Retail investors are buying against the trend, with the scale reaching the 90th percentile in nearly three years, becoming the biggest support.

Written by: Dong Jing, Wall Street Insights

High-beta momentum stocks in the U.S. stock market have encountered the most severe sell-off this round, but the market has not fallen into panic selling.

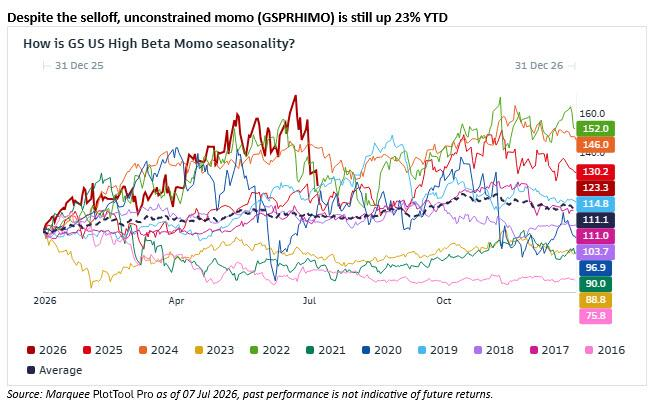

Goldman Sachs' trading desk characterized the trading on July 7 as "an ugly day" in its latest recap report. Due to Samsung's revenue being slightly below buyer expectations and the news of DeepSeek developing its own AI chips, the global AI sector faced a chain sell-off, with the high-beta momentum factor (GSPRHIMO) plunging about 6% in a single day, and the cumulative decline over five days exceeding 20%, beyond Goldman Sachs' previous expectations of a "brief summer pullback."

Goldman Sachs trader Guillaume Soria stated that the speed and magnitude of this round of sell-off are unprecedented since the switch from the "stay-at-home narrative" to "reopening" during the COVID-19 pandemic, but at that time, there were stronger fundamental catalysts, which are not present in this round.

Despite the fierce selling, Goldman Sachs' trading desk clearly stated that "panic mode has not yet been seen on the trading desk." The current de-risking behavior remains orderly, primarily driven by systematic/factor flows rather than panic liquidation. Meanwhile, retail investors have become the most important supporting force in the market—turning to net buying during the day, and the net inflow at the close was at the 90th percentile in nearly three years.

It is worth noting that UBS cash trading desk data also shows that excess selling flow remains mild and does not constitute a panic signal, but it warns that if the selling continues, the situation may shift from orderly to panic liquidation.

The AI sector faces chain impacts, with momentum factor's 5-day decline exceeding 20%

The trigger for this round of sell-off comes from the global AI industry chain.

On July 7, Samsung released preliminary results that, although recording a record operating profit, had revenues slightly below buyer expectations, causing the stock price to drop 9% in the South Korean market in one day. Meanwhile, DeepSeek announced its plan to develop its own AI chips, further exacerbating market concerns about the hardware landscape of AI, triggering a spillover sell-off in the global AI complex.

In the semiconductor ETF and leveraged ETF sectors, trading volume surged sharply. According to Goldman Sachs data, SOXL's trading volume was 35% higher than the 30-day average, with this product having cumulatively fallen 50% from the historical highs set 10 trading days ago; DRAM-related trading volume was 60% above the average; SMH's trading volume was 30% higher.

Goldman Sachs' TMT experts led by Peter Bartlett pointed out that although the overall fundamental view of the technology sector remains positive, especially among tech-specialist investors, buying and defensive actions in recent weeks have clearly become "selective," significantly cooling compared to the fervent buying pace of May and early June.

Goldman Sachs' trading desk noted that SK Hynix's upward guidance and META's cloud business dynamics were seen as triggering factors, but "the fundamental view remains positive," which is one of the important reasons why it has not yet evolved into panic.

Orderly de-risking instead of panic liquidation, but hidden dangers remain

Despite the fierce market sell-off, both Goldman and UBS trading desk data point to the same conclusion: the core of the current sell-off is de-leveraging, rather than new short positions.

The UBS cash trading desk observed that the selling pressure mainly comes from long-term accounts, while hedge funds primarily engage in tactical operations—mainly short covering and selective position building, which corroborates the judgement of "de-leveraging driven" rather than "bearish driven."

However, the hidden dangers cannot be ignored. From a technical perspective, the high-beta momentum (GSPRHIMO) and the broad AI index (GSTMTAIP) have not yet entered the oversold zone despite the current decline, with a year-to-date increase of still 23%; and from a 5-year dimension, related positions remain in an extremely crowded state.

Goldman Sachs' trading desk candidly stated: without upward catalysts, there is still more room for further sell-off.

Furthermore, July has historically been one of the months where the momentum factor performs the worst, and this month looks set to become the worst July on record for high-beta momentum. Historical data from Goldman shows that the maximum historical drawdown of this factor is about twice the current decline, indicating that if a shift in market leadership occurs, the current decline could still significantly expand.

As institutions generally withdraw, retail investors’ contrarian buying has become the most significant structural feature of this market round. Goldman Sachs data shows that retail investors turned to net buying during the day and continued to increase their positions, eventually reaching a net inflow scale that was at the 90th percentile in nearly three years, being one of the most important supporting forces in the market of that day.

At the same time, the internal market structure has not collapsed completely. There were 283 constituents of the S&P 500 that closed with gains that day, showing a certain breadth of support, echoing Morgan Stanley strategist Michael Wilson's earlier proposition of "the market continues to broaden."

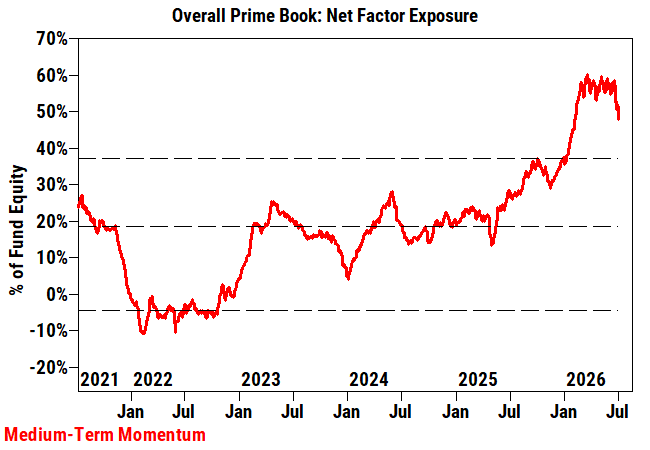

Facing the current situation, Goldman trader Guillaume Soria's attitude tends to be cautious, suggesting that characterizing the 20% decline over 5 days as a "healthy pullback" is too far-fetched, but pointed out that after the strong performance of 57% in the first half of the year, the extreme positions of the momentum factor have been reset—from a historic peak a month ago to the 60th percentile in a one-year retrospective, with overall performance still remaining strong.

Soria believes that the current situation may be in the "late stage" of this round of adjustments, but if negative news expands the cracks into chasms and market leadership shifts, it could evolve into a more profound correction.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。