Author: Nancy, PANews

The crypto market continues to fluctuate, with overall trading activity remaining sluggish, yet Hyperliquid maintains its expanding momentum, with its global perpetual contract market share consistently rising.

As a key contributor, Trade.XYZ, the core driver of the HIP-3 market, has surpassed the trading volume of Hyperliquid's crypto perpetual contracts within less than a year, becoming the platform's current core growth engine.

With the rapid rise of Trade.XYZ, market expectations for its potential token issuance continue to heat up. However, there are concerns in the market about whether the token issuance by Trade.XYZ would lead to a siphoning attack on Hyperliquid, thereby diminishing the value capture of HYPE.

Hyperliquid's countercyclical growth, Trade.XYZ accounts for nearly half of the trading volume

Although the overall trading activity in the crypto market has not fully recovered, Hyperliquid has shown a countercyclical growth trend.

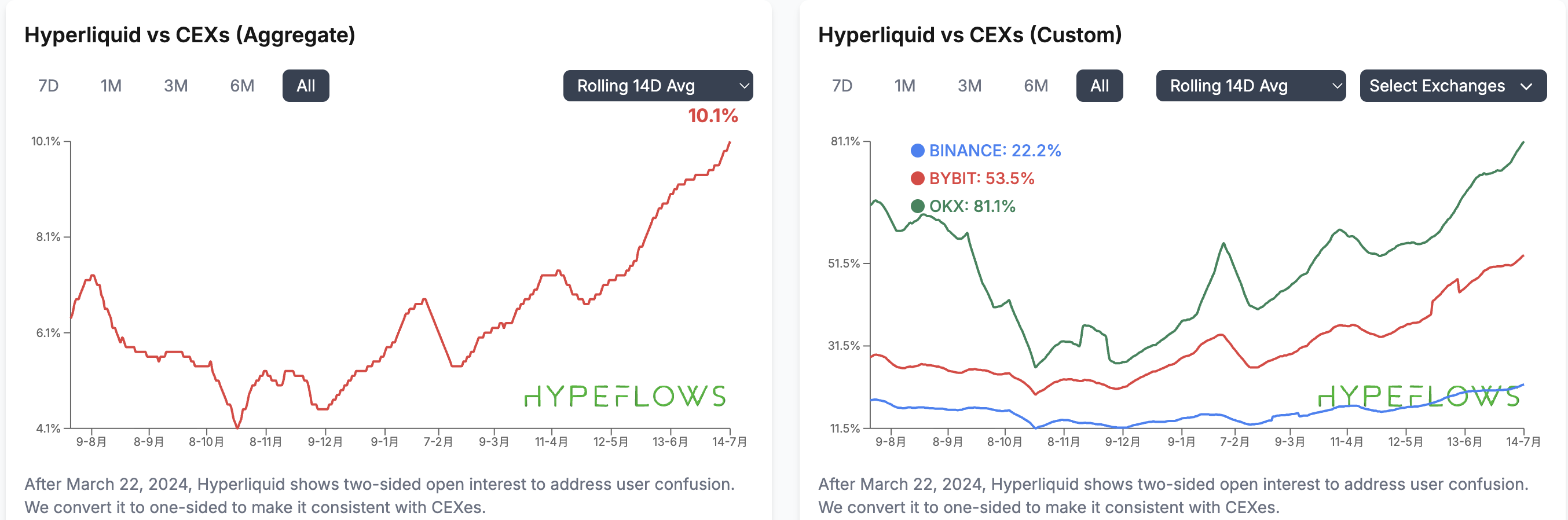

Hypeflow data shows that as of July 14, in terms of open interest (OI) scale (14-day rolling average), Hyperliquid's OI has reached 22.2% of Binance, 53.5% of Bybit, and 81.1% of OKX, further narrowing the gap with leading centralized exchanges (CEX) since the beginning of the year.

From the perspective of the global perpetual contract market, the trading volume share of Hyperliquid has risen to 9.2%, setting a historical high, while this percentage was only 5.4% at the beginning of this year.

This indicates that, with increasing liquidity and sustained user stickiness, Hyperliquid is rapidly encroaching on market share, further enhancing the competitiveness of on-chain perpetual contracts.

