Author: Sebastien Davies

Translated by: Shen Chao TechFlow

Shen Chao Guide: A founder transitioning from traditional finance to on-chain infrastructure reflects on: why RWA credit is insufficient, why narrative financing is dead, and why liquidity itself is infrastructure. This article dissects the underlying logic shift of blockchain finance from rapid expansion to refined operations, indicating the competitive focus of the next generation of stablecoins and treasury management systems — it's not who goes online first, but who can operate continuously under real market conditions.

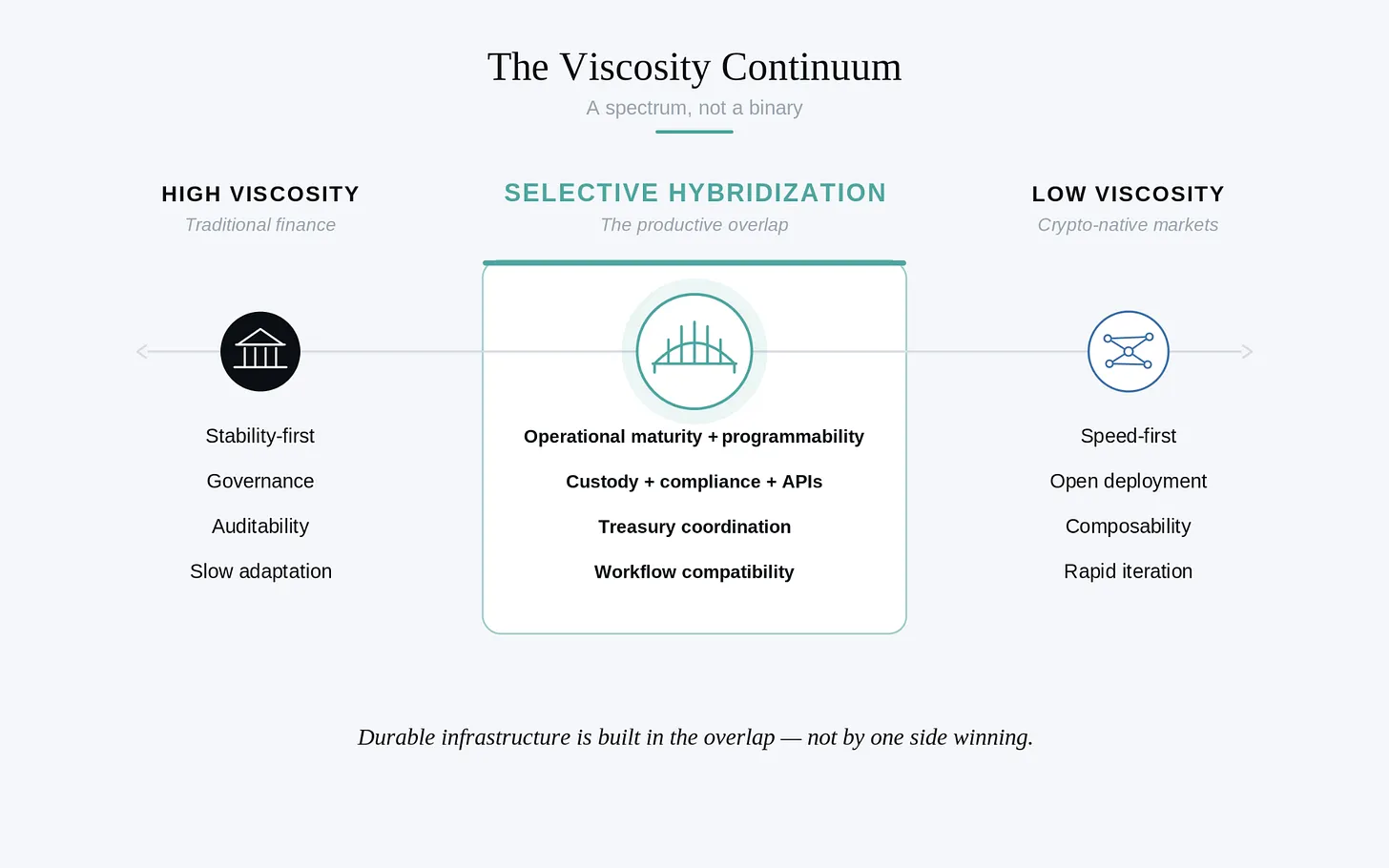

The evolution of financial infrastructure is rarely as neat and tidy as market narratives suggest. More often, it is a slow realization of the gradual failure of old assumptions. As the digital asset industry matures, discussions about decentralized finance have shifted from narrative-driven to a rational examination of established systems. The core characteristic of today’s financial markets is not speed but friction. More precisely, it is viscosity.

In fluid dynamics, viscosity measures the resistance to flow of a substance. In financial systems, it manifests as institutional inertia, compliance requirements, and embedded behaviors. A fundamental error of early blockchain finance was the assumption that technological superiority would drive adoption. Financial systems do not evolve because of elegant technology; they evolve because of workflow compatibility.

The Viscosity of Financial Systems

This friction is rarely an accidental byproduct of legacy technologies. In traditional finance, it is often intentionally designed. Hierarchical controls, capital standards, and operational committees ensure that key functions continue to operate in times of stress. Externally, it appears as bureaucracy, while internally it is viewed as rational management of client assets and institutional reputation.

This design philosophy is inevitably stability-first. Product development is a gated process, with functions constrained by custody rules and reporting standards. Execution slows down, but durability becomes a feature rather than a later patch. When failures occur, they rarely present as sudden collapses but manifest as integration delays and inadequate responses to change.

Crypto-native markets evolve under different assumptions. Friction is minimized to accelerate experimentation, deployment, and global expansion. Permissionless deployment and token incentives allow capital to flow at extraordinary speeds, often without the same operational assurances. Building happens at the market's edge, products quickly find demand, but often leave users as the first real-time testers of code and incentive designs.

