Author: Nancy, PANews

A little over a month ago, Strategy attempted to sell 32 BTC for the first time. Although the scale was insignificant, both Bitcoin and MSTR suffered significant losses. Now, Strategy has again stepped in, selling 3588 BTC at a loss of over $55 million, a dramatic increase in selling scale, but the market response has been much more mild.

In fact, faced with an annual dividend bill of over $1.7 billion and a stalled financing wheel, this largest global Bitcoin entity is bidding farewell to the era of "buying only" and shifting towards a defensive stage that prioritizes cash flow and liquidity.

Strategy cuts losses and sells coins, hoarding mode faces interest pressure

On July 5, Michael Saylor again published the Bitcoin holdings Tracker. As per usual practice, Strategy typically announces new Bitcoin accumulation plans the day after relevant information is released.

However, this time, just as Bitcoin prices began to recover, the market was greeted not with "continue buying," but with Strategy's first major sale of Bitcoin.

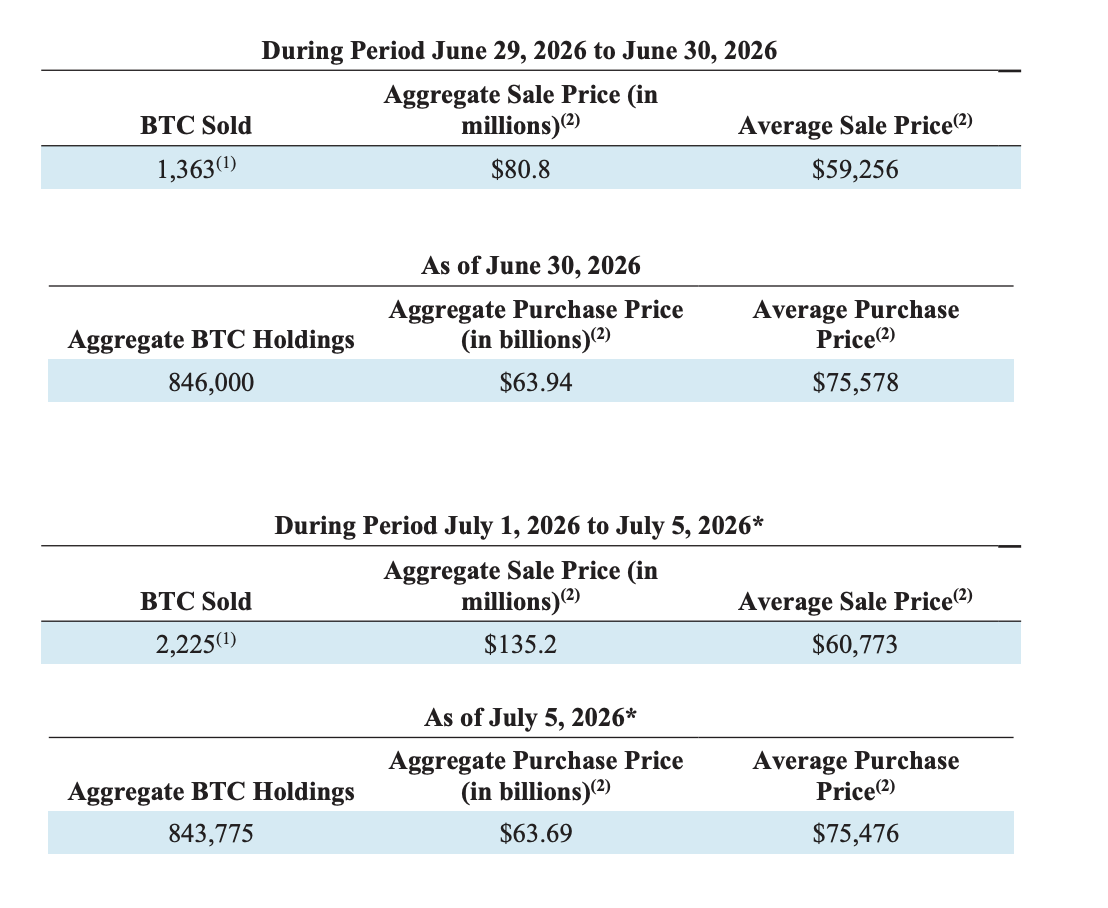

According to the latest disclosure, Strategy sold a total of 3588 BTC between June 29 and July 5, cashing out approximately $216 million. Of these, 1363 BTC were sold at an average price of about $59,256 on June 29-30 (worth about $80.8 million), and 2225 BTC were sold at an average price of about $60,773 from July 1-5 (worth about $135.2 million).

The funds raised from this sale are primarily used to pay preferred stock dividends, including quarterly dividends for STRF, STRE, STRK, and STRD, as well as the full month dividend for STRC in June, while further bolstering dollar reserves. Currently, Strategy's dollar reserves can cover approximately 17.4 months of dividend payments.

