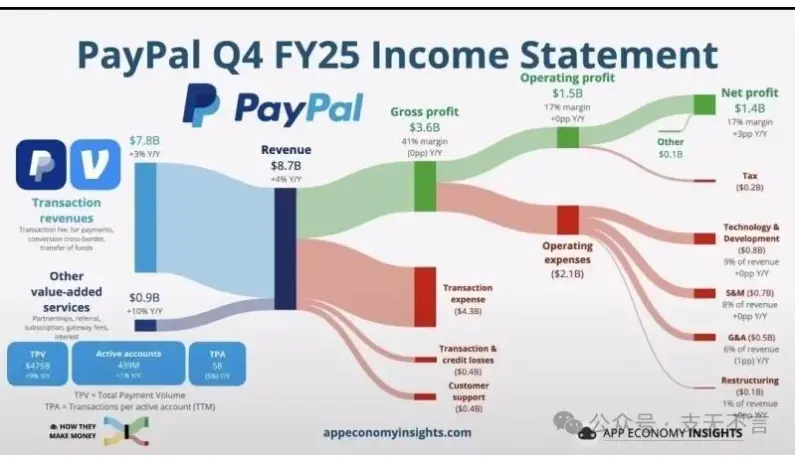

Three weeks ago, on February 3, PayPal announced its financial report, and its stock price plummeted 20% in one day, leading to the resignation of its CEO. The main source of profit, branded checkout, has seen its active user growth rate drop from a previously rapid pace to 1%, and the transaction volume of active accounts has decreased by 5% over the past 12 months.

Whether it is one-click link payment from Stripe, biometric verification from Apple Pay, or simply using Google to autofill credit card information, it seems more convenient than that slightly outdated blue icon interface, which might not even remember the login password.

It was once a legend created by Elon Musk, Peter Thiel, and Reid Hoffman. Pelosi once held a large stock, and Cathie Wood was its most loyal supporter, but they both chose to liquidate.

PayPal's market value has dropped from its pandemic peak of 363 billion dollars to a recent low of 38 billion—losing 90% over five years, with the P/E ratio sinking to a low of 7.4. Until Bloomberg revealed today that at least one major competitor is evaluating a complete acquisition, while multiple parties have expressed interest in certain assets, the stock price has finally risen by nearly 10%.

This news itself is the most precise commentary on PayPal's situation. When a company starts to be regarded as prey rather than a hunter, and its market value rises as a result, it indicates that the market's confidence in its independent operation is lower than the expectation of being acquired.

The once payment empire, like the twilight of the British Empire, still has its flags planted across the world, and the sun has not yet set, but the eyes of those who see it no longer hold the same awe as before. Everyone knows deep down that the times have changed. But how did it fall so low?

