Author: ChainFeeds

Translator: Deep Tides TechFlow

Deep Tides Introduction: This article summarizes the four most important research observations in the recent crypto market: the failure of Ethereum's value capture, BlackRock warning that AI valuations have reached the halfway point, Multicoin's heavy investment in Zcash and HYPE, and why Wall Street is rejecting ChatGPT. For investors seeking to understand the logic of current cycle allocations, these four judgments are directly related to whether you should still hold ETH, how much longer AI stocks can increase, and whether there is a genuine demand for privacy AI tracks.

Comprehensive Analysis of the Ethereum Ecosystem: What Changes Have Occurred in Investment Logic?

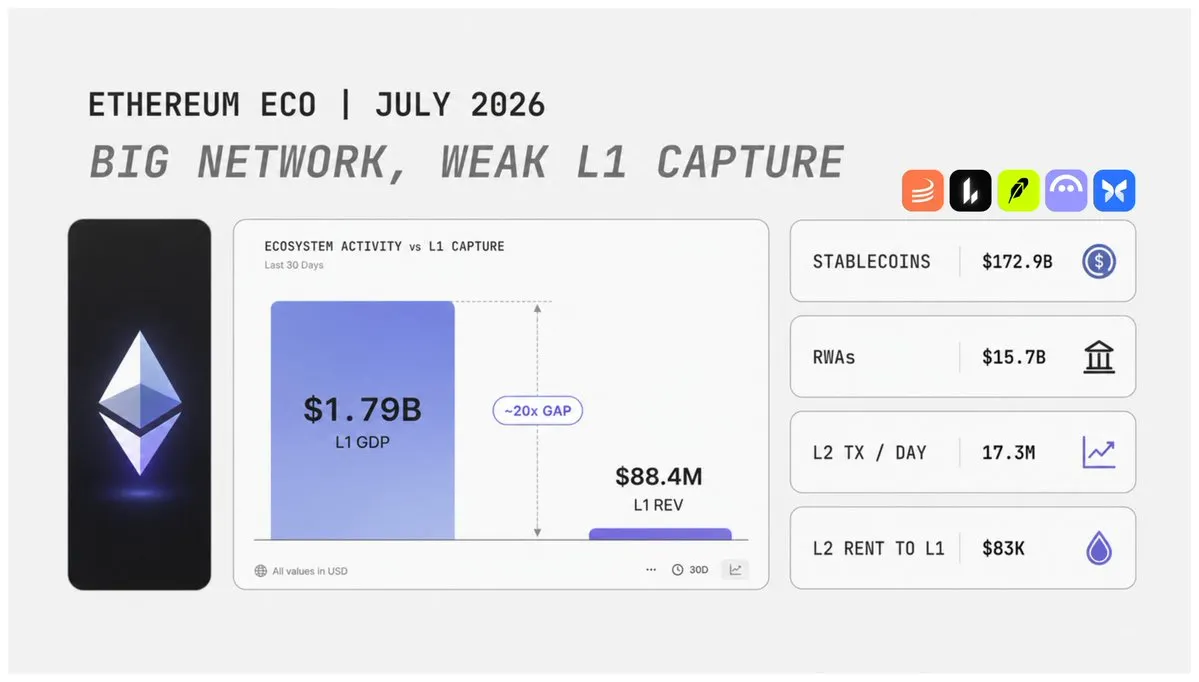

Nick Researcher re-examines Ethereum from a macro and financial perspective. Data for the second quarter of 2026 reveals a complex signal: Ethereum's revenue improved slightly from the previous quarter, but the fee capture ability of L1 (mainnet) remains far below last year; on-chain yields are approaching historical lows; DeFi activity has declined; the L2 (Layer 2) ecosystem continues to expand, with projects like Robinhood starting to develop based on Ethereum-related infrastructure, yet these activities have not contributed enough value to L1; meanwhile, the dilution rate of ETH remains close to Bitcoin's level.

