Authors: Scott Galloway & Ed Elson

Translation: Shenchao TechFlow

Shenchao Digest: SpaceX just joined Nasdaq 100 and received 31 "buy" ratings among 32 analysts, but the stock price dropped by 12%. This is not coincidental—Wall Street analysts have a long-standing optimistic bias, especially those investment banks that underwrote the company’s IPO. When Morgan Stanley sets a target price of $300 (double the current price), while stating "bear market scenario $75, bull market scenario $600," they are essentially saying nothing at all. Ironically, the SEC just abolished the regulations preventing analyst corruption seven months ago.

A considerable proportion of Generation Z (and 10% of Americans) are maintaining long-term friendships with AI chatbots.

- SpaceX joined Nasdaq 100 and received nearly unanimous "buy" ratings—but the stock price still fell by 12%

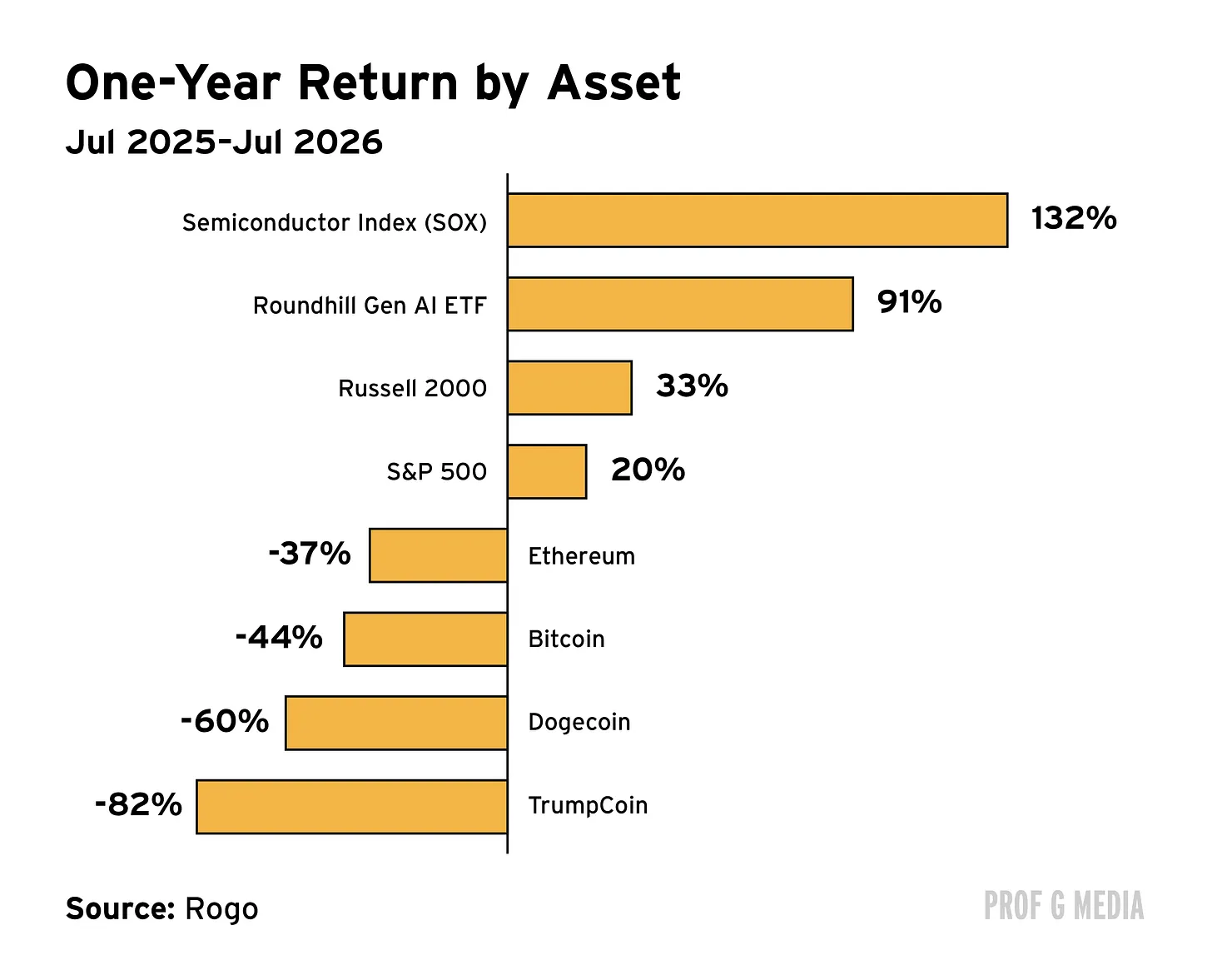

- The cryptocurrency market has lost half its value since last October, along with most of its "cool" factor