The outcome is complementary tension rather than a clean dichotomy. Traditional finance sacrifices execution speed for predictability. Crypto-native systems accept brokenness, as iteration is a major source of competitive advantage. However, the reflexivity of low-viscosity markets means liquidity can disintegrate as quickly as it accumulates, generating rapid contagion when stress arrives.

As the industry matures, expectations have shifted. Crypto-native capital has begun demanding institutional characteristics: transparency, risk management, professional financial oversight. A meaningful middle ground has emerged where participants operate on blockchain rails but expect the operational rigor of more mature systems.

Selective Hybridization

Two systems are gradually merging. Crypto infrastructure is becoming more viscous in areas essential for institutional scale: custody, compliance, risk management. Traditional institutions are modernizing their delivery through APIs and programmable settlement systems, reducing integration friction.

The most enduring infrastructure will combine the iterative speed of digital assets with the decades-long perfected control structures of traditional finance. For institutions, the challenge is rarely cognitive but integrative. Replacing financial systems and reporting structures creates significant organizational friction, and continuity still takes precedence over optimization. The winners will be those who embed themselves into existing workflows, transforming integration from organizational surgery to a more gradual transition.

The following reflections come from firsthand experience of this structural maturation, building an on-chain financial management solution called Elara. They analyze why the order of infrastructure has been reversed and how we design systems for the eventual fusion of these two worlds.

The End of Narrative-Driven Infrastructure

Joining the TrueFi board gave me firsthand insight into a market undergoing profound structural repricing. The platform primarily operates as a credit market for real-world assets (RWA), but the assumptions that supported early industry expansion have clearly lost weight. My traditional finance background indicates that the core challenges in credit persist: moving loans on-chain does not resolve counterparty risk.

Blockchain provides transparency, automated payments, and condition-based payments, but they do not improve the underlying economics of loans or the credit of borrowers. In a competitive environment where platforms vie for the same limited supply of high-quality credit, margins compress and losses compound. Many early operators tried to bridge the gap with unsustainable token emissions, a strategy with a clear ceiling.