The biggest controversy regarding ETH currently is that Ethereum has not lost its competitiveness, but the past investment logic is changing. Previously, the bullish logic for ETH was quite simple: more users entering Ethereum pushed L1 activity up, generated more transaction fees, resulting in more ETH being burned, thus enhancing ETH's value capture ability. However, this model is weakening. Users are gradually migrating to L2, while some users are leaving the ecosystem due to unmet expectations regarding L2 experience; transaction fees are declining, while the growth rate of Blob supply exceeds demand; although L2 has processed a significant amount of transaction activity, the fees paid to the Ethereum mainnet remain limited.

The most critical data is that, in the second quarter of 2026, the real economic value generated by Ethereum L1 was $88.4 million, a 7% increase from the previous quarter but a 68% decrease year-on-year. Meanwhile, the application layer on Ethereum L1 generated approximately $1.79 billion in fee revenue. This indicates that applications within the Ethereum ecosystem still possess strong economic value, but as a base layer, Ethereum mainnet has captured only a small portion of it. This represents the core contradiction within the current ETH investment logic.

Ethereum still supports numerous important financial activities, including major protocols such as Tether, Circle, Lido, Aave, and Uniswap, all significant participants in the Ethereum ecosystem. Stablecoins remain one of Ethereum's strongest advantages; in the second quarter of 2026, the supply of stablecoins on Ethereum L1 reached $172.9 billion, and although it decreased by about 4% quarter-on-quarter, it still maintains a massive scale. However, scale is not the only key factor; capital flow velocity is also crucial. If stablecoins merely stay on-chain without trading, settling, or being collateralized in financial activities, they do not create sufficient economic value. Currently, Ethereum has a massive asset scale but lacks adequate capital turnover efficiency.

Real-world assets (RWAs) may become an important growth driver for ETH in the next phase. Currently, the on-chain RWA scale on Ethereum L1 has exceeded $15.7 billion, a year-on-year increase of approximately 90%, including tokenized government bonds, commodities, and equity assets. However, simply having higher TVL is not enough to prove value capture ability. In the second quarter of 2026, Solana experienced higher daily trading volumes in RWA than Ethereum, despite having lower RWA TVL, indicating that Ethereum's advantages lie more in institutional depth while Solana's lies in capital flow velocity.

For ETH, the future upward logic requires three conditions to be met simultaneously: first, more institutional assets entering the Ethereum ecosystem; second, more financial settlement activities occurring on the Ethereum network; third, on-chain assets needing to generate higher real transaction frequencies. The token economic model of ETH currently still has advantages, with an annualized net dilution rate of around 0.85%, approaching BTC levels. However, risks also exist, with the total on-chain yield already declining to 2.68%, a historical low, where 94% of yields come from ETH issuance rather than real user fees. This means whether ETH can gain re-valuation in the future depends critically on whether it can become the settlement layer in the institutional financial system.

BlackRock Report: The Current AI Market Has Reached the "Halfway Point" of the 2000 Internet Bubble, One Indicator Has Turned Red