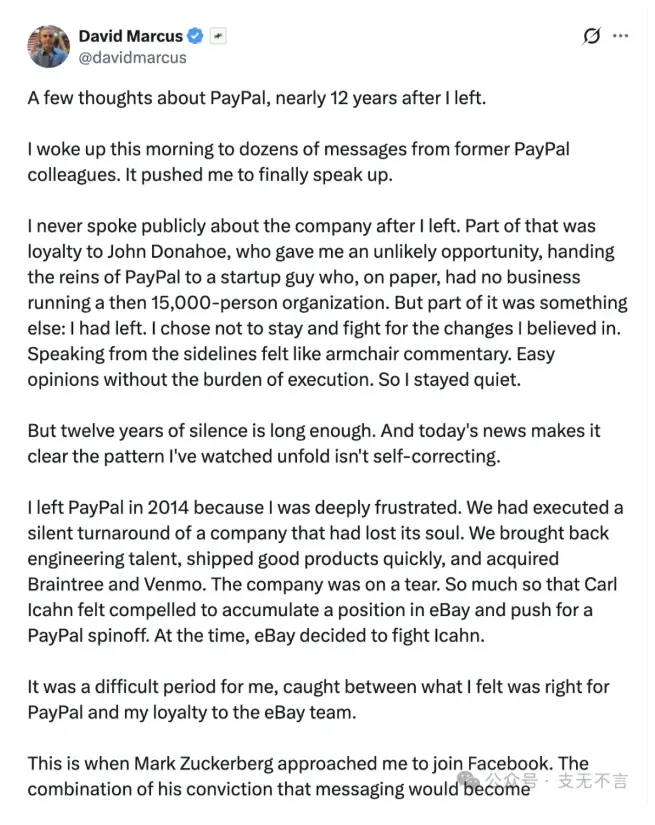

"It really hurts to see a company I love so much come to this point."

On February 3, former PayPal president David Marcus posted a lengthy article on X, rarely criticizing the company he had devoted himself to.

David Marcus's career has always been accompanied by radical financial innovation. He currently serves as CEO of Bitcoin Lightning Network payment company LightSpark. During his time at PayPal, he recruited top engineering talent and led the acquisition of Braintree and Venmo; during his time at Facebook, he was one of the leaders of the sensational stablecoin project Libra. Although Libra failed due to regulatory reasons, today's stablecoin boom is enough to prove David’s foresight and boldness.

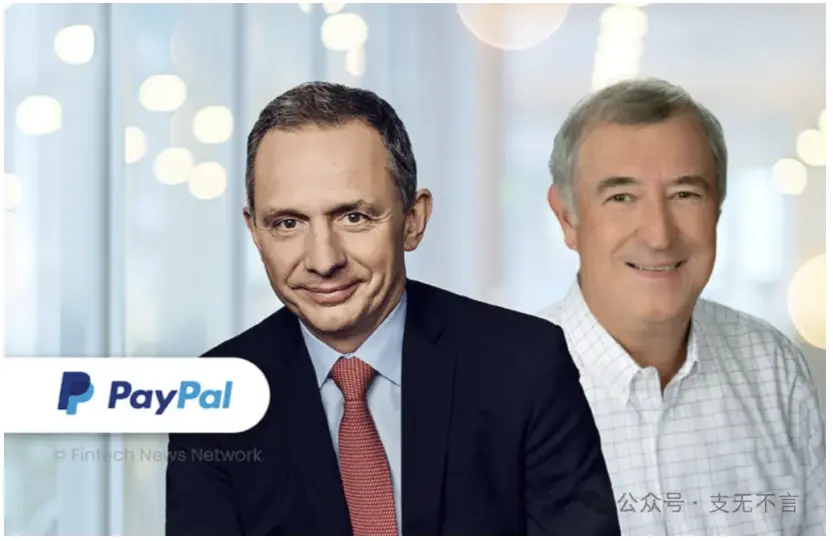

In addition to the stock price crash, another reason that prompted David to post this long message was the resignation of former CEO Alex Chriss, who left less than three years after taking up the position, and was succeeded by former HP CEO Enrique Lores.

Enrique Lores served as CEO of HP for seven years, introduced the profitable model of printing as a service, and initiated large-scale layoffs. He is undoubtedly an expert in cost reduction and business restructuring. If the PayPal board had long been considering an outright or partial sale of PayPal,this candidate seems even more reasonable.

David subtly expressed his dissatisfaction: "I don’t know Enrique. He may be a great leader, but at least from the paper information, he is an executive from the hardware industry, now parachuted into a payment company."

This resonates with David's core criticism. Unlike the market voting with its feet due to poor financial performance, David believes that PayPal's Achilles' heel is—"the company's leadership style has completely shifted from 'product-driven' to 'finance-driven.' Over time, belief in the product has given way to financial optimization."

To paraphrase a famous saying by Benjamin Franklin: any company that sacrifices product quality for short-term stock price performance will ultimately fail to keep up with the trends of the product era and will also lose stock value.

David believes PayPal has lost its "mojo." This was a spirit from the time of the PayPal mafia, a kind of wild energy that dared to flip the roof of the office to solve an impossible problem. But today, that energy has been replaced by compliance checks and financial optimization.

