Shenchao Guide: When one dollar is spent on a growth channel, what quality of users comes back? Stacy Muur, founder of Green Dots, answers this question in an entire article. Her judgment is that by 2026, distribution will become increasingly intolerant of false demand; for example, surface-level appealing numbers like impressions, clicks, installations, and wallet connections are becoming ineffective. The only measure of a channel is whether it can bring users who complete KYC, deposit real funds, transact repeatedly, and are willing to stick around. Paid advertising, PR, KOLs, display ads, and task airdrops—each channel is reassessed by her in terms of value. For teams developing financial products, this is a practical map shifting from vanity metrics to user quality.

Author: Stacy Muur

Translation:Shenchao TechFlow

Source: Green Dots Research

The distribution of Fintech and Web3 is shifting from cheap surface metrics to empirical user quality. By 2026, stronger teams will measure channels with these standards: verified users, accounts with funds, active wallets, repeated transactions, fee generation, retention.

At Green Dots Research, we always circle back to the same distribution question: What quality of users comes back when a Fintech or Web3 product spends one dollar on growth?

For many years, distribution has been treated as a matter of channel mix. Teams have tested paid advertising, KOLs, PR, tasks, airdrops, referral marketing, Discord events, community promotion—almost every growth mechanism you can think of has been tried.

The problem is that many teams measure the easiest metrics to inflate: impressions, clicks, installations, wallet connections, or task completions.

By 2026, this logic will no longer hold.

A stricter filter is not "Can this channel generate activity," but "Can these activities turn into trustworthy products, complete activation, retain users, and generate revenue."

This is even more critical for financial applications.

A Fintech product requires users to bind identities, transfer funds, hold balances, trade assets, bear risks, or trust a certain protocol. A Web3 product often requires users to connect wallets, deposit funds, bridge chains, sign transactions, or interact with smart contracts.

Therefore, a cheap installation or wallet connection means very little—users might never complete KYC, never deposit, never trade, and disappear after claiming rewards.

My judgment: 2026 will be a year of increasing impatience towards false demand in distribution.

Markets Are Shifting from "Quantity" to "Quality"

The distribution of Fintech and Web3 is shifting from quantity-based growth to quality-based growth.

The question is no longer: How many users can this channel bring?

The better question is: Of these users, how many will verify their identity, deposit funds, trade, stay, pay fees, refer others, or return on their own without spending more money?

The marketing budget also leaves less room for false efficiencies.

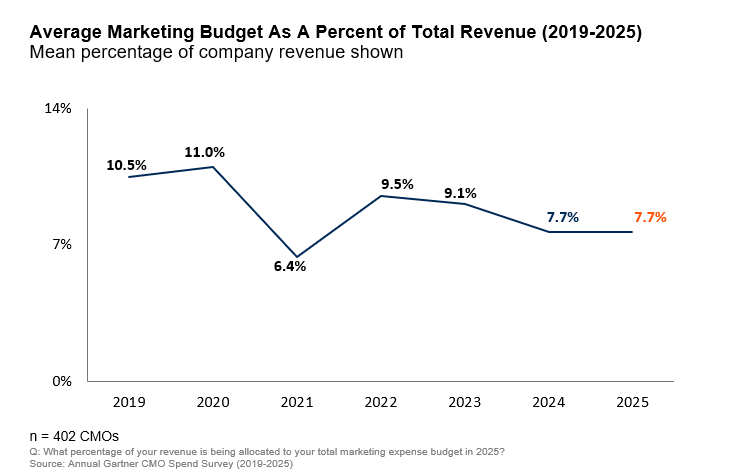

The Gartner 2025 CMO Spend Survey found that marketing budgets are flat at 7.7% of company revenue, while 59% of CMOs say the budget is insufficient to execute their strategies. Paid media still consumes 30.6% of marketing budgets, but media inflation means less is obtained for every dollar spent.

Caption: The share of marketing budgets relative to revenue peaked at 11.0% in 2020, fell to 6.4% in 2021, rose back to 9.5% in 2022, then receded to 7.7% in 2024 and 2025. Source: Gartner 2025 CMO Spend Survey

Meanwhile, digital advertising continues to expand.

