Written by: Rita

Trends Guide

Goldman's latest outlook on the second-quarter performance of the U.S. semiconductor sector gives a somewhat twisted judgment: almost all sub-sectors' performance expectations will be exceeded, but that may not be good news. The reason is straightforward: the Philadelphia Semiconductor Index rose 88% in the second quarter, while the S&P 500 only rose 14%, and this gap has already incorporated most of the good news into stock prices.

The truly noteworthy aspect of this outlook is that Goldman's specific ratings have begun to decouple from performance expectations themselves. Similarly expected to exceed expectations, some companies are maintained as bullish while others are downgraded to neutral or even bearish, with the dividing line not based on performance, but on how much the stock price has risen prior.

Goldman’s bullish lines of thought are semiconductor equipment, computing power, and storage. The expectation for analog chips has also been raised overall. Computing power benefits from revised capital expenditures from hyperscale cloud providers, with room for upward adjustment in server CPUs and specific ASIC projects. In the storage line, Goldman favors hard drives and NAND flash memory, reasoning that these two types of products have not seen significant new supply recently. For semiconductor equipment, Goldman expects WFE spending to pull forward inventory, with long-term visibility extending to 2028. In the analog chip sector, Goldman prefers companies with larger exposure in industrial, aerospace defense, and data center end markets, logic being that the recovery pace of demand in these areas is steadier than in consumer electronics, leading to greater certainty in performance realization.

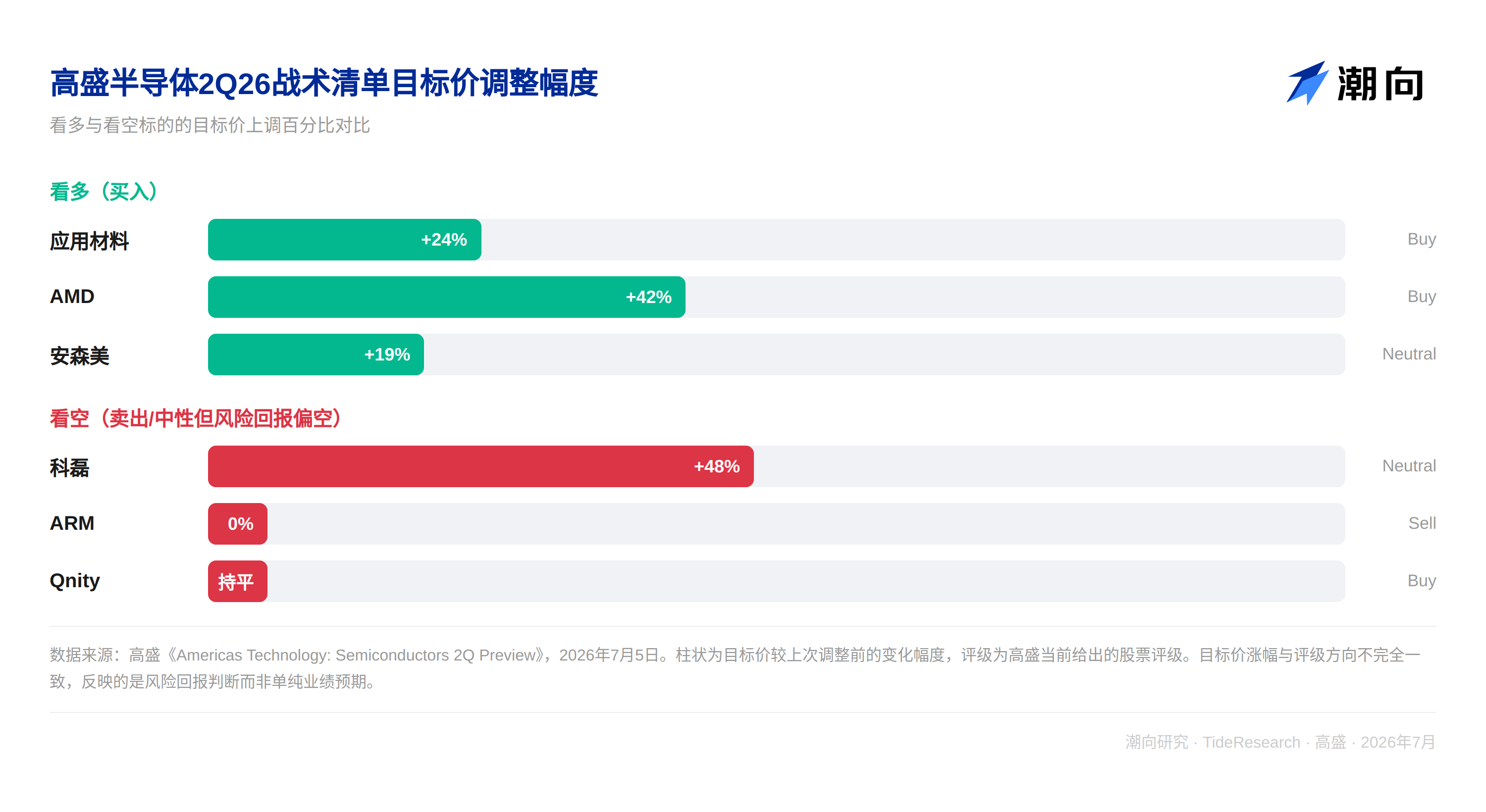

Same outperformance, yet ratings diverge

In Goldman’s tactical list, companies like Applied Materials (AMAT), AMD, and ON Semiconductor are bullish, whereas companies like KLA Corporation (KLAC), ARM, and Qnity (Q) have a weaker risk-reward ratio.