Strategic Shift

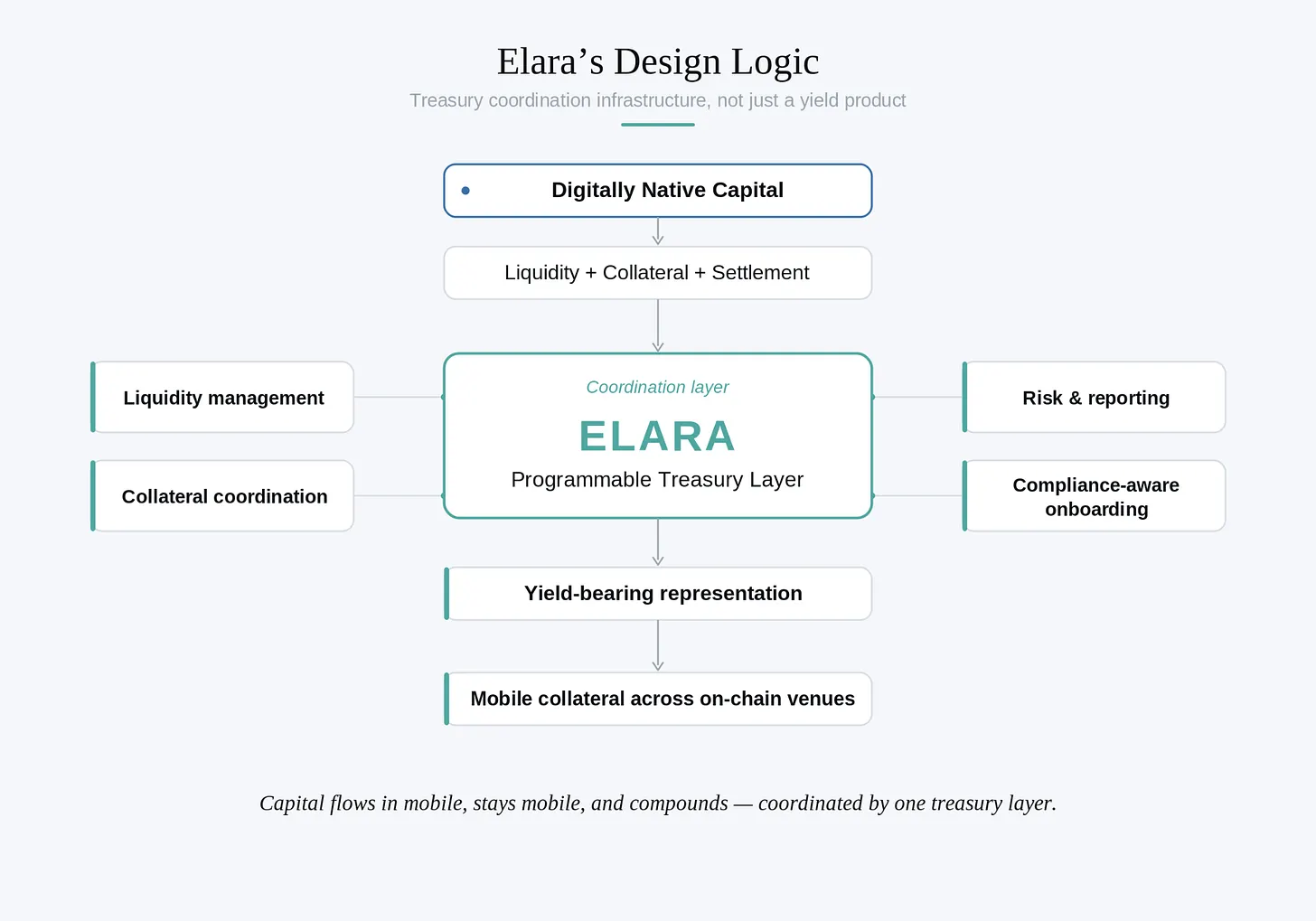

If the digital asset credit market is to mature, it requires more than isolated lending infrastructure. It needs financial infrastructure that can coordinate liquidity, collateral, settlement, and capital flow in an increasingly interconnected on-chain environment. This realization pushed us to shift from standalone products to financial architecture.