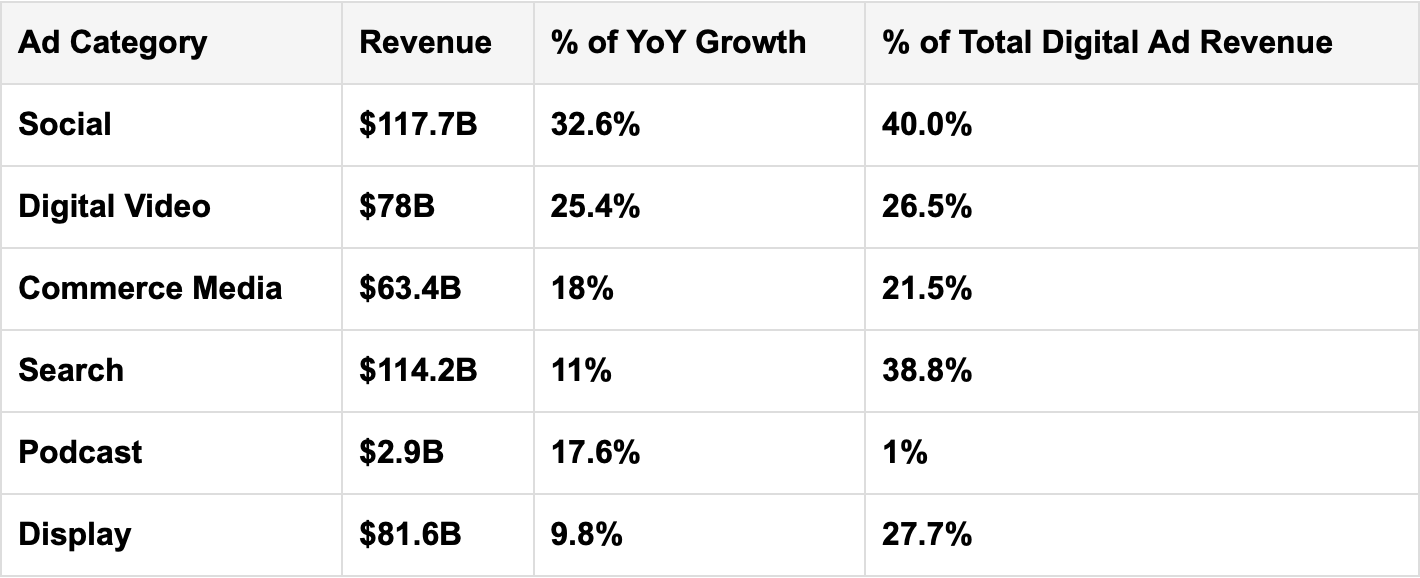

IAB and PwC report that in 2025, U.S. digital ad revenue reached $294.6 billion, a 13.9% year-on-year increase. Social media ads accounted for $117.7 billion, search $114.2 billion, display ads $81.6 billion, digital video $78 billion, and programmatic ads $162.4 billion.

Caption: U.S. digital ad revenue by category in 2025. Social media is highest at $117.7 billion, followed by search $114.2 billion, display $81.6 billion, digital video $78 billion, e-commerce media $63.4 billion, and podcasts $2.9 billion. Social media had the fastest year-on-year growth at 32.6%. Source: IAB / PwC

Therefore, this market is crowded on both ends.

More money flows into digital channels, but teams have less and less room to waste on low-quality users.

This is why the core distribution question of 2026 is straightforward: How many of the users acquired stay, transact, deposit, pay fees, refer others, or return on their own without spending more money?

Paid Advertising Remains Fundamental

Paid media is still the most controllable way of large-scale distribution. It allows teams to test messages, capture demand, and push traffic through a measurable funnel.

But in Fintech and Web3, paid customer acquisition needs to look much deeper than CPC, CPI, or CPL.

For instance, search ads still hold value because they capture clear intent.