- The proportion of first-time homebuyers has hit a historic low, while home prices have reached a historic high

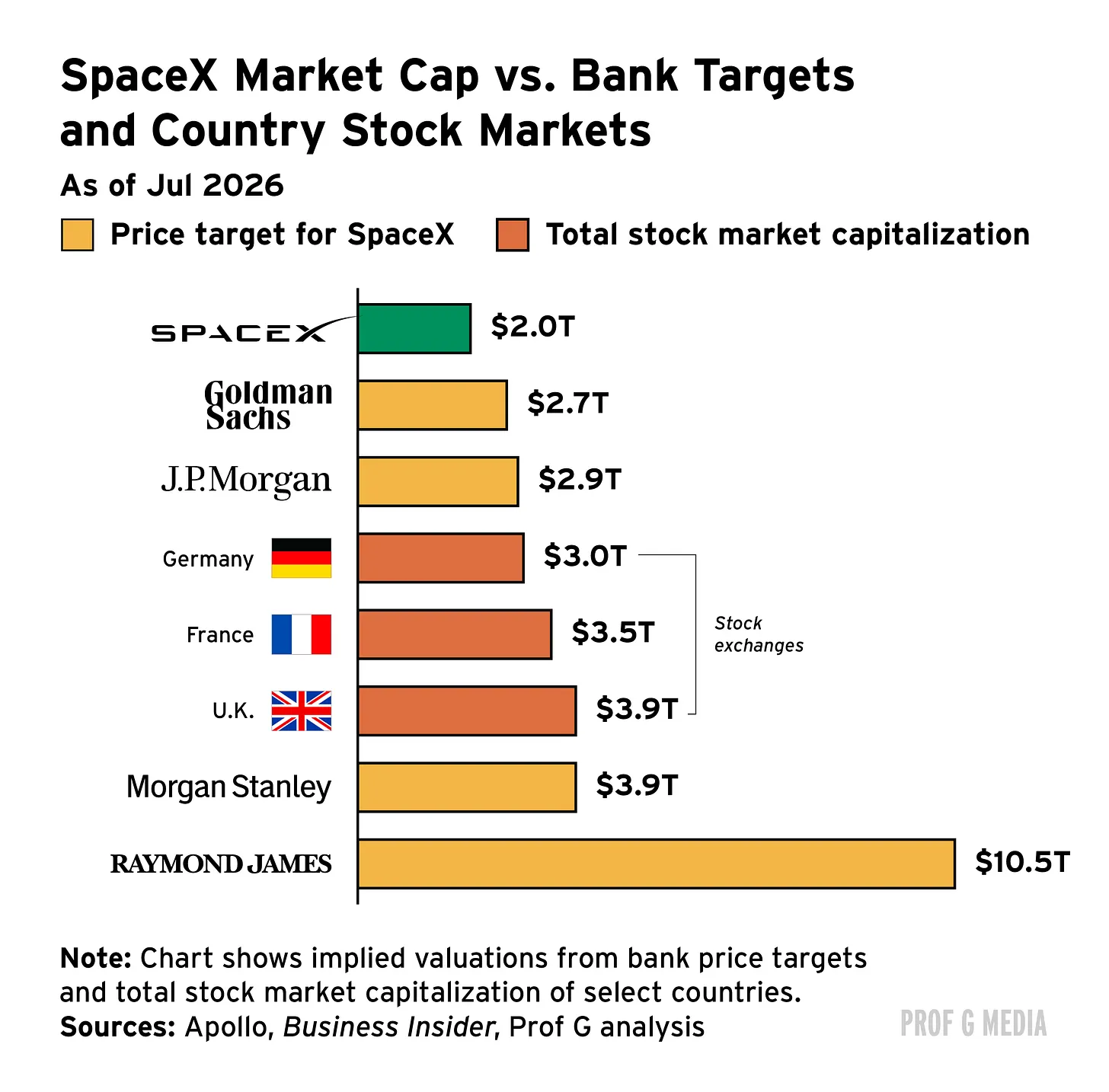

Who determines the valuation of SpaceX?

SpaceX officially joined Nasdaq 100 last week. It qualified through new fast-track listing rules that reduced the required trading history from at least three months to just 15 days and eliminated the minimum public float requirement. Before the rule change, Nasdaq 100 stocks had to have a minimum float of at least 10%.

