Author:Eric SJ

Many people say that Web3 has no business model.

This statement is only half correct.

Web3 indeed has many projects that essentially remain in the “token subsidy + narrative financing + liquidity exit” loop.

However, if you shift your perspective away from FDV, airdrops, listings, and narratives to see who is genuinely paying, where the money ultimately flows, and how protocols generate revenue, you will find:

Web3 does not lack business models; rather, many business models do not have a strong binding relationship with token prices.

This is also why they are often overlooked by the market. The so-called business model essentially answers four questions:

Who pays?

Why are they willing to pay?

How does it eventually turn into revenue and profit?

Can this model sustain long-term?

Based on this standard, the business models in Web3 that have already been validated by the market can roughly be divided into five categories:

Transaction fees

Stablecoin reserve earnings

Funding spreads

Block space selling

Protocol-level service fees

This article will briefly discuss these five models and how they make money.

Five Proven Cash Flows

Generally, a complete business model can be explained very simply, so the following examples of each model will not take much space, because their models are clear enough.

First: Transaction Fees—Hyperliquid

Let's start with transaction fees, which is the earliest validated business model in the industry. From CEX, DEX to cross-chain bridges, the business model is based on this framework; the difference is just in the medium through which it is realized.

The advantage of this type of business model is that revenue is direct and cash flow is clear; the downside is that it is highly cyclical; revenues explode in bull markets and shrink rapidly in bear markets.

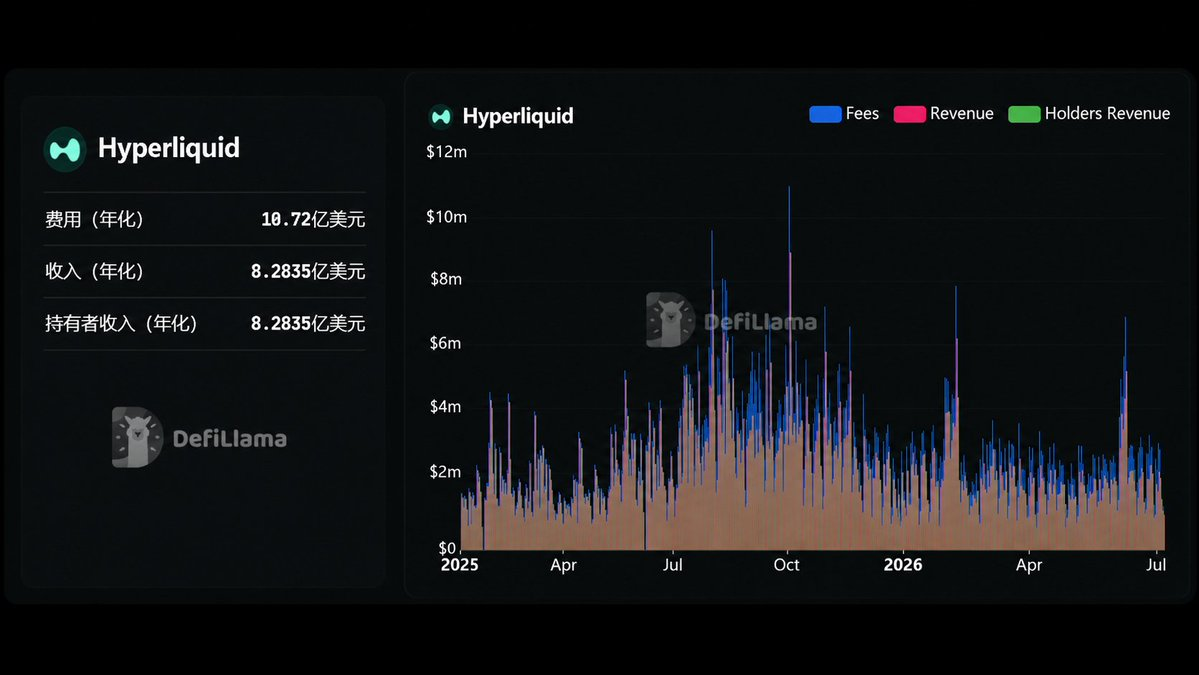

I believe Hyperliquid @HyperliquidX is the best example of the transaction fee model, bar none.

The reason is simple: First, it does not rely on complex narratives for fees; the structure is clear and straightforward, and most importantly, it maintains sufficient transparency.