Viewing ARM and KLA together illustrates the issue best. ARM's own performance is not poor; Goldman views its operational fundamentals as stable, but the problems lie in two areas: firstly, the continued weakness in the smartphone market will drag down its royalty income, and secondly, operating expenses are higher than expected. Looking only at these two aspects, it barely equates to “third-quarter guidance slightly below market expectations,” which does not qualify for a “bearish” rating. What truly crushes the rating is the stock price; ARM's previous price increase was substantial, incorporating several quarters’ optimistic expectations, so even slight underperformance is enough to trigger a downgrade.

KLA represents a different type of decoupling. The current round of equipment spending is focused on DRAM expansion, while the demand intensity for testing and measurement equipment associated with DRAM production is inherently lower than that for logic chips. This has nothing to do with KLA's own operational capabilities; it is purely a structural allocation issue within this round of capital expenditures. Even if performance slightly exceeds expectations, it is likely to underperform its peers. Although the target price has been raised from $155 to $230, the rating remains only neutral.

Companies bullishly maintained: Applied Materials, AMD, and ON Semiconductor

The situation for the companies that are still bullish is quite the opposite.

The logic for Applied Materials is that DRAM demand will drive it to become one of the top growth companies in the industry by 2026. Goldman sees visibility extending to 2028 and believes there is room for price increases, raising the target price from $520 to $645.

In AMD’s line, server CPU demand will drive this quarter's performance to exceed expectations, even though the PC side may lag behind. The target price was raised from $450 to $640, with the 2027 EPS forecast 13% higher than the consensus expectations in the market.

For ON Semiconductor, there is a different typical case; previously, due to rumors about the acquisition of Synaptics, its stock price dropped by 30%. Market expectations were already very low, and Goldman believes this actually provides a decent risk-reward ratio, with the target price raised from $80 to $95.

The commonality among these three cases is that the stock prices had not previously risen to the extent of exhausting expectations, meaning that the performance exceeding expectations can truly realize stock price space.

Storage sector and Qnity, the two extremes of logic

The storage sector embodies this logic even more extremely. SanDisk’s target price was raised from $1200 to $2200, with the 2026 EPS forecast more than 30% higher than the consensus expectations in the market. Seagate’s target price was raised from $700 to $960, both companies' logic being the tight supply of hard drives and NAND leading to sustained strong pricing. Western Digital maintains a neutral rating, with a target price raised from $400 to $650, but its year-to-date increase has reached 240%, clearly outperforming the Philadelphia Semiconductor Index, which explains why it is unable to achieve a higher rating, despite good performance expectations.

Qnity is the most subtle case in this logic. It is a wafer manufacturing materials company that spun off from traditional materials business and listed independently. Goldman includes it in the maintained buy rating list, giving long-term positive judgment on its improved wafer foundry capacity utilization and operational execution. However, in this tactical grouping of the outlook, Goldman still categorizes it under a weaker risk-reward ratio, reasoning that the prior stock price increase has been significant, and the room for further upward movement is not as ample as before. This is different from ARM and KLA, where the performance itself has issues; Qnity is the only one of the three cases where “the company is fine, and the stock price is fine; it's just no longer cheap,” perfectly completing the spectrum of decoupling ratings and performance: even with a buy rating, it does not mean the forthcoming stock price movement will be proportional to the performance realization.

Trends Perspective

The truly interesting aspect of this outlook is that it inadvertently exposes a blind spot in institutional ratings: ratings themselves measure the difference between how much expectations regarding performance and stock prices have already been reflected, rather than simply judging whether performance is good or bad. Neither ARM nor KLA are companies with deteriorating fundamentals; the former suffers from the backlash of its own rise, while the latter is weighed down by the structural allocation in this round of capital expenditures, both of which are largely unrelated to the company's operational capabilities.

One more point worth noting is that Goldman has existing or seeks investment banking business relationships with most companies mentioned in the report. Such conflicts of interest do not necessarily imply bias in judgment, but verifying the target prices and ratings provided by institutions independently is always a good practice.

For investors, the truly useful part of this report is to remember that whether performance exceeds expectations and whether stock prices can continue to rise within the same earnings season are never the same thing. Understanding how much a company has increased in value in the past is often more important than understanding how much it earned this quarter.

Disclaimer

This article is a compilation and interpretation of third-party brokerage research reports by Trends Guide. The ratings, target prices, profit forecasts, and related judgments quoted in the article reflect the opinions of the analysts from that brokerage and represent the position of their affiliated institution, not the opinions of Trends Guide, and do not constitute any investment advice.

The market has risks, and decisions need to be independent. This article should not serve as the basis for buying or selling any securities.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。