Written by: Rita

Trends Introduction

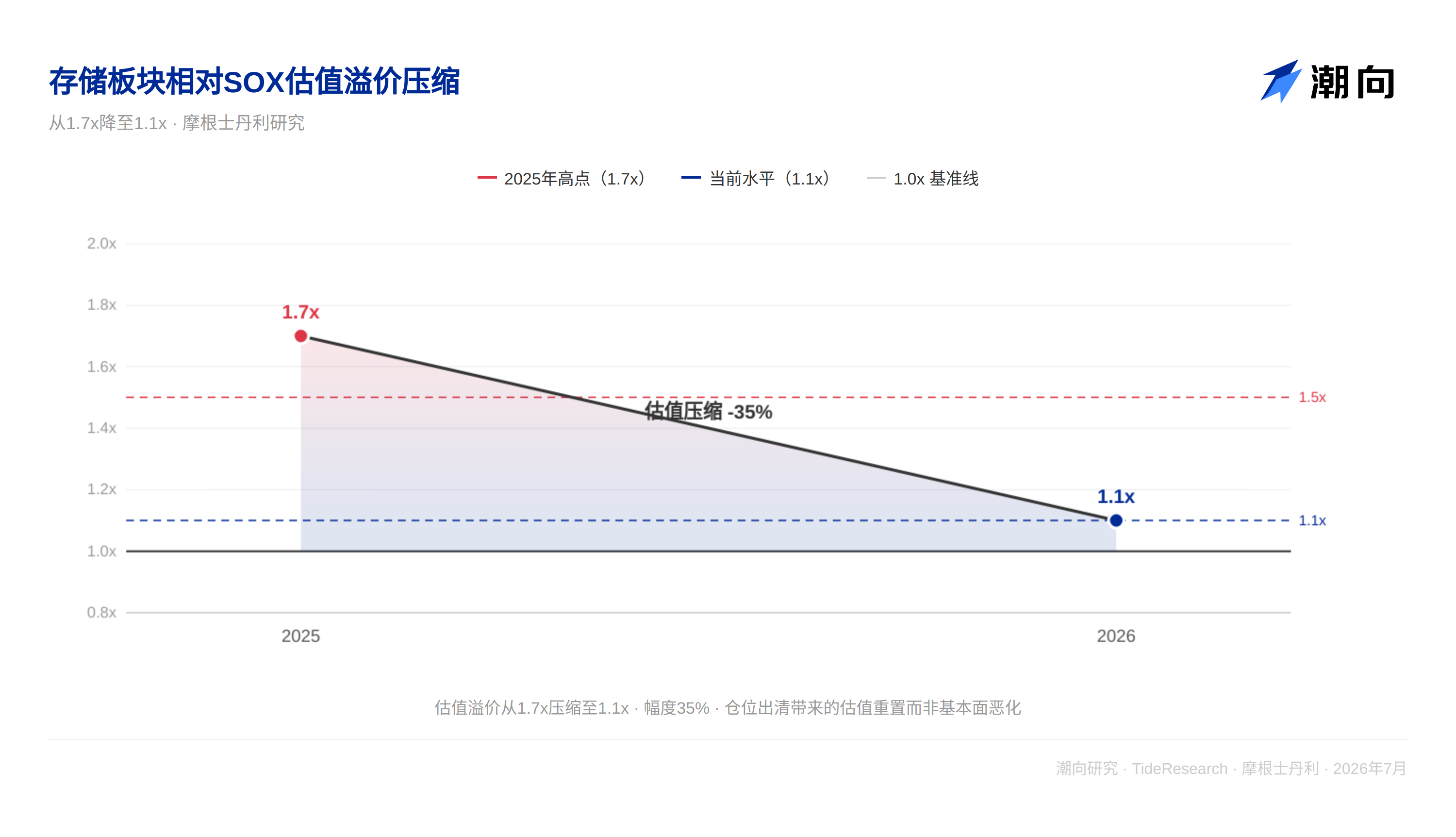

In the past month, Asian storage stocks fell by 15% to 25%, while the chip sector remained flat overall. Memory chips were sold off unilaterally, and the valuation premium between the two quickly compressed from over 1.5 times to 1.1 times.

On July 14, Morgan Stanley provided the assessment during a TMT live broadcast: the fundamentals of storage have not reversed, and the market is completing a shift in pricing anchors.

In the first half of the year, everyone was concerned about "how high prices can go." As the second half begins, the focus is shifting to "how long high profits can last." Three contentious points are influencing this judgment: how much CSP capital expenditure will increase, whether LTA protects profits or limits them, and whether Yangtze Memory will disrupt the supply-demand balance of NAND.

Goldman Sachs concluded that the storage industry is still in the later stages of an upward cycle, but the logic driving stock prices has switched from "price elasticity" to "profit sustainability."

