Why did a $216 million Bitcoin sale to replenish reserves not reduce the $1.25 billion sale limit at all?

Written by: David Christopher

Translated by: Saoirse, Foresight News

Recently, Strategy disclosed that from June 29 to July 5, the company sold 3,588 Bitcoins, totaling approximately $216 million. The proceeds from this sale were used to distribute STRC dividends while replenishing the US dollar reserves previously consumed for dividends. Even after this sale, Strategy still claims that its $1.25 billion reserve building limit remains fully available.

In other words, this $216 million Bitcoin sale used to replenish reserves does not take away from the $1.25 billion limit designated for building reserves. The two are distinctly defined financially: replenishing reserves versus building reserves. However, both operations essentially inject funds into the same US dollar reserve for the same purpose, differing only in accounting classification.

In other words, this Bitcoin monetization plan never locked the total maximum sales scale at $1.25 billion. This limit only restricts one type of operation: obtaining funds to build US dollar reserves through Bitcoin sales. Apart from this, the plan also allows Strategy to sell Bitcoin for other purposes, with this sale being a typical example.

Three Major Funding Pools

On June 29, after the stock prices of MSTR and STRC had been under pressure for several weeks, Strategy launched its Bitcoin monetization plan as part of its overall digital credit capital framework. The plan allows the company to sell Bitcoin for three core purposes:

- Building Reserves: Selling Bitcoin can raise up to $1.25 billion to strengthen US dollar reserves;

- Covering Preferred Stock-related Expenses: Selling Bitcoin to pay fixed dividends on preferred shares, debt interest; or selling Bitcoin to replenish reserves after using reserves for interest payments — when management determines that selling Bitcoin is more advantageous than issuing common stock;

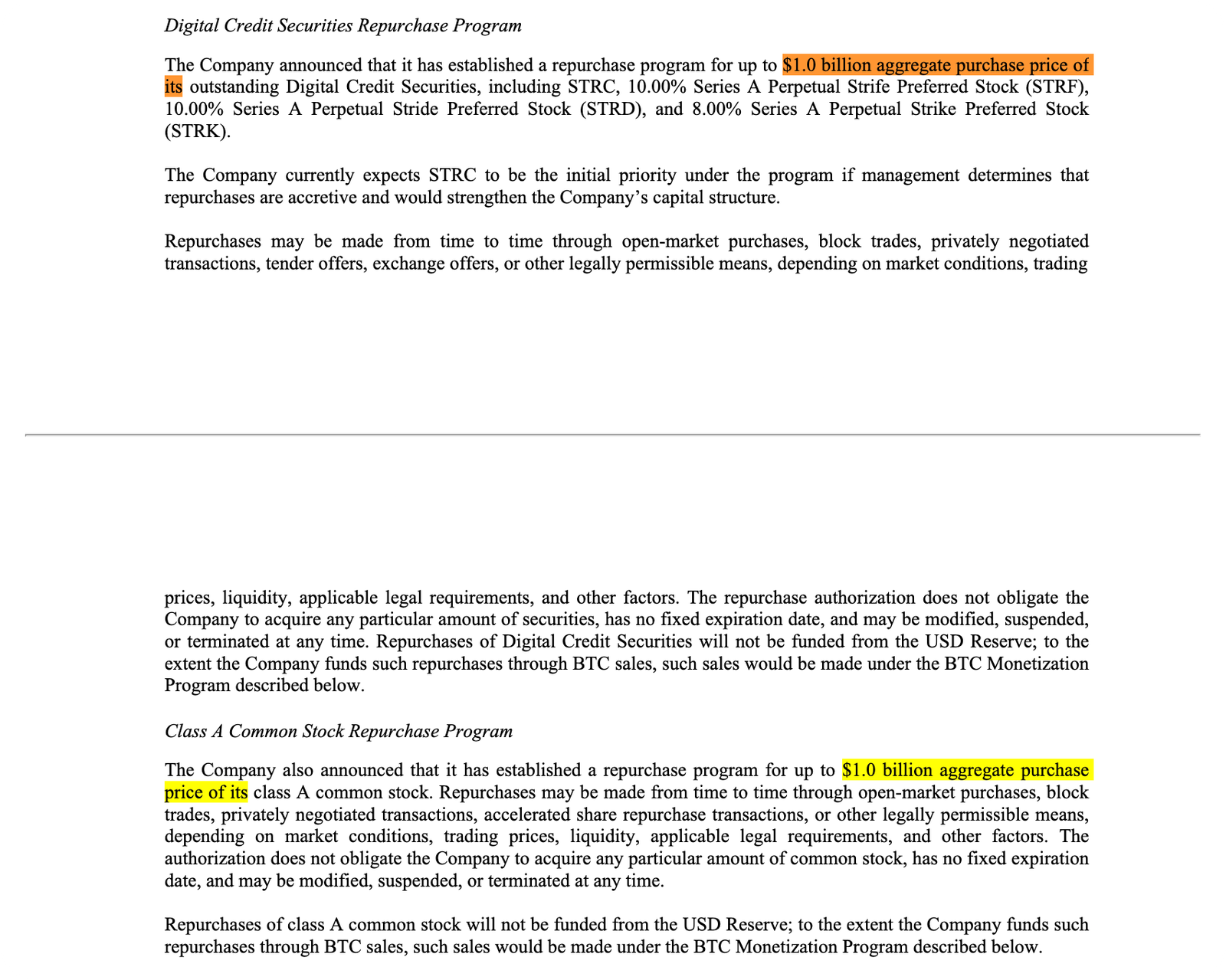

- Share Repurchase Funds: Selling Bitcoin for repurchasing preferred shares or MSTR common stock, with a maximum limit of $1 billion for each category, and proceeds from sales can also cover related expenses such as taxes and fees from repurchases.

