Author: EXIO Research Institute

When "Safe Assets" Are No Longer Safe

On June 30, 2026, in the Tokyo foreign exchange market, the US dollar reached 162.36 against the yen. It was on the same day that Bitcoin rallied back to $60,000.

The last time the yen was at this level was in 1986. That year, the Chernobyl nuclear power plant exploded, Microsoft went public, and the aftermath of the Plaza Accord was still reshaping the global economic landscape. Thirty-nine years later, the yen returned to the same place—but this time, it was not appreciating, but collapsing.

For savers in Japan, this means that nearly one-third of their hard-earned purchasing power has evaporated in less than five years. For global wealth holders, this is a textbook-level case of how the narrative of "safe assets" is slowly unraveling.

This is not a coincidence. It is a monetary experiment spanning four decades, reaching its climax.

Chapter 1: From the Pinnacle of the World to a Liquidity Trap — A 40-Year Journey of the Japanese Economy

The Plaza Accord: A "Designed Prosperity"

On September 22, 1985, the United States, Japan, West Germany, France, and the United Kingdom signed an agreement at the Plaza Hotel in New York to coordinate interventions in the foreign exchange market to push for the depreciation of the US dollar. The yen surged from 240 yen to 1 dollar to 120 yen within two years—an appreciation of 100%.

For Japan at the time, this was a "great power passport." With a stronger yen, Japanese companies' overseas purchasing power skyrocketed. Mitsubishi purchased Rockefeller Center, and Sony acquired Columbia Pictures. The world was talking about "Japan First."

But the Plaza Accord was also a slow-motion bomb.

To hedge against the impact of yen appreciation on exports, the Bank of Japan cut interest rates from 5% to 2.5% during 1986-1987. Cheap capital flooded into the stock and real estate markets. On December 29, 1989, the Nikkei 225 index reached 38,957 points—this record remains unbroken to this day.

Bubble Burst: A 30-Year Balance Sheet Repair

In 1990, the bubble burst.

The Bank of Japan urgently raised rates to burst the bubble but it was too late. The stock market plummeted by 60%, and commercial real estate prices fell over 70%. Businesses and households entered a "balance sheet recession"—not because they had no money, but because they were afraid to spend, afraid to borrow, and only dared to pay off debts.

For the next thirty years, Japan experienced almost all the "impossibles" found in economics textbooks:

• Zero Interest Rate Policy (ZIRP): Entered the zero interest rate era in 1999

• Quantitative Easing (QE): Became the world's first central bank to implement QE in 2001

• Negative Interest Rates: Reduced policy rates to -0.1% in 2016

• Yield Curve Control (YCC): Pegged 10-year government bond yields near 0%

• Central Bank Direct Purchase of ETFs: The Bank of Japan became the largest shareholder on the Tokyo Stock Exchange

Each of these was a "first" in global central bank history. Each attempted to break deflationary expectations. Each ended in failure.

The legacy of Abenomics: The Limits of the Money Printer

In 2013, Shinzo Abe came to power with "three arrows": bold monetary policy, flexible fiscal policy, and structural reforms.

The first two arrows were shot. The Bank of Japan's balance sheet soared from 160 trillion yen before Abe took office to over 760 trillion yen (about $4.7 trillion)—over 130% of Japan's GDP.

The yen depreciated from 80 yen to the dollar in 2012 to 125 yen in 2015. Export companies cheered, but ordinary families' purchasing power was slowly eroded.

Yet the third arrow—structural reform—was never truly shot.

Chapter 2: 2026, The Critical Point

The Paradox of BOJ Rate Hikes

On June 16, 2026, the Bank of Japan raised the policy interest rate to 1.0%—the highest level in 31 years since 1995.

Logically, rate hikes should support the currency. However, after the interest rate increase, the yen not only did not strengthen but also accelerated its decline from 155 to 162.36 within two weeks.

The market was telling the BOJ a harsh truth: a 1% interest rate is still laughably low globally. The Federal Reserve's policy rate is at 4.25-4.50%, with a spread over 350 basis points. As long as this spread exists, shorting the yen is the most crowded and least imaginative trade in the world.

Red Alert for the Banking System

On June 28, 2026, Nikkei Asia reported a disturbing news item: several of Japan's largest banks were seeking assistance from the government and the BOJ—they were struggling to raise US dollar funds for promised US investment projects.

The more the yen falls, the higher the cost for Japanese institutions holding dollar assets. The amount they promised for US investments—as part of US-Japan tariff negotiations—amounts to hundreds of billions of dollars.

