Software devours the world, and stablecoins devour blockchain.

This time, it is no longer Coinbase's Base or Robinhood L2; Circle and Stripe have almost simultaneously chosen to build their own stablecoin Layer 1, completely freeing themselves from the constraints of existing public chains, reconstructing everything from the underlying mechanism to the Gas token around stablecoins.

Banks lose their deer, and stablecoins chase them.

On the surface, Circle's Arc and Stripe's Tempo directly compete with Tron and Ethereum, but in reality, they are targeting the global clearing power of the "post-central bank - banking system." The Visa and SWIFT systems that support fiat currencies can no longer meet the global liquidity needs of stablecoins.

Cross-Border Crisis: Card Organizations Yield to Stablecoin Public Chains

The Wintel alliance monopolized the personal PC market for nearly 30 years until the ARM system rose in the mobile sector, causing Intel to gradually decline without making mistakes.

Bank cards and card organizations did not synchronize; the first card organization, Diners Club, established a credit accounting system for restaurants and "iron fans" in 1950. Loyalty became the precursor to credit and points systems, and it wasn't until the 1960s that it connected with the banking industry. Starting with credit cards, local banks in the U.S. broke through state and national boundaries, sweeping the globe.

Compared to banks that need to oscillate periodically around leverage under the Federal Reserve's command, card organizations like Visa/MasterCard operate a cash flow business that is guaranteed regardless of the weather. For example, in 2024, Capital One acquired Discover for $35.3 billion, transforming into a giant organization that combines card issuing and card organization.

The integration of traditional banks is the precursor to stablecoin issuance and the establishment of stablecoin public chains. Only through integration can all channels of issuance, distribution, and repayment be controlled.

After the Genius Act, the operational logic of the dollar has completely changed. Traditional commercial banks bear the responsibilities of credit creation and currency issuance (M0/M1/M2), but Tether and Circle's U.S. Treasury positions have already surpassed those of several national entities.

Stablecoins directly connect to government bonds; the banking industry can still issue stablecoins for self-rescue, but card organizations and cross-border payment channels face survival crises.