Stripe, which conquers developers with its simple API, has this mojo. Open Stripe, and the constantly changing "Global GDP running on Stripe" in the upper left corner exudes a conqueror’s quality.

In recent years, Apple Pay, which has vigorously promoted Passkey, has this mojo. Relying on underlying security chips and Face ID, it has pushed the payment experience to the extreme comfort—just raise the wrist, scan the face, and finish, without even having to open the App. This is beyond PayPal, which still relies on the three-step experience of redirecting pages, reauthorizing, and waiting for confirmation.

The representative of Neobank, Revolut, has this mojo. With strong execution power, this emerging company has connected an all-stack financial platform covering dozens of countries for stocks, currency exchange, and cryptocurrencies in a very short time, and is continuously expanding its reach.

These three companies have one thing in common: their mojo does not come from scale, user numbers, or even money. It comes from a product belief: a belief that what they are doing will make a difference in some corner of the world.

And this is just the tip of the iceberg. Shop Pay, Klarna, Affirm, Afterpay, Wise, Cash App, Adyen—every cut in the payment lane is crowded with people.

PayPal once had this kind of thing. That HTML code, that blue button allowing an American uncle selling second-hand goods from his garage and a small factory owner in Guangzhou to complete cross-border settlement, was in itself a declaration of changing the world. But the process of losing it was quiet, almost silent.

When discussing PayPal's development over the past few years, one cannot ignore Venmo.

Venmo did one thing right: it turned transfers into a social activity—splitting dinner bills, sharing rent, and sending an emoji to a friend is much more fun than a bank transfer. Its spread among young people in the U.S. resembles a social app more than a payment tool. "Venmo me" has even become a verb, synonymous with transferring money among American youth.

PayPal's acquisition of Venmo was actually a byproduct of acquiring the payment service provider Braintree; this product, which was not very noticeable at the time, is now a bright spot in PayPal's dim financial reports: $1.7 billion in revenue by 2025, over 100 million monthly active accounts, 50% year-over-year growth in Pay with Venmo transaction volume, and 40% growth in debit card users.

But behind these numbers, several deep-seated issues are brewing: those who are optimistic about it are obsessed with the doubling debit card transaction volume, believing this cash cow is entering a harvest phase of monetization; while those who are worried about it counter, if this prosperity relies solely on draining the remaining social circle, how long can this afterglow last?

This rift essentially reflects Venmo's entrapment in an ecological niche: upward, it cannot breach the hard wall built by Apple Pay and Google Pay; downward, it cannot burrow into the deep-seated underground networks of Stripe and Adyen. Venmo's growth is strong, but its ceiling is also quite obvious.

First is the internal friction of the growth model. The 20% revenue growth rate is backed by only 7% growth in active users—Venmo is no longer expanding its territories, but rather taxing its existing users, extracting more from the same group, while failing to attract a new generation.

Secondly, there is the dual dilemma of geography and product identity. Venmo remains locked in the U.S. market, capturing America’s dining tables, but has not yet entered the world’s cash registers.

Finally, the comprehensive financial vision temporarily fell short. In the business ecosystem PayPal designed for Venmo, there was also a shopping plugin called Honey, intended to connect the "discovery-settlement" link. But due to a scandal over altering affiliate links in 2024, Honey almost collapsed, severing this traffic pipeline, which also dampened Venmo's transformation journey.

How can a standalone consumer payment application prove its worth to users to open it actively? This is a question Venmo is striving to answer, but the answer has yet to be revealed.

Venmo reflects PayPal’s anxiety on the consumer side. On a further frontier, PayPal is also betting on two other cards—one called PYUSD and the other called agentic payment. The commonality between these two cards is that the track is vast enough, but the odds of winning have not yet settled.