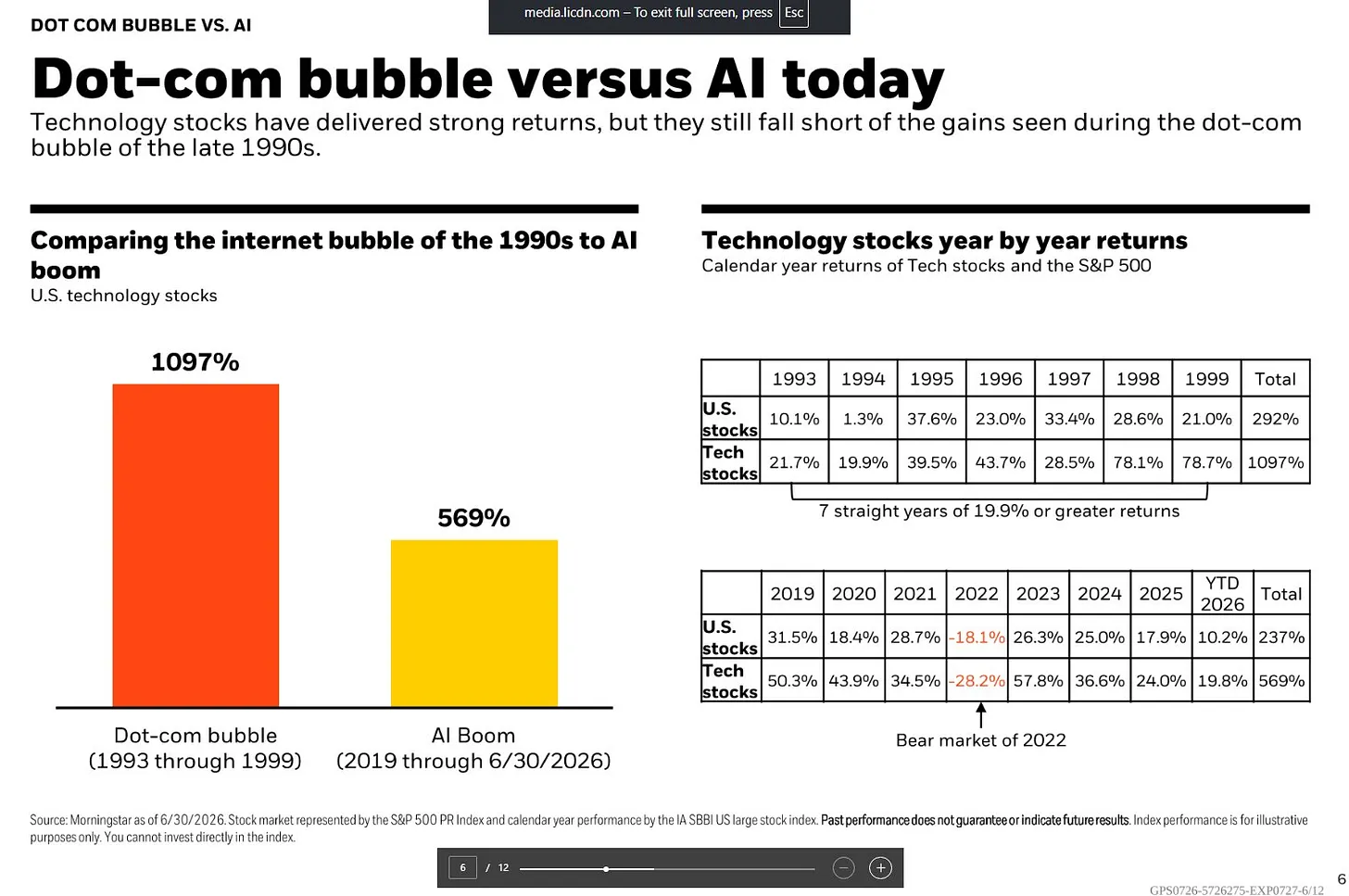

According to BlackRock citing Morningstar data, between 1993 and 1999, U.S. technology stocks gained a cumulative 1,097%, while the overall U.S. stock market rose 292% during the same period. Technology stocks experienced an annualized return rate of no less than 19.9% for seven consecutive years, with particularly impressive gains in 1998 and 1999, reaching 78.1% and 78.7% respectively.

In contrast, during the AI market cycle from 2019 to June 30, 2026, technology stocks have risen a cumulative 569%, and the overall U.S. stock market has increased 237% during the same period. While this round of market conditions has also performed strongly, the rhythm is markedly different. During this period, technology stocks underwent a significant adjustment in 2022, decreasing by 28.2%, followed by a rebound of 57.8% in 2023, with subsequent increases of 36.6% and 24.0% in 2024 and 2025 respectively, and a continued rise of 19.8% in the first half of 2026.

The greatest difference between the two market phases occurs in the later stages: during the Internet bubble period, the market rapidly accelerated in the last two years, with cumulative gains approaching 200% in 1998 and 1999; while the AI market showed a clear acceleration in 2023, but the subsequent increase gradually narrowed. In other words, the current trend of the AI cycle is more stable compared to the Internet bubble, but there remains considerable disagreement in the market about whether it will enter the final phase of frenzied increases.

Current market valuation has become the core of the controversy surrounding the AI market. The Schiller CAPE (Cyclically Adjusted Price to Earnings Ratio) of the S&P 500 has risen to about 40 times, returning to high levels seen during the Internet bubble. This indicator calculates valuation levels based on the average inflation-adjusted earnings over the past decade; 40 times means that investors are willing to pay $40 for every $1 of long-term average profit, a similar level was only observed around the year 2000 historically.

