Jito announced a new proposal, with all revenue shares from the new trading platform JTX to be used for repurchasing and destroying JTO.

Written by: Maher, Foresight News

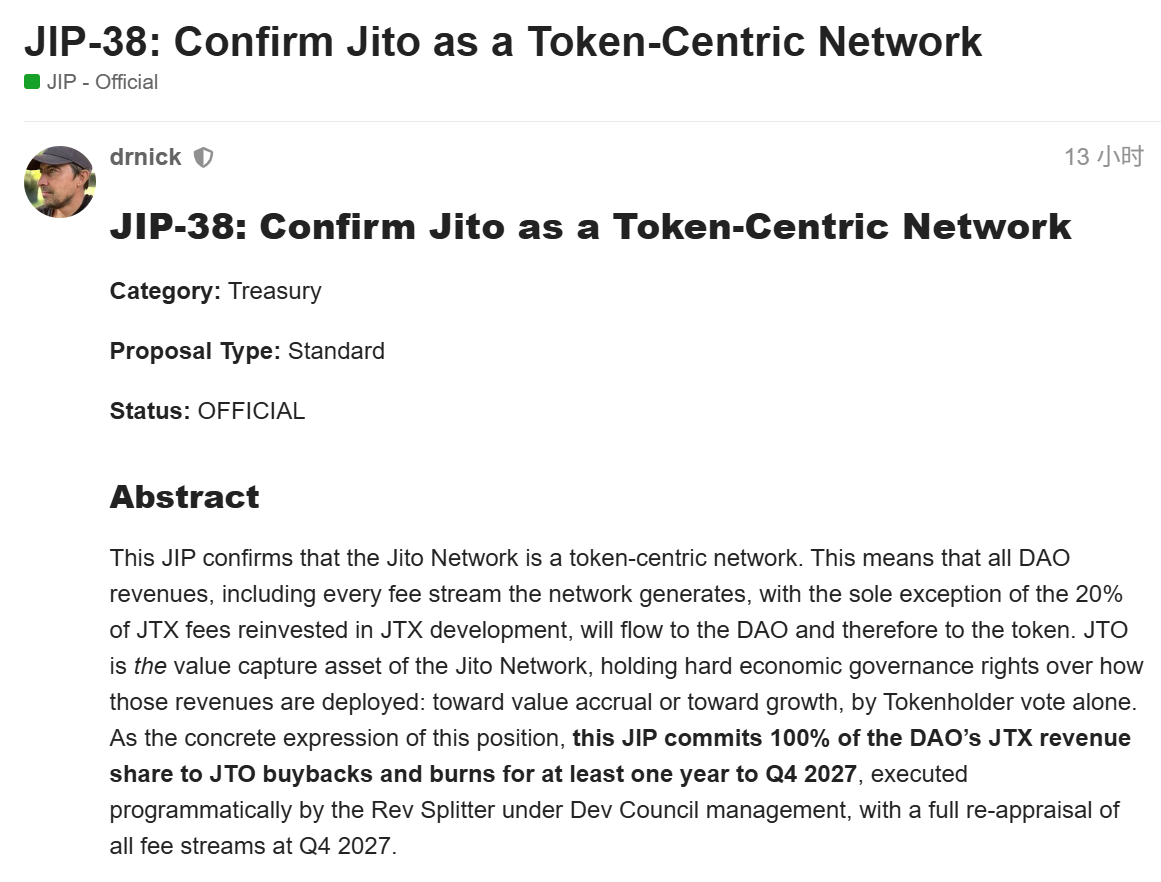

On July 13, 2026, the Solana ecosystem infrastructure protocol Jito announced the new proposal JIP-38. This proposal clarifies the rigid terms of value capture: 80% of the fees from the new trading platform JTX will be used to repurchase JTO tokens on the open market and permanently destroy them through a programmed mechanism, with a commitment period lasting at least until Q4 2027 after the launch of JTX.

The historical high of JTO was $5.30, and it dropped to as low as $0.21 in February this year, a decline of over 96%. Currently, JTO has rebounded from its low to $0.63, reaching a peak of $0.8853.

New JTX Trading Platform

Jito is a project in the MEV (Maximum Extractable Value) infrastructure and liquid staking space on Solana. Its core products include JitoSOL (liquid staking token), Block Engine, and Block Assembly Marketplace (BAM). These products enable validators and stakers to capture MEV more efficiently while providing better block building services for the Solana network. Over the past few years, Jito has gradually improved its revenue distribution and incentive mechanisms through a series of governance proposals.

In July 2026, Jito announced the launch of the JTX trading platform, further extending from infrastructure to the application layer.

JTX is a self-custodial trading platform that will initially support spot and staking-related assets, with perpetual contracts set to launch later this year. Early users will receive priority access, permanent usernames, and referral rewards. The launch of JTX is seen as an important step for Jito to extend its technical advantages (MEV protection, ordering capabilities) into the trading scenario while opening new revenue streams for the DAO.