Programmable financial systems could ultimately create tighter integration between liquidity management, collateral coordination, and credit formation within digital-native markets. Not because each component needs to reside within a closed ecosystem, but because fragmented infrastructure creates operational drag, capital inefficiencies, and counterparty complexities.

Long-term opportunities are never just about issuing loans. Instead, they involve participating in a broader coordination layer around digital capital: financial management, collateral liquidity, liquidity routing, settlement infrastructure, and risk-adjusted capital deployment. The boundaries between financial, settlement, and credit systems are becoming increasingly porous. Capital starts to flow through these environments in a way that resembles interconnected operational infrastructure rather than isolated products.

At the heart of this shift is a practical economic point. Sustainable financial infrastructure cannot indefinitely rely on token emissions or incentive programs. These mechanisms can accelerate early adoption, but they rarely generate lasting economics on their own. More resilient models emerge from multi-layered participation across the capital stack. Building infrastructure close to financial coordination, liquidity management, and collateral flow allows the economy to compound like a real financial system.

Programmable Financial Infrastructure

Our focus has shifted to stablecoins and financial infrastructure, which are no longer simply trading tools or ways to temporarily exit volatility. They have become the foundational settlement rails for a new class of digital-native capital. This shift changes the nature of the questions. Once digital dollars operate as a financial vernacular rather than a speculative tool, operational demands will rise significantly. The challenge is not just to generate returns; we need to coordinate liquidity, reporting, custody, and risk-adjusted returns in a fragmented environment.

We want to build a collateralized financial asset pegged to the dollar that is native to this ecosystem. Not another on-chain tool, but infrastructure designed around capital efficiency, programmability, and operational flexibility. These ideas ultimately led to Elara.

A more impactful architectural decision is to separate liquidity from yield generation. Traditional fixed-income products distribute returns through periodic cash flows. In a programmable environment, value accumulation can manifest differently. Rather than forcing holders to sacrifice liquidity for yield, Elara is designed so users can deposit underlying assets and receive yield-bearing representation that can be freely transferred.

This distinction is subtle but operationally significant. As capital markets become increasingly digitized and interoperable, the ability for collateral to remain liquid while compounding introduces different financial dynamics. Capital continues to operate within broader on-chain systems rather than becoming static once deployed into yield products. Staked representations compound programmatically while remaining integrated with digital-native liquidity and collateral venues.

When such assets are utilized in credit markets, the results are significant. Collateral is no longer necessarily idle throughout the loan term. Underlying yields can partially offset financing costs, creating a more capital-efficient relationship between financial management and credit formation.

The architecture of Elara reflects our broader argument. Traditional financial operators are increasingly drawn to blockchain systems, not because existing products are outdated, but because programmable infrastructure has expanded what these products can become. Static tools begin to operate more like coordinating software: composable, interoperable, and continuously integrated with broader liquidity and settlement environments.

All this does not eliminate the realities of operating within digital-native markets. These environments are still faster, more fragmented, and structurally more reflexive than traditional fixed income systems. Liquidity conditions can shift quickly. Strategies involving market making, financial coordination, and on-chain liquidity management continue to carry execution risk, smart contract exposure, and operational complexities. Elara does not pretend that blockchain-based infrastructure behaves like traditional finance. The goal is closer to the opposite: to acknowledge the nature of low-viscosity digital markets and introduce greater discipline in how capital flows through them. Programmable infrastructure will not eliminate financial risks. As digital-native capital markets mature, the operational architecture around these risks becomes part of the product itself.

Liquidity is Infrastructure

On a practical level, underlying strategies focus on stablecoin liquidity provision and market making across decentralized financial markets. As stablecoin usage expands to trading, payments, collateral, and financial management, liquidity coordination has become an increasingly important financial function. The fragmented liquidity environment creates demand for active capital deployment, arbitrage capture, rebalancing, and ongoing financial management across on-chain venues.

