Author: degentrading

Translated by: ShenChao TechFlow

ShenChao Guide: Everyone wants to turn into neocloud (new type of computing cloud), with xAI, Meta to SoftBank all entering the market to sell computing power. The author degentrading uses a real contract where Google pays SpaceX to reverse engineer: 110,000 GB200 cards, at a rental price of $11.6 per card per hour, a 100MW data center can break even in less than a year. This article systematically dissects the cost structure and ledger of neocloud, answering a core question: why building data centers and selling computing power is the best business now.

"xAI reaches cooperation with Google."

"Meta signals a willingness to sell its surplus computing infrastructure."

"SoftBank plans to provide 10GW scale AI computing power in the US."

It seems everyone wants to become neocloud and start selling computing power. Why is that?

Let me guide you through the neocloud's accounts, starting with a real case.

On June 5, 2026, Google announced it will pay SpaceX $920 million each month to rent the computing power of the xAI data center.

This batch of computing power includes 110,000 Nvidia GPUs, plus CPUs and other memory components, which means a fully equipped data center (Colossus 2).

Here the GPUs are Nvidia's GB200 NVL72.

At this price, the unit price for each GPU is $920 million / 110,000 / 720 = $11.6 per hour.

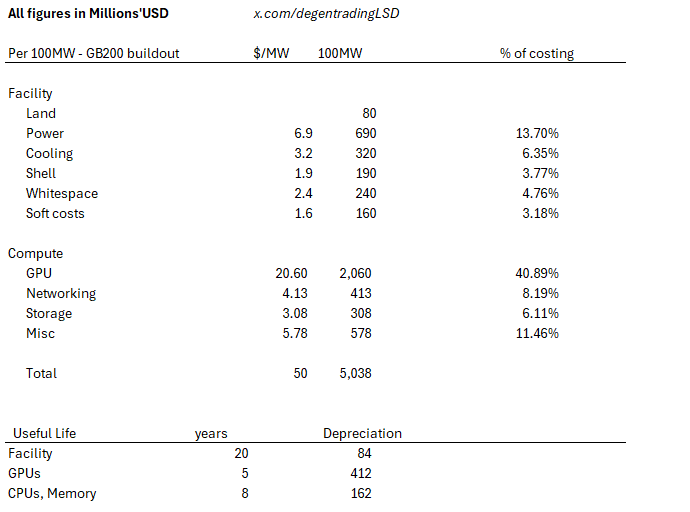

Let's imagine a 100MW data center filled with GB200.

Caption: The author's estimation of the construction cost for a 100MW data center is about $5 billion per GW

My estimate is about $5 billion per GW. Thus, the construction cost for 100MW is approximately $5 billion.

This number aligns with industry estimates. Note, this is the construction cost for GB200. The more advanced the chip, the more expensive it is; for example, the construction plan for GB300 has a computing power cost about 20% higher.

Jensen Huang said a cost of $10 billion per GW is actually very realistic—if you consider Rubin's computing power costs, they are double that of Blackwell. Costs for electricity and others are also rising.

We also know each GB200 consumes about 1200 watts, so 100MW translates to approximately 83,333 GPUs.

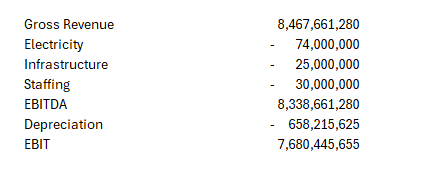

Using the economic model of the xAI contract, revenue is 83,333 × $11.6 × 365 × 24 = $8.467 billion per year.

The cost structure is as follows:

Annual electricity cost of $740,000 per MW, annual infrastructure maintenance of $250,000 per MW, annual labor cost of $300,000 per MW.

Caption: The accounting of the 100MW data center based on xAI contract rent ($11.6 per card per hour) shows a payback period of less than a year

So we see a crazy scenario: a payback period of less than a year.

I must say, this SpaceX contract is absurdly generous. Is Google facing a serious shortage of computing power?

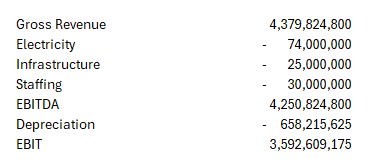

If we switch to a less insane, more normal assumption, such as a price of $6 per hour.

Caption: After the rent drops to $6 per card per hour, the payback period extends to about two years

The payback period extends to about two years.

I estimate that the long-term contracts signed by neocloud with hyperscale cloud providers have prices close to about $4 per hour. Hyperscale cloud providers then resell this computing power at a higher price, for example, AWS's price over $12.

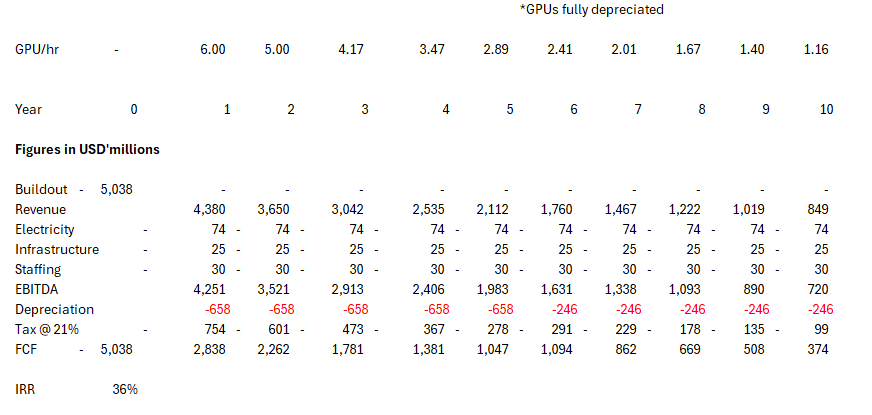

Just for fun, I created a profit and loss estimate for a single data center, which looks like this.

Caption: Estimated profit and loss statement for the construction of a single data center

Of course, we can argue that GB200 loses value after five to six years. However, A100, which was released in 2020, is still being rented out for $1 to $2 per hour. This card rented for about $3 in 2021, and hyperscale cloud providers are still renting it out for $2 to $3.5 per hour now.

Gavin Baker believes that the depreciation cycle for GPUs should be extended to about 10 years. I agree with him, especially as the demand for agent AI and inference grows.

In the end, the current computing power market is pricing for a serious shortage.

If someone tells you otherwise, they are turning a blind eye.

SpaceX is renting computing power because the prices it charges are incredibly profitable (also because of issues connecting Colossus 1 and 2). When Musk signed this contract, he also retained the right to terminate the lease early, saying, "If computing power becomes particularly tight, I've said we might need to take it back at some point."

In short: now everyone wants to be neocloud because computing power is extremely tight, and it's printing money.

Based on current facts, the ability to build data centers and sell computing power is the best business right now.

This is also the reason why hyperscale cloud providers are willing to prepay to neocloud, locking in the supply of computing power.

Let me emphasize again that the valuation of a neocloud should equal the net present value of all the computing power contracts it can secure. Therefore, financing ability, accurate depreciation rhythms, and execution capabilities are the three most important levers affecting valuation.

Those who claim this is all circular financing (call it whatever term you want) should know: Anthropic now offers inference services with a gross profit margin exceeding 70%. Those cutting-edge laboratories that consume the most computing power can switch to positive cash flow anytime they want, as long as they are willing.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。