The key force driving this round of growth is the HIP-3 market.

Since its launch in October last year, the HIP-3 market has rapidly expanded in scale. Hyperscreener data shows that as of July 14, the cumulative trading volume of HIP-3 has exceeded $386.7 billion. Among them, on-chain stock assets are the main business sector contributing to the growth of HIP-3, with related trades accounting for over 61.5% of the overall transaction volume in this market.

As the trading scale of HIP-3 continues to expand, its contribution to the overall ecology of Hyperliquid is also continuously increasing.

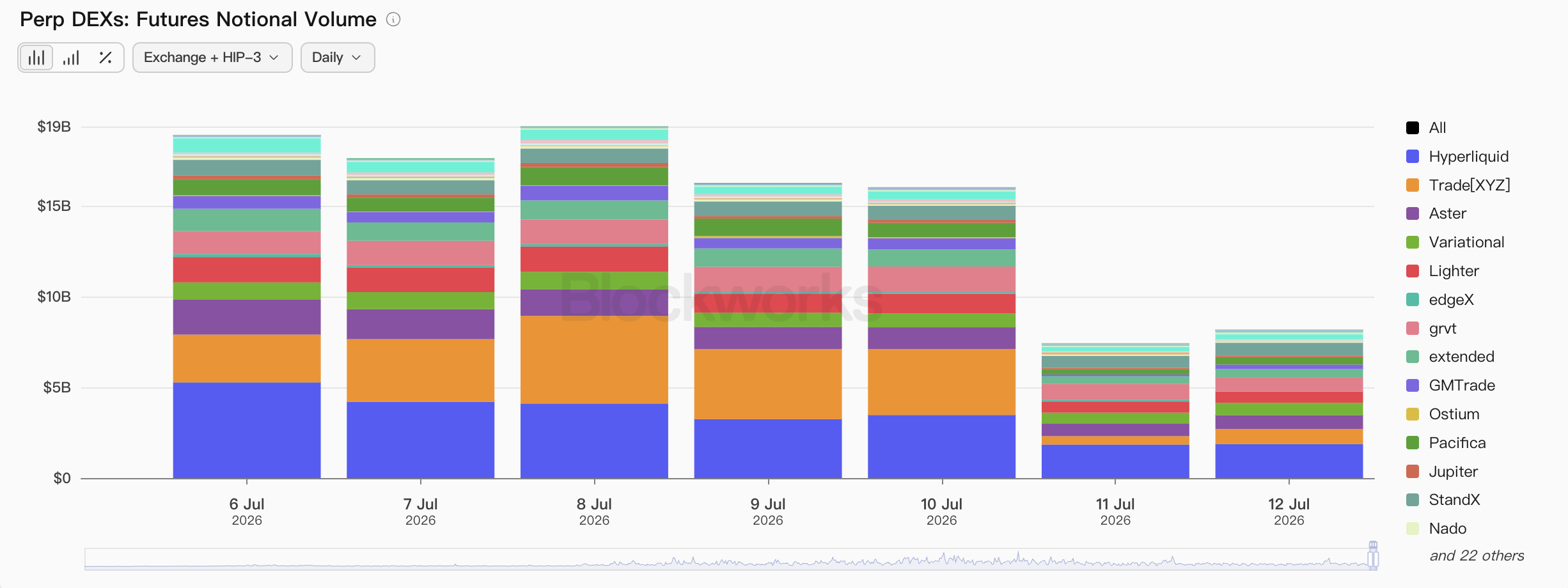

Blockworks data shows that in terms of nominal trading volume on Perp DEX, Trade.XYZ's trading volume recently has exceeded Hyperliquid's crypto perpetual contracts for multiple consecutive days, ranking first in the entire market and significantly leading competitors like Lighter, Aster, and grvt, becoming the core source of liquidity for Hyperliquid.