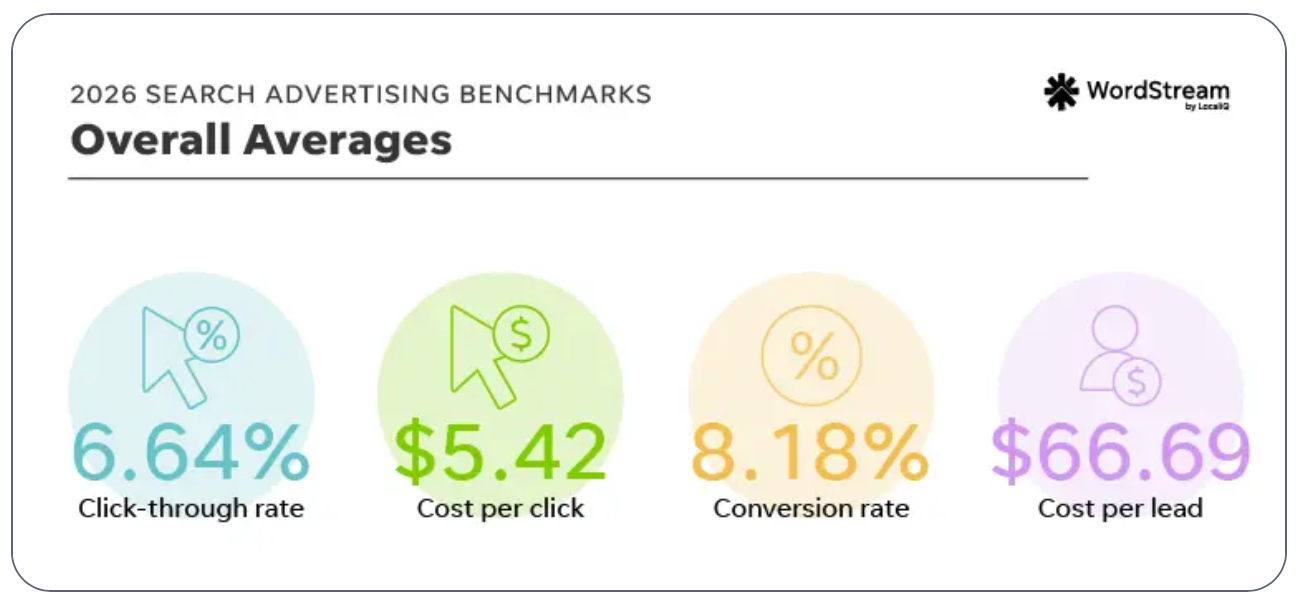

WordStream's 2026 Google Ads benchmarks report an average search CPC of $5.42 and an average CPL of $66.69, based on over 13,000 campaigns from April 2025 to March 2026. In the financial and insurance sector, the average CPC is $3.39, and the average CPL is $74.44.

Caption: Overall averages for search ads—click-through rate of 6.64%, cost per click of $5.42, conversion rate of 8.18%, cost per lead of $66.69. Source: WordStream 2026

Useful figures, but just the starting point.

For Fintech, true paid customer acquisition metrics are KYC completion rates, first deposits, first transactions, accounts with funds, retention balances, revenue per user, fraud rates, and payback periods.

Considering the data for financial applications, this is even more important—this category is still growing, but competition is becoming finer. Adjust reports:

- In the first half of 2025, sessions for financial apps increased by 16% year-on-year

- Financial app installations in Latin America increased by 59%

- Global financial app CPI dropped from $1.51 to $1.13

- Banking apps had the highest next-day retention among financial subcategories, reaching 20.6%

Paid social plays another role. It performs better in education, remarketing, message testing, creator amplification, usually more than high-intent conversions.

