Written by: Rita

Trend Guide

On July 7, Samsung Electronics announced its preliminary results for 2Q26: operating profit of 89.4 trillion won (approximately 58.4 billion USD), an increase of 1810% year-on-year and 57% quarter-on-quarter, with revenue of 171 trillion won, a year-on-year increase of 129%, both exceeding market expectations. This figure surpasses Nvidia's last quarter revenue of 53.5 billion USD, making Samsung the company with the highest quarterly operating profit in the world.

Morgan Stanley provided an immediate interpretation: in line with expectations, but profit momentum remains strong. The memory business profit margin exceeds 70%, and the overall operating profit margin of the company reaches an impressive 52%, astonishing even after deducting about 10% for employee bonus provisions. Morgan Stanley maintains an overweight rating on Samsung, its preferred target, with a target price of 381,000 won, currently standing at 318,000 won, implying about 20% upside potential.

Memory is the only protagonist, with profit margins exceeding 70%

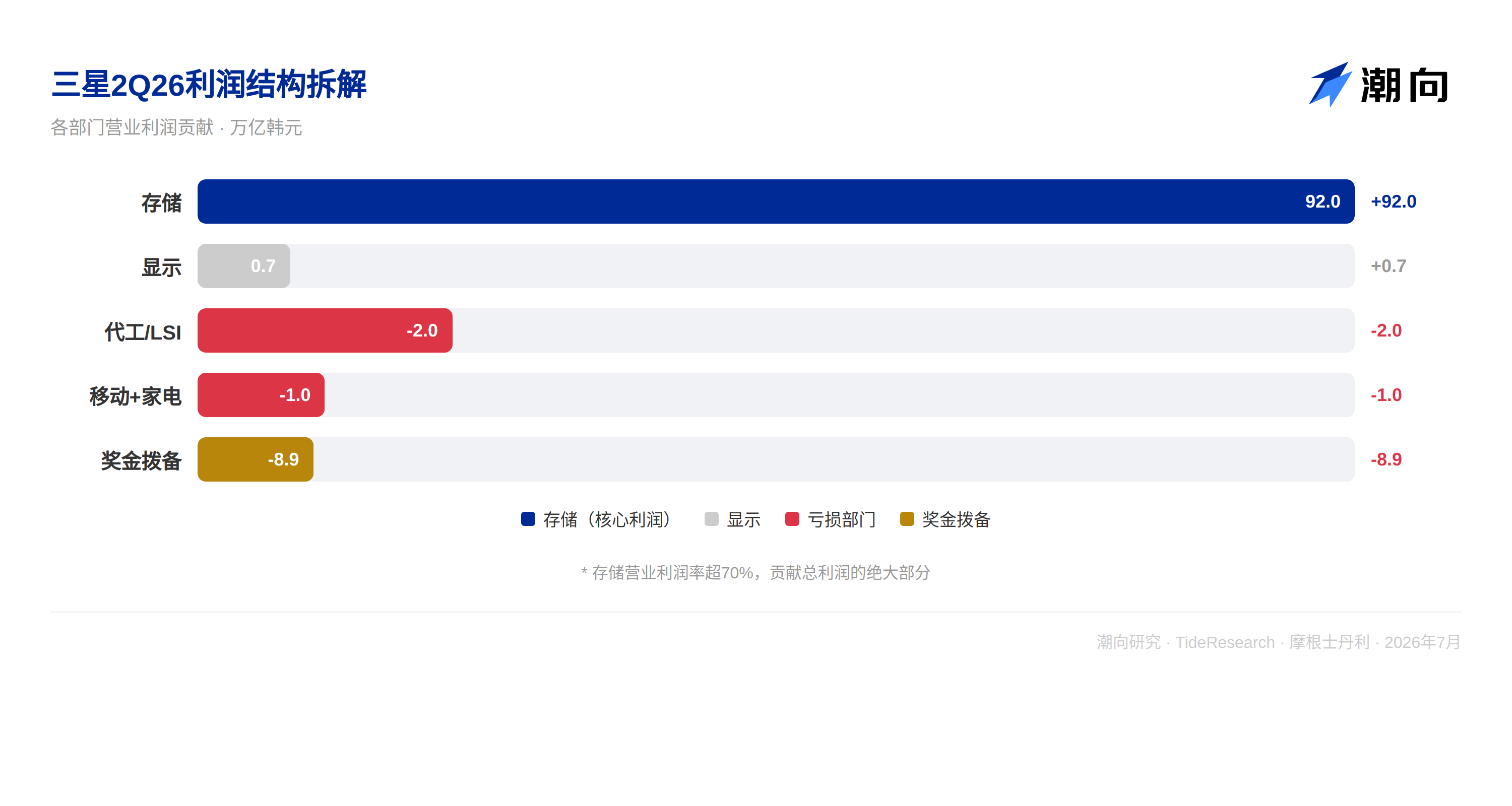

In Samsung's profit structure for 2Q26, memory is the absolute mainstay. Morgan Stanley estimates that the operating profit from the memory division is close to 92 trillion won, accounting for the vast majority of the company's total profit. The average price of DRAM has increased by about 56% quarter-on-quarter, combined with the simultaneous increase in NAND prices, resulting in an operating profit margin for the storage business exceeding 70%.

