Key Takeaways

- David Schwartz says the SEC treated XRP as a security by arguing holders expected profits from Ripple’s efforts.

- Former SEC regional director Marc Fagel says the case targeted Ripple’s XRP sales, not the crypto token itself.

- Their dispute centers on whether calling XRP “just code” meaningfully limited the SEC’s legal theory.

The disagreement between Ripple CTO Emeritus David Schwartz and former SEC official Marc Fagel unfolded on X on July 13, centering on whether the SEC challenged only Ripple’s sales practices or effectively treated XRP itself as a security.

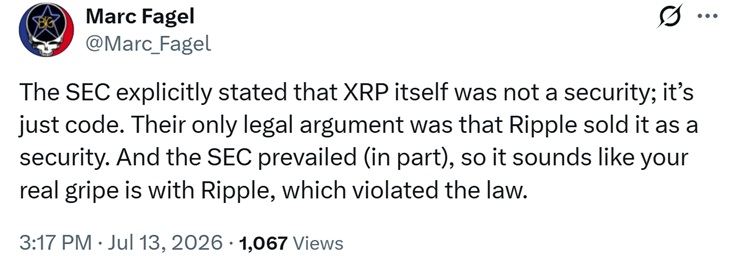

According to the former SEC official, the case “wasn’t against XRP, just Ripple.” He said the SEC recognized that XRP, as code, was not inherently a security. Under that interpretation, the violation arose from Ripple selling XRP under circumstances that created investment contracts.

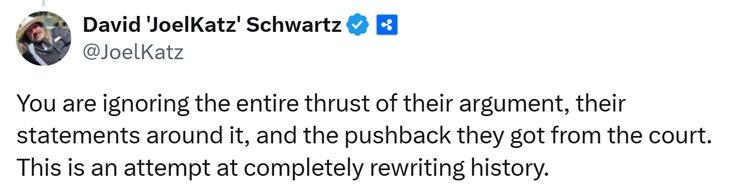

Schwartz rejected that characterization, calling it “a bizarre attempt to rewrite history.” While acknowledging the SEC conceded XRP was not a security per se, he argued the agency’s broader legal theory still treated XRP as a security by claiming holders expected profits from Ripple’s efforts.

He also stated the SEC’s filings, public statements and the court’s ruling contradicted Fagel’s interpretation and showed that the agency’s argument extended beyond Ripple’s sales conduct.

Marc Fagel, a retired attorney, spent more than 15 years at the SEC and served as Regional Director of its San Francisco office from 2008 to 2013. Across his 28-year legal career, he specialized in securities enforcement and oversaw investigations involving public company disclosures, insider trading and investment advisers.

That background lends weight to his interpretation. He claimed the agency’s “only legal argument was that Ripple sold it as a security.” He also pointed to the SEC’s partial victory, suggesting the criticism should concern Ripple’s conduct rather than an attempt to classify XRP itself as a security.

The Ripple CTO Emeritus rejected that distinction, arguing that describing XRP as “just code” did not concede that only Ripple’s sales methods could create a securities violation. He wrote:

“The SEC is absolutely *not* conceding here that the only issue is whether Ripple ‘sold it as a security’ as you claim.”

“It is merely conceding that XRP is not ‘per se’ a security, that is, would necessarily be a security regardless of any facts and circumstances surrounding it other than its inherent nature as a digital token,” Schwartz clarified.

The rebuttal centers partly on Ripple’s programmatic XRP sales through cryptocurrency exchanges. The SEC alleged those transactions were securities offerings even though buyers generally did not know whether Ripple or another market participant had sold them the tokens.

According to Schwartz, this cannot be explained simply by saying Ripple “sold it as a security.” Buyers in blind exchange transactions were not necessarily exposed to Ripple’s representations or aware of the seller’s identity.

Instead, he said, the SEC used a broader Howey theory under which XRP holders joined a common enterprise and reasonably expected profits from Ripple’s efforts. That argument connected buyers to Ripple without requiring a direct contract or an identifiable company sale. Schwartz stressed:

“The SEC absolutely argued that holders of XRP reasonably expected profits from Ripple’s efforts and were in effect partners in a shared venture.”

He maintained that only such a broad theory could encompass exchange sales.

For Schwartz, the phrase “just code” carries less legal significance than Fagel suggests. The concession established only that XRP was not automatically a security because of its technical characteristics.

It did not establish that the SEC’s securities theory depended solely on how Ripple sold XRP. Instead, he said, the agency linked its investment-contract analysis to XRP holders, Ripple’s activities and expectations of profit.

He further argued that the SEC resisted separate analyses for different XRP transactions, relying instead on one Howey theory for institutional sales, exchange sales and other distributions.

To support that interpretation, Schwartz cited the language used in the SEC’s complaint and public statements, which referred to XRP itself as the security and described Ripple executives Brad Garlinghouse and Chris Larsen as “security holders.” He shared:

“The complaint itself frequently refers to XRP itself as the security. The SEC’s press release complained Ripple ‘sold XRP’ without a registration statement. It described Chris and Brad as ‘security holders’.”

The court ultimately made distinctions the SEC had resisted, finding that certain institutional sales were investment contracts while Ripple’s programmatic exchange sales were not. Schwartz views that partial rejection as evidence that the court narrowed the agency’s broader theory.

That disagreement remains central to the case’s legacy. Future courts applying the reasoning in the Ripple ruling will help determine whether the decision is understood primarily as a transaction-specific analysis or as a broader rejection of the SEC’s attempt to link exchange buyers to Ripple’s continuing efforts.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。