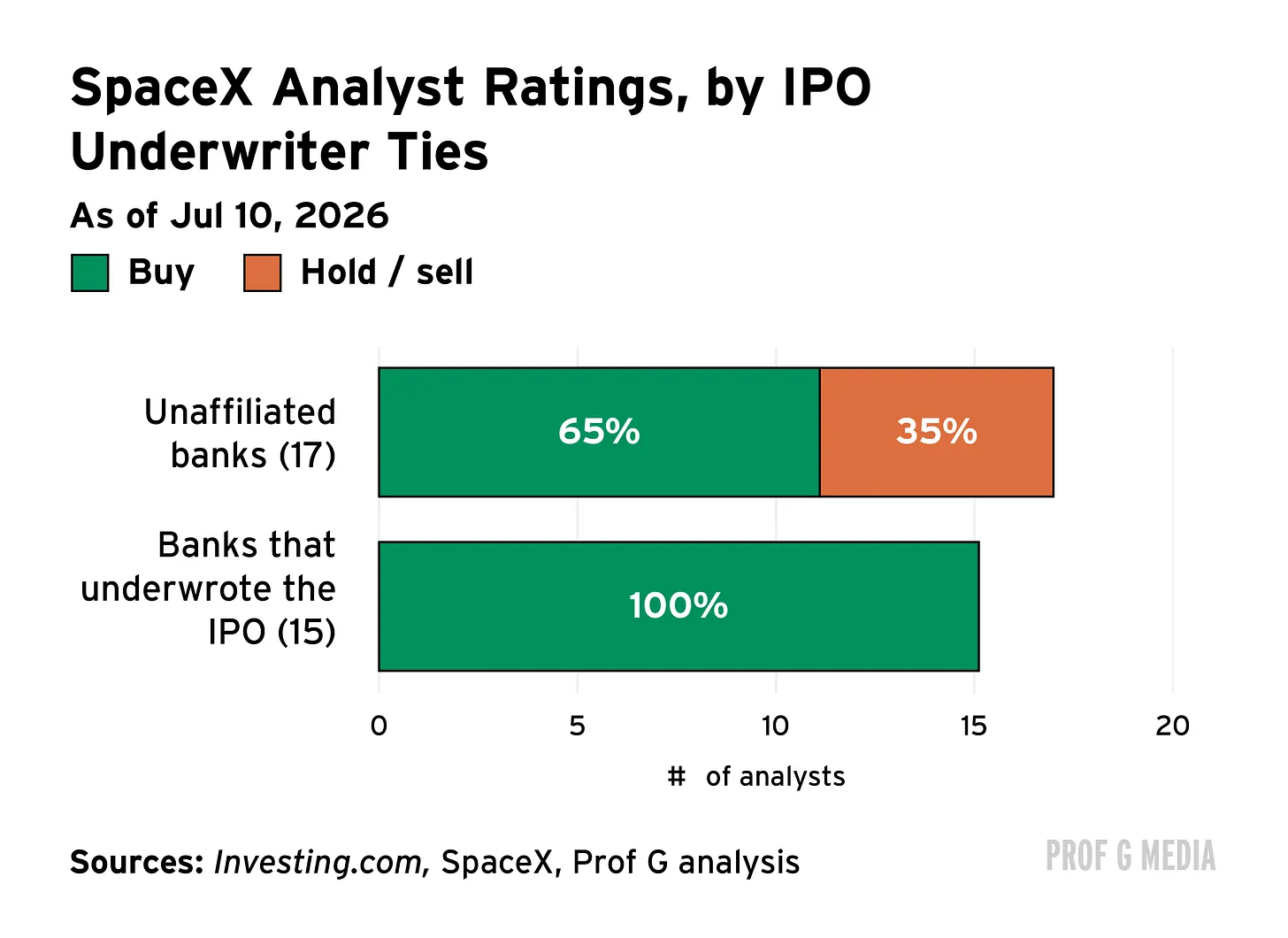

The stock also received a barrage of new ratings from Wall Street analysts. Among the 32 analysts covering SpaceX, only one issued a "sell" rating—which came from CFRA Research, an independent financial intelligence company without investment banking, asset management, or trading departments.

Financial analysts typically set target prices to estimate the future value of stocks and write reports explaining their reasoning for clients. SpaceX's target price is notably optimistic.

Brian Gesuale of Raymond James predicts that SpaceX will reach $800 per share within the next 12 to 18 months. To achieve this, SpaceX's stock price must rise over 400%, which would bring its market value to $10.5 trillion, equivalent to one-third of the U.S. GDP. This would make SpaceX's value exceed the combined value of the U.K., French, and German stock markets.