This is a typical "dollar trap": Japan is required to export capital, but its currency is depreciating at the fastest rate in 39 years. Each depreciation makes the next dollar financing more expensive.

Circle + Nomura: A Digital Patch for the Fiat Currency System

On June 25, 2026, Circle, the world’s second-largest stablecoin issuer, announced a collaboration with Nomura Securities, planning to provide instant foreign currency settlement services for Japanese companies as early as 2027.

This news is typically framed within the narrative of "crypto adoption." But in the context of the yen hitting a new low in 39 years, it tells a different story: Japan is searching for a back door to escape the traditional foreign exchange system.

Stablecoins essentially bypass the existing interbank settlement system. When a Japanese company settles cross-border through USDC instead of the SWIFT network, it saves not just transaction fees—it circumvents the entire bank-intermediated dollar clearing system.

This is also why Circle chose Nomura: not Coinbase, not Binance. It is Japan's largest brokerage, a systemic player holding 300 trillion yen in client assets.

$3.5 Billion of Futile Effort

On April 30, 2026, the Ministry of Finance of Japan intervened in the foreign exchange market.

According to market analysis firms, Japanese authorities spent approximately $35 billion in a single day attempting to support the yen's exchange rate. This was one of the largest single-day intervention actions in Japan's history.

The result? The yen briefly rebounded to 155, then continued to decline. Two months later, it not only returned to pre-intervention levels but also hit a new low in 39 years.

Market analysis platform Lambda Finance pointed out in a report in May: "The MOF will not tolerate the USD/JPY consistently breaking above 160—that is the practical intervention bottom line."

Two months later, this bottom line was ruthlessly breached.

This is not a failure of the intervention strategy. It is a manifestation of a deeper law: in an era of global capital free movement, a country's foreign exchange reserves are like a cup of water trying to extinguish a forest fire in front of a $7.5 trillion foreign exchange market.

Chapter 3: The Mirror of Bitcoin

Yen vs Bitcoin: A Picture is Worth a Thousand Words

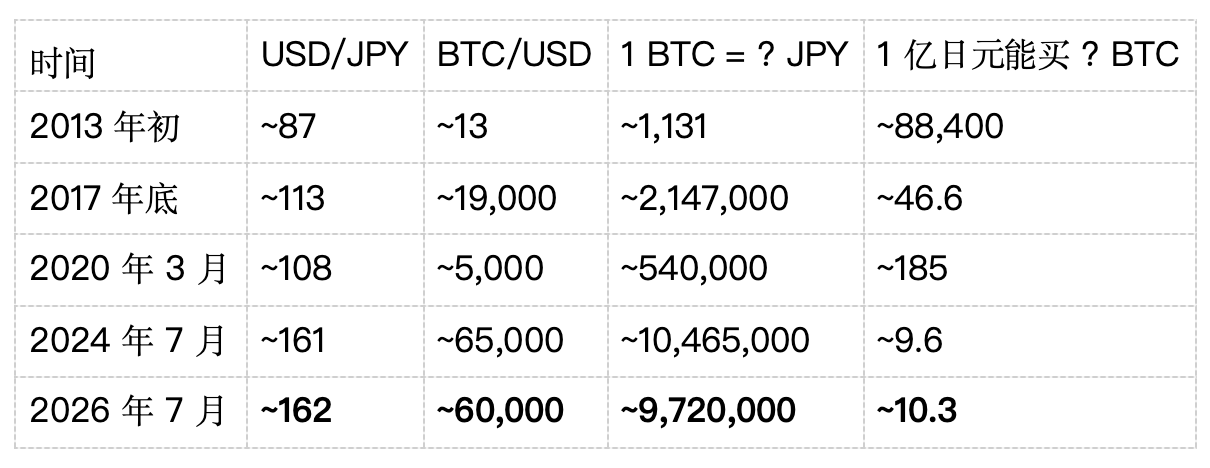

Let’s look at a simple set of numbers:

In the past 13 years, the purchasing power of 100 million yen in Bitcoin has shrunk from 88,400 BTC to 10 BTC. This is not volatility; it is the intergenerational transfer of currency value.

Data source: CoinGecko historical prices (BTC/USD), Investing.com historical exchange rates (USD/JPY). July 2026 data is a real-time snapshot.

The yen is depreciating, but Bitcoin, when priced in yen, has not become cheaper—because the price fluctuations of Bitcoin itself far outweigh the buffering effect of the yen's exchange rate. For Japanese investors, the core variable determining gains and losses in holding BTC is not the direction of the yen, but the global pricing of BTC itself.

Bitcoin is Not "Digital Gold," but the "Escape Key for Sovereign Currency"

The traditional narrative positions Bitcoin as "digital gold"—a tool for hedging against inflation. But this framework underestimates the true meaning of Bitcoin.