You can clearly see its revenue structure through the on-chain interface. DeFiLlama's fee metrics for Hyperliquid include contract trading fees and Builder fees (excluding spot), meaning that users initiating contracts, placing orders, consuming orders, market-making, and using Builder Code will incur fees at different levels.

As for where this fee flows, that is not the topic of this section, so it won't be elaborated on here, but some data needs to be shared to show how well it has created a closed loop:

Thus, its business model is very direct: the larger the transaction volume, the more transaction fees; the more transaction fees, the more revenue; the more revenue, the more repurchases.

However, the issues with the transaction fee model are also quite apparent: it is sensitive to market conditions; revenues will be attractive in bull markets, but will clearly contract in bear markets (see the change trend on the right of the image).

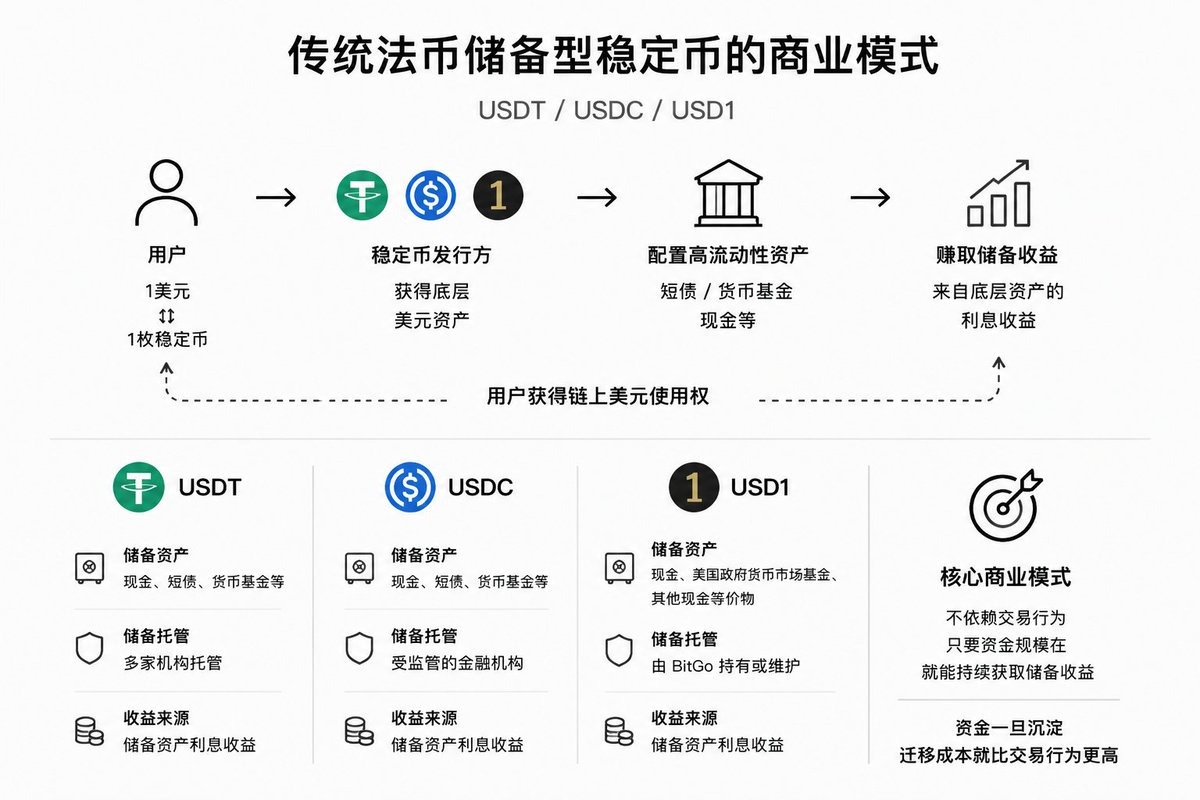

Second: Stablecoin Reserve Earnings—USDT/USDC/USD1

Stablecoins can be broken down into two dimensions: one type is traditional fiat-backed stablecoins, represented by USDT and USDC; the other is like Ethena, which strictly speaking does not count as a “reserve earnings” type, as it relies on funding metrics and basis in the crypto market, which is out of the scope of this section.

The underlying business models of USDT and USDC are essentially similar to “on-chain money market funds.”

Users exchange 1 dollar for 1 stablecoin, and the issuer acquires the underlying dollar assets, then allocates short-term debt, money market funds, cash, and other high liquidity assets to earn reserve earnings.