Research has found evidence that analysts show upward bias in stock recommendations, especially if their banks are connected to the stocks they analyze. This was particularly rampant during the dot-com bubble. A typical example: just two months before Enron's collapse, 16 of the 17 sell-side analysts covering the stock rated it "buy" or "strong buy." Many of them were from banks that had business ties with Enron.

After the bubble burst, investor protection measures were implemented, making it illegal for bank analysts to be influenced by their investment banking departments. However, studies show that even after these reforms, affiliated analysts (i.e., those covering companies with business ties to their investment banking departments) remain reluctant to issue pessimistic recommendations.

The optimistic bias among analysts is deeply ingrained. Even controlling for accuracy, more optimistic analysts are more likely to get promoted to top brokerage firms, and more optimistic analysts are more likely to be mentioned on corporate earnings call.

Nowadays, among all 84 holdings in the Global X Artificial Intelligence and Technology ETF, only 2% of stocks have a net "sell" recommendation.

Analysts from banks that underwrote SpaceX's IPO are generally more optimistic than non-affiliated analysts. 100% of affiliated analysts issued "buy" recommendations. Among the 17 analysts who did not underwrite SpaceX's IPO, only 65% did the same.

Despite the optimistic ratings, SpaceX's stock price fell by 12% last week and is down 36% from its peak.

Morgan Stanley's target price is $300—double the current stock price. They also wrote that their bull market scenario is $600 and the bear market scenario is $75. They are telling us: it might drop 50%, but it could also rise 300%. So they’re essentially saying nothing.

What we learned from the dot-com bubble is that structural conflicts of interest are embedded in stock research. If you give a company a "sell" rating, that company is unlikely to be interested in working with you to underwrite their IPO, from which you could earn a 1% underwriting fee. So, it’s natural for Musk to choose investment banks that are friendly to him.

The SEC attempted to combat this in 2003 by regulating the separation of investment banks' research departments from the banking departments responsible for securing underwriting fees. Seven months ago, this rule was terminated by the SEC.

Afterwards, former SEC Chairman Arthur Levitt wrote an article in The Wall Street Journal titled "SEC May Enable Wall Street Analysts to Be Corrupt Again." He warned of the dangers of abolishing this regulation.

I don't think analysts have the same influence as they used to. In the 90s, these analysts were on CNBC all day long. But today is different, as there are so many other sources of information.

To some extent, I find these target prices embarrassing. Years from now at a party, people will ask you, weren’t you the one who said SpaceX would hit $300? Isn’t that going to be awkward?

For those unfamiliar with these ratios, no company trades at 100 times revenue. This simply does not happen; companies trading at very high sales multiples are software companies, where revenue generally converts directly into profit—there are not many fixed costs. For SpaceX, it has enormous costs: rockets, Nvidia GPUs, etc. It is not only losing money, but losing astonishing amounts.

Do you really want to pay 100 times? You would have to wait a hundred years to recoup your money. Its growth is also not fast: the growth rate is around 15%. SpaceX markets itself as an AI company, but it only has a 3.5% market share, so this is really just hype.

Capital Migration

The cryptocurrency market has erased over half its value in the past eight months, with $8 billion in outflows from Bitcoin ETFs over the last eight weeks. Meanwhile, AI has become the new frontier. It is the most exciting technology for people and captures the same sense of disruption and potential that cryptocurrency once represented.