However, BlackRock believes that simply focusing on long-term valuation indicators is not comprehensive; the 12-month forward P/E ratio provides another perspective. Currently, the forward P/E ratio for the S&P 500 is about 21 times, mainly because corporate profit expectations have risen in tandem with stock price increases. Data shows that S&P 500 second-quarter earnings are expected to grow by 23% year-on-year, maintaining double-digit growth for the seventh consecutive quarter. BlackRock believes this earnings growth is quite rare historically. Meanwhile, the current P/E ratio for the Magnificent Seven (Mag 7) tech giants is about 26 times, while profit growth is expected to exceed 30%, with an overall profit growth rate of about 27.6%.

Thus, the biggest contradiction in the current market is that long-term valuation indicators have emitted signals of overvaluation risk, but corporate profit growth continues to support these high valuations.

As of May 31, 2026, according to Morningstar data, technology stocks account for 37.5% of the total market capitalization of the U.S. stock market, exceeding levels seen during the late 1990s Internet bubble. If we further consider companies like Alphabet, Meta, and Amazon, which, while not classified as tech stocks, are deeply involved in the AI industry, the actual concentration of AI-related assets could be even higher.

Current market leadership is also shifting from traditional Mag 7 to a broader range of AI-benefiting companies; a new market concept called MANGOS is taking shape, representing Meta, Anthropic, Nvidia, Google, OpenAI, and SpaceX. Morningstar's Global Next Generation Artificial Intelligence Index rose approximately 45% in April and May 2026, followed by a pullback in June.

Market concentration is one of the aspects where the current AI cycle is most similar to the Internet bubble. At the end of 1999, a handful of tech companies such as Cisco, Intel, Microsoft, and Oracle propelled the last round of Nasdaq increases. Nowadays, while leading AI companies possess stronger profitability, if future profit growth fails to meet market expectations, a highly concentrated investment portfolio could still face rapid adjustment risks.

BlackRock believes that determining whether AI has formed a bubble is itself a significant judgment, as it implies that the market assumes AI cannot lead to long-term productivity increases. The question that investors truly need to focus on has shifted from "How much more can AI increase?" to "How long can AI profit growth be sustained?"

Dialogue with Multicoin Partner: The Crypto Market Has Hit Bottom, and Three Cryptocurrencies Are Promising in This Cycle

Tushar Jain, managing partner of Multicoin Capital, shared his views on the current crypto market and elaborated on the investment logic for Solana, Hyperliquid, and Zcash.

Tushar Jain stated that he still believes Solana is the correct technological architecture for internet capital markets, needing a permissionless open-source chain to consolidate everything onto one platform. He remains optimistic about Solana's performance and architecture. However, at the same time, derivative trading volume is shifting toward Hyperliquid. He currently holds significant positions in both assets and is optimistic about both. Solana is the leader in spot trading and will facilitate the spot trading of tokenized securities, yet Hyperliquid clearly leads in derivatives. Instead of being an extremist for one, it’s better to think from a probabilistic perspective and hold both. He is not a maximalist for any asset and will not stubbornly cling to a certain position or viewpoint.

Looking ahead to 2026, a very clear choice for him is Zcash (ZEC). Although its position is relatively small due to liquidity and market cap restrictions, Multicoin has already accumulated a considerable proportion of the total supply. He likes Zcash's momentum, use cases, and community, reminiscent of early Bitcoin. When he saw it rising last year and communicated with many early supporters, he found that even when the price fell, they still held fast to their beliefs, indicating it’s not a short-term speculative game. Moreover, Zcash has no fundamentals (no cash flow and income), which means its value entirely depends on consensus, giving it even greater upward potential; as a store of value, the larger it is, the better.

Multicoin indeed holds a position in HYPE, but Tushar Jain advises investors to examine their inferred logic and draw their own conclusions. The assumptions they set are not aggressive: first, the CAGR of crypto derivatives is 35% (down from 45% over the past five years, having already slashed a quarter off the growth rate); second, DEX will capture 32% of the derivatives market share (rising from almost zero in 2022 to 16% now, doubling to 32% within two years aligns with trends); third, Hyperliquid will maintain a 30% share in decentralized derivatives (this is conservative because trading volume data can easily be inflated, but currently, Hyperliquid holds 59% of the entire network's real open contracts, which is hard to fake); fourth, USDC collateral will linearly grow with trading volume (as long as traders’ leverage preferences remain constant, the stablecoins used as collateral will naturally grow in proportion to trading and open positions).