After the news was announced, Bitcoin briefly fell, and Strategy's stock price also retreated during the session, but both later rebounded and recovered their losses.

In fact, this is not the first time Strategy has sold coins. On June 1, Strategy sold 32 BTC, breaking the long-standing "buy only" practice for the first time since 2022. At that time, it directly triggered a Bitcoin plunge, MSTR stock plummeted, and STRC preferred stock also accelerated below par, sending the market into panic.

Compared to the initial symbolic test, this sale expanded to 3588 BTC, more than a hundred times larger than the last instance, and is a genuine loss sale. Based on Strategy's average holding cost of about $75,651, this transaction realized a loss of approximately $55.45 million, while the 32 BTC sold in June had a transaction price still slightly higher than the holding cost.

The fundamental reason driving this sudden increase in the sale scale is the ongoing rising pressure of dividend payments.

Since its launch, Strategy has constantly increased the STRC dividend rate, reflecting changes in the market's risk perception and signaling that the company's fixed cash expenditure pressure is growing day by day. Not long ago, Strategy also changed STRC to a semi-monthly dividend mechanism and increased the dividend rate to 12%.

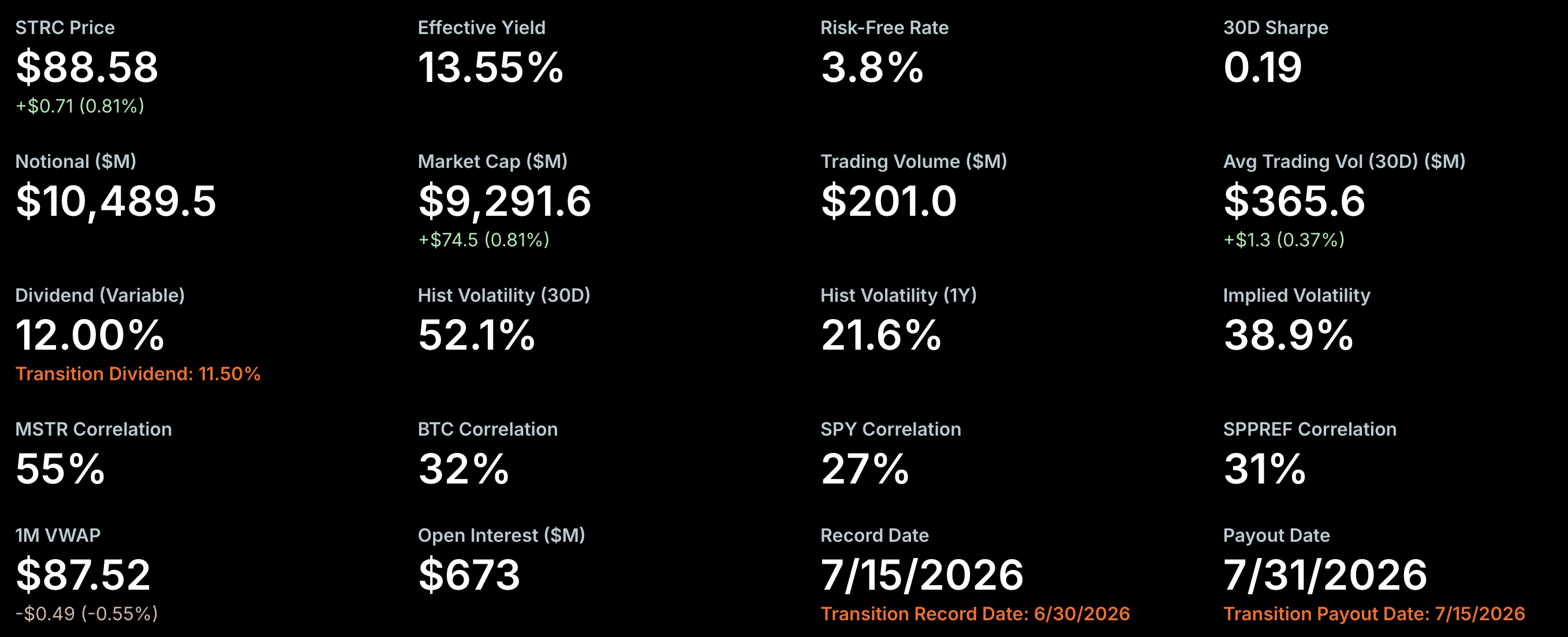

Based on the current total nominal amount of approximately $10.49 billion, STRC alone requires about $1.258 billion in cash dividends each year, coupled with other preferred stocks, Strategy's annual dividend expenditure has reached approximately $1.763 billion. Currently, Strategy's $2.55 billion dollar reserve, under the assumption of not relying on external financing and maintaining neutral cash flow from traditional software operations, can only cover about 24.3 months of STRC dividend payments.