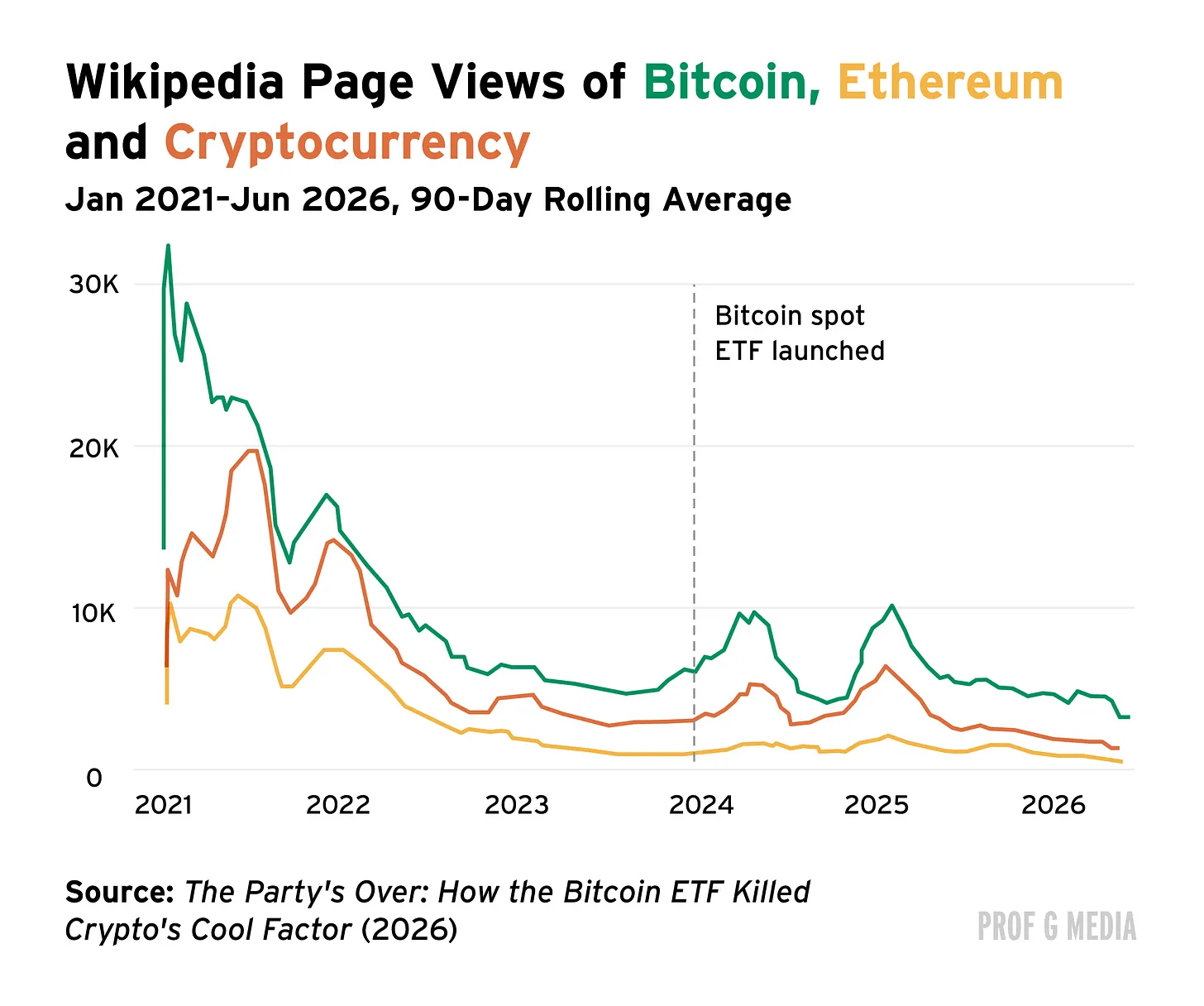

Cryptocurrency has lost its cool, with academic research to support this. A recent paper by David Krause, Associate Professor of Finance at Marquette University, pinpoints the turning point to a specific date: January 2024, when the first Bitcoin ETF launches. Krause's argument is that the moment Wall Street made cryptocurrency simple and mainstream, it no longer felt cool.

As a proxy for public interest, he measured the frequency with which people search for cryptocurrency terms and visit related Wikipedia pages. After the Bitcoin ETF launches, he found that by June 2026, Google searches for Dogecoin dropped by 63%, searches for "cryptocurrency" fell by 47%, and visits to both pages on Wikipedia decreased by 76% and 56%, respectively.

The only selling point for cryptocurrency is that prices are rising, people want to buy it because they know that something someone bought for $1 is now worth $60,000. So it really is just a trend-based asset, the type of thing you talk about at parties.

But now, when you say you hold Bitcoin, you are no longer doing something exciting. When the SEC Chair is a crypto bro, and Secretary of Commerce Howard Lutnick is a crypto bro, and everyone from Epstein Island is involved... it is no longer anti-establishment. The claims of use cases have also evaporated.

If you want to sound exciting, you might tell people you are betting on the prediction market.