What Happened in the Past Month

Chip stocks fell 15% to 25% while the broader market remained flat, with the SOX index hardly moving, but memory companies were sold off unilaterally.

The fundamentals have not reversed; rather, the valuation framework is in motion. The valuation premium of memory relative to SOX quickly compressed from a high point to 1.1 times, returning to the upper end of the historically reasonable range. The market is transitioning from "chasing price increases" to "verifying profit sustainability," which is a typical characteristic of the later stages of the cycle.

Demand for storage from AI servers is still increasing, HBM capacity remains tight, and the supply-demand gap in traditional DRAM and NAND has not fully closed. However, the market is no longer willing to pay unlimited premiums for "price increase expectations," and it is now demanding evidence that "profits remain stable even after price increases."

Contention One: How Much Will CSP Spend

AI servers are the ultimate source of demand for storage. The capital expenditure figure from CSP is the most important question.

Goldman Sachs estimates that CSP hardware capital expenditure will total approximately $339 billion in 2026 and about $406 billion in 2027, which is 30% and 37% higher than market consensus, respectively. This is the biggest point of divergence between the market and sell-side analysts. Why such a big difference? The land reserves, power approvals, and number of ongoing projects for hyperscale cloud providers are all at historic highs, and these leading indicators suggest that capital expenditure will not peak in 2026.

Whether this expectation can be fulfilled is the biggest variable in the short term. The earnings reporting season starting at the end of July will provide the first verification. If CSP raises its capital expenditure, market confidence in long-term storage demand will strengthen. If the figures are below expectations, the market will question the sustainability of the cycle.

Contention Two: Does LTA Protect Profits or Limit Them

LTA is the topic of greatest divergence among institutional investors.

Concerns center around: after a large number of contracts are locked in, price elasticity will decrease, and the short-term EPS elasticity from price increases will be compressed. This concern is reasonable from a short-term perspective, but the goal of this cycle has shifted from going higher to maintaining for longer.

Goldman Sachs holds the opposite view. LTA provides a floor for profits but does not cap prices. In a non-agreement era, memory manufacturers face the worst-case scenario of price collapse during down cycles. After the introduction of LTA, over half of the contract volume was locked in at agreed prices, significantly reducing the risk of price drops during downturns.

The market's past valuation habits for memory stocks were based on the assumption that "prices will fluctuate dramatically." LTA is starting to loosen this assumption. Once LTA covers a majority of contract volume, fears of a down cycle will be significantly weakened. Goldman Sachs believes the market has not yet fully priced in this change, but it is happening.

Contention Three: Will Yangtze Memory Disrupt the Balance of NAND

Yangtze Memory is representative of China's NAND capacity expansion. Goldman Sachs conducted a scenario analysis: Fab4 and Fab5 each plan about 100kwpm capacity, and once all five fabs are operational, theoretical capacity could account for 24% of the global market share.

The key lies in the method and timing of capacity deployment, not just the numbers themselves. If Yangtze Memory gradually brings on capacity according to market demand without aggressive expansion, the tight NAND supply and demand could continue until 2028. If the five fabs go into production quickly, the NAND market will face severe oversupply, which could disrupt the pricing structure.

Goldman Sachs believes there is currently no evidence that Yangtze Memory is accelerating capacity expansion. However, this is a variable that needs continuous monitoring. If Chinese companies obtain more advanced technology nodes, or if external conditions change, the speed of capacity release could alter the entire market's supply and demand landscape.

Trends Perspective

The pricing logic of storage stocks is shifting from "cyclical goods" to "stable profit goods." The past decade's habit was to "give high prices when prices go up and floor prices when they go down," because everyone knows both increases and decreases can be drastic. However, the popularity of LTA is flattening the volatility. Once more than half of the contracts are locked in by agreements, fears of down cycles will disappear.

Goldman Sachs's live broadcast on July 14 was essentially saying one thing: the storage cycle is still alive, but the driving force has changed. In the first half of the year, it was "price elasticity"; in the second half, it is "profit sustainability." CSP determines the demand ceiling, LTA determines the profit bottom line, and Yangtze Memory determines the supply risk.

Three variables all point in one direction: the downside risk of storage stocks is smaller than in historical cycles, and the upside elasticity is also weaker than in historical cycles. The market's divergence lies in whether this combination is positive or negative. Goldman Sachs's view is clear: storage stocks are transitioning from "cyclical high volatility" to "structural medium to high returns," and the market has not yet fully realized that this change signifies a fundamental shift in valuation methods.

Now the question is, how many companies can pass this threshold.

Disclaimer

This article is a整理与解读 of the third-party brokerage research report (Morgan Stanley, July 14, 2026) by潮向研究. The ratings, target prices, profit forecasts, and related judgments quoted in this article are all the opinions of the brokerage analyst and represent the position of their respective institution, not the views of潮向研究, and do not constitute any investment advice.

The market has risks, and decisions should be made independently. This article should not be used as the basis for buying or selling any securities.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。