Author: Ed Elson

Translator: Deep Tide TechFlow

Deep Tide Guide: After the SpaceX IPO, JPMorgan gave a valuation of $2.9 trillion, while Raymond James went even higher with an outrageous call of $10.4 trillion—more than the combined market value of Microsoft, Amazon, Meta, Tesla, and Berkshire. Are these analysts crazy? No, they are just exchanging compliments for IPO underwriting fees. In December 2025, the SEC quietly abolished the core regulations preventing analyst conflicts of interest, and Wall Street's incentive mechanisms have returned to the era of the internet bubble.

Twenty-three years ago, a scandal broke on Wall Street. Stock analyst Henry Blodget became famous for being bullish on popular stocks during the internet bubble, only to later be found out for actually being bearish in private. In emails to colleagues, Blodget described many of the stocks he publicly recommended as "crap," "dogshit," and "POS." After the bubble burst and valuations plummeted, Blodget was charged with securities fraud and banned for life by the SEC from the securities business.

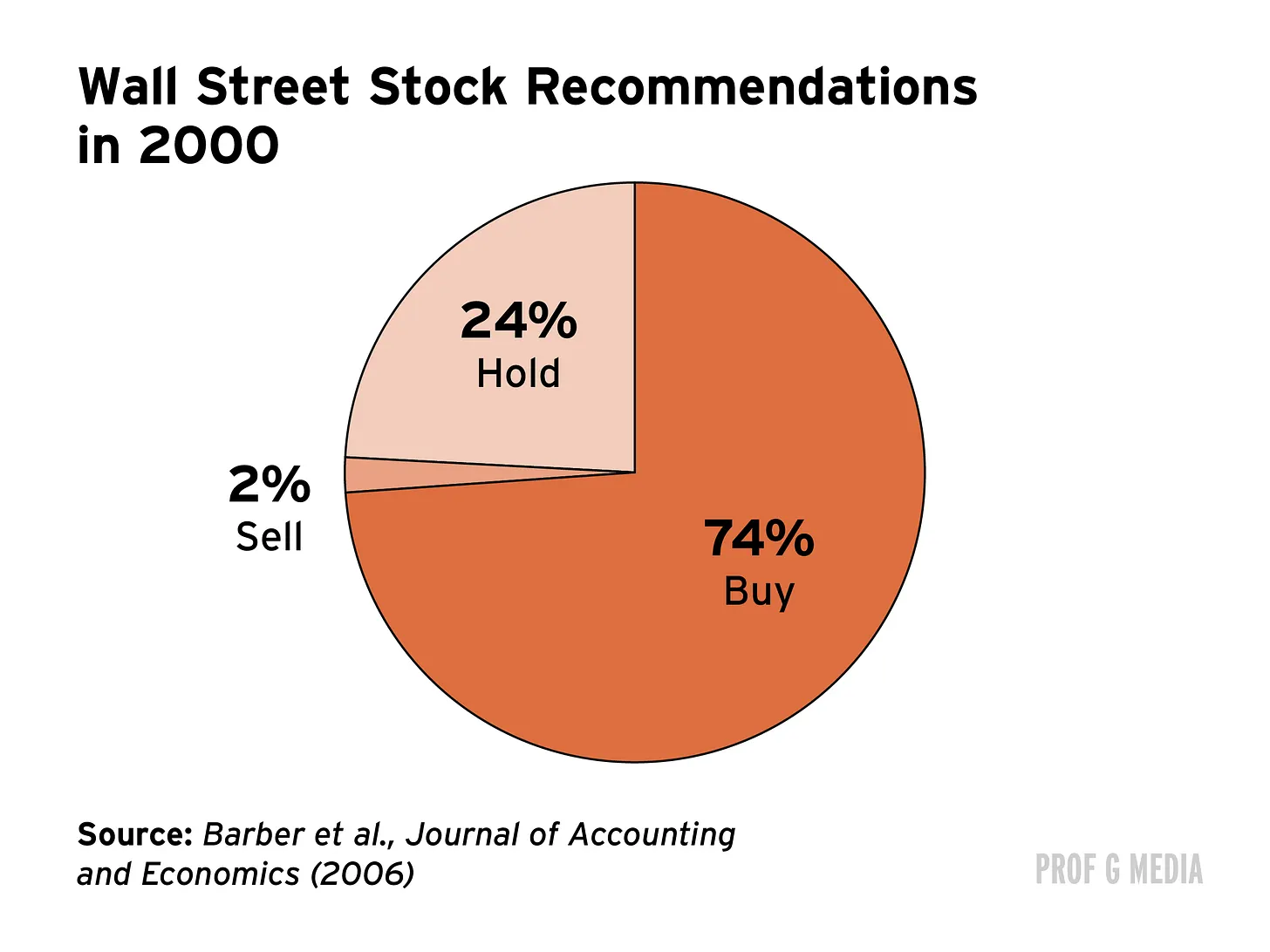

Blodget was a representative figure but not an exception. At Solomon Smith Barney, another analyst publicly rated a company as "buy," but privately referred to it as a "pig." An analyst at Lehman Brothers admitted in an email that "ratings and price targets are meaningless anyway," and retail investors could be misled. "This is the nature of my industry," he wrote. This was an epidemic: by 2000, three-quarters of stocks were rated as buys, with only 2% rated as sells. We all know what happened next.

Why do Wall Street analysts recommend stocks they know are junk? One word: incentive. Since IPOs and equity financing are important revenue sources for investment banks, analysts are incentivized to publish flattering research to win deals and earn fees. In 2002, a Merrill Lynch employee complained to colleagues, aptly summarizing this conflict of interest: "John and Mary Smith are losing their retirement just because we don’t want to upset [investment banking clients]."

After the bubble burst, the SEC realized they had to do something. They created the Global Research Analyst Settlement (GRAS) in 2003. The goal was to eliminate conflicts of interest caused by investment banking and equity research analysts being in the same team. So, they completely separated the two departments: equity research was no longer allowed to communicate with investment banking (unless compliance personnel were present), and the compensation of the two teams was also independent. This way, the investment bank could continue its business (winning deals), and analysts could publish unbiased research.

Why am I saying this?