At the Crossroads of AI: Why Wall Street Is Saying "No" to ChatGPT and Claude?

Privacy AI is not a single technological route but revolves around the same core issue: where plaintext exists in the process of a prompt leaving the user's device, being transmitted over the network, entering the server that runs the model, and returning results; who can read it, and how users verify whether their data is genuinely protected. The privacy mechanisms currently on the market essentially address the same event but adopt different trust models.

Protocol-level privacy relies on service provider commitments; for example, in enterprise-grade zero-retention schemes, service providers can know user identities and also process user prompts but promise not to save data, mainly executing this through contracts and brand reputation. Anonymous proxies hide user identities but do not conceal input content, with downstream model service providers still capable of seeing plaintext. TLS can only protect data security during machine-to-machine transmissions, yet the recipient can still read all content in the end.

Oblivious HTTP (OHTTP) further separates the right to knowledge of identity and content, allowing relays to know the origin of requests without being able to read content, and the recipient can process requests without knowing who sent them. OHTTP has become an IETF standard and is beginning to be used by some companies in production environments. However, for closed-source flagship models, such schemes are nearing the limits of privacy protection because the model weights themselves are the most core asset of AI companies. A single top model training could cost tens of millions of dollars, and laboratories rely on the capability gap between models to maintain valuations, thus are unlikely to easily open model weights or complete service codes.

Structural privacy solutions attempt to use hardware, cryptography, or physical isolation mechanisms to replace traditional trust commitments. Among them, Trusted Execution Environment (TEE) confidential computing is currently the closest to commercial deployment. TEE places the model inference process into a hardware enclave, a sealed area similar to that inside a chip, where even the server operator cannot directly read the data within. The chip generates an attestation (remote proof) to prove to users that the designated model and code are being used.

However, TEE still has limitations: prompts are only protected once they enter the enclave; prior proxies and relay links may still present reading risks. End-to-end encryption (E2EE) further closes off intermediate links by allowing user devices to directly use enclave keys to encrypt prompts, enabling intermediate nodes to only relay ciphertext. However, the cost of E2EE is increased engineering complexity, as all functionalities dependent on plaintext data need to be redesigned.

Fully Homomorphic Encryption (FHE) and Multi-Party Computation (MPC) attempt to completely eliminate trusted parties, allowing servers to compute directly in ciphertext. However, since Transformer models involve numerous complex operations, FHE inference costs remain much higher than regular inference, with the cost of ciphertext computation potentially reaching thousands of times that of plaintext. Currently, encryption chips are under development, but large-scale commercial application still requires time. In contrast, local inference is the most thorough privacy method since the model runs on the user's own device, eliminating servers, relays, and data leakage issues, but at the cost of model capability and hardware expenses.

The future competitive point of Privacy AI may not be limited to chat scenarios but could extend to more complex agent workflows. Currently, all privacy inference mechanisms primarily address data protection between prompts and models. However, AI agents need to call external tools while executing tasks, such as calendars, databases, search engines, and internal enterprise systems, which could all become new plaintext exposure points. A fully locally running agent, if wanting to access information outside of the training set, still needs to send queries to external services, while service providers cannot read plaintext and thus can’t complete tasks.

Currently, mainstream solutions remain at the protocol level, such as managing tool calls through a central gateway, hiding personal identity information before requests are sent, controlling access permissions, and logging invocation behaviors. However, this approach still relies on service provider trust, as the tool server still needs to read plaintext queries. Structural solutions then attempt to run tools like MCP Server directly within TEE, allowing users to verify privacy commitments through attestation. Nevertheless, TEE can only protect transmission processes and cannot guarantee that the ultimate service provider will not read query contents. The real difficulty lies in open-ended searches and complex agent scenarios, as encrypted searches currently still face performance and cost issues.

Future value capture points in Privacy AI may concentrate on unresolved issues: running training loops within enclaves, providing end-to-end protection for tool calls, and creating search systems that do not expose query content. Whoever can solve one of these core aspects may establish a truly difficult-to-commercialize infrastructure advantage.

