Article Translated by: Block unicorn

Tokenization stitches together two completely different worlds: one being always online, permissionless DeFi protocols with prices that fluctuate every few seconds; the other being traditional funds, where settlements adhere to a set timeframe managed by a group of licensed holders.

Integrating the two requires exceptional coordination skills, but for those able to successfully achieve this, there is immense value to be had. In today’s article, I will explore who is orchestrating the connections between these two worlds and who is extracting value from them.

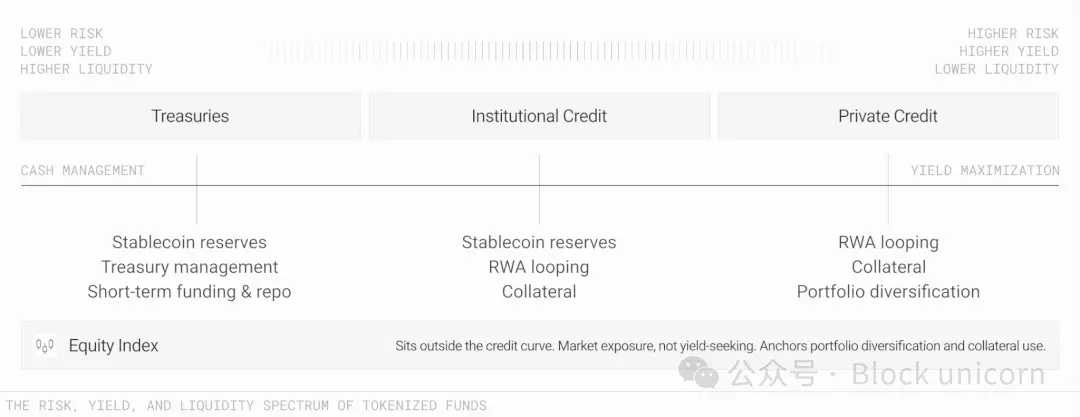

The scale of tokenized real-world assets (RWA) pools exceeds $33 billion, with tokenized U.S. Treasury bonds accounting for about $15 billion. However, it’s noteworthy that its share has dropped from 55% to below 45% in just one year. Meanwhile, the sizes of other tokenized funds have grown, including institutional credit funds (e.g., Apollo’s ACRED) and private credit funds (e.g., Henderson Park’s JAAA).

The maturation of tokenization offers financial executives or chief financial officers managing corporate cash a range of choices with varying risk preferences. Those seeking low-risk, low-return but high-liquidity investments can opt for treasury bond funds, while those pursuing higher yields and stronger programmability can choose riskier investment options. The security of yield is no longer as concerning as it once was. These tools supported byTreasuries are audited by the same auditing firms that audit traditional bonds.

This is the strongest argument for tokenizing real-world assets about to create a wave among institutional investors.

If someone asks me what the difference is between off-chain currency and on-chain currency, I would say it is composability. It is composability that allows one dollar to serve multiple purposes across channels, enabling greater compounded growth. The ability to redeem instantly and make your funds work more efficiently makes them seem like funds on steroids.

Traditional finance forces us to make choices between yield, liquidity, and transferability. Tokenized funds, if managed properly, can allow us to enjoy all three at once.

But “proper management” is no easy task. The composability of funds involves an engineering problem.

Stitching Together Two Distinct Worlds

Blockchain brings speed, cost-efficiency, and rapid settlement to tokenized risk-weighted assets (RWA). However, tokenized money market funds remain funds, not stablecoins. They still require updating their net asset value daily based on the fund manager’s schedule. They still need to maintain a KYC-verified holder population. For instance, BlackRock's BUIDL has a minimum investment threshold of $5 million, while Circle's USYC is restricted to non-U.S. participants. They still need to adhere to redemption cutoff times since their underlyingTreasuries’ settlement relies on off-chain infrastructure, which has a settlement cutoff time of 5 PM Eastern Time.

This is an essential legal substance of the product. If daily net asset value settlements are removed, it ceases to be a money market fund. If the whitelist mechanism is abolished, the SEC will come knocking.

So, how can a fund maintain its established timelines, holder settings, and redemption windows while allowing tokens representing that fund’s shares to flow at internet speed? The fund requires a specifically built infrastructure to maintain net value at the end of periods, support epoch-based settlements, and adhere to strict legal boundaries when transferring assets across blockchains. This poses a tricky coexistence problem.

LayerZero and Centrifuge recently released a report detailing how they are addressing this issue.

Resolving Points of Conflict

Three points of conflict determine whether this coexistence model can succeed. If the coordination layer can handle these points of conflict correctly, the funds can operate at internet speed without violating legal boundaries.

The first is price.

What is the value of the token between two net asset value settlement periods? Some issuers will freeze the token price at yesterday’s level and accept that stagnation. When interest rates fluctuate at noon, a price freeze can be easily manipulated. While continuous price changes are harder to manipulate, they are also more difficult to align with the fund's actual accounts.

The second is compliance factors.