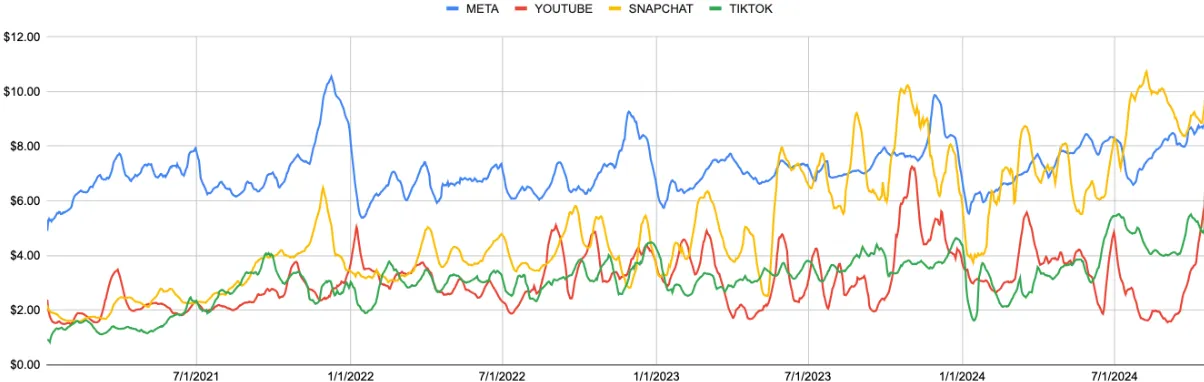

Gupta Media's 2025 social CPM tracking reports average CPMs: Meta $8.19, TikTok $4.82, YouTube $4.99, Snapchat $8.60, Pinterest $4.67. You calculate the numbers behind the funnel.

Caption: Meta usually peaks between $6 to $9; Snapchat saw over $10 spikes in 2023-2024; TikTok and YouTube are lower, fluctuating between $2 to $5. Source: Gupta Media 2025

My judgment: The best Fintech and Web3 teams will optimize towards quality evidence—verified users, funded accounts, active wallets, repeated transactions, revenue.

PR Becomes "Trust Distribution"

PR is often seen as a channel for launching. For financial products, I think it is more accurately understood as trust distribution.

Journalists are still willing to take useful PR, but the bar is higher. Cision's 2025 State of the Media Report found that 86% of journalists will outright reject pitches that do not match their field or audience. Meanwhile, 72% of journalists still consider press releases to be the most useful PR resource, and 85% say that the best way to build relationships is with a simple introductory email.

For Fintech and Web3, the strongest PR assets are substantial content: exclusive data, security practices, regulatory clarity, proof of reserves, risk frameworks, market maps, and founder comments.

Generic launch announcements have weak distribution capabilities unless they carry real market signals.

However, PR is rarely the cheapest customer acquisition channel. Its value is spread throughout the funnel. A credible article can improve search visibility, investor confidence, partner conversion, landing page trust, creator narratives, and founder authority. Therefore, I expect more financial companies to invest in research-driven PR in 2026.

KOL Marketing Becomes an Operational Layer

Creator marketing is becoming a serious budget line.

CreatorIQ reports:

- The average annual KOL marketing budget grew by 171% year-on-year

- 71% of organizations increased funding

- Nearly two-thirds of new spending comes from traditional paid and digital channels

IAB also reports that creator advertising will reach $37 billion in 2025, projected to reach $44 billion in 2026.

This makes sense for Fintech and Web3. Financial products need frequent explanations. Users must understand the use cases, risks, mechanisms, and why they should trust the product. Good creators often explain things more clearly than the brand's own channels.

But this channel has a very clear failure mode.

A creator with good reach may still bring low-quality users, compliance risks, or just attention without any activation. This is especially true in the crypto space—audiences have long been accustomed to sponsored posts, token incentives, and short-term narratives.

Stronger creator strategies in 2026 will be more selective.

📎 Extended reading: Why Most KOL Campaigns Fail | Green Dots Research (Most KOL campaigns fail not because creators are ineffective, but because teams buy attention before they properly fix positioning, audience matching, campaign structure, trust, and product maturity.)

I expect better outcomes to come from expert micro-creators, vertical analysts, founder collaborations, product explanations, long-term ambassador programs, and creator content that can be reused in paid advertising.

Key metrics should shift from "reach" to "actions that retain."

- For Fintech, this may be accounts with funds, deposits, card usage, transfers, or subscription revenue.

- For Web3, this may be exchanges, deposits, staking, lending, governance participation, fee generation, or repeated wallet activity.

Display Ads Still Have Their Place, but Not as Cheap Noise

Display ads are often undervalued, but this category still represents a large volume.

IAB and PwC report that display ads will reach $81.6 billion in 2025, up 9.8% year-on-year. Programmatic ads will reach $162.4 billion, growing 20.5%.

The issue is quality.

The ANA 2025 Q3 Programmatic Transparency Benchmark report shows that the nominal CPM for web and mobile is $4.27, while the TrueCPM is $6.66. This difference is significant—once you factor in quality, visibility, and supply chain efficiency, cheap inventory can conceal waste.