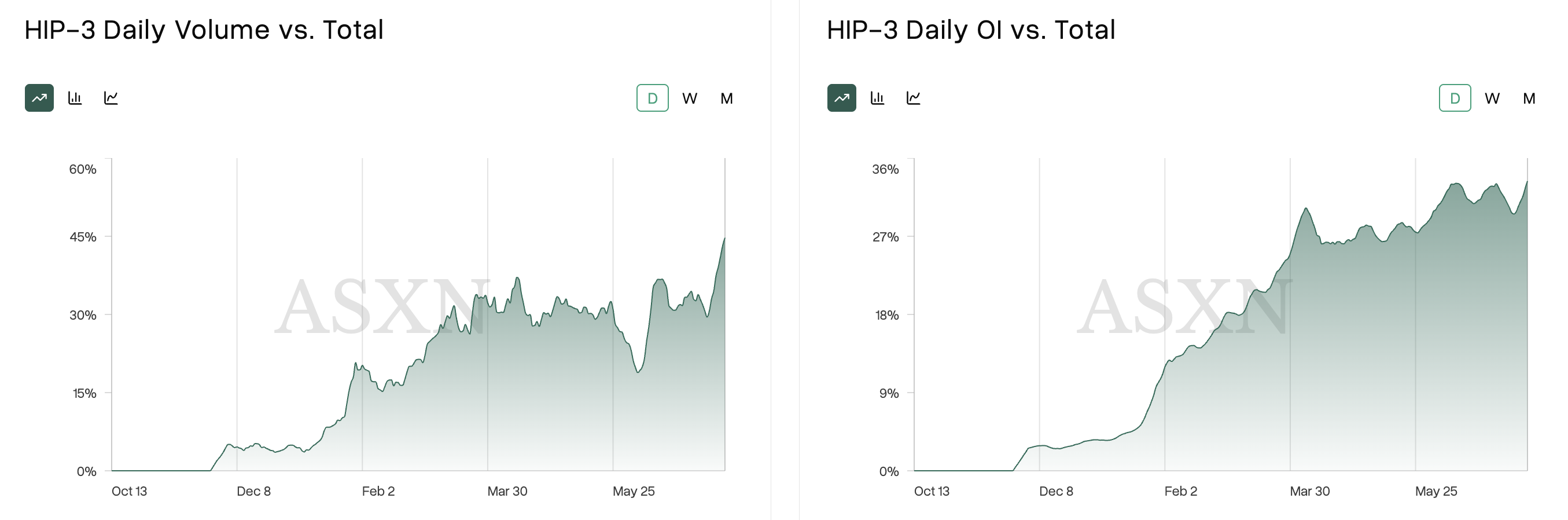

At the same time, Hyperscreener data shows that as of July 14, the daily trading volume of HIP-3 accounted for 44.7% of Hyperliquid's overall trading volume, while this percentage was only 4.92% at the beginning of this year; the proportion of daily open interest also jumped from about 3.5% at the beginning of the year to 33.4%. In less than a year, HIP-3 has transformed from a fringe business into the core growth engine of Hyperliquid.

In the HIP-3 market, Trade.XYZ is almost the sole player. Hyperscreener data shows that as of July 14, Trade.XYZ contributed 93.9% of the trading volume and 99.8% of the open interest in the HIP-3 market, nearly monopolizing the entire HIP-3 market, which has sparked concerns in the market about centralized risks. (Related reading: The watershed moment for HIP-3: After Trade.XYZ swallows 90% of the market, multiple players withdraw)

Expectations for Trade.XYZ token issuance rise, but this may not be the best solution at the current stage

The rapid growth of Trade.XYZ's business is forming a significant network effect. As liquidity gathers and the user base expands, its leading advantage in the HIP-3 market is further solidified, making it nearly impossible for competitors to shake it in the short term.

For this reason, market expectations for token issuance by Trade.XYZ are continuously heating up. Many viewpoints suggest that such a large platform will ultimately issue tokens to incentivize liquidity, expand user growth, and establish its own value capture system.

This has also raised market concerns that if Trade.XYZ launches an independent token in the future, it may continue to siphon off traffic, capital, and market attention from Hyperliquid's ecosystem, thereby weakening HYPE's value capture capability. Especially after Trade.XYZ's trading volume temporarily exceeded Hyperliquid's native crypto market, this discussion has further intensified.

However, from the current perspective, the market may be overestimating the possibility of Trade.XYZ issuing tokens. In fact, a deep binding of interests has already been established between Trade.XYZ and Hyperliquid.

