tZERO claims 105 patents and six potential litigation targets, striking the first blow in the patent war of the tokenization industry against Securitize.

Written by: Sanqing, Foresight News

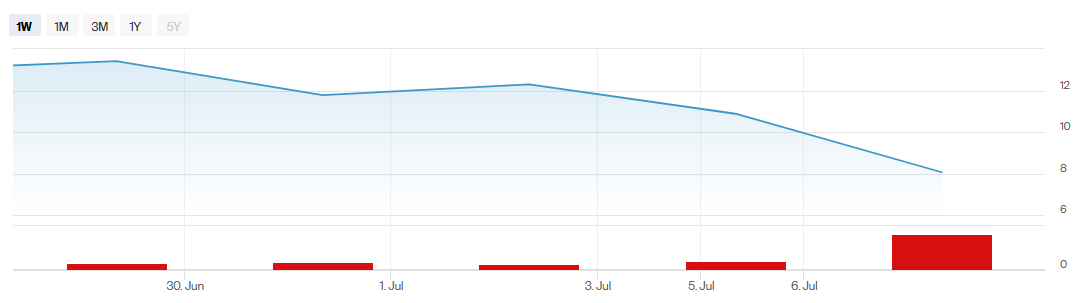

On July 2, Securitize (NYSE: SECZ) officially landed on the New York Stock Exchange through a SPAC merger completed with Cantor Equity Partners II. On the first trading day, it once rose, and the market viewed it as a landmark event for traditional capital market recognition of the tokenization industry. However, just a few trading days later, the script took a sharp turn. As of the close on July 7, SECZ reported $8.06, a single-day plunge of 25.92%, with an intraday low of $8.00, a drop of about 40% from its high in the first week of listing.

Image source: New York Stock Exchange

This is a company selected by BlackRock's tokenized money market fund BUIDL as a transfer agent, recognized in the capital market as a leading platform in the tokenization field, with a pre-merger estimated value of $1.25 billion. The contrast of the continuous decline after listing has led many investors to begin examining the gap between the "tokenization narrative" and the "secondary market reality".

SPAC mechanism exposes problems ahead of fundamentals

In recent years, cryptocurrency-related companies that went public through SPACs have almost all experienced similar valuation re-pricings during the trading period.

Twenty One Capital (XXI), also operated by Cantor Fitzgerald affiliates, dropped about 25% on the day it went public on December 9, 2025, through SPAC merger, closing at $11.42; it then continued to decline, with its stock price at one point falling below $6, losing over 80% from its peak of $49. ProCap Financial (BRR), a cryptocurrency fund company that completed a merger in the same period, had an issue price of $10, and its stock price now hovers around $2.4, a drop of about 76%.

Many market participants attribute this plunge to the SPAC structure itself rather than deteriorating company fundamentals.

According to CoinDesk, Arca's Jeff Dorman publicly stated that these fluctuations are more a result of the SPAC mechanism than deteriorating fundamentals. After SPAC listing, the investor structure undergoes a complete shift, from SPAC subscribers who prefer fixed returns, to true holders of stocks who focus on long-term fundamentals, and this turnover process itself creates severe volatility.

The market's confidence in the "tokenization" story itself has not collapsed; what has collapsed is the confidence in the SPAC pricing mechanism. Despite the drop in stock price, Securitize still tokenized its own stock worth $295 million on the first day of listing and deployed it to Solana and Avalanche.

The decline of Securitize is also compounded by the overall pressure on cryptocurrency concept stocks in the U.S. stock market. As of early July, Coinbase's and Circle's stock prices have dropped approximately 63% and 74% respectively from their historical highs set in July 2025, while the S&P 500 index has only retreated about 2% from its June peak. When the stocks of the entire sector fluctuate more easily than the underlying assets, it is challenging for a newly listed tokenization platform to stand out.

Patent litigation tears open rifts in the industry

On June 15, tokenization infrastructure company tZERO sent a "cease and desist" letter to Securitize, accusing its DS Protocol and Vault Registrar core products of infringing on patents held by tZERO, specifically involving U.S. Patent 11,216,802 (self-executing smart contract rules for security tokens) and 11,394,560 (crypto integration platform).

tZERO demanded that Securitize cease the commercialization of related products by June 18, or it would seek injunctive relief and monetary damages.

Securitize took the initiative and filed a "declaratory judgment action" (case number 1:26-cv-00722, Securitize, Inc. v. tZERO Group, Inc. et al.) in the U.S. District Court for the District of Delaware on June 22, requesting the court to confirm that its products do not infringe on tZERO's patents and labeling the accusations as "baseless" and "lacking substantive content," claiming they "violate the spirit of fair competition in the industry."