In the long-standing discussion of "value attribution" in the crypto industry, many project revenues ultimately flow to development teams or related entity equity, while token holders only have governance rights but lack direct economic capture. Jito has clearly positioned itself through JIP-38: the primary revenues of the network should flow to the DAO and be governed by JTO token holders who decide on their use through rigid governance rights.

Core Mechanism of JIP-38

According to the full text of JIP-38 released on Jito’s official forum, the proposal first confirms the Jito Network as a token-centric network: other than the 20% of JTX platform fees for the platform's own reinvestment, all other major network revenues (including JitoSOL related fees, BAM revenue, Block Engine revenue, and the 80% share of JTX) will flow to the DAO and be governed by JTO token holders. The deployment direction—whether for value accumulation (buybacks, destruction, or future distribution) or growth investments (subsidies, incentives, expansion)—must be voted on by token holders through the JIP process.

For the new revenue line, the proposal provides the strongest binding commitment: 100% of DAO's JTX revenue shares will be used for programmed repurchases of JTO in the open market, with all purchased tokens permanently destroyed, executed for at least one year and comprehensively reassessed by Q4 2027. Buybacks and destructions need to be verifiable on-chain.

At the execution level, a Rev Splitter mechanism will be introduced, responsible for collecting JTX platform fees and programmatically executing the buybacks. This mechanism will be actively managed by the Dev Council under a revocable authorization framework and aims to gradually promote automation and decentralization. The Dev Council will need to provide regular reports to the DAO every epoch, including fee collection, JTO purchases, and quantities destroyed along with on-chain references.

Non-JTX revenue flows will continue to execute according to existing arrangements: the BAM subsidy program will operate according to the previous JIP-37 until the hard deadline of Q3 2026 and then return to regular DAO governance. In Q4 2027, relevant analytical institutions will submit a comprehensive fee flow analysis report (covering buyback performance, growth returns, etc.), at which point token holders will decide on the next stage of the revenue routing scheme through JIP—this can include full buybacks and destructions, JTX buybacks combined with other growth investments, distribution activation after buybacks, or any other configuration. The final decision-making power remains with JTO holders.

The proposal emphasizes that this move does not require using existing treasury funds and relies entirely on new revenues. Implementation will be advanced by the Dev Council, CSD, and Jito Foundation, and governance documents will be updated accordingly to reflect the "token-centric" policy.