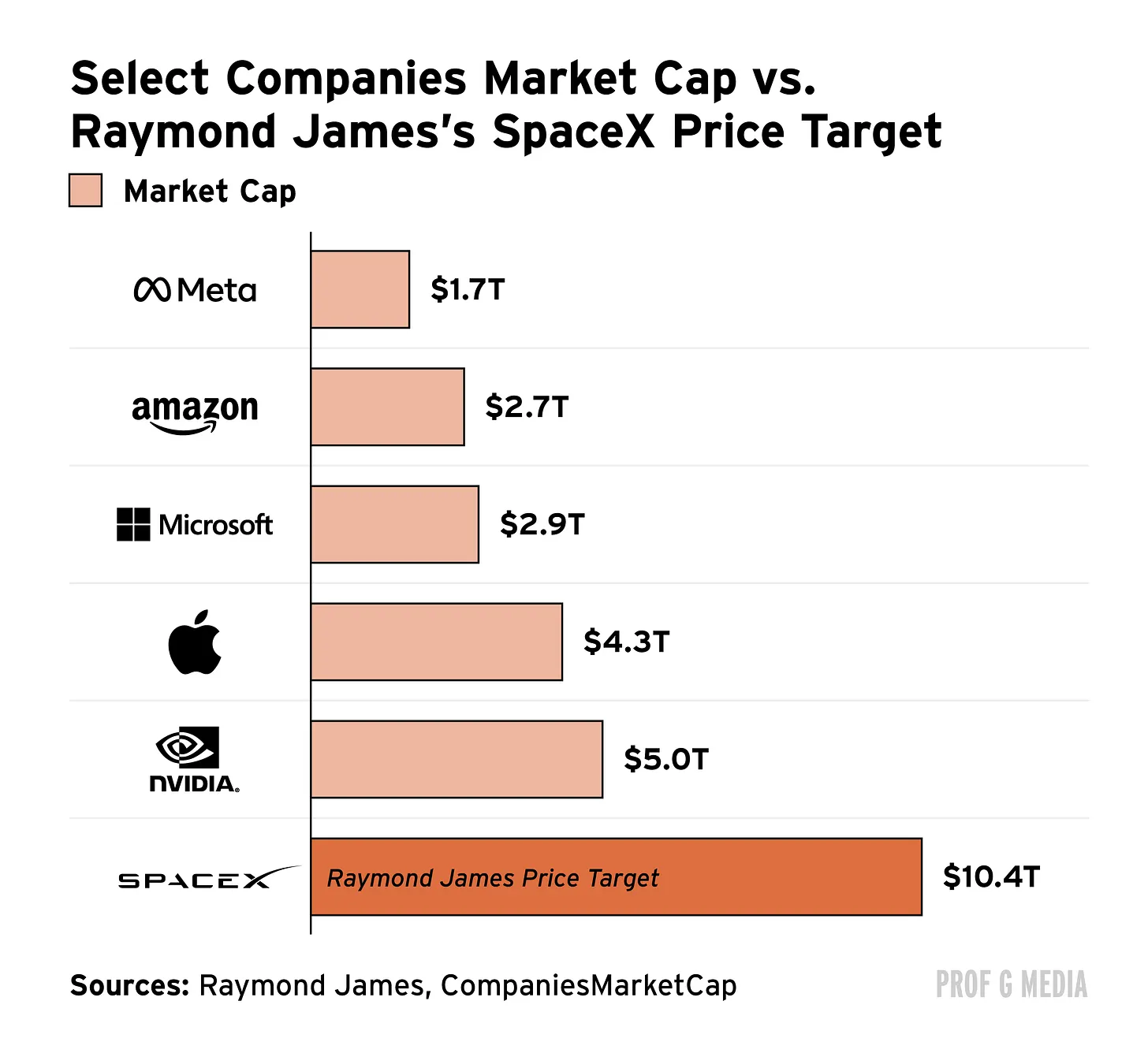

Last week, major investment banks on Wall Street released research on SpaceX stock, with target prices that are through the roof. Before discussing, remember that SpaceX is now worth $1.8 trillion. With projected revenue of only $19 billion in 2025, this valuation is at least $1 trillion too high. (I have explained why here.) Now, let's see what Wall Street "believes."

JPMorgan believes SpaceX is worth $2.9 trillion, which is 58% higher than the current valuation. Their argument is that SpaceX's "potential impact on humanity" is "greater than any company they have seen." Deutsche Bank claims the company is even more valuable: $3.3 trillion. In their view, this rocket manufacturer represents the "pinnacle of civilizational ambition." Morgan Stanley has an even higher number: $3.9 trillion. Morgan Stanley claims SpaceX is the "ultimate frontier of AI." But the truly outrageous target price comes from the lesser-known investment bank Raymond James, whose chief analyst claims SpaceX is worth—wait for it—$10.4 trillion. This would make SpaceX more valuable than Microsoft, Amazon, Meta, Tesla, and Berkshire Hathaway... combined.

I have just one question: WTF? I had to read Raymond James's report a second time just to confirm I wasn’t hallucinating. (I wasn’t.) Their "model" predicts SpaceX's revenue will grow from $19 billion to over $5 trillion by 2035. (This is nearly one-fifth of the U.S. GDP.) Allegedly, 94% of that revenue will come from AI, which means the company’s AI business would have to become 23 times larger than Nvidia, even though it is currently 67 times smaller. Like I said a few weeks ago: pass me that crack pipe.

