Author: Ray Dalio

Have you noticed that the Federal Reserve has announced it will stop quantitative tightening (QT) and start quantitative easing (QE)? Although this has been described as a technical operation, it is nonetheless a form of easing policy—this is also one of the important indicators I monitor to track the evolution of the "big debt cycle" dynamics described in my last book.

As Chairman Powell stated: "At some point, reserves need to gradually increase to match the size of the banking system and the economy. Therefore, we will increase reserves at specific points in time," and the specific increments are worth close attention. Given that the Federal Reserve has the responsibility to "control the size of the banking system" during bubble periods, we need to simultaneously monitor its pace of injecting liquidity into emerging bubbles through interest rate cuts.

More specifically, if there is a significant expansion of the balance sheet against a backdrop of lower interest rates and high fiscal deficits, we will view this as a classic fiscal-monetary coordination operation where the Federal Reserve and the Treasury work together to monetize government debt. If this situation occurs while private credit and capital market credit creation remain strong, the stock market continues to hit new highs, credit spreads approach lows, unemployment is low, inflation is excessive, and AI stocks have formed a bubble (as indicated by my bubble indicators), then in my view, the Federal Reserve is injecting stimulus into the bubble.

Given that the government and many individuals advocate for significantly loosening policy constraints to implement aggressive capitalism-oriented monetary and fiscal policies, and the current unresolved massive deficit/debt/bond supply-demand issues need to be addressed, I suspect this is far from the technical issue it is claimed to be—this concern should be understood. I understand that the Federal Reserve is highly focused on financing market risks, which means that in the current political environment, it tends to prioritize market stability over strong anti-inflation measures. However, whether this will evolve into a comprehensive classic stimulative quantitative easing (accompanied by large-scale net bond purchases) remains to be seen.

We should not overlook the current situation: when the supply of U.S. Treasury bonds exceeds demand, the central bank buys bonds through "printing money," and the Treasury shortens debt maturities to fill the long-term bond demand gap, these are typical dynamic characteristics of the later stages of the debt cycle. Although I have comprehensively explained its operational mechanism in my book "Why Nations Fail: The Big Cycle," it is still necessary to point out that we are approaching a classic milestone in this big debt cycle and briefly review its operational logic.

My goal is to impart knowledge by sharing thoughts on market mechanisms, revealing the essence of phenomena like teaching someone to fish—clarifying the logical thinking and pointing out current dynamics, leaving the rest for readers to explore on their own. This approach is more valuable to you and allows me to avoid becoming your investment advisor, which is beneficial for both parties. Here is my interpretation of the operational mechanism:

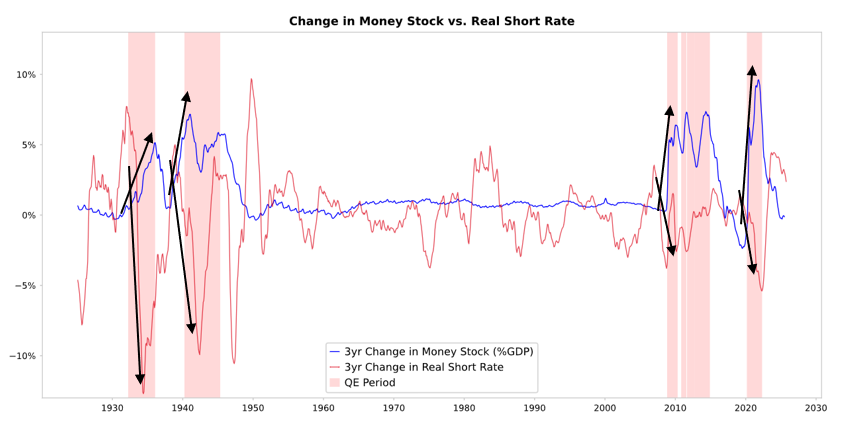

When the Federal Reserve and other central banks purchase bonds, they create liquidity and lower real interest rates (as shown in the figure below). The subsequent developments depend on the direction of the liquidity flow:

If liquidity remains in the financial asset realm, it will push up financial asset prices and lower real yields, leading to an expansion of price-to-earnings ratios, a narrowing of risk premiums, and a rise in gold prices, creating "financial asset inflation." This benefits holders of financial assets relative to non-holders, thereby widening the wealth gap.

Typically, some liquidity will transmit to the markets for goods, services, and labor, pushing up inflation. Under the current trend of automation replacing labor, this transmission effect may be weaker than usual. If the inflation stimulus is strong enough, nominal interest rates may rise to a level sufficient to offset the decline in real interest rates, at which point both bonds and stocks will face dual pressure on nominal and real values.

Transmission Mechanism: Quantitative Easing Transmits Through Relative Prices

As I explained in my book "Why Nations Fail: The Big Cycle" (which cannot be detailed here), all flows of funds and market fluctuations are driven by relative attractiveness rather than absolute attractiveness. In simple terms, everyone holds a certain amount of funds and credit (the central bank influences its scale through policy) and decides the flow of funds based on the relative attractiveness of each option. For example, borrowing or lending depends on the relative relationship between the cost of funds and expected returns; investment choices primarily depend on the relative levels of expected total returns across various assets—expected total returns equal the sum of asset yields and price changes.