The HIP-3 mechanism inherently requires project parties to continuously hold, stake, and consume HYPE. Currently, Trade.XYZ has staked 500,000 HYPE as the margin for HIP-3 deployment and has participated in approximately 100 Ticker Dutch auctions, consuming about 65,000 HYPE (approximately $4.1 million). Notably, since May this year, Trade.XYZ has won at least 30 Ticker auctions, with more than half concluding at the base price of 500 HYPE. This means that for each new trading market added by Trade.XYZ, there is a continuous consumption of HYPE. As its business scale continues to expand, its demand for HYPE will not decrease but rather continue to grow.

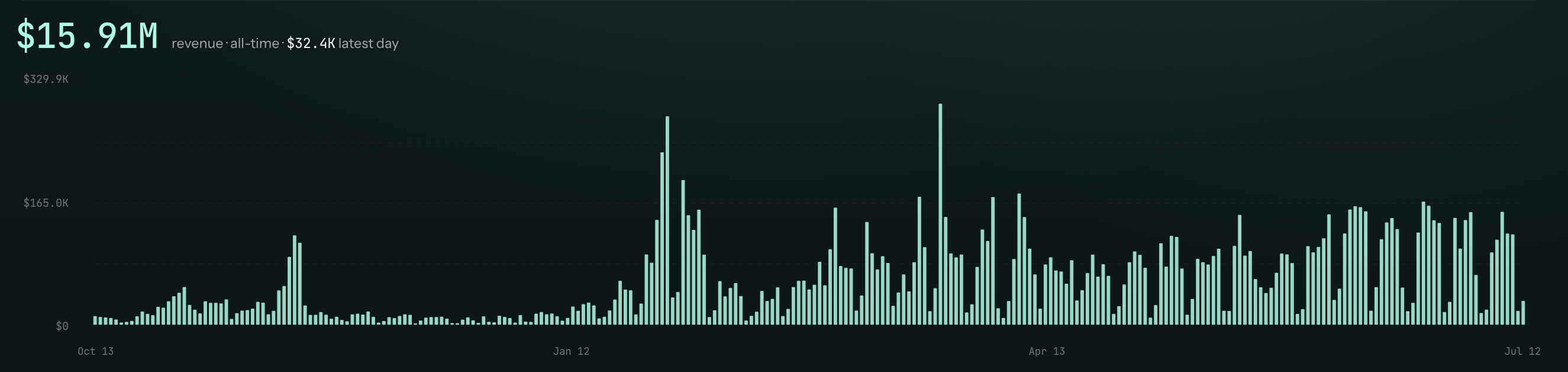

At the same time, Trade.XYZ already has a relatively mature business model, and the necessity of issuing tokens is decreasing. According to hl.eco data, as of now, Trade.XYZ's cumulative protocol revenue has reached $15.91 million. This means that its business growth can rely on real fee income for drivers, rather than depending on token issuance for financing or user incentives.

In fact, for platforms that already have stable cash flow, issuing tokens may not be a profitable business. To maintain the token price and ecosystem incentives, project parties typically need to continually invest funds in buybacks, staking rewards, liquidity subsidies, etc. This not only erodes existing profits but may also crowd out investment in product development, market expansion, and ecosystem construction. In contrast, directly investing business revenue into product iteration and user growth often leads to higher capital allocation efficiency.

Furthermore, regulatory factors have also reduced Trade.XYZ's motivation for token issuance. Currently, a large number of trading targets of Trade.XYZ involve US stocks, stock indices, and Pre-IPO assets, which are already in areas with high regulatory scrutiny. Therefore, maintaining a trading infrastructure without a platform token helps reduce potential compliance risks and can retain greater strategic flexibility for future business expansion.

From this perspective, Trade.XYZ and Hyperliquid seem more like a community of interests. Trade.XYZ can continually expand market scale through low-fee strategies and a rich array of asset targets, while Hyperliquid continuously gains new liquidity and fee income. For Trade.XYZ, recklessly issuing an independent token would not only struggle to create new value increments, but may also disrupt the existing balance of interests.

Therefore, at least at this stage, compared to issuing tokens, continuing to expand the business relying on the Hyperliquid ecosystem and binding value through continuous holding and use of HYPE may still be the current lowest-cost and highest-efficiency development path for Trade.XYZ.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。