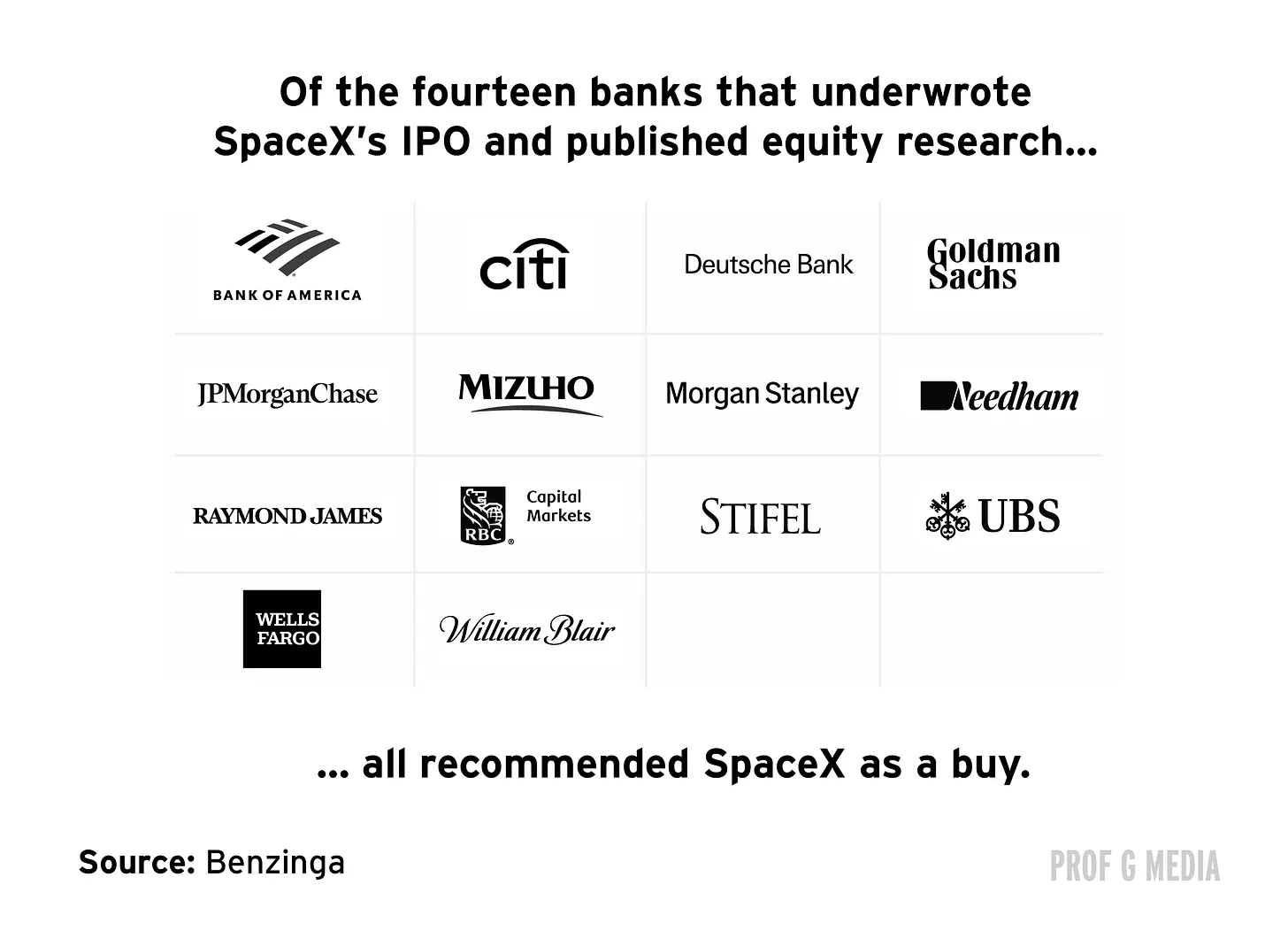

These target prices are absurd—absurd to the point of being inexplicable. Until you realize one thing that connects them: they are all published by banks underwriting the SpaceX IPO. Yes, Raymond James, Morgan Stanley, JPMorgan... all participated. In fact, not a single bank underwriting SpaceX's listing rates the stock as anything but a buy.

