One day, all assets will be tokenized.

Written by: WallStreetBets

Translated by: Luffy, Foresight News

Over the past decade, the cryptocurrency industry has built a trading system for native crypto assets: spot exchanges, perpetual contracts, stablecoins, lending protocols, and a complete ecosystem of Meme coins. This has also cultivated a whole generation of users who have long been accustomed to entering the market at any time, having global liquidity, and operating in a trading market unbound by the 4 PM closing time of U.S. stock markets.

In my view, the next super track for the cryptocurrency industry will be migrating traditional physical assets to the underlying blockchain. Stocks, U.S. Treasuries, public mutual funds, gold, crude oil, and credit products will all be brought on-chain.

Assets like gold and Nvidia do not require additional explanations; the real transformative opportunity in the market lies in changing the public's trading channels, trading hours, and the various operational methods after acquiring the assets.

The financing of SpaceX, under Elon Musk, and the trends in the secondary market have already demonstrated a new model of asset circulation. The same asset can have liquidity generated simultaneously in traditional brokerages, the private market, and cryptocurrency platforms. Traditional brokerages receive IPO subscription intentions, private platforms open early shares to qualified investors, while the cryptocurrency sector launches perpetual contracts for SpaceX IPO and tokenized related products, matching traders' expectations for the opening price of the stock at listing.

In the early stages, some derivatives could not meet market demand due to insufficient circulating shares of the underlying assets. Traders would go through brokerages, private deals, perpetual contracts, and tokenized products just to gain exposure to related assets.

This is exactly the core trend that most people overlook; the source of the assets can come from the traditional financial system, but the boundaries of trading and circulation will completely break through traditional frameworks.

Stablecoins have already completed the on-chain migration of the U.S. dollar, allowing capital to circulate freely globally, and settlements can occur even during the bank's off-hours. Today, stocks, funds, and commodities are developing along the same path.

Why is the tokenization wave exploding now?

For years, asset tokenization has remained at the conceptual level. Larry Fink, CEO of BlackRock, compared the traditional financial system to postal letters, with tokenization being the email. Subsequently, BlackRock launched the BUIDL fund, with underlying assets including cash, U.S. Treasury bills, and repurchase agreements. Investors hold tokens worth a stable 1 U.S. dollar, and earnings are distributed in the form of newly issued tokens; compliant investors can transfer holdings between on-chain wallets.

Franklin Templeton has already deployed government money market fund infrastructure on-chain, with the product named BENJI. Now, BENJI is further expanding its services, collaborating with multiple banks and digital asset platforms for trading and collateral financing.

These underlying asset categories have already existed; tokenization alters the method of asset ownership registration, the speed of holding transfers, and the financial scenarios available for reuse after issuance.

Robinhood has launched over 200 U.S. stock and ETF tokens for EU users, covering assets like Nvidia, Apple, and Microsoft, with tokens supporting unbroken transactions five days a week.

Plume Network focuses on the asset issuance side, providing asset management institutions with a one-stop on-chain asset infrastructure without needing institutions to build the entire system from scratch.

TheoriqAI operates above the issuance layer, creating various investment strategies that deploy tokenized assets into on-chain lending and treasury value-added scenarios.

A few years ago, the industry was still debating whether large traditional financial institutions would adopt public blockchains; today, the answer is clear: major institutions have already put it into practice.

Robinhood CEO Vlad Tenev recently stated that the biggest opportunity in the cryptocurrency industry is not to create more native cryptocurrencies but to become the underlying infrastructure for physical assets. Tokenizing stocks, futures, and private market assets is precisely the intersection of traditional finance and cryptocurrency convergence.

Robinhood's major expansion into tokenization has also brought this topic out of the crypto circle and into the public eye.

Airbnb CEO Brian Chesky has indicated that he has been focusing on the tokenization track for many years: "The key highlight is not the tokens themselves, but the significant reduction in trading friction."

This is also the core reason why the topic of tokenization is heating up rapidly. The market is not chasing the concept of "tokenization," but rather a new financial product with zero friction. The industry discussion focus has shifted from "Can assets be tokenized?" to "Which tokenized products can retain long-term users?"

Asset tokenization is technologically feasible, but the real challenge lies in the continued retention of users.