• Banking Industry -> Stablecoin Issuers USDT, USDC

• Card Organizations/SWIFT/PSP -> Stablecoin L1

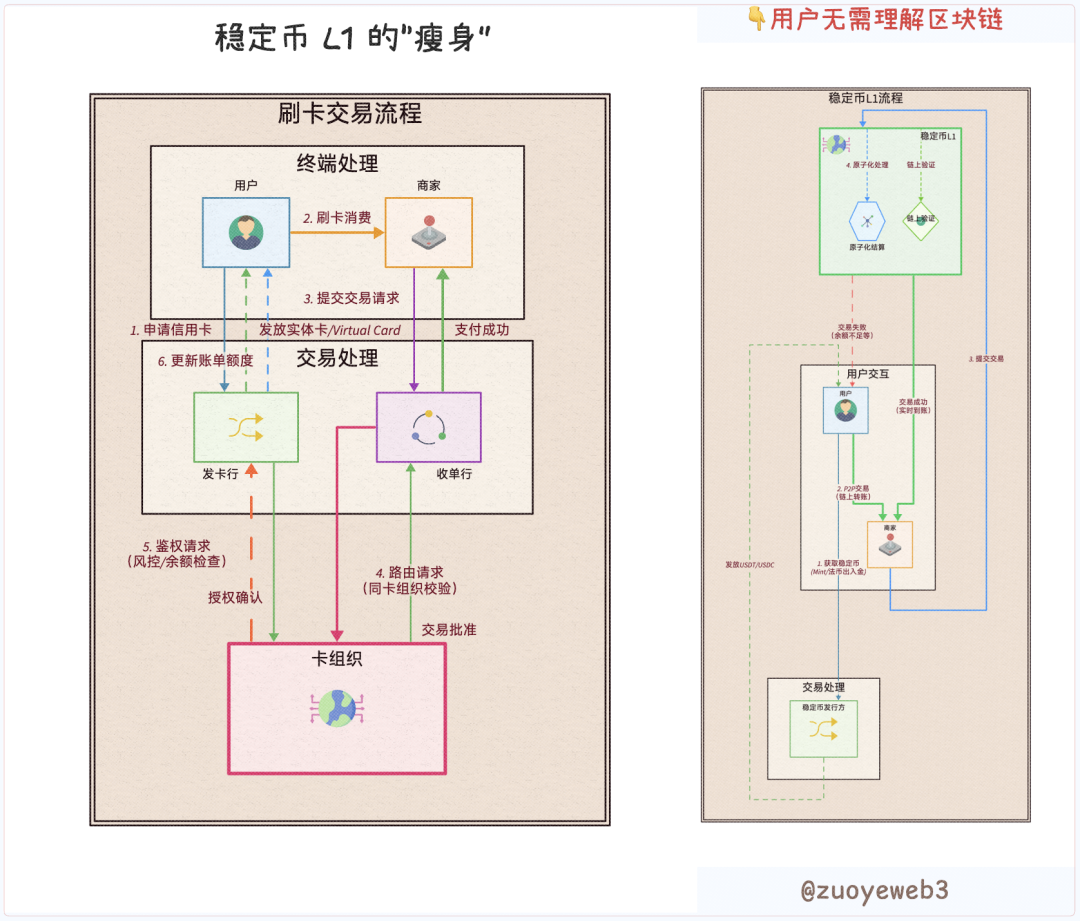

In traditional transaction flows, users, merchants, issuing institutions, acquiring institutions, and card organizations are completely different roles. However, the programmability of blockchain fundamentally changes everything; any role can be reduced to "user," whether it is the privacy vault and confidential transfer needed by institutions or the convenience required by individuals, distinguished only by different codes.

Stablecoin L1 further eliminates the necessity of any non-user institutions; only users, stablecoins, and L1 are needed to complete any role and function interchangeably, even for compliance reviews by regulatory authorities.

Image Description: Innovation in Transaction Process

Source: @zuoyeweb3

Of course, this does not mean that specialized issuing and technical service institutions will disappear; rather, it means that from a couplable code perspective, suppliers can be reviewed and selected. For example, with U cards, the profits from virtual cards are taken by upstream entities, and the U card issuer itself can only lose money while gaining exposure.

Technological innovation is the precursor to changes in organizational relationships.

Now, it would be sufficient to establish a Visa from scratch, keeping all profits to distribute to users.

Just like Capital One, before acquiring Discover, it had to pay a 1.5% fee to Visa/MasterCard, and USDT/USDC also need to pay Gas Fees to Tron and Ethereum.

At the same time Circle promotes Arc, Coinbase Commerce directly connects with Shopify, and Circle has also chosen Binance as its partner for the yield-generating stablecoin USYC.

Tether once claimed that 40% of public chain fees were generated by it, and Circle even had to provide an additional "subsidy" of $300 million to Coinbase in a single quarter. Therefore, it is reasonable to eliminate existing channel providers and establish its own distribution channels and terminal networks.

However, Circle chose to build independently, while Tether opted for external competition with Plasma and Stable.

The only exception is Stripe, which lacks stablecoins but controls the end-user network. After acquiring Bridge and Privy, it has completed a technological closed loop. Boldly predicting, Stripe will eventually issue or "support" its own stablecoin.

In summary, stablecoin issuance, distribution channels, and terminal networks are all building their own closed loops:

• Stablecoin Issuers: Circle's Arc, Tether's Plasma and Stable, USDe's Converge

• Distribution Channels: Exchanges like Coinbase and Binance, existing public chains like Ethereum and Tron

• Terminal Networks: Stripe's self-built Tempo

The freedom of the French is not the freedom of the British; USDT's L1 is not the habitat of USDC. When everyone no longer wants to make do, the competition between existing public chains and card organizations flows like the Yangtze River, unstoppable.

Technological Diffusion: Public Chains Easily Accumulate, Institutional Clients Hard to Expand

Extremist defense of freedom is not evil; a restrained pursuit of justice is not a virtue.

Privacy is no longer a concern for ordinary users. Just like QUBIC's devouring of Monero cannot compare to the heat of treasury strategies, privacy transactions from a liberal perspective are merely "paid privileges" for institutional users. What ordinary users truly care about is transaction fees.