Where does the whitelist verification layer run? If it runs every time a transfer is made, then tokens cannot access open DeFi and can only transfer between approved wallets. If this layer is encapsulated in a vault, the vault will hold regulated shares and issue a freely transferable receipt token to holders who have completed one KYC verification. This receipt can be composable through DeFi, with compliance embedded in the vault rather than being checked at every transfer. Centrifuge's deRWA framework is a great example.

The third conflict occurs during cross-chain asset transfers.

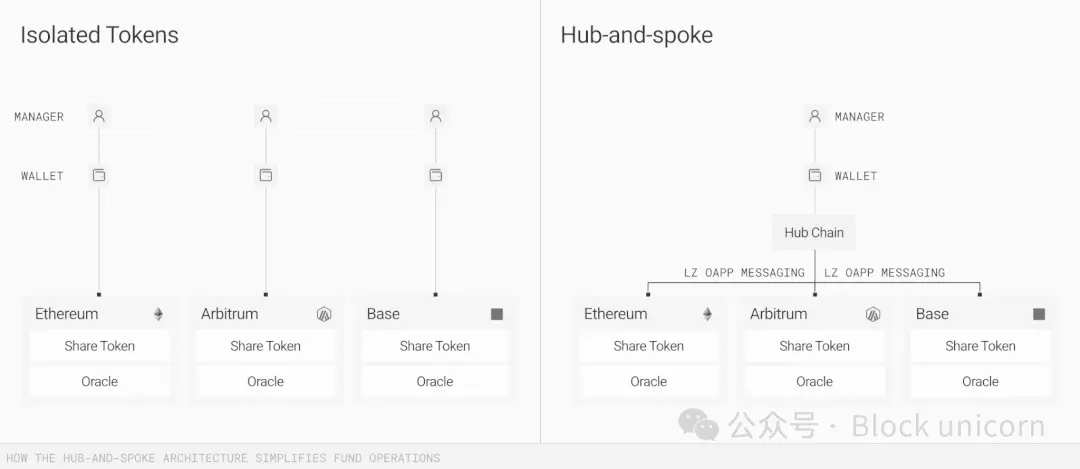

When tokenized funds are deployed across nine chains, you need a unified data source to clarify ownership and values. While on-chain infrastructure can be real-time updated, once discrepancies arise, updates and verifications are still needed across nine chains. The more fault points there are, the higher the likelihood of errors.

LayerZero and Centrifuge address this issue by constructing a central radiating model. In this model, one authoritative chain manages net values, accounting, and compliance. The message layer (coordinated by LayerZero in this instance) pushes these updates to the radiating chains where the tokens are utilized.

Centrifuge’s V3 architecture is built on this model, where each funding pool chooses a central chain as its data source, broadcasting chains as distribution terminals for deposits, and enabling DeFi composability. LayerZero is responsible for transmitting operational data between chains to ensure synchronization of net value updates, compliance directives, and cross-chain balance statuses.

What I mentioned before is precisely this enviable yet crucial coordination mechanism that brings value to those who can execute it. Whoever can maintain the consistency of the fund's authoritative status across chains will find it hard to be replaced. While fund managers still control timelines and blockchains still hold composability, some intermediary participant must achieve both simultaneously.

The weakest part of asset transfer is the tally of transferred assets.

When assets are transferred between different chains, they may temporarily disappear from the fund’s visible asset balance sheet. Centrifuge V3 will issue tokenized confirmation information for assets in transit, so that even while the underlying tokens are still in the transfer process, the fund’s balance sheet can maintain continuity. This is akin to off-chain date accounting. While tedious, it is crucial.

Despite these conflicts, why should institutional investors still consider tokenized funds?