The case is currently in its early stages, assigned to Judge Gregory B. Williams, with no substantive answers, counterclaims, motions to dismiss, or settlement news yet. This means there are various possible directions for the case, including out-of-court settlements, partial dismissals, or even tZERO retracting its accusations.

The weight of this lawsuit far exceeds that of a normal business dispute.

tZERO's patent claims were not made spontaneously. Founded in 2014, this company, which evolved from Overstock.com (a well-established online retailer in the U.S, whose founder Patrick Byrne was an early advocate of blockchain), began a strategic review of its intellectual property portfolio after completing a management change at the end of 2025.

According to tZERO's announcement on June 15 regarding the enforcement progress of its intellectual property portfolio, it holds 105 patents covering 23 patent families, with a business scope spanning compliance securities token systems, crypto asset integration, KYC certification processes, and other core aspects of tokenization infrastructure.

More critically, tZERO has made it clear that its patent review has identified "at least six" other market participants with potential infringement behaviors, covering various fields such as compliant RWA platforms, institutional infrastructure, prime brokers, and decentralized exchanges, with plans to issue infringement warning letters to more companies after completing its analysis.

As of July 8, the case remains in its early stages, with both parties yet to submit substantive answers, counterclaims, or settlement documents.

In fact, Securitize is facing patent pressure not only from tZERO. At the same time, Liquid Rarity Exchange has already filed an independent lawsuit against Securitize regarding two other patents, seeking compensation and requesting injunctive relief.

In other words, Securitize may just be the first, but not the only one. According to rwa.xyz data, the RWA market size has accelerated from about $22 billion at the beginning of the year to over $33 billion, with the industry moving from "proof of concept" to the "actual deployment" stage.

This is the background in which tZERO chose to convert its long-dormant patent portfolio into a commercial chip; as the patent barriers of the tokenization industry begin to be genuinely asserted, almost all platforms claiming to "hold core technologies" may be drawn into similar disputes. This is more worthy of long-term attention than a stock price pullback.

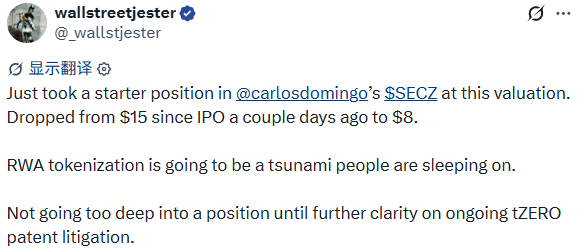

As X user wallstreetjester stated, he "just built a position" in SECZ but clearly expressed that he "will not deepen the position until there is clearer progress in the litigation." This represents the true mentality of some potential buyers.

Primary market trusts institutions, secondary market trusts liquidity

The shareholder lineup of Securitize is quite luxurious. BlackRock's BUIDL fund chose it as a transfer agent, and during the PIPE financing phase, institutional investors such as Borderless Capital and Hanwha Investment were also introduced, with the SPAC transaction itself initiated by Cantor Fitzgerald affiliates.

This narrative of "traditional financial institutions co-sponsoring" is highly persuasive during the primary market financing phase and is also an important support for Securitize's pre-merger estimated value reaching $1.25 billion.

However, the secondary market does not recognize sponsorship, only liquidity. The market still buys the "tokenization" story, but what has really cooled is the short-term pricing of this specific stock, Securitize.

The name BlackRock can prompt primary market investors to be willing to buy into the valuation story, but it does not translate to secondary market investors willing to continue holding while the patent disputes are unresolved and SPAC turnover pressure persists. Trust is a static brand asset, while liquidity is a dynamic result of competitive games; this plunge just proves that there is no necessary conversion relationship between the two.

Securitize's stock price will eventually stabilize or rebound as the investor structure turnover completes; this is a phase pain that almost all SPAC-listed companies must go through. However, the patent war provoked by tZERO is something that participants in the tokenization industry should be wary of.

tZERO holds 105 patents and has identified at least six potential infringement targets, which means that the next round of competition in the tokenization industry may no longer only rely on compliance licenses, institutional relationships, or trading volume.

For those platforms still relying on "we were the first to achieve a certain technical solution" to tell their valuation stories, a cease and desist letter could suddenly halt that narrative.

The drop of Securitize represents a loss of short-term valuation; meanwhile, tZERO's lawsuit may unveil a patent war that the entire tokenization industry is not yet prepared to face.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。