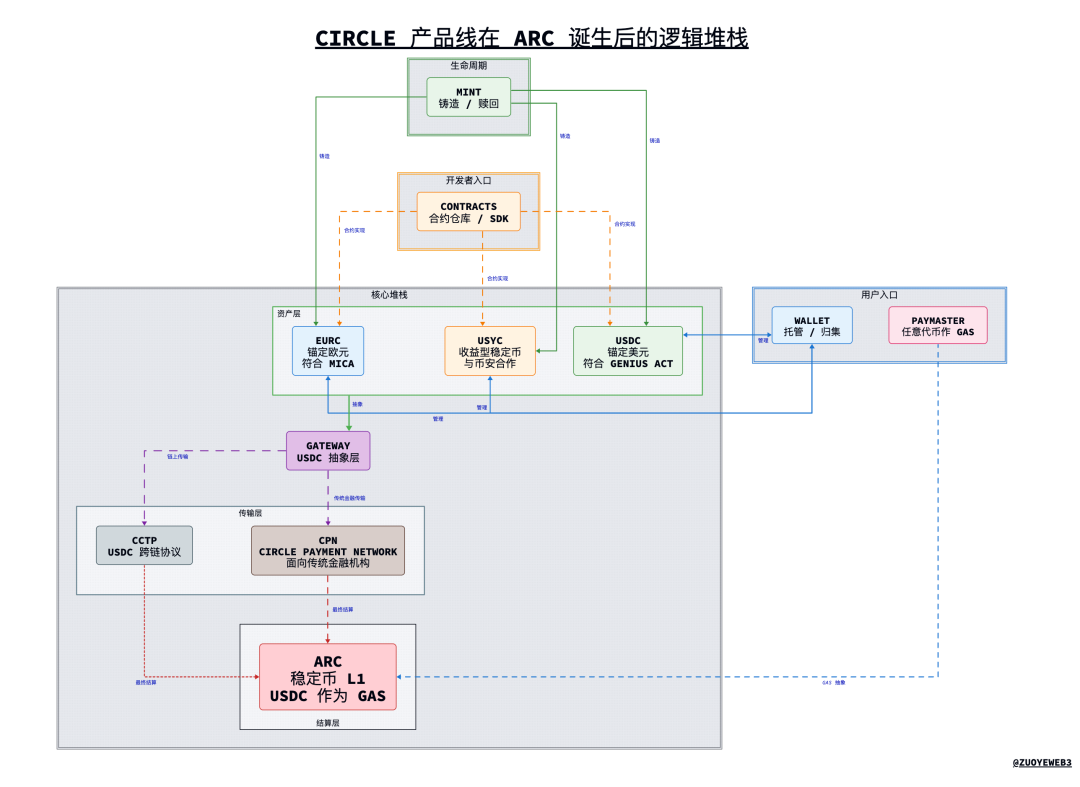

Before issuing Arc, Circle's product line had already diversified, even becoming somewhat complex. Only under the unified organization of Arc could it potentially exert synergistic effects, allowing USDC to escape the awkward position of being an appendage to Coinbase.

Image Description: Logic Stack of Circle's Product Line After the Birth of Arc

Image Source: @zuoyeweb3

Taking Arc as an example, we can glimpse the technological architecture of future stablecoin public chains. It should be noted that the above is merely my personal understanding of the logical architecture and does not necessarily represent the actual situation (universal disclaimer).

- Product Description

• USDC/EURC/USYC: Circle's three main stablecoin product lines, USDC is pegged to the dollar and complies with the Genius Act, EURC is pegged to the euro and complies with MiCA regulations, and USYC is a yield-generating stablecoin that collaborates with Binance.

• CPN (Circle Payment Network): A cross-border clearing network initiated by Circle based on USDC, similar to SWIFT.

• Mint: Users can mint USDC and other stablecoins here.

• Circle Wallet: Individual and institutional users can manage various Circle stablecoins in one place.

• Contracts: Contracts for stablecoins like USDC written by Circle.

• CCTP: Cross-chain technology standard for USDC.

• GateWay: An abstraction layer for USDC, allowing users to interact directly with USDC without needing to know the underlying public chain and technical details.

• Paymaster allows any token to serve as a Gas token.

• Arc: A stablecoin Layer 1 initiated by Circle, with USDC as the native Gas Token.