USD1 follows a similar logic but with subtle differences. According to official documentation from World Liberty Financial, USD1 is backed by cash, U.S. government money market funds, and other cash equivalents.

What users receive is the on-chain dollar usage right, and what the issuer receives is the residual income rights of the underlying dollar assets.

This is also why the business model for stablecoin issuers is very robust.

It doesn’t necessarily require users to trade every day; as long as the stablecoin scale remains, it can continuously earn reserve-side income. The core of this business model is not “is there anyone trading,” but “is there enough money willing to stay.”

Once funds settle in, the migration cost is higher than the transaction behavior.

Third: Funding Spreads—Ethena/AAVE

Here are two cases to highlight, one being the aforementioned Ethena @ethena

Its main product is also a stablecoin, but unlike reserve earnings, its stablecoin's underlying source is rate revenue.

This means it earns contract fees and basis revenue by employing a neutral hedging strategy on assets like BTC and ETH (there's also a small portion of reserve earnings from the staking rewards of Ether).

The other case—AAVE @aave—is representative of the funding spread model.

Traditional banks make money simply by: taking in funds at low cost and lending them out at a high price, earning the spread in between;

Aave does something similar to banks, but it does not collect deposits and make loans itself; instead, it organizes depositors, borrowers, collateral, interest rate models, and liquidation mechanisms using smart contracts.

Users deposit assets into Aave's liquidity pool, borrowers use collateral to borrow assets and pay interest. The more money borrowed from a liquidity pool, the higher the utilization rate, thus increasing the borrowing interest rate; if there is much idle money in the liquidity pool with no one borrowing, the rate decreases.

This mechanism essentially provides automatic pricing for on-chain funds.

The protocol's income from Aave comes from taking a percentage of the interest paid by borrowers. In other words, most of the interest paid by borrowers will be distributed to depositors, while the remaining portion enters the protocol treasury through reserve factors, becoming Aave's protocol income.