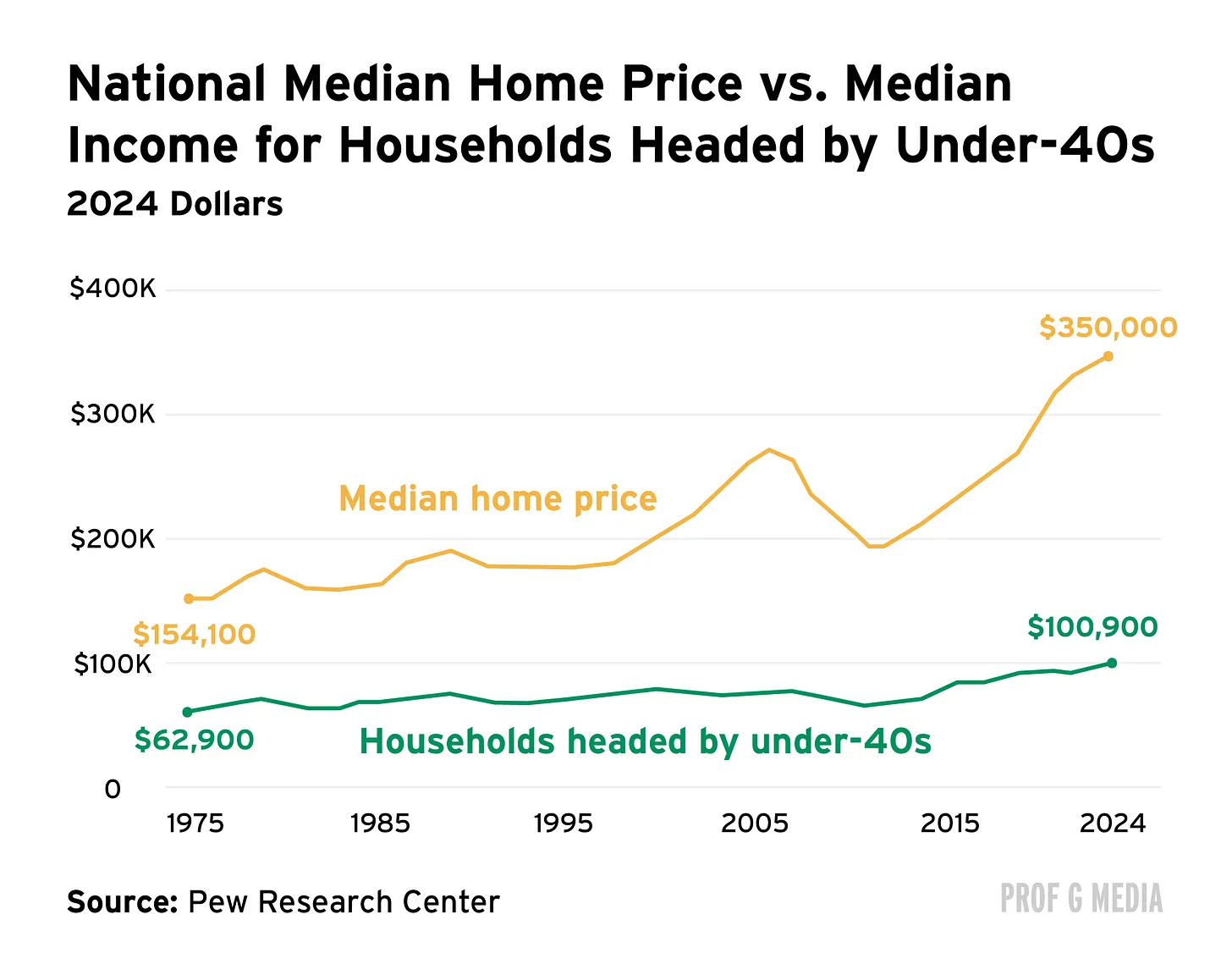

Home Prices Shouldn't Only Rise

The U.S. housing market is showing new signs of stress. Last month, the median price of homes in America hit a historic high of $408,800, and in April, the National Association of Realtors reported that the proportion of first-time homebuyers dropped to 21%, the lowest level since NAR started tracking data in 1981.

This is part of a broader trend: Homeownership is increasingly out of reach for the average American. In fact, 75% of homes currently on the market are unaffordable for the typical family.

The housing market looks particularly bleak for young people. Between 2019 and 2024, inflation-adjusted median home values have risen by 30%, while median inflation-adjusted household income for those under 40 has only increased by 9%.