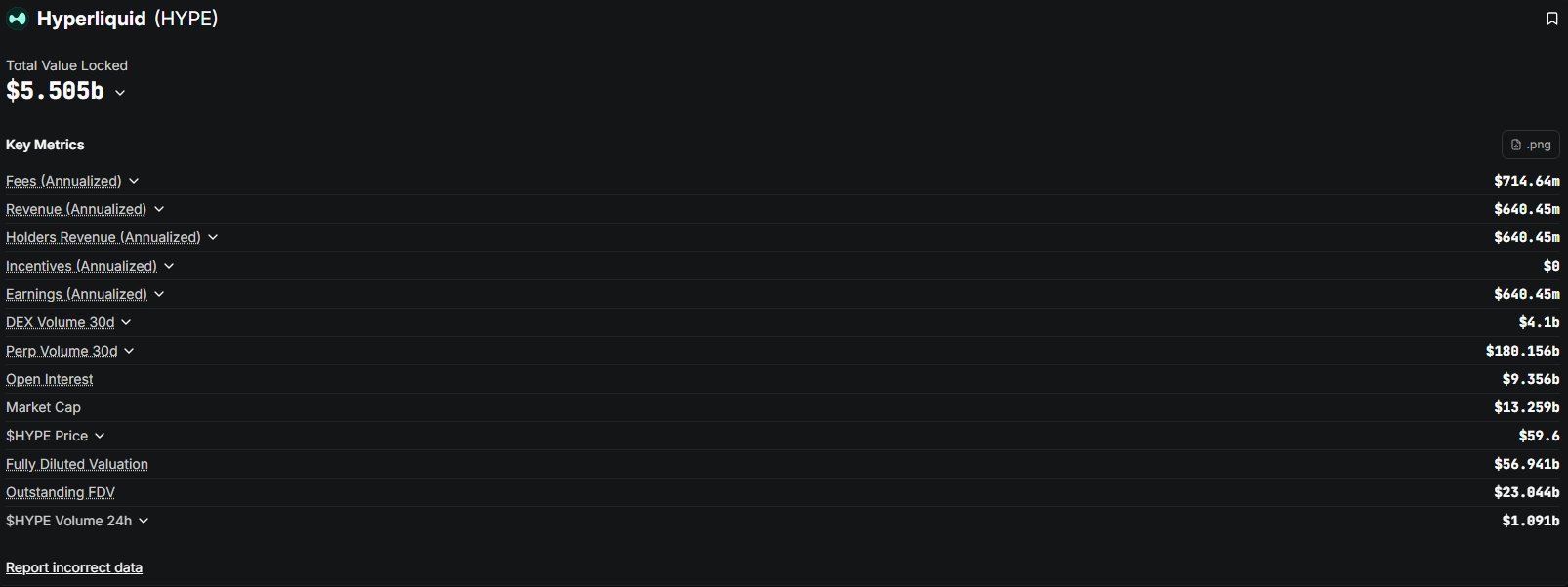

Hyperliquid proves that round-the-clock trading has become a market necessity

HyperliquidX confirms that traders actively flock to efficient, highly liquid, year-round trading platforms.

Perpetual contracts were the first category to be realized, as they belong to synthetic assets that do not require resolving custody, clearing, or various regulatory and legal challenges at once, allowing for rapid listing of targets.

The process for bringing physical assets on-chain is more cumbersome; custody, clearing, and regulatory rules in various countries need to be matched and implemented.

The perpetual contract market has already validated the strong demand for 24/7 uninterrupted trading, prompting the industry to explore more market structures that can be migrated on-chain.

Synapse Protocol is building the underlying for options trading. Its portfolio margin system allows market makers to use Hyperliquid perpetual contract holdings as margin for options sellers, hedging against the price volatility of the underlying assets. This mechanism is particularly friendly to emerging assets. Hypercall has launched SPCX options, supporting intraday and same-day expiry contracts, providing trading exposures that cannot be realized on Nasdaq.

Ondo Finance has expanded this model to the public market. Ondo Global Markets integrates tokenized U.S. stocks and ETFs into crypto wallets, using stablecoins as the trading medium; Ondo Perps provides traders with around-the-clock leveraged exposure, relying on the Ondo ONE system.

Crypto users are already familiar with this operational logic: deposit stablecoins, choose the target, and complete the transaction. The existing challenge in the industry is that once tokenized assets are deposited into wallets, sufficient liquidity and diverse value-added scenarios need to be established to retain users.

