BitMine lost all profits directly through options trading.

Written by: Oluwapelumi Adejumo

Translated by: Chopper, Foresight News

BitMine is strongly positioning itself in Ethereum holdings, attempting to turn it into a stable cash flow source, with nearly $46 million generated from staking operations last quarter.

However, the $92.1 million loss from derivative options completely offset staking profits, compounded by continuously rising asset management costs and the company’s aggressive stock issuance, significantly compressing the profit space for original shareholders.

The third-quarter financial report for the 2026 fiscal year, ending May 31, showed the company’s revenue skyrocketed from $2.1 million in the same period last year to $46.5 million; of which 98% ($45.7 million) came from staking and node validation services. BitMine is accelerating its divestment from Bitcoin mining operations and fully transitioning to Ethereum holding models.

Despite the significant revenue increase, the company recorded a net loss of $83.6 million for the quarter, compared to a slight loss of $623,000 during the same period last year, with losses expanding sharply.

Massive options loss wipes out all Ethereum staking earnings

The core factor dragging down this quarter's performance is the company’s Ethereum derivative options trading strategy. BitMine reported a total loss of $92.1 million from Ethereum-related derivatives this quarter, approximately double the total revenue from staking operations during the same period. Of this, $78.6 million came from unrealized losses on options contracts, and $14 million from losses on exercised positions. The $534,000 gain from open contracts can barely offset some losses.

In the same period last year, the company had not engaged in any derivative trading, leading to a qualitative leap in asset management risk exposure. In the first nine months of the fiscal year, accumulated losses from derivatives reached $133.3 million, with $79.3 million from exercise losses and $54.5 million from expired contracts, and only $515,000 in profit from open contracts. During the same period, staking and validation services generated merely $56.9 million, with derivative losses exceeding staking revenue by more than twice.

BitMine stated that its options strategy primarily involves selling put options, as part of an overall position management plan. Selling put options can earn premiums and increase asset holdings at dips, but if market conditions reverse and contracts are exercised under unfavorable conditions, it can lead to massive losses. This major loss clearly illustrates that attempts to enhance earnings through options have currently completely offset the stable income generated from node staking services.

Meanwhile, the company's administrative and general management expenses skyrocketed from $744,000 during the same period last year to $37.3 million. Management explained that the increase was mainly due to digital asset custody and asset management service fees, salary increases, and the rise of cash and stock compensation for directors.

Excluding the valuation changes of crypto assets, staking revenues were sufficient to cover this quarter’s sales and management costs. Even after deducting multiple non-cash items, the company's adjusted net loss under non-GAAP measures still reached $70.8 million. This financial report indicates that the node validation business has formed a considerable and stable cash flow, but the overall trading strategy continues to consume staking profits.

Continuous issuance of BMNR stock hoarding Ethereum dilutes shareholder equity significantly

The funds used by BitMine to massively hoard Ethereum almost entirely came from public market issuances of common stock, and the costs were entirely borne by existing shareholders. As of May 31, during the nine-month period, the company had cumulatively sold 340.7 million shares of BMNR common stock through an off-market issuance plan, raising $11.87 billion after deducting issuance costs; during the same period, it spent $11.69 billion to purchase Ethereum.

Shareholder equity has been massively diluted. The number of circulating common shares increased by 149% over nine months, growing from 232.4 million shares on August 31, 2025, to 579.7 million shares by the end of May 2026; further issuance continued after the quarter ended, with total shares reaching 603.2 million as of July 9.

Thanks to equity financing, BitMine held a total of 5.42 million Ethereum as of May 31, with a total holding cost of $19.05 billion; by the time of writing, the holdings had increased to 5.7 million Ethereum.

