The largest channel, and DEX has become the backend.

Written by: HelloLydia¹³

The mountain gate has been removed, and there are more gatekeepers.

Robinhood Chain launches with great fanfare, and OUSD emerges dramatically, as both logos clash on the wall. In a moment, everyone speaks of permissionless, and all discussions center around decentralization.

The public's view is simple yet sharp: all platforms are squeezing towards the entrance, stocks, Perp, predictions, wealth management, all will be completed in one all-in-one app. Since it has come to this, it is certainly still the major channels of TradFi that are the strongest; it is wise to recognize this reality.

Given this, what significance does decentralized operation of DEXs hold?—This deserves a serious debate.

140+ partnering institutions of OUSD

Topic One: Decentralized pioneer dYdX and the rising star Perp DEX Lighter have both turned to the broker chain Robinhood Chain, indicating that the largest channels prevail, and DEX can only become a backend.

To respond to this judgment, we must distinguish between two concepts: one is "infrastructure" that is available for access, and the other is the "backend" that can be replaced.

The accessible infrastructure sells a kind of liquidity-rich scarcity. It represents a share of something, and anyone can access and use it, like Uniswap’s pool or TSMC’s chips.

The replaceable backend sells services from the infrastructure side. It must enter the domain of channel providers and redeploy itself according to others' game rules, often coupled with price reductions and promotions.

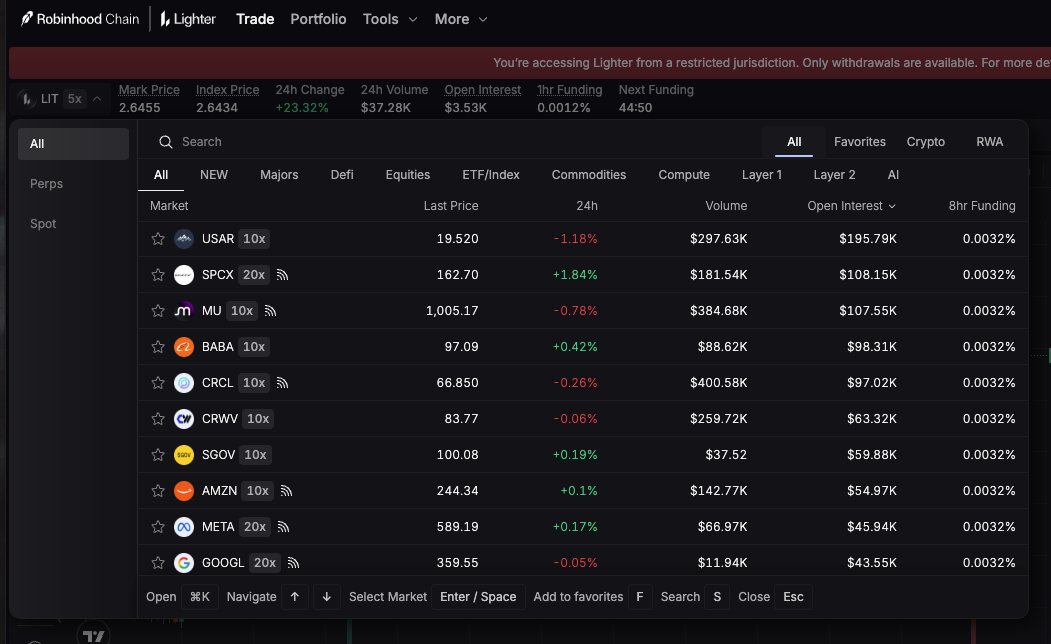

Lighter is more akin to the latter this time. It has deployed a USDG-denominated instance on Robinhood Chain separately, while the main Lighter site uses USDC. The valuation assets are different, and the order book is separated, essentially creating two independent markets. The instance on Robinhood Chain needs to bootstrap liquidity itself.

The Lighter instance on Robinhood Chain mainly features RWA assets, with liquidity separate from the main site

So what does the "scarcity" of DEX refer to? We can say that TSMC's moat is its chip technology, but it is difficult to assert that the moat of DEX is its technological level. In today's world, where speed and fees have been pushed to extremes, the only liquidity that can stand out for DEX to become "infrastructure" is the liquidity that others lack but it possesses, or that it possesses better liquidity than others.

Topic Two: Liquidity is certainly important, but decentralization cannot provide the best liquidity and trading experience; only single-chain can achieve that. Look at dYdX, isn’t it starting over? This shows that decentralization is merely an excuse for the losers.

"An excuse for losers," is not the case. On the contrary, decentralization is the favorite cloak worn by the successful ones in TradFi; Robinhood Chain openly states it aims to create Open Finance, emphasizing "decentralization," "AI-native," and RWA.