Turning Point

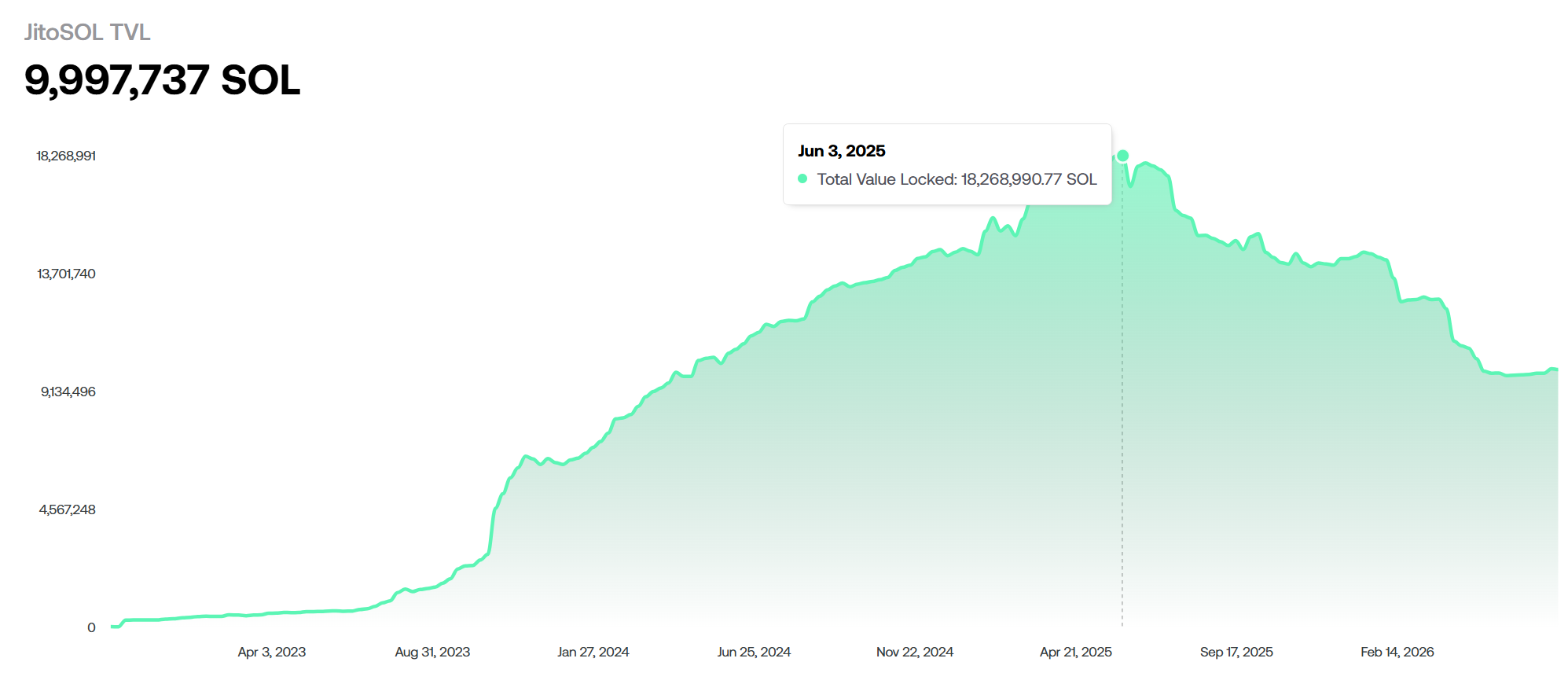

The latest data from the JitoSOL website shows that the amount of SOL staked in its protocol decreased from 18 million in June 2025 to below 10 million.

The LST (liquid staking) market for Solana has changed dramatically. The multi-token matrix of Sanctum, the zero-protocol sharing of Jupiter (JupSOL), and the ever-emerging Restaking yield mechanisms have eaten away at Jito's market share. The staking management fees that Jito used to earn are drying up, and JTX may represent a defensive, last-ditch effort as the main cash cow collapses.

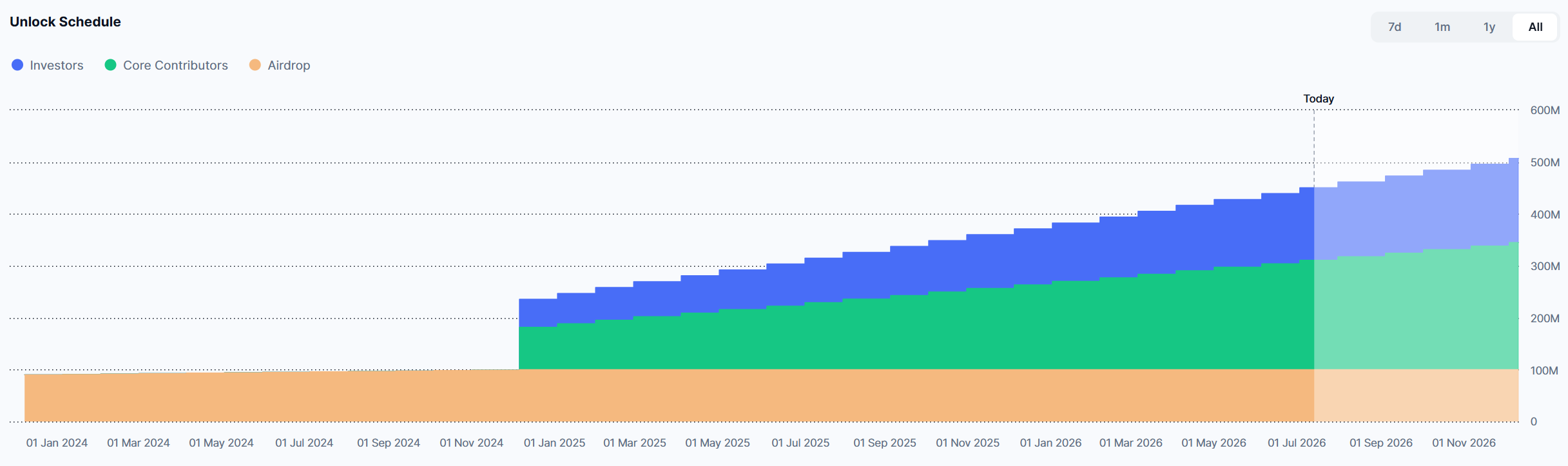

Furthermore, its token unlock pressure has also negatively impacted its price significantly.

Currently, the maximum monthly unlock supply is 1.15% (11.31 million tokens), valued at over $7.3 million. When the market is in a severe bear phase, the continuous selling pressure has become one of the major reasons for dragging down the token price.

For JTO holders, the buyback directly strengthens the token's value capture attributes. Programmed buybacks and permanent destructions will reduce the circulating supply, while the execution method on the open market provides transparency and verifiability. If the trading volume and fee income of the JTX platform meet expectations, the scale of buybacks is expected to provide continuous support.

Of course, the proposal also involves dependency risks: the scale of commitments is tied to the actual revenue of JTX, which is still in its early stages and must face fierce competition from other DEXs and trading platforms in Solana.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。