Bitcoin does not hedge against inflation. It hedges against the unsustainability of the monetary system.

Japan provides the most extreme example: no hyperinflation, no regime change, no wars happening at home. Everything seems "stable." But beneath the surface of stability, the central bank's balance sheet has inflated to 130% of GDP, interest rates have lingered near zero for a quarter of a century, and the yen has returned to the same low point after nearly forty years.

This is the "boiling frog" type of currency depreciation. It is not dramatic, but equally lethal.

For savers in Japan—especially the aging population holding large amounts of cash and Japanese government bonds—Bitcoin offers something they cannot find within the banking system: the escape key.

An asset unaffected by any central bank balance sheet. An asset that cannot be diluted by QE. An asset whose supply is mathematically locked.

This is not about "faith" in cryptocurrency. It is about recognizing that in a world where all central banks are racing to print faster than each other, holding an asset that cannot be printed is not speculation—it is risk management.

Chapter 4: Implications for Wealth HoldersJapan is Not an Outlier, but a Pioneer

Japan’s monetary dilemma has its particularities in terms of demographics and debt dynamics. But the pattern it reveals—aging + high debt + central banks forced to maintain easing → long-term currency depreciation—is the trajectory almost all developed economies are entering.

The yen of 2026 provides a thought-provoking reference point for observing the monetary prospects of other developed economies.

For PI clients, the core question is not "Is Bitcoin too volatile?" but:

How many assets in your portfolio can truly not be diluted?

Real estate?—subject to policies, taxes, and demographic changes. Gold?—with annual mining of about 3,000 tons, new supply at 1.5-2%. Government bonds?—nominal values are guaranteed, but purchasing power is not. Stocks?—companies can issue more shares. Indices can be replaced with components.

Bitcoin is the first and currently the only large-scale financial asset that cannot be systematically diluted by any institution or mechanism.

Allocation Framework (Not Investment Advice, For Consideration Only)

Without changing the red line of investment advice, a thought-provoking analytical perspective is worth considering:

Different investors have different positions on Bitcoin based on their risk tolerance and asset structure—some view it as a small tail risk hedge, while others categorize it alongside gold as a value-retaining tool. Each choice depends on individual financial situations, investment goals, and risk preferences, with no universal standard answer.

The above is merely an abstract statement of asset allocation thoughts and does not constitute suggestions or recommendations regarding any assets or proportions. Any allocation decisions should be based on individual financial situations and in consultation with licensed financial advisors.

Chapter 5: Future Outlook — When Consensus is Breached

When the Blind Spots of Consensus Are Revealed

Forward-looking statement: The following discussions about the yen exchange rate, Bitcoin price, and market trends are based on extrapolations and analyses of data from third-party sources and current market conditions and do not constitute predictions, guarantees, or commitments regarding future prices, exchange rates, or market trends. Past performance and current trends do not represent future results.

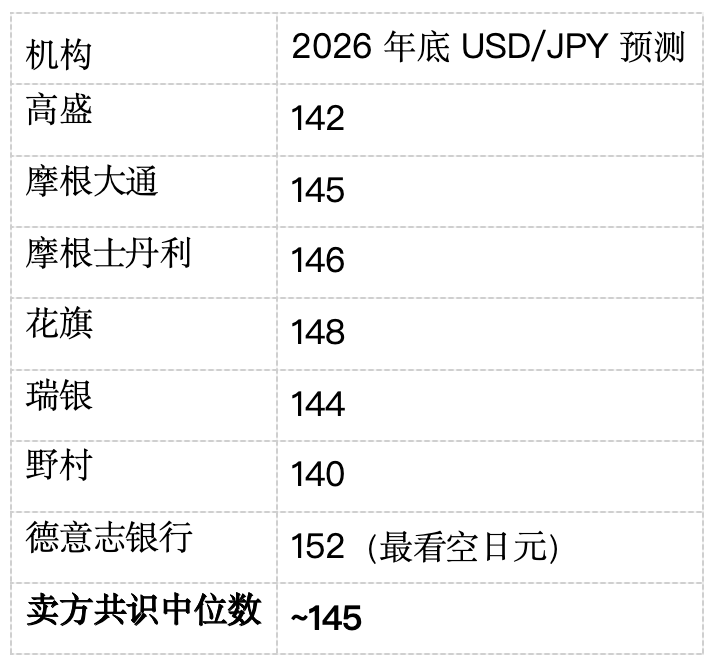

In May 2026, major global investment banks had the following predictions for the year-end USD/JPY (compiled by Lambda Finance):

Just two months later—on July 2, 2026—the USD/JPY stood at 162.55.