The foundry and logic chip (LSI) divisions’ losses narrowed to about 2 trillion won, while the mobile and home appliance divisions incurred a total loss of about 1 trillion won, and the display division contributed approximately 700 billion won in profit. Besides memory, other business lines overall continue to be a drag.

The profit structure of Samsung Electronics has completely turned into a “memory dominance.” The 92 trillion won profit from memory corresponds to the total profit of 89.4 trillion won, implying that all other businesses combined are at a loss. The foundry is losing, the mobile segment is losing, and the home appliances are losing, while only the display division contributed a meager profit of about 700 billion won. Samsung has essentially transformed into a storage company, with other operations just holding it back.

Bonus provisions eat into some profits, but cannot mask the real profit momentum

There is a detail in the financial data that may be easily overlooked. In May of this year, Samsung reached an agreement with employees to link performance bonuses to operating profit, allocating 10.5% of the semiconductor division's annual operating profit for special bonuses. Morgan Stanley estimates this provision accounts for about 10% of the 2Q operating profit, approximately 8.9 trillion won.

Without this one-time provision, Samsung's operating profit would approach 100 trillion won. The provision has lowered the reported figures, but the actual profit momentum is stronger than the statements indicate. Morgan Stanley explicitly pointed out in their report that the operating profit margin is as high as 52% (with the memory business exceeding 70%), a figure achieved after accounting for the substantial bonus provisions. In other words, Samsung's true profit capability is even more vigorous than what the reports suggest.

The employee bonus provision is an important variable in Samsung's profit structure. The higher the annual operating profit in 2026, the larger the absolute amount of the bonus provision will be, but the ratio of provision is fixed at 10.5%. This means that as profits continue to grow, the provision amount will increase proportionally, but it will not change the direction of profit expansion.

Morgan Stanley's full-year forecast: 412 trillion won, storage growth exceeding 1100%

Morgan Stanley's core judgment of Samsung is that the profit recovery cycle is far from over, and the market may not have fully accounted for the entire year's profit scale in 2026.

Morgan Stanley expects Samsung's full-year operating profit in 2026 to reach 412 trillion won, with storage business profits increasing by over 1100%. If this number is realized, it would mean Samsung's profit in 2026 would be more than 50 times that of 2025. In 2025, Samsung's total operating profit was only about 7.7 trillion won, whereas for 2Q26 alone, it has already reached 89.4 trillion.

Morgan Stanley believes this is not impossible, as the current storage cycle is unlike any before. The demand for HBM and DDR5 from AI data centers is continuously squeezing the supply of traditional storage, and the expansion of supply capacity will take at least 2 to 3 years to release significantly. The duration of the supply-demand mismatch far exceeds market expectations.

There are two key variables to monitor. The first is long-term supply agreements (LTA). Storage manufacturers are signing more and more long-term agreements with customers, and Morgan Stanley believes this will significantly enhance the predictability and stability of Samsung's profits, reducing market uncertainty pricing due to cyclical fluctuations. If LTA becomes the industry norm, the valuation method of storage stocks may need to shift from cyclical stocks to growth stocks.

The second is the continued demand for advanced storage driven by AI computing. Samsung's technology nodes in DRAM and logic base levels are more advanced than competitors, and the advantage of "computing power-to-power ratio" is expanding. Against the backdrop of AI computing power consumption becoming an increasingly bottleneck, Samsung's advanced processing advantages may translate into sustained pricing power premiums.

Trends Perspective

Samsung's stock price has risen 165% this year, outperforming almost all peers, yet Morgan Stanley still calls for overweight. The core contradiction lies in the fact that the market is pricing Samsung as a “cyclical stock,” providing a valuation typical of the middle of the cycle, while Morgan Stanley believes the strength and sustainability of this storage cycle far exceed any previous instances.

Morgan Stanley used a very straightforward comparison: Samsung's current stock price corresponds to a PE ratio of only 6.6 times for 2026, and a PB ratio of 3.2 times. If we follow Morgan Stanley's forecast for a full-year 412 trillion won profit, the implied PE ratio is about 5.5 times. For a company with an operating profit margin exceeding 50% and an oligopolistic position in the AI storage field, this valuation is clearly not expensive.

The validation point will be the earnings conference call on July 30. The guidance provided by management for 3Q will be more important than the preliminary results themselves, as the market wants to know not only "how much was earned in the past," but also "how long can it continue to earn in the future." If the 3Q guidance continues to exceed expectations, Samsung's valuation may undergo a systemic reassessment.

Disclaimer

This article is a整理与解读 of a third-party brokerage research report (Morgan Stanley, July 7, 2026) by Trend Research. The ratings, target prices, profit forecasts, and related judgments quoted in the text represent the views of the brokerage analysts, only reflecting the position of their institutions, and do not represent the views of Trend Research, nor do they constitute any investment advice.

The market has risks; decisions should be independent. This article should not be used as the basis for buying or selling any securities.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。