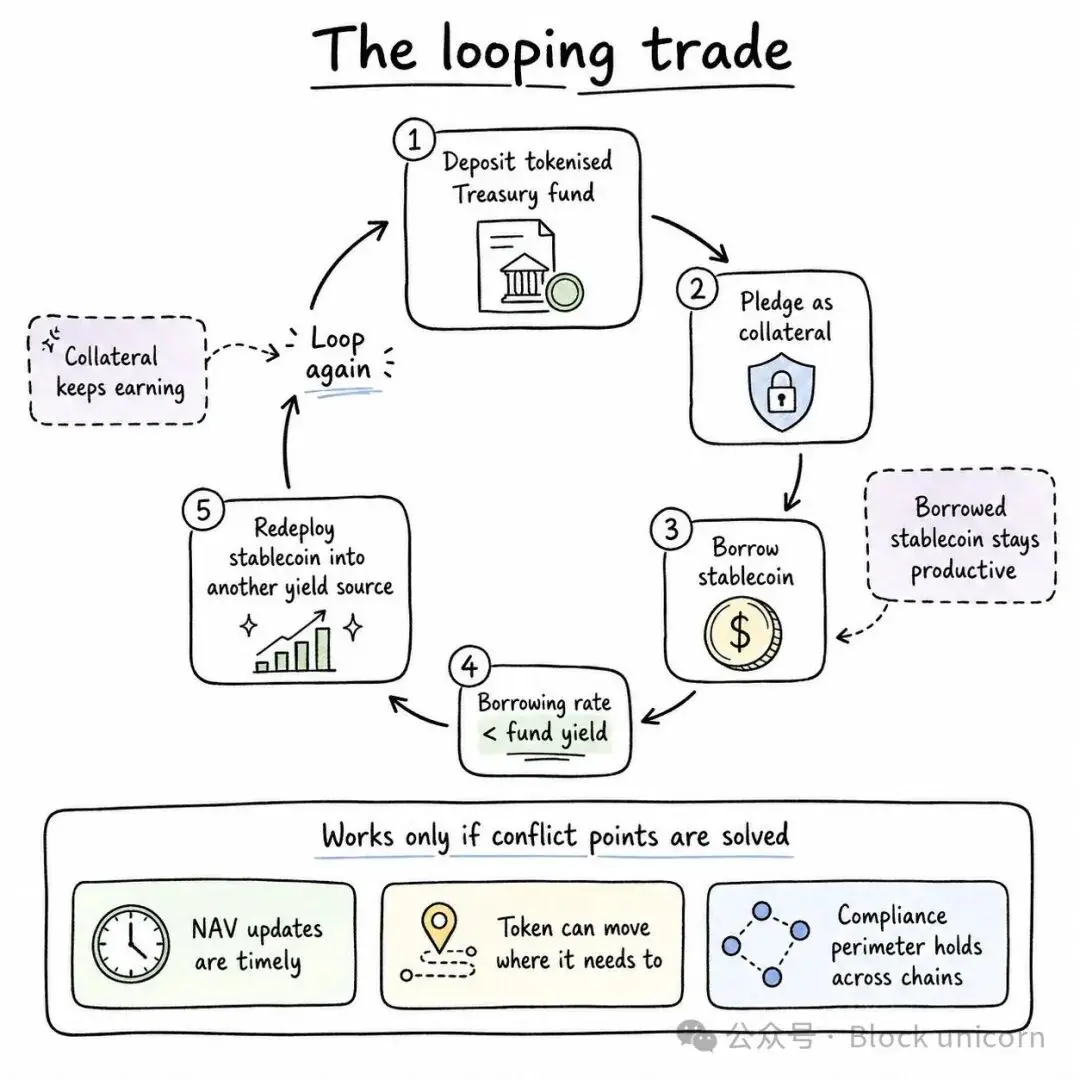

One of the best ways to optimize idle funds through tokenization is through circular trading. Financial executives can deposit tokenized treasury funds and use them as collateral to borrow stablecoins. If the borrowing rate is lower than the fund's yield, holding that fund can yield returns. Afterward, the financial executive can redeploy the stablecoin funds into other income sources and repeat this cycle.

The entire circular trading can only operate effectively once the above conflict points are resolved. This poses the next challenge for those building tokenized infrastructure. These points of conflict have been exploited in the past. For instance, if the on-chain net asset value price of a smaller tokenized product remains unchanged for two to four hours and lags behind the underlying asset price, arbitrage opportunities can arise before the next net asset price surge.

When off-chain net values trigger liquidity constraints, if independent on-chain smart contracts attempt to process token redemptions immediately, redemption gate conflicts may occur. This can result in smart contracts holding “isolated” or unexecuted token trades that continuously attempt to execute simultaneously, conflicting against off-chain limits.

Currently, large private credit funds and business development companies (BDC) are facing this situation. Three weeks ago, Apollo Global's $26 billion private credit fund—the Apollo Debt Solutions Fund (ADS)—had to set a redemption limit of 5% after investors attempted to redeem about 16.8% of shares. If a similar situation arises with funds trading tokenized versions simultaneously, the possibility of conflicts in redemption pathways would be hard to dismiss. In the second quarter, investors redeemed $15.6 billion from widely held private credit funds, which was higher than the approximately $13.9 billion in the previous quarter.

Failures may occur during cross-chain message transmissions, leading to positions that are not fully settled. Only through monitoring each mode of failure and ensuring that qualified personnel are responsible can trust be gained from institutional investors.

If tokenization is to realize its potential, it must address the following challenges. It is not merely about putting U.S. Treasuries onto a blockchain or creating a new asset class. Those constructing the infrastructure must break the outdated rules that force investors to choose between yield, liquidity, and transferability. If tokenization can allow dollars to serve multiple roles simultaneously without undermining the credibility brought by existing safeguards, then those institutions holding billions of dollars in cash will surely take notice.

As I previously wrote, SWIFT, as today’s coordination layer, has a value and influence that surpasses either end of the network it serves. The value of Visa also exceeds that of all global banks it serves, except for JPMorgan.

This is the motivation behind taking on the role of the coordination layer in the evolving world of finance. It allows participants to secure a place in the capital markets over the next decade. Centrifuge is defining the role around funds, while LayerZero is responsible for constructing the bridges connecting various components.

That’s all for today, and I’ll see you in the next article.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。