Stocks, the most easily popularized consumer-level token assets

SpaceX, Nvidia, Tesla, Apple, Microsoft, Coinbase, Robinhood, and the S&P 500 index are all well-known targets. This is also the core reason why major exchanges prioritize the layout of stock tokens.

Robinhood first launched U.S. stock and ETF tokens for EU users, and subsequently developed its own dedicated public chain, upgrading its business from trading stock tokens within the app to a foundational network that carries the circulation of various on-chain assets. Robinhood has also successfully pushed stock tokens to a massive base of retail investors outside the crypto circle.

Before stock tokens became the core narrative of the cryptocurrency industry, projects like Streamex had already deeply cultivated this track.

Bitget is a representative case that intuitively demonstrates the complete ecosystem of integrating tokenized stocks into cryptocurrency exchange accounts. Bitget launched "Stock 2.0," issuing rToken tokens through the compliant RWA protocol Reality. The platform claims that rToken addresses multiple pain points in the industry: direct connection to Nasdaq and NYSE liquidity, 1:1 pegging to underlying targets, synchronizing corporate dividend distributions, and completing the entire clearing process within the Bitget ecosystem.

rNVDA and rTSLA are the most straightforward examples: the well-known stocks of Nvidia and Tesla are no longer held in traditional brokerage accounts but have been included in cryptocurrency trading accounts.

Ordinary investors can also purchase Nvidia and Tesla through traditional apps, with the main change being the storage scenario after asset purchase. In traditional brokerage accounts, stock assets are isolated within the brokerage's proprietary system; in cryptocurrency exchange accounts, compliant stock tokens can share the same pool of funds as spot, margin, grid trading, copy trading, and wealth management products, with dividends automatically converted to USDT and credited to the account balance.

Holdings are directly counted towards available trading funds, rather than being separately isolated in brokerage accounts.

Bitget believes that when stock tokens coexist with crypto spot, collateral, and various derivatives in the same account, the utilization value of the assets will be significantly enhanced.

Bitget executive Gracy stated that direct connections with traditional brokerages can address liquidity and dividend issues, while Bitget achieves the same advantages through tokenization, while preserving the full range of use cases for assets in cryptocurrency accounts.

The cryptocurrency trading app Fomo is closer to ordinary users, integrating crypto assets and physical asset exposure into the same mobile trading interface, primarily responsible for product distribution and target exposure, without participating in asset issuance and underlying trading infrastructure.

The RWA ecosystem on Solana

In just six months, the cumulative transaction amount of physical assets launched on Solana based on the Sunrise protocol has exceeded $3.5 billion, with 14 million transactions covering about 221,000 wallet addresses.

Sunrise employs the Wormhole native token transfer framework to deploy specified assets from issuers to Solana. Wallets, aggregators, and liquidity platforms can uniformly connect to the same asset address without needing to split multiple wrapped versions to redirect liquidity.

The SPCX tokenization product perfectly confirms this operational logic. Backpack Securities is responsible for compliant issuance, and on the day of SpaceX's listing on Nasdaq, Sunrise simultaneously deployed its tokens on the Solana chain. Within the first 24 hours of launch, that asset traded over $50 million across 51 trading markets on Solana, exceeding $100 million in trading volume within four days.

Backpack handles securities compliance and user asset access, while Sunrise connects to Solana ecosystem traders, liquidity, and cross-chain routing. The cycle from asset issuance to trading has been significantly shortened, but whether the target can maintain trading volume ultimately depends on market demand.

Commodities, a bridge connecting institutions and retail investors

U.S. Treasuries are the most successfully landed category of RWA on the institutional side, with the core advantage being their ability to generate stable returns on-chain; stocks are the optimal targets for the retail side, as Apple, Tesla, Nvidia, and the S&P 500 have a wide audience; commodities lie in between. Institutions use them to hedge risks, pledge reserves, deploy in physical industries, and for macro asset allocation.

Gold, crude oil, silver, copper, natural gas, and mineral rights all fall under the category of commodities. The traditional trading market for commodities has long been mature, and the difficulty has always been providing convenient access channels for ordinary investors.

Holding physical commodities has a very high threshold; ETFs simplify the buying process through brokerage channels, while futures are accessible to professional traders. Tokenization introduces an additional third path, where assets can circulate outside of traditional trading hours, with faster clearing speeds, and can be directly used in various on-chain financial markets.