The resulting yields stem from the real market structure dynamics within the digital-native capital market: trading activity, liquidity fragmentation, volatility, and operational complexity necessary to maintain efficient settlement. Unlike many reflexive crypto yield structures of earlier cycles, these opportunities do not rely on leverage to create economic activity.

These environments are structurally distinct from traditional fixed-income markets. Returns are influenced by liquidity conditions, execution quality, volatility status, smart contract risks, and broader market participation. When trading activity contracts or liquidity compresses, the opportunity set can narrow significantly. During stress periods, financial coordination and risk management become even more crucial. This model reinforces a broader argument: the economy is increasingly not accumulating around reflexive token incentive structures, but around disciplined financial management and infrastructure capable of efficiently coordinating capital under changing conditions.

Financing for Vision

The initial instinct was influenced by previous cycle financing dynamics, raising capital around the vision itself. Early discussions centered on the scale of opportunity: digital dollar infrastructure, programmable financial systems, and the long-term integration of traditional finance with blockchain-based settlement rails.

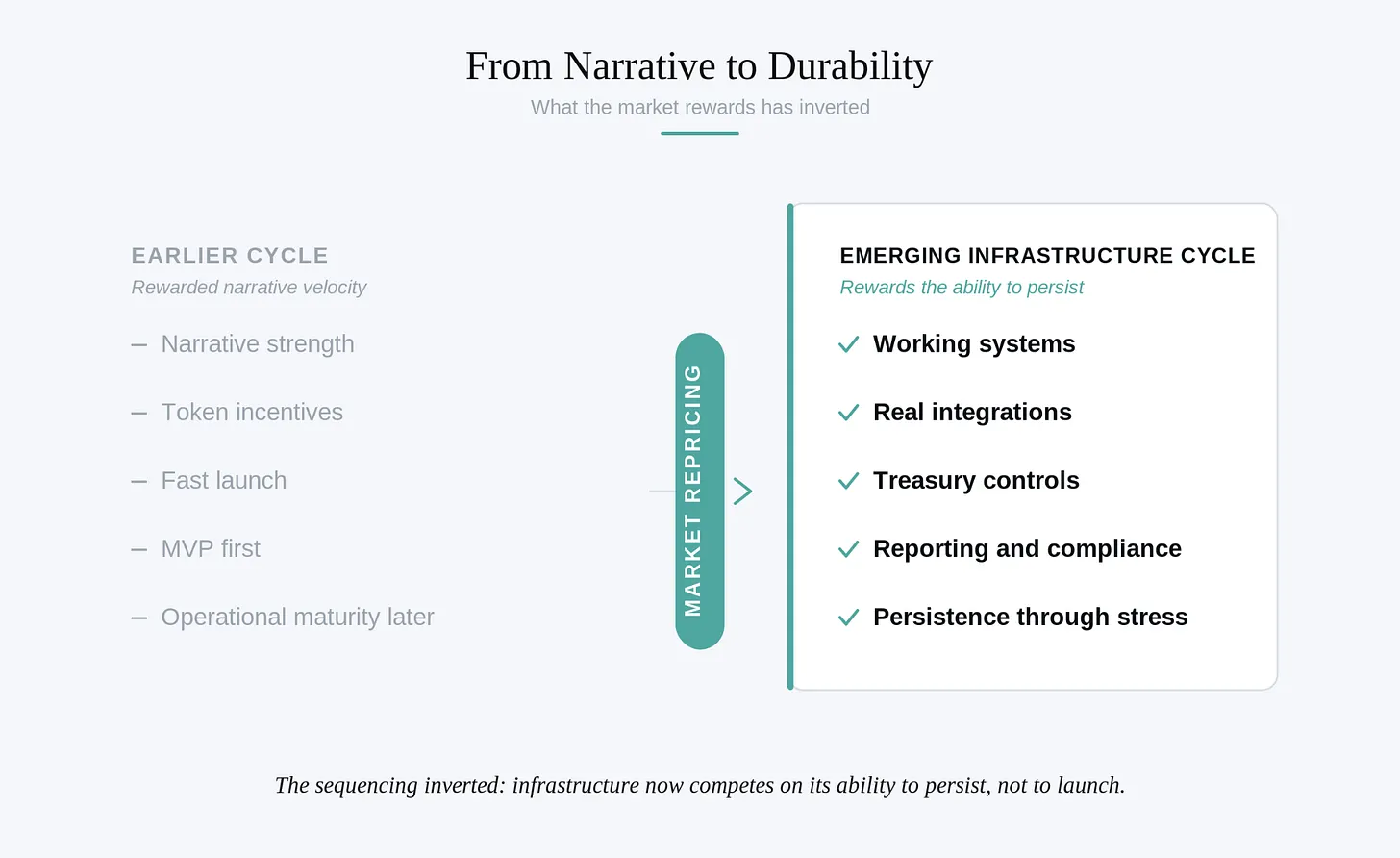

A few years ago, this approach might have worked. The crypto market rewarded narrative speed for much of the last cycle, where strong arguments and token models could attract significant capital before infrastructure matured. As we enter dialogues today, the environment has shifted.

Members of the execution team engage with potential investors before meaningful infrastructure has been built, assuming the power of ideas would drive the conversation. Instead, dialogue has shifted to operations. Investors want systems that operate, integration, reporting structures, financial controls, counterparties, compliance frameworks, and evidence that the infrastructure can operate under real market conditions.

This shift is both inevitable and healthy. It reflects the lessons of the last cycle when the market became less willing to fund abstract financing after witnessing loosely built systems crumbling under stress. Technology has accelerated this change. As advances in AI-assisted software development progress, the scarce value of early code begins to collapse. MVPs become easier to build, interfaces easier to replicate, and infrastructure more accessible. As software becomes commoditized, operational trust becomes more valuable.