ANA also reported in Q2 2025 that $26.8 billion of global media value loss is still attributed to inefficiencies in programmatic.

For Fintech and Web3, broad, cheap display ads as direct response channels tend to be very weak. They can still be useful in specific roles: remarketing, ads on trusted financial media, newsletter sponsorships, native advertising, B2B account-based marketing, and contextually placed ads around market events.

Higher quality contexts are the bets for display advertising in 2026.

Web3 Enters the "Post-Task Era"

Web3 has a distribution advantage that most Fintech products lack: public behavior data.

A wallet can show what users actually do. This makes tasks, points, airdrops, whitelisting, and wallet-based activities powerful growth tools.

But the market has also learned the weaknesses of this model. Many users acquired through protocols never retain, never generate revenue, and merely inflate metrics while waiting for airdrops. The initial logic was close to "fake it till you make it": create visible activity volume, demonstrate traction, attract capital, and then hope for real usage to catch up.

When everyone does this, the system starts to collapse. Yield farmers simulate demand, teams report inflated growth, token rewards are dumped, and the next protocol has to pay more for lower-quality activities.

We do not yet have a clean set of public time series that show that total market investment in task platforms is declining. However, evidence from 2025-2026 explains why protocols are increasingly skeptical about "making tasks the primary customer acquisition engine."