- Logical Stack

• The main part: divided from top to bottom into: USDC/EURC/USYC -> Gateway -> CCTP/CPN in parallel, with CCTP mainly used on-chain and CPN primarily promoted in traditional financial institutions -> Arc.

• Viewing the main part as a whole, Mint is the recharge entry, Wallet is the fund aggregation entry, Contracts are the programming entry, and Paymaster is a functional feature that allows any token to be used as a Gas token.

Under a mechanism named PoS, which is actually DPOS, Arc can theoretically achieve 3000 TPS with a maximum of 20 nodes and sub-second transaction confirmation times, with Gas Fees potentially as low as below $1. It also thoughtfully prepares privacy transfer and vault modes for institutions, ready to accommodate large-scale corporate funds on-chain, which may also be a significant reason for Circle to build its own L1. Beyond stablecoin trading and transfers, enterprise-level asset management is also a key area of competition.

Moreover, the universal L1 architecture reserves interfaces and full-function architecture for more assets like RWA to go on-chain. Malachite, developed from CometBFT by Informal Systems, which was acquired, theoretically has the potential for 50,000 TPS.

Next comes the familiar EVM compatibility, MEV protection, FX (foreign exchange) engine, and trading optimization. It can be said that with the support of Cosmos, launching products at the level of Hyperliquid technically faces no bottlenecks; if it were L2, the difficulty would not exceed deploying Docker instances.

In Arc's plan, cryptographic technologies such as TEE/ZK/FHE/MPC will all be integrated. It can be said that today's technological diffusion makes the startup costs of public chains incredibly close to a constant; the challenge lies in ecological expansion. Building distribution channels and terminal networks took Visa 50 years, the USDT/Tron alliance 8 years, and Tether has already been established for 11 years.

Time is the greatest enemy of stablecoin L1, so stablecoins have chosen a strategy of separating action from words:

• Action: Retail use -> Distribution channels -> Institutional adoption

• Words: Institutional compliance -> Mass adoption

Whether Tempo or Converge, both target institutional adoption, while Arc strongly promotes a path of global compliance. Compliance + institutions is the GTM strategy offered by stablecoin L1, but this is not the whole story; stablecoin L1 will promote in a more "Crypto" manner.

Plasma and Converge will collaborate with Pendle, and Circle is subtly promoting the 24/7 exchange of yield stablecoins USYC and USDC. Tempo is led by Matt Huang, founder of Paradigm, with a core focus on being more blockchain-oriented rather than more fintech-oriented.

Institutional adoption has always been a means of compliance. Just as Meta claims to protect user privacy, in real business, there must first be users to drive institutional adoption. Let’s not forget that USDT's earliest and largest user base has always been ordinary people in Asia, Africa, and Latin America, and now it has also entered the institutional spotlight.

Distribution channels have never been a field where institutions excel; the grassroots marketing army is the true foundation of the internet.