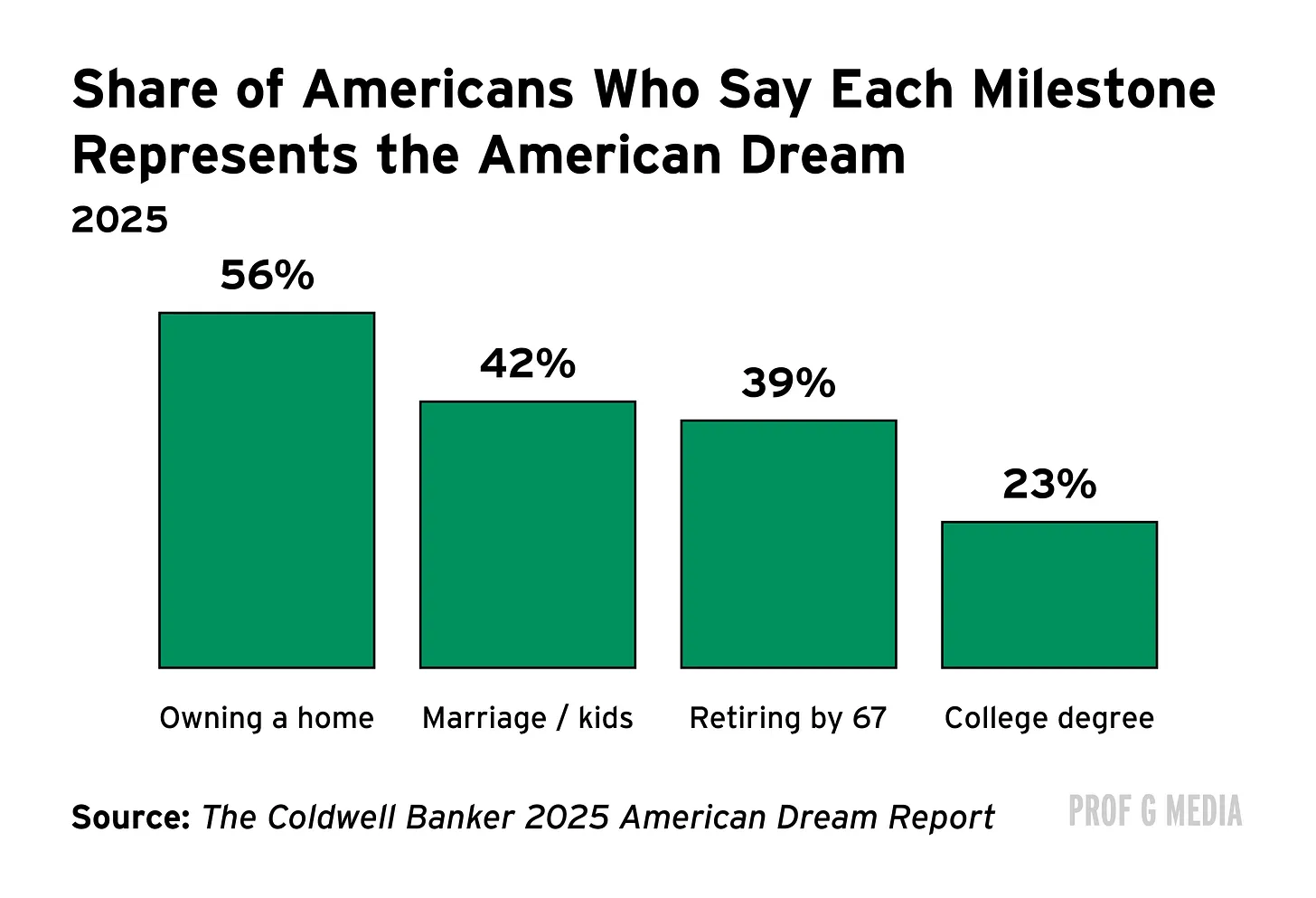

Americans still want to buy homes. 56% of Americans believe homeownership represents the American Dream, and nearly two-thirds of Americans who do not currently own homes wish to buy one within the next five years. Affordability issues make this goal more challenging—and delay other life milestones. Nearly one-fifth of prospective homebuyers delay marriage or having children until they own a home, and 17% delay career changes or getting pets.

Homeownership is a symbol of American culture but is also seen as a savvy financial decision. 93% of Americans believe buying a home is "absolutely" or "probably" a better investment than buying stocks. But this is not necessarily the case.

Moody's compared two individuals with annual incomes of $150,000: one a homeowner purchasing a $500,000 home (with a 20% down payment and a mortgage interest rate of 6.25%) and the other a renter paying $2,500 a month in rent, with that rent increasing 3% a year, who invests the difference at a 10% return. After 30 years, assuming average annual rent and home price growth, the renter's net worth would be $2.8 million, while the homeowner's would be $1.6 million. This analysis does not account for taxes.