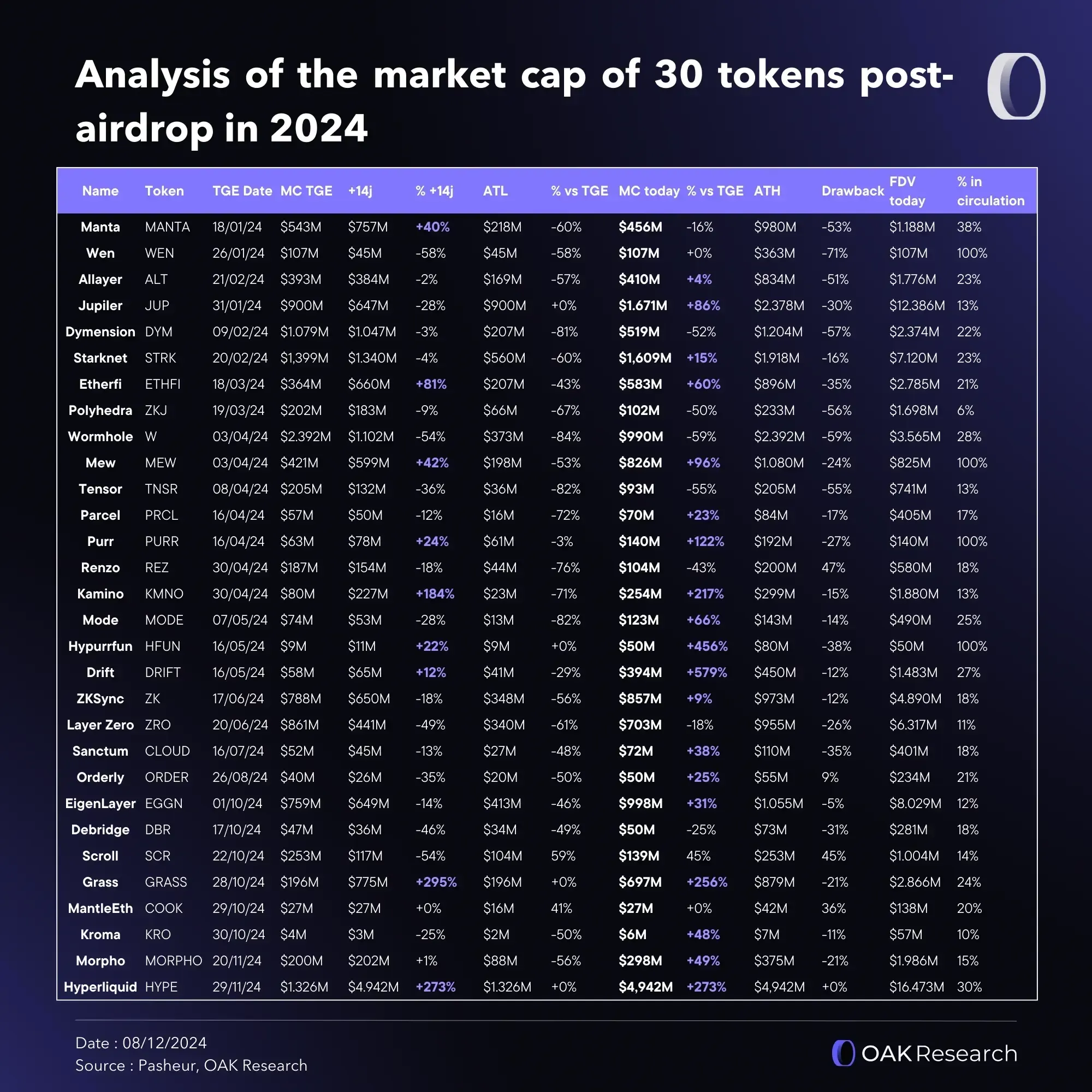

DappRadar found that since 2017, projects have distributed over $20 billion through airdrops, with 88% of airdropped tokens depreciating within three months. It also found that activity often returns close to baseline within weeks, with many users cashing out right after claiming rewards.

Caption: A comparison of the TGE market values, 14-day performance, historical highs and lows, current market values, drawdowns, FDV, and circulating supply of 30 airdropped tokens in 2024. Performance varies greatly—Hyperliquid, Drift, Grass, Kamino, Hypurrfun, etc. are far above TGE levels, while many others are still significantly below their issuance estimates. Source: DappRadar

A recap of the top five airdrops of 2025 from Decrypt shows that the market has cooled compared to 2024. The top five airdrops in 2025 peaked at $4.5 billion, while airdrops in 2024 sent out over $19 billion at historical peaks. Several major airdrop tokens in 2025 saw significant declines from their peaks.

Another 2025 paper on "witch detection" analyzed 193,701 addresses, including 23,240 witch addresses, illustrating the extent of the fake user issue.

Operational Conclusion: Tasks will not disappear, but their role has changed. I would view them as a filtering or educational layer, rather than a primary customer acquisition engine.

A stronger approach would be to have users prove their suitability through meaningful actions: deposits, trades, holding periods, governance, fee generation, referrals, wallet history, retention.