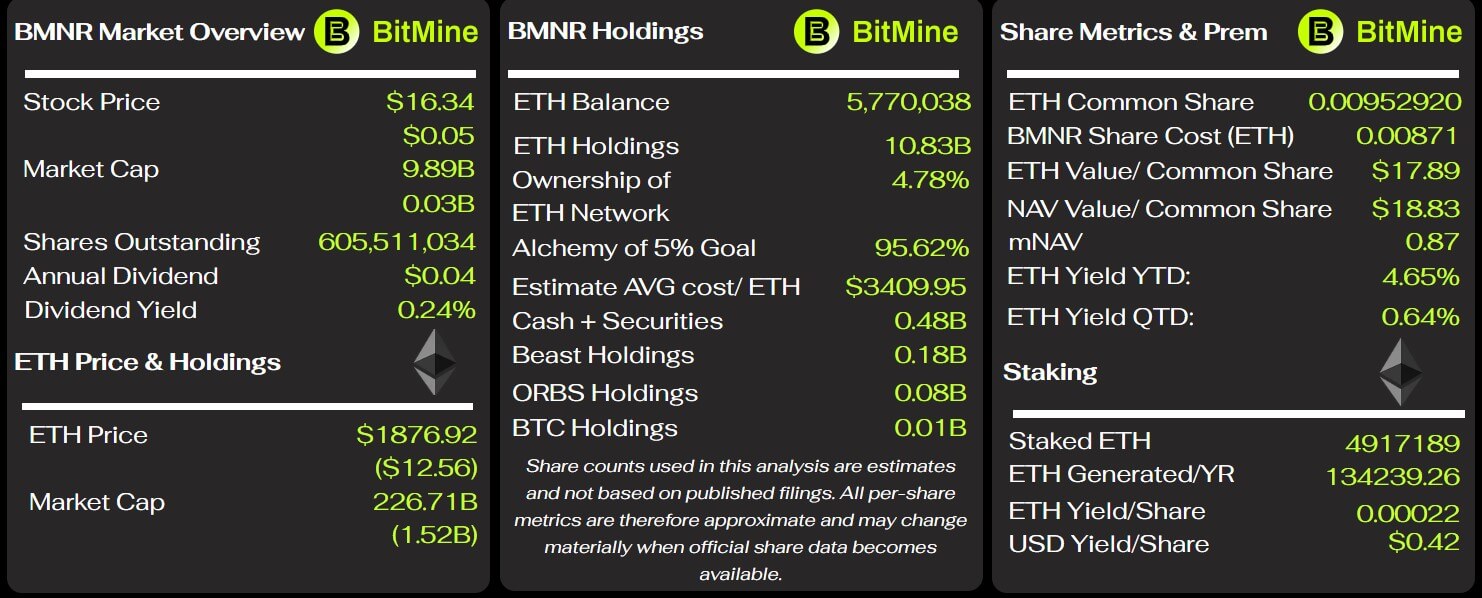

Key metrics for BitMine, source: BitMine Tracker

At the end of May, the market value of these Ethereum holdings was only $10.86 billion, with an unrealized loss of about $8.2 billion, representing a loss margin of 43%.

This impairment of holdings is the main source of the company's $9.04 billion unrealized losses on digital assets in the first nine months of the fiscal year, during which the company accumulated a net loss of $9.1 billion. The massive unrealized loss directly reflects BitMine's high-cost stock purchases of Ethereum, with all risks borne by shareholders.

In January this year, the annual shareholder meeting approved raising the company’s authorized common stock limit from 500 million to 50 billion shares. This authorization does not mean the company must issue shares in full but provides management ample room to continue issuing stock for purchasing digital assets and other investments.

BitMine indicates that its ability to expand Ethereum holdings depends heavily on maintaining open financing channels. A decline in Ethereum prices, a weakening company stock price, or decreased investor subscription willingness could elevate future financing costs and even restrict the company from issuing securities under favorable conditions.

This business model's supporting conditions extend beyond staking annualized returns and anticipated price increases for Ethereum; it also requires shareholders to accept significant equity dilution, enduring long-term floating losses in the tens of billions, to continuously provide funds for the company's hoarding of cryptocurrencies.

Long-term service contracts elevate staking operational costs, compress profit space

BitMine relies on staking operations to hedge against position price fluctuations, but accompanying long-term cooperation agreements incur fixed costs and revenue sharing that continually compresses overall profits. The company signed a ten-year consulting agreement with the third-party service provider Ethereum Tower, spending $12.8 million this quarter for this purpose, accounting for approximately 28% of the current total staking revenue. Cumulatively, in the first nine months, this expense reached $37.5 million; the company estimates annual costs between $40 million and $50 million, based on a tiered fee structure according to the total value of the managed digital assets.

This agreement can only be terminated under a few specific conditions. If BitMine terminates the collaboration without just cause, it must pay Ethereum Tower 85% of the estimated service fees for the remaining contract period.

Additionally, after acquiring node operator Pier Two, BitMine signed another ten-year management service agreement. The agreement stipulates that Ethereum Tower receives 2% equity in the MAVAN platform and receives a monthly share based on the native staking rewards percentage of the platform. As of May 31, the company had not yet accrued expenses related to this agreement, and the sharing costs have not yet appeared in the profit statements of the staking business.

BitMine stated that the vast majority of Ethereum is staked through MAVAN, and in the long term, staking rewards will adequately cover asset custody costs. Focusing solely on operational aspects this quarter, staking income does indeed cover sales and administrative expenses excluding valuation changes of crypto assets. However, the ten-year fixed consulting fees, future revenue sharing, and various comprehensive asset management expenses combined mean that relying solely on staking income is insufficient for a complete assessment of the business's real profitability.

BitMine has no debt but is increasingly dependent on capital markets

At the end of May, BitMine's asset-liability structure showed extremely low leverage, with $340.3 million in cash and $433.1 million in working capital, and no traditional debt. The company reported total assets of $11.63 billion and total liabilities of only $30.1 million, with the vast majority of assets comprising digital assets like Ethereum. From the balance sheet, the company does not face an immediate repayment crisis, but cash outflows from operating activities reached $287.6 million in the first nine months. The company states that the cash consumption mainly stems from legal, consulting, and investment banking expenses related to the expansion of Ethereum holdings.

After the end of the quarter, BitMine issued an additional 3.5 million shares of perpetual preferred stock BMNP with an annualized yield of 9.5%, raising $273.8 million. This issuance temporarily supplements liquidity, but the new annual $33.25 million preferred stock dividend is a rigid expense. This security is classified as equity rather than debt, but its repayment priority is higher than that of common stock, and the high dividends continue to occupy the company’s cash flow.

Management believes that existing cash, expected operating cash flows, and market-based issuance tools are sufficient to support the company’s operations for at least the next 12 months. This assertion hinges on the premise that capital markets remain open for financing: if Ethereum's market stays low for a long time, the company's stock price weakens, and investor willingness to subscribe declines, the company’s financing costs will rise, limiting operational flexibility.

In summary, according to the latest financial report, BitMine currently faces a set of contradictory realities: on the one hand, the company has built a mature staking business that generates tens of millions of dollars in quarterly revenue, which can cover core operational expenses; on the other hand, substantial losses from options trading completely engulf staking profits, long-term cooperation contracts continuously elevate management costs, and the expansion of Ethereum hoarding completely relies on stock issuance, with total share capital having more than doubled.

Therefore, BitMine's long-term economic benefits depend on whether staking income can stably cover various asset management costs and options losses, the company's ability to continuously and stably attain equity financing, and whether Ethereum prices can significantly rebound.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。