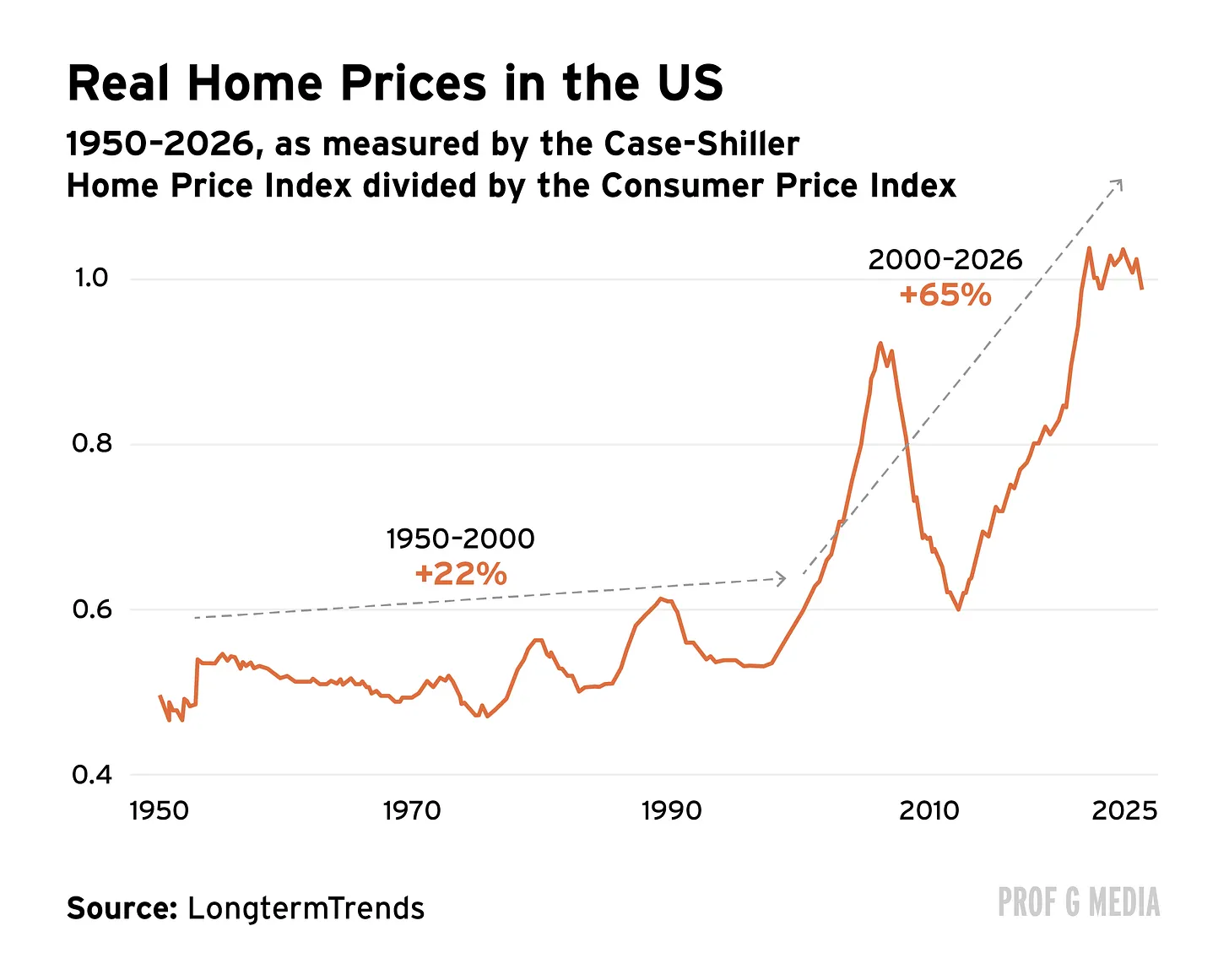

If you look at the long-term history of home prices, there is no reason to believe they should rise. But it has become an investment category. If you talk to your grandparents, they never discuss the concept of real estate investment. They bought the houses they needed to live in.

So how did we end up in this situation? The government incentivizes people to buy homes, so they want prices to rise or at least remain stable. You hear politicians say they want young people to have affordable housing, but they do not want to harm the housing values for retirees who depend on these prices because young people do not vote as much as older people. Well, you can only choose one.

Moreover, if you buy an asset at a historical high point, and it truly seems unaffordable for ordinary people like yourself, it may indicate that it's not a good investment.

I understand the emotional impulse to own your own place, but emotional impulses are different from investment decisions. If you look at housing's long-term returns relative to the stock market, housing has underperformed the stock market significantly.

This dialogue has an interesting similarity to the cryptocurrency phenomenon: the drive supporting the rise in cryptocurrency prices stems from people's fundamental belief that it will continue to go up. I think there exists a fundamental belief between Americans and those currently without homes that home prices will rise. If you believe that, you are more motivated to buy a home rather than invest in something else.

The only reason you should assume your home will be worth more in five years than it is today is if you invest in renovations to make it better, or if you believe that the specific location where you bought will become a hot community where everyone wants to live.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。