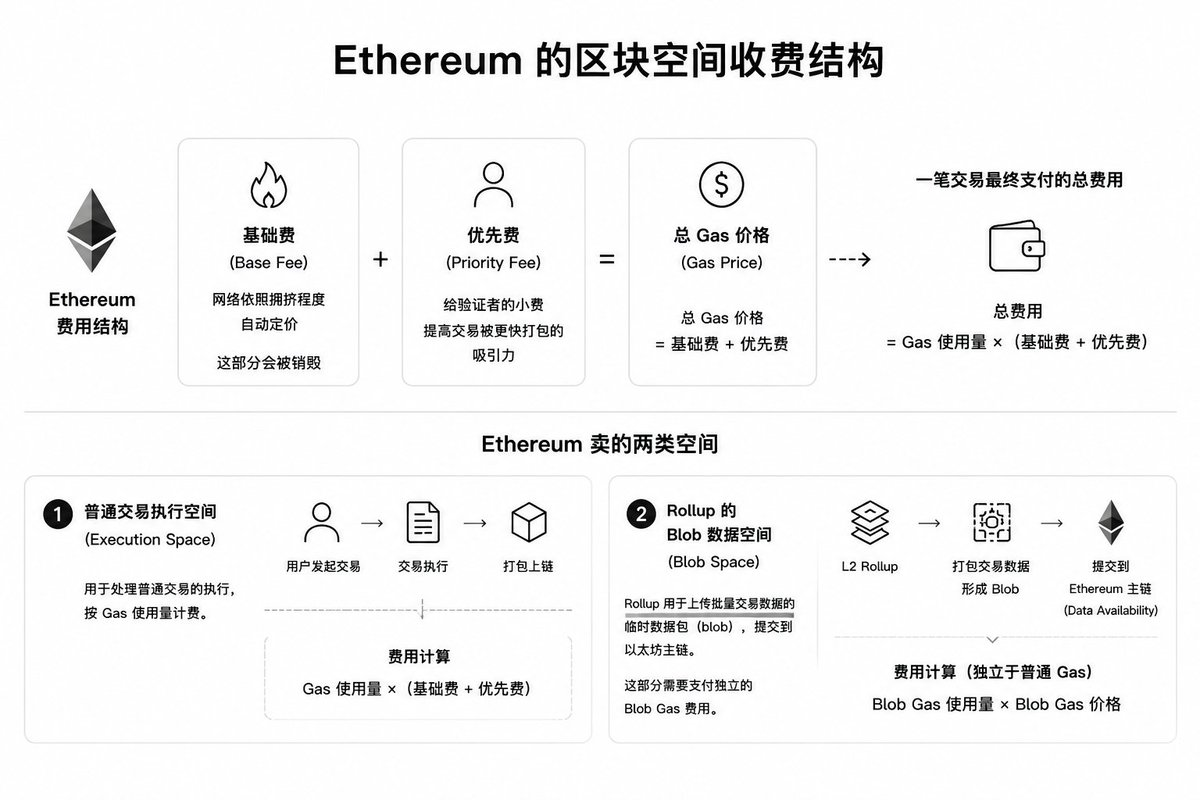

Fourth: Selling Block Space—Ethereum $ETH

What public chains really sell is not TPS but block space.

Ethereum's block space fee structure consists of two parts: base fee + priority fee, where the former is automatically priced according to network congestion, and this part will be burned; the latter is a tip you give to validators to make it more attractive for the transaction to be packed faster.

Therefore, its fee structure is: total Gas price = base fee + priority fee

And the total fee paid for a transaction = Gas used × (base fee + priority fee)

Apart from this, since Ethereum has an entire ecosystem with many Layer 2s, it sells two types of space:

One type is the ordinary transaction execution space, as mentioned above;

The other type is the blob data space used by Rollup.

Blobs are temporary data packets used by Rollup to upload bulk transaction data; they contain data that is submitted to the Ethereum main chain during the packaging process, and this blob also needs to pay a blob gas, which is an independent pricing standard from ordinary transaction gas.

Technical analysis is beyond the scope of this chapter, so I won't expand on that; let me show a graphic summary:

Fifth: Infrastructure Service Fees

Besides transaction fees, stablecoin reserve earnings, funding spreads, and block space sales, I believe Web3 has a fifth type of business model that is becoming increasingly important:

Infrastructure service fees, many of which are in the form of subscriptions.

This is not a case of users being charged once per transaction, nor is it about stablecoin issuers using reserves to buy short-term debt; rather, it involves project teams, applications, and blockchains themselves consistently paying fees to use certain critical infrastructure.

As time passes and existing businesses mature, many protocols in Web3 are evolving from “token issuance projects” to “infrastructure providers.”

1. For example, deBridge @debridge acts as a cross-chain bridge; in addition to its own cross-chain trading services, it also supports establishing cross-chain bridges for various chains on the B-side, essentially selling cross-chain communication capabilities. Project teams need to use its protocol services to transmit messages, instructions, and liquidity across chains.

2. Again like OP Stack @Optimism that sells the capacity to open chains and share an ecological network. Superchain member chains enjoy OP Stack standardized construction and ecological synergy while returning a portion of their revenue to the Optimism collective.

3. Another example is Chainlink @chainlink that sells oracle and trusted data services. DeFi requires price information, derivatives need to be fed prices, and cross-chain requires message verification. These are not one-time needs but ongoing infrastructural demands.

Thus, this type of model can be understood as the Web3 version of SaaS, only instead of selling software accounts, it sells underlying capabilities like cross-chain, opening chains, oracles, automation, and data verification.

This kind of revenue may not be the most attractive in the short term but holds significant long-term commercial value. Once project teams integrate their businesses into these infrastructures, the migration costs become high.

In the future, I will consider discussing 1-3 of these models in more detail (depending on the feedback for this article).

Finally, a Brief Conclusion

To summarize in one sentence:

Web3 does not lack business models; rather, many business models do not directly reflect in token prices.

Each model listed one example for elaboration.

1. Transaction Fee—Hyperliquid @HyperliquidX

2. Stablecoin Reserve Earnings—USDT/USDC/USD1 @worldlibertyfi

3. Funding Spreads—Ethena/AAVE @ethena @aave

4. Selling Block Space—Ethereum

5. Protocol-level Service Fees—ChainLink/OP/deBridge @chainlink @Optimism @debridge

If we look at these five business models together, we will notice a distinct change:

Web3 is not just narratives; it is also showing increasingly clear cash flows.

The five models mentioned above will not cover all of Web3’s future, but at least currently, they are among the most easily validated and tracked real cash flow business models.

To avoid extending the length too much, this article discusses what these models rely on to make money, without elaborating where all this money flows.

The next article will address a more critical question: what factors will influence the quality of these business models?

Because truly good business models are not about making money in the short term, but about turning demand into cash flow in a long-term, stable, and explainable way.

Web3 is the same.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。