For instance, if the yield on gold is 0% and the yield on a 10-year U.S. Treasury bond is currently about 4%, if the expected annual price increase for gold is less than 4%, one should choose to hold Treasury bonds; if the expected increase exceeds 4%, one should choose to hold gold. When assessing the relative performance of gold and bonds against the 4% threshold, inflation rates must be considered—these investments must provide sufficient returns to offset the erosion of purchasing power due to inflation. All else being equal, the higher the inflation rate, the greater the expected increase in gold prices—because inflation primarily arises from the depreciation of other currencies due to increased supply, while the supply of gold is essentially fixed. For this reason, I pay attention to the state of money and credit supply and the policy trends of central banks like the Federal Reserve.

More specifically, in the long run, the value of gold always synchronizes with the inflation rate. The higher the inflation level, the lower the attractiveness of the 4% bond yield (for example, a 5% inflation rate would enhance the attractiveness of gold, supporting its price, while simultaneously weakening the attractiveness of bonds as real yields drop to -1%). Therefore, the more money and credit the central bank creates, the higher I expect the inflation rate to be, and the lower my preference for bonds relative to gold.

All else being equal, the Federal Reserve's expansion of quantitative easing is expected to lower real interest rates and increase liquidity by compressing risk premiums, thereby lowering real yields and pushing up price-to-earnings ratios, particularly enhancing the valuations of long-term assets (such as technology, artificial intelligence, and growth companies) and inflation-hedged assets like gold and inflation-linked bonds. When inflation risks re-emerge, tangible asset companies such as mining, infrastructure, and physical assets are likely to outperform pure long-term tech stocks.

Under lagging effects, inflation levels will be higher than previously expected. If quantitative easing leads to a decline in real yields while inflation expectations rise, nominal price-to-earnings ratios may still expand, but real return rates will be eroded.

A reasonable expectation is that, similar to the end of 1999 or 2010-2011, there will be a strong liquidity-driven rally that will ultimately be forced to tighten due to excessive risks. The liquidity frenzy phase before the bubble bursts—just before the tightening policies are sufficient to suppress inflation—is the classic ideal selling opportunity.

This time is different because the Federal Reserve will create a bubble through easing policies.

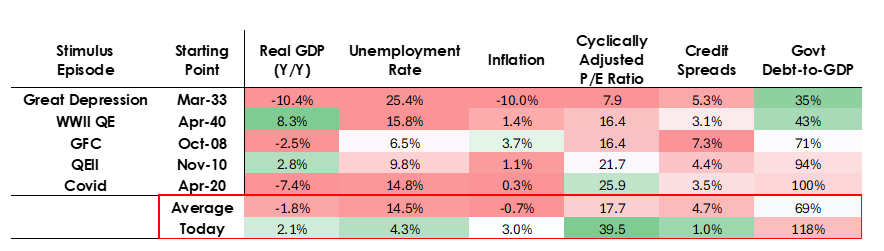

While I believe the operational mechanism will unfold as I described, the environment for implementing this quantitative easing is fundamentally different from the past—this easing policy is being conducted within a bubble rather than during a recession. Specifically, in previous instances of quantitative easing:

- Asset valuations were in a declining state, with prices low or not overvalued.

- The economy was in a contraction or extremely weak state.

- Inflation rates were low or on a downward trend.

- Debt and liquidity issues were severe, with widening credit spreads.

Thus, quantitative easing is essentially "injecting stimulus into a recession."

In contrast, the current situation is exactly the opposite:

Asset valuations are high and continue to rise. For example, the S&P 500 index yield is 4.4%, while the nominal yield on 10-year Treasury bonds is only 4%, with a real yield of about 1.8%, resulting in a stock risk premium as low as about 0.3%.

The economic fundamentals are relatively strong (the average real growth rate over the past year has been 2%, and the unemployment rate is only 4.3%).

Inflation is slightly above the target (around 3%), but the growth rate is relatively moderate, while the reversal of globalization and inefficiencies caused by tariff costs continue to push prices higher.

Credit and liquidity are abundant, with credit spreads approaching historical lows.

Therefore, the current quantitative easing is essentially "injecting stimulus into a bubble."

Thus, this round of quantitative easing is not "injecting stimulus into a recession," but rather "injecting stimulus into a bubble."

Let’s see how this mechanism typically affects stocks, bonds, and gold.

Given that government fiscal policy currently has a strong stimulative effect (as massive unpaid debts and huge deficits are being compensated for by large-scale issuance of Treasury bonds, especially in relatively short-term bonds), quantitative easing is effectively monetizing government debt, rather than merely reactivating the private system. This makes the current situation different and appears more dangerous, making it easier to trigger inflation. This looks like a bold and risky gamble on economic growth, especially on AI growth, funded by extremely loose fiscal, monetary, and regulatory policies, which we need to closely monitor to respond appropriately.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。