Competitive advantages shift from who can tell the most compelling story to who can build systems capable of sustained operation under real market conditions. The order has been reversed. Early cycle rewards rapid launches followed by later operationalization. Emerging markets reward the opposite: infrastructure businesses are now competing on sustainability rather than launch ability.

The Power in Numbers

These realizations compel us to ask deeper questions: why has the pace of institutional adoption of digital assets been slower than many early builders expected? This brings us back to the viscosity issue.

Banks, corporate treasuries, asset management firms, and institutional allocators move slowly for rational reasons. Their operating models are built on continuity, auditability, risk control, and decades of accumulated procedural trust. The presence of reporting standards, investment committees, custody frameworks, and compliance processes is to mitigate the probability of uncontrolled failures when managing large sums of money. What appears as friction from the outside is, internally, the infrastructure itself.

Crypto-native systems evolve around different assumptions. Capital liquidity, composability, rapid iteration, and open deployment enable blockchain infrastructure to scale quickly to global markets. The advantage is adaptability. The weakness is that speed may outpace operational reinforcement, as demonstrated in the last cycle — when liquidity, incentives, governance, and risk became increasingly intertwined.

The long-term capital base likely to migrate on-chain will continue to retain high viscosity characteristics, even as underlying settlement infrastructures become more programmable. This realization shaped Elara. Building solely for speculative speed is unappealing; waiting for significant institution allocators to fully migrate on-chain before building anything is also unrealistic. The practical path is to build around the existing digital-native capital present in these markets while embedding the operational values that institutional participants will eventually require.

In practice, this means designing for financial discipline, reporting awareness, and durability from the outset rather than treating these functions as future upgrades. Collaboration with ArkenYield reflects the same philosophy. At its core is a tokenized market-making and fund management strategy, operating in low-viscosity digital markets while incorporating operational assumptions typically associated with institutional financial infrastructure: active liquidity management, controlled fund operations, risk monitoring, and an emphasis on capital preservation beyond yield generation. This positioning allows the system to maintain economic productivity in today’s market environment while gradually aligning with the operational expectations of more traditional capital pools.