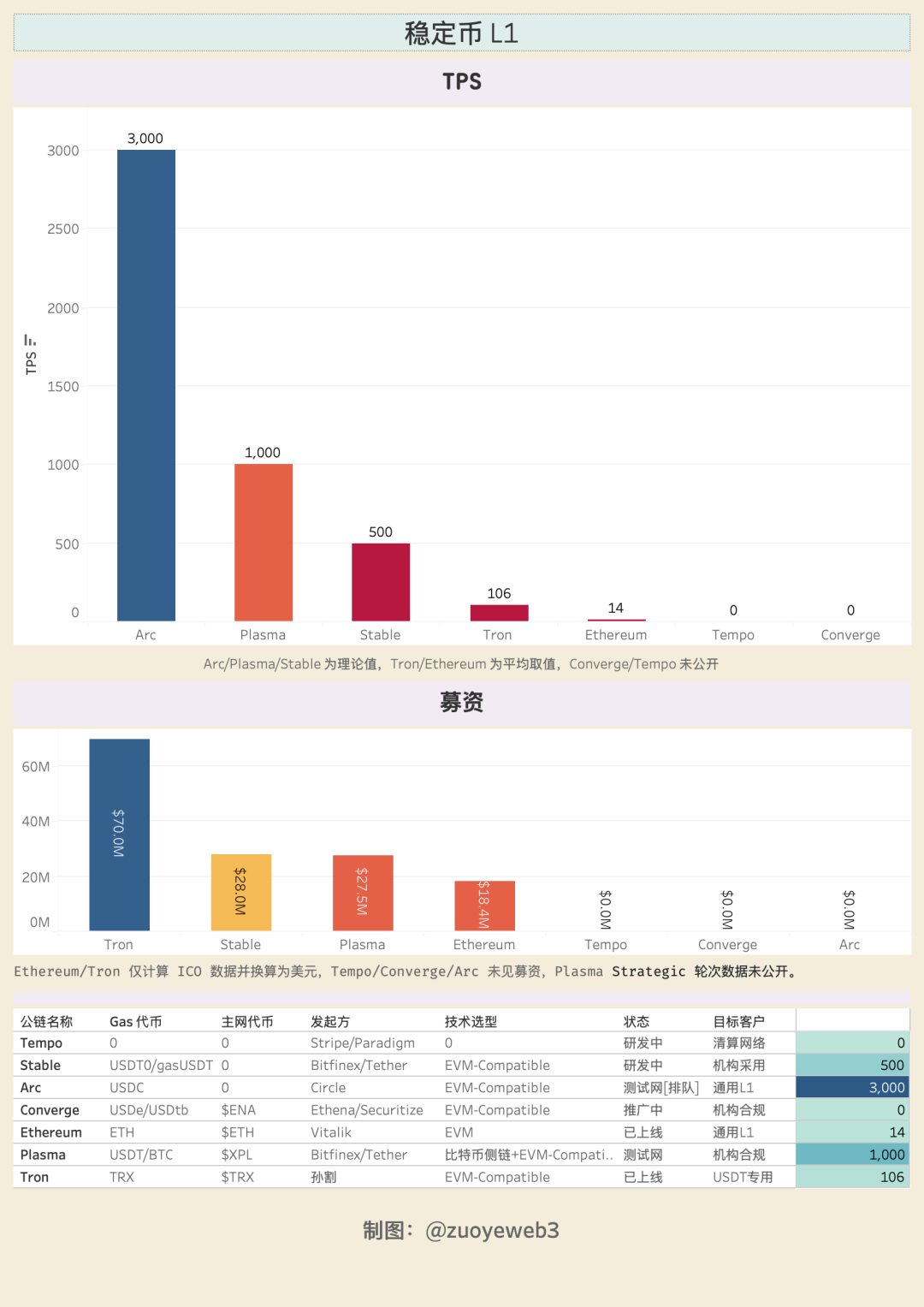

Image Description: Comparison of Stablecoin L1

Image Source: @zuoyeweb3

Emerging stablecoin L1s either raise significant funds or are backed by strong entities. Under the regulations of the Genius Act and MiCA, they cannot pay interest to users, nor can they use this to acquire customers. However, USDe has relied on revolving loans to reach a market cap of $10 billion within a month.

The gap between on-chain yield distribution and user conversion leaves market space for yield-generating stablecoins. USDe manages the chain, while USDtb, in cooperation with Anchorage, becomes a compliant stablecoin under the Genius Act.

Yield can greatly promote user adoption, which is a deadly temptation. Beyond the boundaries set by rules lies a good arena for each party to showcase their capabilities.

Conclusion

Before stablecoin L1, TRC-20 USDT was the de facto global USDT clearing network, and USDT was the only stablecoin with real users. Therefore, Tether does not need to share profits with exchanges; USDC is merely its compliant substitute, just as Coinbase is a reflection of Binance on Nasdaq.

Stablecoin L1 is challenging Visa and Ethereum, fundamentally reshaping the global currency circulation system. The global adoption rate of the dollar is gradually declining, but stablecoin L1 has already targeted foreign exchange trading. The market is always right, and stablecoins aspire to do more.

After more than a decade since the birth of blockchain, it is already quite exciting to see innovations in the public chain space. Perhaps the most fortunate aspect is that Web3 is not Fintech 2.0, and DeFi is also changing CeFi|TradiFi, while stablecoins are changing banks (deposits/cross-border payments).

I hope stablecoin L1 continues to be the inheritor of the core principles of blockchain.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。