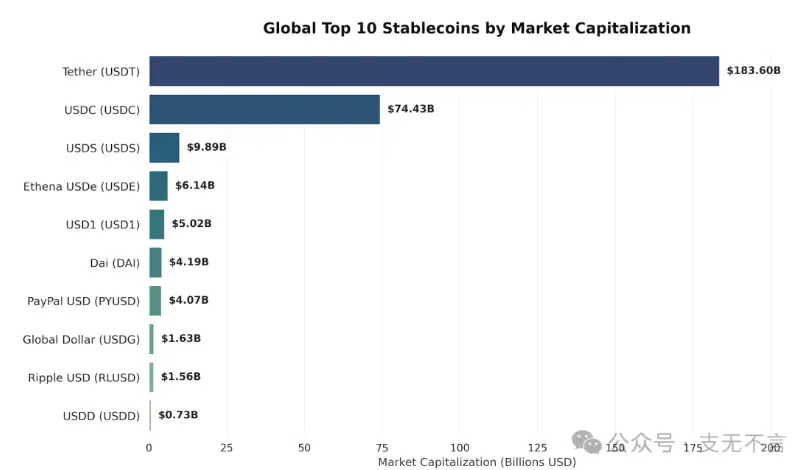

Objectively speaking, PYUSD has not performed poorly. Since its release in 2023, its market size has reached $4 billion, consistently ranking in the top ten global stablecoins by market value. However, compared to Tether's approximately $180 billion USDT and Circle's roughly $70 billion USDC, PYUSD's scale is negligible.

It instead proves one thing: even if everyone can issue stablecoins, the barriers to channel distribution and user perception are still very high, and even a behemoth like PayPal cannot expect to crush the competition.

When PayPal announced a 4% annual interest for PYUSD holders in April 2025, the industry was once astonished that the giant was about to kill the competition, yet developments are incremental. The trillion-level usage of stablecoins currently primarily stems from cryptocurrency trading hedges, cross-border arbitrage, gray area fund transfers, DeFi lending, LP, and yield farming's underlying assets, none of which PYUSD excels at.

Certainly, future stablecoin use cases will become more mainstream and commonplace, such as cross-border B2B payments, on-chain settlements, and everyday retail; however, the competition is extremely fierce—not to mention the two towering giants USDT and USDC, innovative-oriented USDe, and family-backed USD1 are all fierce opponents, and PYUSD does not have a guaranteed advantage.

Besides stablecoins, PayPal also has its sights on agentic payment. They have abandoned error-prone web crawlers and turned to API integration with merchants’ order management systems. Merchants only need to sign an agreement, and PayPal can distribute their real-time data such as inventory, colors, and prices to mainstream AI platforms like Google Gemini and PayPal’s own app.

The idea is clear, but this is an untested market. Recently, Qianwen handed out red envelopes to treat people to milk tea, which served as market education for domestic consumers regarding AI shopping. However, changing consumer habits is not something that can happen overnight, and whether chatting with AI to shop will become mainstream or whether the main shopping experience inherently lies in a person slowly selecting goods while comparing prices remains unknown.

Even if in the future people truly become accustomed to saying to ChatGPT, "Help me buy an iced, three-sweet oolong tea," the platforms controlling transaction retention data will still be those with vast user bases, and these AI platforms are also likely to have their own direct payment methods or share the benefits; in this brand-new chain, PayPal's position remains questionable.

After discussing so much loss and uncertainty, you might think that PayPal's story has come to a conclusion.

But the truth is never one-sided. Braintree remains the underlying payment engine for many global platforms. Pay Later handled over $40 billion in transactions in 2025, leading the BNPL market in the U.S. The Fastlane one-click checkout launched in August 2024 is one of the few proactive moves, directly challenging Apple Pay and Shop Pay. Coupled with 400 million active accounts and over $6 billion in free cash flow for the year—these assets, in the eyes of any company looking to position itself in the AI agency economy, are strategic tickets that cannot be replicated from scratch.

Almost thirty years of accumulation have not been in vain and will not disappear into thin air. It’s just a pity that the great river flows on, washing away everything.

The one who knows best how to use this ticket may no longer be PayPal itself.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。