This extends to the surrounding operational layers necessary to responsibly support institutional participation. Identity verification, compliance coordination, and onboarding workflows were often considered secondary in early cycles, but have become foundational as the market matures. Our collaboration with Keyring strengthens this layer by integrating compliance and identity infrastructure into the system architecture rather than treating them as external afterthoughts.

Over time, the distinction between crypto-native and institutional financial infrastructure will likely become less rigid. Hedge funds, asset management firms, fintech platforms, payment companies, and ultimately corporate treasuries are increasingly exploring how programmable settlement and digital dollar infrastructure can improve liquidity management and capital efficiency. As this integration accelerates, the systems most likely to sustain will not be the fastest acting or most ideological. They will be the systems that already speak the operational language understood by institutional capital.

We do not intend to build a purist alternative to the existing financial system, nor do we assume that institutions will fully migrate on-chain overnight. Financial systems rarely transform through sudden replacement; they evolve through gradual integration, workflow adaptation, and trust accumulation. The design of Elara is based on a simpler observation: digital-native capital increasingly needs funding management infrastructure established with operational discipline from day one. This means integrating compliance awareness into the architecture itself, viewing reporting as a core layer rather than a downstream concern, and designing around sustainability rather than reflexive incentives. The market may still be early. But infrastructure can no longer operate that way.

How Viscosity Becomes Liquidity

Financial systems do not evolve uniformly. Their pace of change is largely dependent on the surrounding environment.