I know what you’re thinking: if the IPO has already happened, and the banks have already collected their fees, what’s the incentive to publish flattering research now? The answer: more fees. SpaceX has initiated follow-up debt financing, and it is estimated that the company will need to raise $235 billion in the next four years to cover costs. This means hundreds of billions of dollars in future investment banking revenue. There are also rumors that SpaceX will seek to merge with Tesla, which would lead to (spoiler alert) even more fees. In short, Wall Street's most profitable business right now isn’t trading or lending… it’s getting Elon Musk to like you.

Open the Floodgates

But wait. Isn’t the Global Research Analyst Settlement from 2003 specifically designed to prevent banks from babbling nonsense in research for fees? You're right. At least, until seven months ago when it was... terminated.

Yes. On December 5, 2025, the SEC officially abolished the law inspired by Blodget back in the day. According to the agency, the GRAS rules are now useless because they have "largely been replaced by" other rules." They refer to FINRA Rule 2241, a law that technically addresses conflicts of interest, but has done almost nothing in comparison. As former SEC Chairman Arthur Levitt wrote in his article titled "The SEC May Let Wall Street Analysts Be Corrupt Again," "Don’t be fooled by other regulations promising this separation… this is the natural pattern of regulatory surrender."

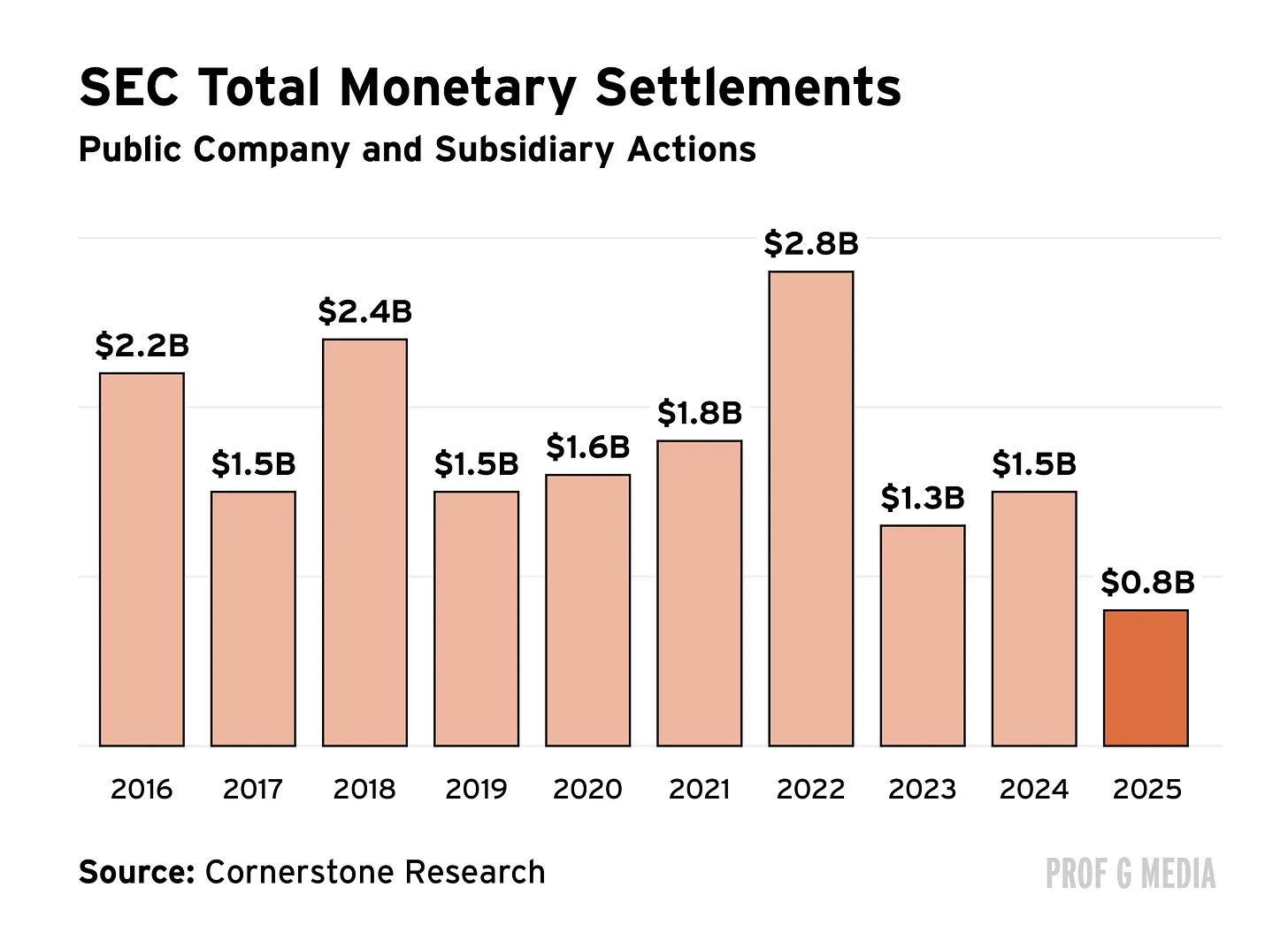

If it weren’t for the fact that the SEC is indeed being torn apart, I would lean toward saying Arthur Levitt is being alarmist. Under Trump, the agency lost one-fifth of its staff. Last year, it took only 56 enforcement actions against public companies—30% less than the previous year, the lowest of any transitional year in a decade. Four months ago, its enforcement chief, Margaret Ryan, mysteriously resigned after attempting (but failing) to investigate insider trading involving the Trump family. Clearly, the SEC no longer exists to protect investors, but rather to facilitate white-collar crime.

Longstanding

If flattering was equivalent to trading rocket launchers during the internet bubble, today it is nuclear weapons. Speaking well of those in power can now earn you millions in deals, unprecedented legislation, or even cabinet positions. Tim Cook didn’t give that gold trophy to the president for the president—he did it for shareholders. In 2026, few things have a greater return than when a sycophant is rewarded, and any executive not realizing this is not fulfilling their fiduciary duty. In other words, who wouldn’t flatter SpaceX?