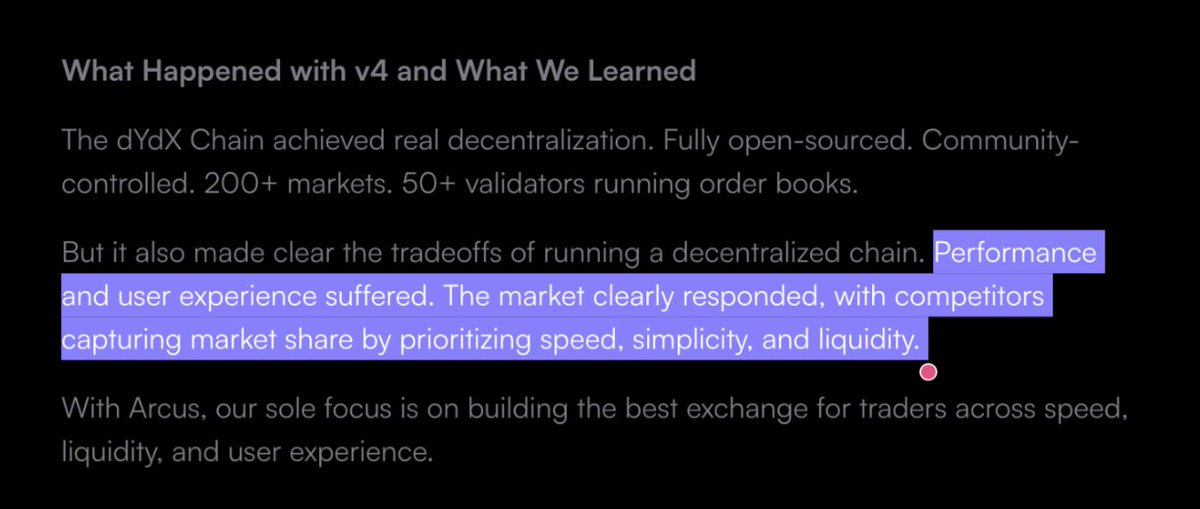

When we discuss decentralization, it is actually a broad spectrum. So far, what can be substantiated is the failure of decentralization in trading systems—i.e., trying to decentralize each layer from matching to settlement on a chain. dYdX Chain took a radical approach down this road, implementing "completely decentralized end-to-end," with all three major components (protocol, indexer, frontend) fully open-source, including the order book and matching engine handed over to validators. But the outcome was a cumbersome system that could not compete with the flexibility and efficiency of rivals.

dYdX founder Antonio wrote a blog reflecting on the past extreme decentralization path for arcus

After dYdX, Hyperliquid and Aster also launched their public chains, but the new generation of Perp DEX chains emphasizes "high performance" more. People seem to increasingly realize that a trading product must be easy to use; one cannot expect users to endure a subpar experience simply because the ideology is correct.

Besides decentralizing trading systems, there is actually a second line: decentralization in decision-making, which specifically relates to what markets are listed and the priority of products regarding Perp DEX. We see that this trend has not diminished but rather become clearer in this cycle.

The clearest evidence comes from TradFi. Robinhood has a license, compliance team, and 27 million users, yet it still needs a chain and an eye-catching slogan for Open Finance. OUSD encompasses more than 140 companies, claiming to be an "open standard" to differentiate itself from singular issuers like USDT and USDC. In this way, what TradFi giants want to express is merely that something mutually agreed upon and collectively decided holds more weight than something issued by a single company.

Thus, separating these two lines allows us to boldly conclude: decentralization in trading systems has basically been refuted at this stage, but we have not seen any company or project yielding ground on decision-making decentralization. Hyperliquid's HIP-3, Aster's AOS-1 and AOS-2, and even the players most qualified to continue with centralization are moving in this direction.

Topic Three: Decentralized decision-making sounds ideal, it’s akin to Hayek's theory of knowledge dispersion; Perp DEX can just learn from Uniswap, no entry barrier, anyone can deploy a market.

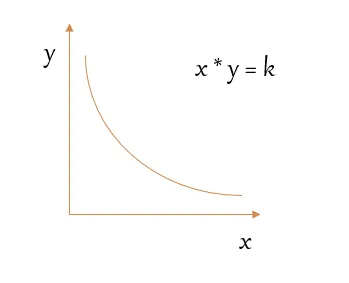

Unfortunately, Perp DEX cannot truly learn from Uniswap. As long as there are two (or more) assets in a spot pool and a formula, pricing can begin. The early charm of Uniswap came precisely from this proud independence of not relying on anyone.

AMM foundational formula

However, contracts must rely on external price feeds, need counterparties, and someone must bear the bad debt under extreme market conditions. Each new market added means an entire set of risks and settlement responsibilities. The entry barrier here primarily exists to clarify the attribution of responsibility. If the gates are removed, who will back a market without reason?

@ventuals made a pre-IPO perpetual contract on Hyperliquid's HIP-3, previously worked with OpenAI and Anthropic, with a trading volume exceeding 650 million dollars. Due to the structure of HIP-3 being self-deployed and risks self-borne, it meant that eventual would not truly monopolize liquidity while having to bear real operating costs, ultimately leading to shutdown (team members later joined Phantom). HIP-3 continued to concentrate towards TradeXYZ, presenting a winner-takes-all situation. This leads to an interesting outcome: the entrance is permissionless, but the exit may be centralized.

Promises of decentralization and equal opportunity are common misconceptions about permissionless and decentralized concepts. Permissionless implies that one no longer needs to nervously apply to a center, but does not mean everyone has the capability to bear the same risks.

A DEX can clarify the rules from day one: who can propose, who can vote, who bears the responsibility. Aster's AOS-1 and AOS-2 are basically products of this idea, transforming the originally internal team decisions about listing into a set of public standards, with validators voting for the outcome one by one. New markets entering through this process share the same trading venue, pooling Aster's liquidity and infrastructure.

Returning to the initial discussion about channels, Aster has never denied their importance. It would not be surprising if one day it reaches out to larger TradFi entrances, or allows more people to build their trading markets based on Aster Code; the distribution and traffic are necessary tasks to undertake.

However, who can determine whether an asset qualifies for existence and how to present the decision-making process in a decentralized manner is the essence of DEX's permissionless foundational nature; mere "frontend" and "backend" cannot substitute for this.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。