Key Takeaways:

- Farside says STRC’s $100 price mechanism may weaken if Strategy raises coupons.

- Strategy plans buybacks, a dollar reserve and possible BTC sales to manage risk.

- STRC traded near $75 before rebounding, with Farside urging buybacks or a shift toward SOFR.

Strategy’s move to create a Digital Credit Capital Framework has sharpened scrutiny of one of its most complex financing tools: STRC.

Farside Investors, a UK investment adviser, argues that STRC’s price-stability mechanism is fundamentally unstable. The product was largely issued around $100, with a mechanism intended to guide the market price back toward that level.

In theory, if STRC trades below $100, Strategy can raise the dividend to support the price. If it trades above $100, the company can lower the dividend. Farside says that structure creates a dangerous feedback loop. If investors become more concerned about Strategy’s credit risk, STRC could fall. Raising the dividend to support the price could then increase cash strain and further weaken confidence.

The firm also notes that the coupon is discretionary, not automatic. That gives Strategy flexibility, but it also creates uncertainty for investors trying to value the security.

Farside said borrowing at 11.5% to buy bitcoin looks unattractive on basic financial terms. Even if bitcoin performs well over the long term, it may not rise smoothly enough to cover that cost without forcing asset sales during weak markets.

The analysis points to a sharp valuation split. If investors assume STRC keeps paying an 11.5% dividend in full, Farside’s calculator values the instrument at about $144 using an 8% discount rate.

But STRC is not a fixed-rate bond. Strategy has the right to lower the coupon by 25 basis points each month, potentially all the way down to Secured Overnight Financing Rate (SOFR), which Farside cites at around 3.6%. Under that assumption, the instrument is valued at about $55.

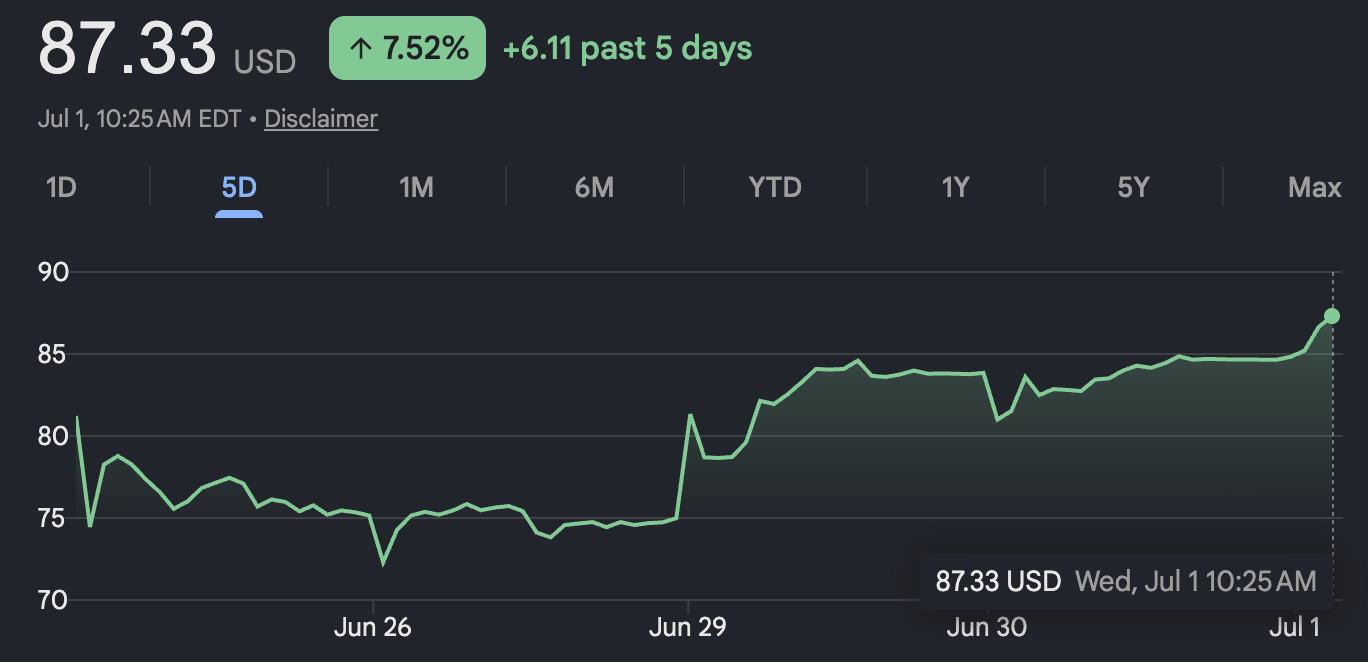

STRC Price – 1 July 2026, 10:25 EDT. Source: Google Finance

That gap explains why STRC is difficult to price. It was not issued at $55 or $144, but around $100, meaning investors were effectively buying into uncertainty over future coupon policy and the credibility of the price-stability mechanism.

STRC has recently traded around $75, roughly 25% below its target price, before rebounding to $86. Farside said that suggests the stability mechanism is already failing, or at least no longer functioning as investors may have expected.

The critique comes as Strategy adopts a broader capital framework. The company plans to build a U.S. dollar reserve, raise the STRC dividend to 12%, buy back preferred securities at a discount, and authorize bitcoin sales to help fund dividends and reserves.

That marks a notable shift. For years, Strategy issued equity at a premium to its bitcoin holdings and used the proceeds to buy more BTC. With the stock now trading closer to the value of its holdings, that machine is less effective.

Andrei Grachev, managing partner at DWF Labs, said the company is no longer simply a one-way bitcoin buyer. He described the change as a managed shift rather than a fire sale, but one that turns the largest source of corporate bitcoin demand into a potential seller. He commented:

Strategy is doing something with bitcoin: shifting it from a reserve you simply hold and never touch, to one you actively manage, selling, buying back, and funding when it serves the balance sheet. The asset stays central; the discipline around it changes completely.

Farside sees two likely long-term solutions: buy back STRC or abandon the price-stability mechanism and move the coupon toward SOFR. Doing nothing may be easier in the short term, but the firm says it only delays the problem.

For bitcoin treasury companies, the message is clear. The market is moving from accumulation at any cost to balance-sheet discipline, liquidity management, and investor trust.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。