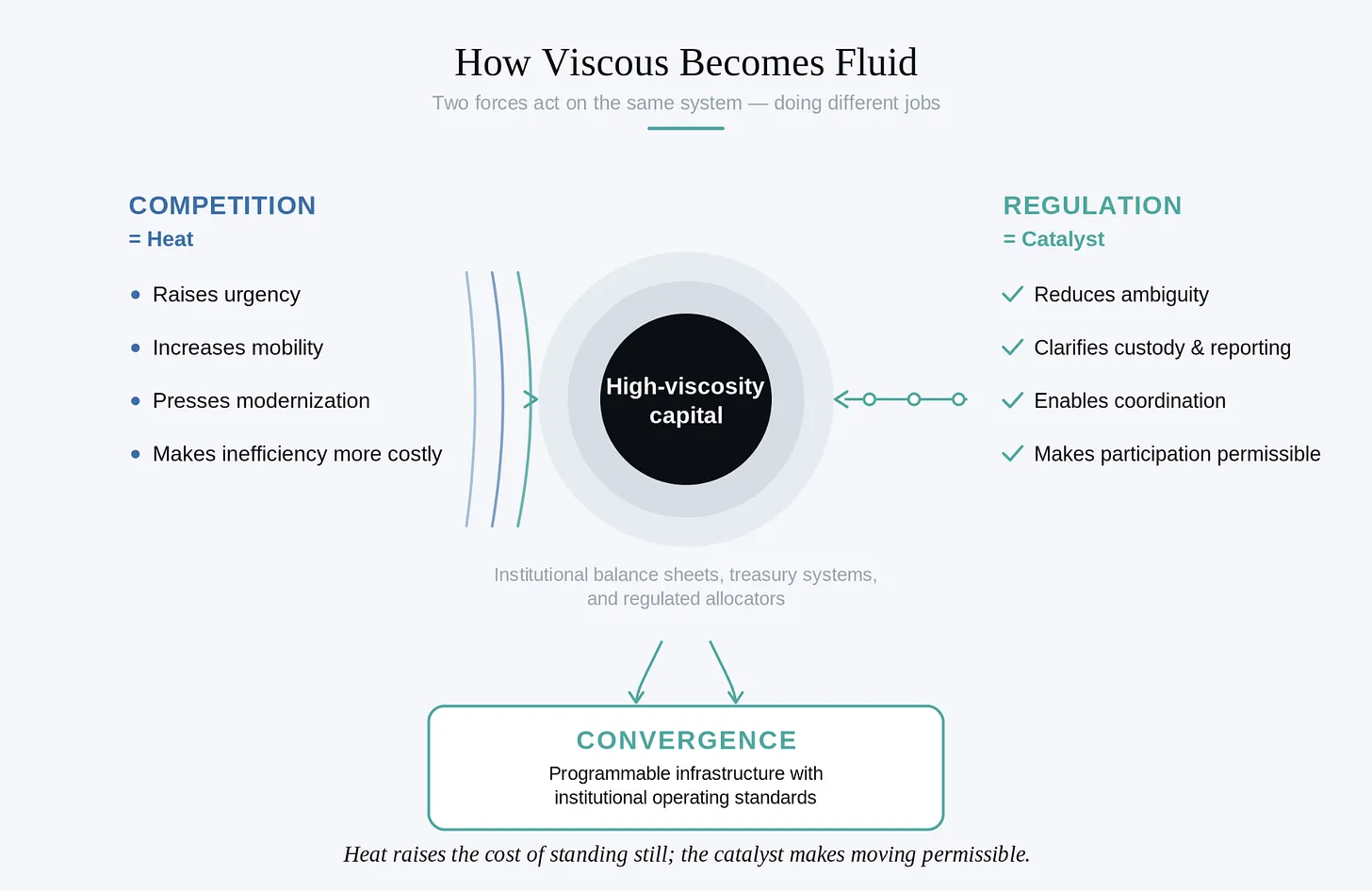

One of the more important developments in recent years is the gradual shift in regulatory attitudes towards digital asset infrastructure. Early regulatory dialogues were primarily focused on restrictions and risk controls. Recent reforms have begun to create pathways for institutional participation rather than prohibiting it. This is a critical shift. Financial systems rarely transform solely through technology. They change when legal, operational, and economic coordination begins to align simultaneously.

Regulation acts more as a catalyst than a barrier. It cannot, by itself, enforce adoption. But once a market matures sufficiently, regulatory clarity can significantly accelerate institutional coordination by reducing uncertainty around custody, reporting, settlement processing, and fiduciary responsibilities. This is most critical in high-viscosity systems because uncertainty itself is friction. Large financial institutions rarely avoid using new infrastructure because they do not understand it. More commonly, they avoid using it due to unacceptable risks posed by operational ambiguity. Once that ambiguity narrows, adoption can shift unexpectedly quickly.

Competition introduces a second force. In stable markets, institutional inertia may persist for years, as the operational costs of transformation outweigh the immediate benefits of optimization. As competitive pressures mount, systems start to restructure. Competition acts as a heat source, increasing capital liquidity and forcing market participants to modernize funding management, settlement infrastructure, and liquidity coordination.

This dynamic becomes the foundation for our thinking about Elara. One of the core limitations of many early RWA models was the assumption that institutional capital would migrate on-chain due to theoretically more efficient infrastructure. In reality, high-viscosity capital providers are asked to transfer assets into environments that still appear operationally fragile, lightly governed, and reflexive under stress. The friction is too high relative to perceived gains.

Designed for Fusion

We approach this problem differently. We did not attempt to force institutional behavior to adapt to crypto-native systems too early; instead, we built infrastructure capable of operating efficiently in today’s digital-native market while embedding the operational assumptions that institutional allocators will ultimately need.

This means integrating compliance awareness into the architecture itself and recognizing that trust, reporting, and risk management are not external constraints on financial infrastructure, but part of the infrastructure itself. It also means moving beyond reflexive incentive structures toward systems capable of maintaining economic utility under changing market conditions.

Durable financial systems rarely emerge solely by speed. They compound through the gradual accumulation of reliability, repeatability, and operational trust. The goal is not just to build for markets that exist today but to build for the conditions under which the financial system itself begins to change. In this sense, the design of Elara is not as a static product but as an infrastructure positioned for fusion. As the digital asset market matures and institutional participation expands, the systems most likely to sustain will be those that can switch between low-viscosity capital environments and the operational expectations of more traditional allocators.

We are not waiting for the financial system to become liquid. We are building infrastructure that can manage both forms of liquidity. Elara is designed to operate in the high-speed liquidity of digital-native capital while being sufficiently durable to support the slower, more prudent movement of institutional balance sheets over time.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。