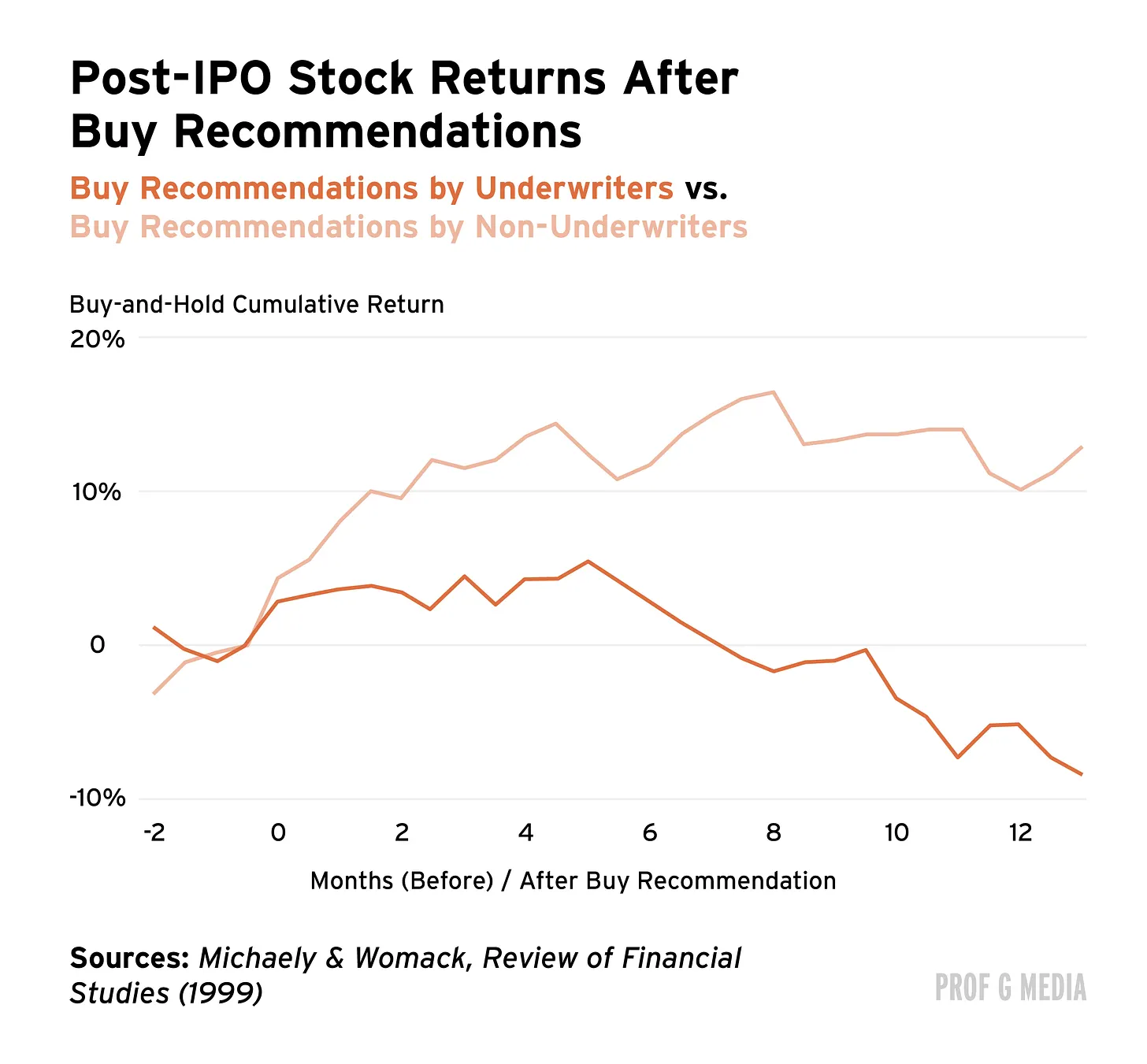

Of course, the trouble lies with retail investors. SpaceX has already fallen over 30% from its peak, and anyone who bought after the IPO is now underwater. This follows a trend: research shows that IPOs recommended by analysts from underwriting banks perform poorly and lose money on average. The lesson: if someone is paying you to buy a stock, proceed with caution.

The fact is, SpaceX is a terrible investment at the current price. Morgan Stanley's stock research report implicitly acknowledges this, providing a "deliberately wide" price range with a bull case target price of $600 and a bear case target price of... $75. Translated, that means: "We have no damn idea."

People wonder why so many Americans hate Wall Street. This is the reason. It doesn’t mean analysts are bad—it just means the incentives are bad. In the words of Charlie Munger: "Show me the incentives, and I’ll show you the outcomes."

The solution is simple: fix the incentives. Either restore the Global Research Analyst Settlement or find another way to eliminate conflicts of interest. It shouldn’t be that hard, but it may be difficult for this administration, as it would undermine the culture of corruption they’ve worked so hard to build. So if you expect things to change, take this analyst's advice: don’t hold your breath.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。