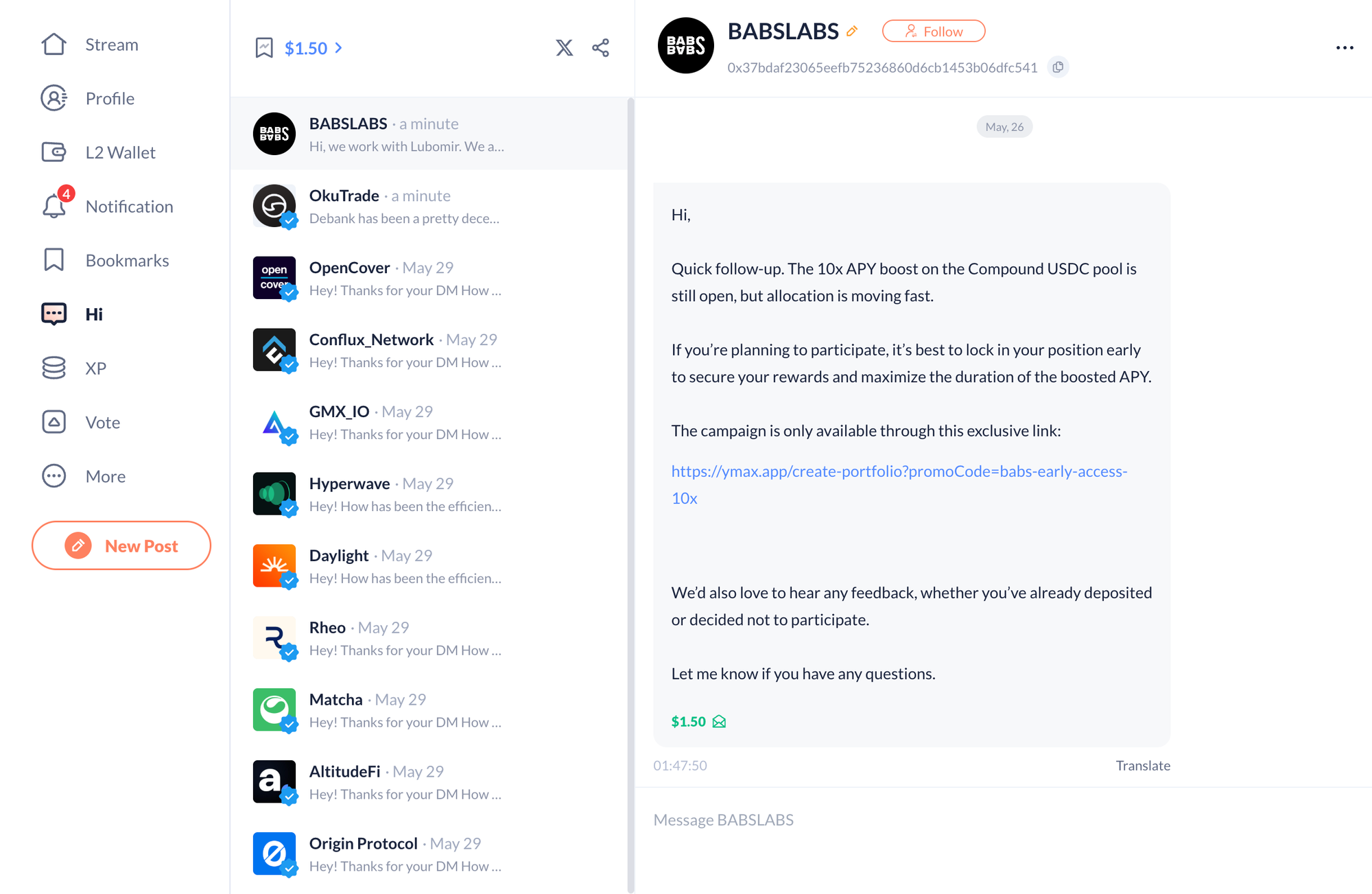

The same logic applies to targeted wallet-based reach and cold outreach via private messages in DeBank style. Mass messaging carries reputational risks and usually yields low quality.

Narrow, perceived wallet reach may be useful when user's on-chain activities have clearly demonstrated product relevance. However, this remains very experimental. The public conversion benchmarks for this strategy in 2025-2026 are still weak, so I treat it as a form of guerrilla marketing.

Caption: This private message follows up on a Compound USDC pool's 10x APY boost, stating that the quota is being quickly claimed and includes a link for an exclusive early access event. Source: DeBank

What Teams Should Measure in 2026

The old growth dashboard rewards superficial activity. The dashboard for 2026 needs to reward user quality.

For Fintech, useful metrics are: verified users, KYC completion, first deposits, funded accounts, first transactions, repeated transactions, retention balances, revenue per user, fraud rates, payback periods, and acquisition quality.

For Web3, useful metrics are: active wallets, real liquidity, repeated use, fee generation, deposits, exchanges, staking, lending, wallet history, and retention after incentive decay.

This does not mean that every channel should be judged by last-click revenue. PR, creator marketing, search, paid social, display ads, and wallet-based activities each serve their own purpose.

But each channel should connect to a quality signal somewhere in the funnel.

A distribution system that cannot distinguish between "retained users" and "paying tourists" is a report issue waiting to become a budget concern.

The Distribution Stack We Believe Will Win

The strongest Fintech and Web3 teams will build a stack.

PR creates authority. Founders turn authority into narrative. Creators translate narrative into education. Paid social tests and amplifies messages. Search captures intent. Display and native ads support remarketing. Wallet-based activities filter users. Lifecycle marketing turns acquisition into activation and retention.

This is the transformation we care most about at Green Dots.

Distribution is becoming increasingly intolerant of false demand.

The teams that will win in 2026 will be those that proactively stop considering activity volume as growth before the market forces them to do so.

If you need help designing distribution strategies, feel free to contact us.

Author's note: The author of this article, Stacy Muur, is the founder of Green Dots. Green Dots collaborates with Web3 teams to develop GTM strategies, creator-driven distribution, founder growth, and launch architecture.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。