After Gold Tokenization: How On-chain RWAs Create Real Returns?

Most on-chain real-world assets (RWAs) are currently still concentrated in low-risk assets, such as U.S. Treasury bills (T-bills), and are gradually expanding to other asset classes, such as stocks. Among these, gold is the largest commodity asset on-chain and serves as an important case promoting asset tokenization. The current on-chain gold scale has surpassed $4.9 billion, and its unique value storage properties have made it one of the earliest traditional assets to be tokenized.

However, most current on-chain gold products remain quite limited, primarily allowing users to purchase physical gold without mechanisms to further leverage these assets to generate returns. This leads to an efficiency gap between on-chain RWAs and traditional finance (TradFi) products, also limiting the actual value and application scenarios of on-chain assets.

The next phase of RWA development may focus not just on expanding the scale of assets on-chain but on ensuring these assets have productive and yield-generating capabilities. Taking gold as an example, the traditional financial market has already enabled investors to utilize options to earn returns or hedge risks through products like covered call ETFs. However, traditional products usually have limitations such as high entry thresholds, high costs, the need for KYC, custody, and broker participation. For instance, the currently more mature gold covered call ETF GLDI charges approximately 0.65% management fees, which will be directly deducted from investor returns.

In contrast, on-chain gold products could use smart contracts and structured strategies to reduce entry barriers and attempt to transform originally non-yielding gold assets into income-generating assets. Generating income from gold assets is an important direction for the next phase of RWA development. Gold itself is an approximately $30 trillion-sized asset class and is one of the first commodities to realize on-chain tokenization. Although more than $4.9 billion worth of gold assets currently exist on-chain, the vast majority of funds still remain idle and do not generate returns.

With the development of covered call strategies in traditional financial markets, investors are now able to earn extra returns beyond their gold holdings while also reducing some price volatility risks. On-chain protocols like Enhanced aim to introduce this pattern into blockchains, improving the capital efficiency of RWAs through structured strategies.

The reason gold is suitable as the first case is due to several characteristics: firstly, it has long been regarded as a value storage asset, with its recent prices continuously setting new highs, attracting more investors to allocate; secondly, the rise in global geopolitical and macroeconomic uncertainty further reinforces the demand for gold; finally, gold prices typically do not change as drastically as highly volatile assets, making it better suited to earn stable premiums through covered call options.

The logic of the covered call strategy is that investors hold physical gold while simultaneously selling call options to earn option fee income. If the gold price does not exceed the exercise price, the investors keep the gold and earn returns; if the price increases beyond the exercise price, they must forgo part of the upside. Thus, this strategy is more suitable for investors who are optimistic about gold in the long term but do not expect the price to increase substantially unilaterally.

The Enhanced PAXG Volatility Income Vault is its first Thesis Vault product, aimed at generating returns for users by utilizing gold volatility. This product is based on PAXG (on-chain gold token) and employs a covered call option strategy to allow users to earn option returns while holding gold assets. Its operating mechanism is based on RFQ (Request for Quotes) systems. In the background, assets deposited by users will be auctioned in batches, with market makers providing quotes; subsequently, on-chain option trading will be executed, allowing users to receive option fee income in advance.

Participants can also directly sell covered call options against their own assets and customize exercise parameters, such as exercise price, duration, and direction. In the future, this mechanism could also be extended to other ERC-20 assets beyond gold.

The PAXG Vault employs European-style options, which can only be executed on the expiration date; funds will be locked within each cycle. Users can deposit either PAXG or USDC, with the system automatically converting USDC to PAXG. Option cycles are set to occur bi-weekly, roughly 26 cycles per year, with the exercise price expected to be set in the range of 3%-7% above the current gold price.

Users can choose between two income modes: the compounded mode will automatically convert the received USDC premiums into PAXG and add them to the next cycle to continue generating income, which is more suitable for long-term holders of gold; the income mode, on the other hand, will separate the earnings, allowing users to withdraw USDC at any time, which is better for large fund holders wanting cash flow from idle gold assets.

This model attempts to tackle the core issue of traditional RWAs: not only putting assets on-chain but also ensuring those assets truly generate economic value.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。