Not all commodities are suitable for on-chain migration. Crude oil has different benchmarks, storage locations, contracts, and quality standards; copper and natural gas also have challenges regarding physical delivery. Gold has the lowest threshold due to its global circulation, ample liquidity, and unified pricing system, and it has long been widely traded through ETFs and futures; PAXG and XAUT have also proven that users are willing to hold on-chain gold.

Currently, the mainstay of the on-chain RWA market remains U.S. Treasuries, with a simple and clear product logic: hold short-term U.S. Treasuries, and the returns are distributed to token holders.

The on-chain scale of commodities is still relatively small, but their offline spot market size is extremely large.

Gold is an excellent testing ground to verify whether tokenization can optimize the transaction, circulation, and yield distribution models of commodities, rather than just adding a digital credential for underlying assets.

GLDY, a tokenized gold product with interest-earning functionality

As a millennium-valued asset, most forms of gold holding do not generate cash flow returns. The design concept of GLDY directly addresses this pain point: holders of gold tokens can also earn additional gold returns.

Each token corresponds to 1 ounce of standard physical gold reserves. Streamex states that the anticipated dividends will be distributed in incremental gold, with returns sourced from gold leasing businesses; according to data on the Streamex website, the current total reserve of gold is 3096.6072 ounces.

Custodial gold can be leased to compliant enterprises within the gold industry, including refineries, mints, and jewelry manufacturers, with lessees paying leasing fees in gold, and returns distributed to token holders.

The vast majority of tokenized gold products only provide digital custody, while GLDY adds a layer of gold leasing for value addition, forming a completely different return model, unlike simply holding coins in a wallet.

Like all tokenized assets, the survival of the product depends on a complete trading ecosystem: holders need asset verification, regular dividends, compliant trading channels, and a clear understanding of the source of returns.

The platform's Q1 2026 financial report shows that GLDY has an end-of-quarter asset management scale of approximately $14 million, with gold reserves of 3096 ounces; the dividends from the first two monthly distributions amounted to 10.48 ounces of gold to users. Orca and Wintermute are its underlying infrastructure partners.

The platform has collaborated with Siebert Financial and tZERO to connect traditional brokerage channels. Siebert's wealth management and institutional clients can participate in GLDY through existing brokerage accounts, while tZERO provides custody services relying on a compliant digital securities platform. Siebert manages assets exceeding $20 billion, establishing a wide distribution channel outside the crypto circle.

The parent company, Streamex, has been listed on Nasdaq with the stock symbol STEX, allowing secondary market investors to hold platform equity directly. In July of this year, the company's board approved a stock repurchase plan for up to 10 million shares, with a repurchase price ceiling of $2, as management believes the current stock price seriously undervalues the business.

This ecosystem is complete: Orca provides a secondary trading market, Wintermute acts as a market maker providing liquidity, Chainlink reserves data oracle verification for gold inventory, Aurum is responsible for the underlying data, and Siebert connects traditional wealth management client channels.

I continuously monitor three core indicators: the size of gold reserves, the total amount of monthly dividends, and whether secondary market trading volumes can grow steadily in sync. This is also the ultimate testing standard for all tokenized assets.

The token itself is not the product; the core value lies in the complete trading and value-added market built around the token.

Focus on Long-term Observations

I do not believe that the tokenization of physical assets will result in a unidirectional bull market. I am more concerned with innovative products that can fundamentally change the way underlying assets are utilized.

For stocks, I want to see if traders will continue to use the tokenized versions when traditional markets are closed, and whether these positions will play a role in their other portfolios.

For funds, I am observing whether they will move beyond the issuance phase and start being used as collateral or incorporated into other financial products.

Commodities are my primary focus for experimentation. Holding gold tokens in a wallet is easy to understand, but the real challenge is providing sufficient reasons for users to abandon ETFs and traditional futures in favor of on-chain gold tokens.

Will users still be trading a month from now? Can assets be freely transferred across platforms? Will dividend returns grow in sync with the underlying reserves? If all of the above answers are affirmative, then a truly mature new market will have formed.

Five years ago, the industry debated whether traditional financial institutions would accept public blockchains; today, the financial market is gradually adopting crypto technology as foundational infrastructure.

If this trend continues, one day, all assets will be fully tokenized.

The traditional market has fixed closing times, while the crypto market operates year-round.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。