From a capital allocation perspective, the sale of part of the Bitcoin seems more like Strategy’s decision for capital optimization, which is more certain at this stage. The current trading price of STRC is approximately $88.5. Although it has recovered significantly from the lows, there is still some room to reach the $100 target.

According to Wall Street investment bank Cantor, Strategy's current top priority is to push STRC back to the $100 par value, which is the core of restarting the Bitcoin acquisition engine and stabilizing the overall capital structure. Strategy has also made it clear that its goal is to keep the long-term trading price of STRC between $99 and $100 and will support this through a variable dividend rate, continuously increasing dollar reserves, raising Bitcoin credit ratings, removing convertible bonds, implementing stock buybacks, and upgrading product functions.

For Strategy, before the capital market fully resumes financing capabilities, it is better to fulfill dividend commitments and replenish dollar reserves rather than continue to increase Bitcoin holdings, to enhance market confidence in preferred stocks and the overall capital structure. Grayscale has also pointed out that Strategy's action of selling Bitcoin should be able to restore market confidence in its financing structure, while helping Bitcoin find a more sustainable price bottom and lowering Bitcoin's tail risks.

Surface losses of $10 billion, Strategy begins to enter a defensive mode

Although the scale of this sale is not small, the 3588 BTC only account for about 0.42% of Strategy's total holdings of 843,775 BTC and do not shake its core strategy of holding Bitcoin for the long term. To date, Strategy still holds Bitcoin valued at over $53 billion, remaining the largest Bitcoin holder among global corporations.

However, the continued slump in Bitcoin prices has put Strategy under greater operational and financing pressure. Based on an average holding cost of about $75,476, Strategy currently has an unrealized loss of around $11.34 billion, with the loss percentage nearing 18%.

More importantly, the market's valuation logic for Strategy is undergoing a change.

In the past, investors were willing to pay a high premium for Strategy's "sustained financing and continuous buying Bitcoin" growth story, which enabled it to continually raise funds through issuing common stock, forming a capital flywheel. However, as Bitcoin prices plummet, MSTR’s stock price premium narrows, and the market's expectation of "never selling Bitcoin" is shattered, investors are beginning to reassess Strategy's business model, and its capital flywheel has hit the brakes.

To cope with this shift, Strategy recently officially announced a digital credit capital framework, aiming to enhance digital credit securities, improve liquidity, and support long-term shareholder value while maintaining its long-position strategy.

According to this framework, Strategy will establish a dedicated dollar reserve to pay dividends on preferred stocks and debt interest; it will also set up a $2 billion buyback authorization, with $1 billion allocated for preferred stock buybacks and $1 billion for Class A common stock buybacks. Additionally, the board has approved a Bitcoin monetization plan of up to $1.25 billion, intended to replenish dollar reserves, pay dividends and interest, or fund buybacks.

This means Strategy is moving from a model that relied on continuous financing for expansion to a proactive capital management model that emphasizes liquidity management, capital structure optimization, and stable cash flow. While retaining its core Bitcoin position, Strategy hopes to create a larger safety buffer for future market fluctuations by establishing more adequate cash reserves.

However, there are differences of opinion in the market regarding this strategy. Galaxy's head of research, Alex Thorn, pointed out thatthis capital strategy indeed alleviates concerns about Strategy's liquidity and preferred stock payment pressure in the short term, but is more about "buying time" rather than truly solving its structural issues. Strategy still bears substantial obligations for preferred stock payments, and the market is more concerned about whether it possesses sufficient dollar liquidity to continuously meet payment obligations without harming the interests of common stock shareholders, preferred stock shareholders, and Bitcoin holders. The most controversial aspect is the Bitcoin monetization plan, which means Strategy may sell part of its Bitcoin in the future based on funding needs, and its identity and MSTR premium rests on its narrative as a long-term Bitcoin exposure tool; selling Bitcoin would undermine this story.

Alex Thorn suggested thatStrategy should explore how to create revenue from its Bitcoin holdings by conservatively lending out a small amount of isolated Bitcoin for interest, or generating volatility income through options strategies, rather than selling directly.

Based on the current sale scale, Strategy may continue to sell some Bitcoin depending on the market environment. Investors need to pay close attention to the scale, frequency, and triggering conditions of Strategy's future coin sales. If selling coins becomes the norm or even continues to increase, market confidence in its long-term holding strategy and capital operation model may be tested again. More importantly, the changes in Strategy may just be the beginning. If Bitcoin prices remain under pressure and financing costs rise, and more Bitcoin DAT companies start to follow Strategy's lead by selling Bitcoin to relieve liquidity pressure, this could further suppress coin prices and weaken confidence in the DAT model.

The faith in Strategy's coin hoarding has been shattered, representing not only a temporary bloodstop but also a real test of this high-leverage financial experiment during the downturn phase. Whether a business model that relies on continuous capital market transfusions can smoothly traverse a bear market cycle, the answer may just be beginning to reveal itself.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。