Only the first funding pool has the widely circulated $1.25 billion limit; the third category of repurchase channels can liquidate a total of $2 billion worth of Bitcoin. Just these two categories of channels with clear limits can liquidate over $3 billion worth of Bitcoin, excluding additional funding pools without limit restrictions for dividend payments and reserve replenishment.

Differentiating "Building" from "Replenishing": The Blurry Lines of Accounting Operations

The sole purpose of establishing US dollar reserves is to pay preferred stock dividends and debt interest. According to current rules, these funds cannot be used for stock buybacks. As of June 28, the balance of US dollar reserves was $2.55 billion, sufficient to cover the company's annual fixed expenses of $1.76 billion, supporting interest payments for about 17 months. The board has set a bottom line: reserves must cover at least 12 months of interest payments unless the board approves a lower standard.

That is why the distinction between "building reserves" and "replenishing reserves" is worth careful examination:

- Selling Bitcoin before distributing dividends and adding cash to reserves: defined as building reserves;

- Using reserves first to pay dividends and then selling Bitcoin to fill the reserve gap: defined as replenishing reserves.

The plan distinguishes these as two types of operations, but the ultimate purpose is entirely the same: selling Bitcoin for cash to pay preferred stock dividends and interest. Related details have long been disclosed externally, but this sale incident intuitively reflects how convenient this classification rule is for the company. Strategy sold $216 million worth of Bitcoin, with the funds used for dividends and replenishing reserves, yet still claims that the $1.25 billion reserve building limit remains untouched.

Now the market needs to understand this "Strategy exclusive terminology." "Building" and "replenishing" are merely nuanced accounting expressions but directly determine whether a Bitcoin sale consumes the public limit.

From Simply Accumulating Bitcoin to Active Capital Management

In the announcement on June 29, Michael Saylor stated that this capital framework is designed to meet the company's needs for liquidity, standardized operations, and active capital management. CEO Phong Le expressed it more straightforwardly: Strategy is transforming from simply issuing stocks to acquire Bitcoin into comprehensive active capital operations.

As analyzed by Matt Walsh and Jeff Dorman from Castle Island during their podcast appearance last week, Strategy has effectively transformed into an actively managed hedge fund.

Previously, the market narrative regarding Strategy was quite simple: issue MSTR common stock and buy Bitcoin to provide investors with leveraged Bitcoin exposure. But the new framework has completely changed this logic: the company now actively trades its various capital instruments to balance multiple pressures among common stock, preferred stock, US dollar reserves, and Bitcoin assets.

Walsh and Dorman pointed out that this operational model is internally full of contradictions: issuing common stock can secure preferred stock dividends but lowers the valuation premium of Bitcoin held by MSTR; selling Bitcoin can extend the cash availability period but completely undermines the core narrative of "never selling Bitcoin"; fully paying preferred stock can stabilize market confidence but continuously depletes cash reserves; reducing preferred stock dividends can preserve liquidity but might lead to a sharp decline in preferred stock prices.

The accounting loophole of the reserve limit is a microcosm of this strategic transformation. Bitcoin is no longer the core asset hoarded by the company for the long term but is used as financial leverage to adjust the balance sheet and maintain the operation of the preferred stock payment system.

Conclusion

Investors must now anticipate the risks of Michael Saylor's capital operation model: each operation benefits one side of the capital structure while harming the other side.

This is also the key signal released in the announcement on July 6: Strategy is not without space to sell Bitcoin; its sellable scale far exceeds the numbers visible to the market. Only when investors mistakenly believe that $1.25 billion is the total sales limit will this number represent the company's priority to preserve its Bitcoin holdings; do not fall into this cognitive misunderstanding.

Strategy has now become a financial institution that requires the market to interpret its rules word by word. Every professional expression is crucial: build, replenish, issue, repurchase, stabilize. Investors should dissect every term just like Federal Reserve observers dissect policy documents, determining the potential scale of future Bitcoin sales.

This monetization plan gives Strategy operational flexibility, but the underlying internal contradictions have never disappeared. It is no longer a simple, clear leveraged Bitcoin investment target; betting on this company is essentially a gamble on its ability to manage capital actively — betting that the company can continue to sell, replenish, issue shares, repurchase, and stabilize various capital instruments without a failure in one link that causes everything to spiral out of control.

For my part, I would not participate in this bet.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。