This is not just a prediction deviation. It is a structural failure of the entire sell-side consensus.

Even Deutsche Bank—the most bearish on the yen among the seven—was still 10 yen lower than the current actual level. Meanwhile, Nomura, which is the most bullish on the yen (predicting 140), had a discrepancy exceeding 22 yen from reality.

What happened? The core assumption of the consensus was: Fed rate cuts + BOJ rate hikes = narrowing interest rate differential = strengthening yen. This assumption is logically valid but overlooks a crucial variable: the inertia of capital flows. The scale of yen short positions established by global investors over the past three years is so massive that even if the interest differential narrows from 530 basis points to 350 basis points, it is still far from triggering large-scale liquidations.

Three Possible Futures

Based on existing data and structural forces, we can outline three possible paths:

Path One: Intervention Triggers Reversal (Probability: Low)

The Japanese Ministry of Finance coordinates a large-scale intervention with the Federal Reserve while the BOJ unexpectedly raises rates by more than 50 basis points. The yen quickly rebounds to the 140-150 range.

Lambda Finance warned in their May report: "The arbitrage liquidation in August 2024 proves that 140 can be reached within days." But this reversal requires extreme conditions—it needs cooperation from the US, and in the current context of US-Japan trade negotiations, there is significant uncertainty regarding whether Washington is willing to help Tokyo support the yen.

Path Two: Slowly Sliding into the Abyss (Probability: Medium-High)

The BOJ continues to raise rates slowly by 25 basis points each time, with the yen moving toward 170-180 amidst repeated interventions and rebounds. The independent forecasting model LongForecast’s technical forecast for USD/JPY indicates that the yen may reach 172 by the end of 2026 and breach 180 by mid-2027.

Bloomberg’s report at the end of 2025 already issued warning signals: "The voices bearish on the yen are growing louder in 2026 due to the BOJ's overly cautious policy path." This statement is coming true.

Path Three: Black Swan (Probability: Low, but Consequences Are Huge)

A major shakeup occurs in the Japanese government bond market, or the Japanese banking system faces systemic pressures due to a dollar financing gap. At this point, the BOJ will be forced to choose between "supporting the exchange rate" and "protecting the bond market/banks"—historically, central banks have always chosen the latter.

For holders of yen, the endpoints of Path Two and Path Three are the same: the continuous evaporation of purchasing power.

Institutional Voices

"The direction is favorable for the yen over a 12-month horizon, but it will be chaotic in the short term." — Consensus from multiple G10 foreign exchange desks (Lambda Finance, May 2026)

"Bearish voices on the yen are getting louder in 2026 due to the BOJ's overly cautious policy path." — Bloomberg (December 25, 2025)

"The MOF will not tolerate the USD/JPY consistently surpassing 160—that is the practical intervention bottom line." — Consensus from Lambda Finance foreign exchange strategy (May 2026)

"If Ueda raises rates faster than the market pricing, the USD/JPY will fall below 140." — Multiple G10 foreign exchange desks

The four quotes come from different points in time. Looking back today, the most striking is the third quote: "160 is the intervention bottom line" — two months later, it was 162.

This is precisely the essence of the fiat currency system's dilemma: central banks can talk tough to the market, but the market doesn’t have to believe them. The market only needs to calculate interest differentials.

Implications for Bitcoin

If the yen moves toward 180-200 in the next 2-3 years (as warned by independent forecasting models), then the price of Bitcoin in yen will no longer be 9.8 million yen—but rather 11-12 million yen, or even higher.

The above is a hypothetical extrapolation based on third-party forecasting models and current interest rate differentials. Actual exchange rates and prices depend on multiple variables, including but not limited to the BOJ's policy path, Federal Reserve rate decisions, global capital movements, and geopolitical events.

For Japanese investors, this is not a question of whether Bitcoin will rise. This is a question of whether the yen will continue to fall. The data over the past 40 years provides an answer that cannot be ignored.

Ending: The Last Chapter of the Plaza Accord

The Plaza Accord of 1985 opened the path for the appreciation of the yen. The yen's new low of 39 years in 2026 may be one of the last few chapters of this story.

But the significance of this story extends beyond Japan.

It reminds us: the "stability" of currency is an illusion, a balance artificially maintained by central banks during specific historical periods. When demographics, debt levels, and global capital flows all shift simultaneously, this balance will shatter.

Bitcoin is not perfect. But it offers an alternative outside the fiat currency system. And for astute wealth holders, the option itself is the most valuable asset.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。