Author: Nancy, PANews

The cryptocurrency bear market continues, and exchanges are adjusting their course, extending their business reach towards US stocks and other traditional financial markets, accelerating their transformation into comprehensive financial platforms.

As cryptocurrency exchanges step onto a larger financial stage, direct competition with traditional brokerages has begun. Behind this cross-industry battle, is it an active offense or passive defense? In the traditional brokerage's long-studied home ground, can they still get a piece of the pie?

Entering the new battleground of US stocks, the brokerage business for crypto players is challenging

The brokerage business is being eyed by cryptocurrency players. As the bear market persists, cryptocurrency exchanges are laying out plans for the US stock market, competing with traditional brokerages through different trading paths, and accelerating their transformation into comprehensive financial gateways.

On the surface, this competition arises from differences in user experience. With lower participation thresholds, a 24-hour global trading mechanism, and simplified account opening processes, cryptocurrency exchanges have significantly reduced the entry costs of financial markets, forming certain advantages in reaching retail users. In contrast, traditional brokerages are still hindered by relatively complex account opening processes, capital access requirements, and fixed trading hours, placing them at a relative disadvantage in user acquisition and trading convenience.

This experiential advantage is not enough to translate into real commercial barriers. Once they enter the US stock market, cryptocurrency exchanges will face not a battle for traffic but a highly mature, heavily regulated, low-growth financial system that presents severe challenges in compliance costs, user conversion, and profit margins.

In the crypto world, exchanges have long held absolute dominance, controlling entry traffic, liquidity supply, and pricing power, thus able to earn high trading profits. However, in the US stock market, traditional brokerages' core barriers do not lie in frontend experience but in the underlying financial infrastructure capabilities, including complete licensing and compliance systems, clearing and custody capabilities, institutional client resources, and supporting ecologies like margin financing and market making, which require years of regulatory accumulation, massive capital investments, and trust endorsement. In contrast, while crypto platforms have advantages in trading efficiency and product innovation, their role after entering the US market is more likely to remain as supplementary trading gateways for retail users, making it difficult to become market rule leaders.

The significant rise in compliance costs is another major reality pressure. Cryptocurrency operations around the world remain in a phase of gradually clarifying regulations, retaining some policy flexibility under a framework of financial innovation; however, US stock brokerage operations operate under the world's most mature regulatory framework, strictly adhering to territorial principles and licensing systems, with almost no gray areas. Currently, Coinbase and Kraken are expanding into US stock services through subsidiaries holding brokerage licenses; while Binance, Bybit, Bitget, and other platforms are mainly entering indirectly through collaboration with traditional brokerages or issuers, using channels or distribution models.

From the perspective of user demand, the core users of cryptocurrency exchanges are still primarily focused on cryptocurrency trading, while US stocks play more of a supplementary role for asset allocation and cyclical needs. Therefore, the layout for US stocks is essentially more of a defensive strategy. Moreover, US stock users generally have already opened accounts with traditional brokerages, making migration willingness and costs relatively high. Simultaneously, in a mature market characterized by low volatility and low speculation, the appeal of crypto assets is also relatively limited, further constraining user expansion space.

In terms of profit models, the US stock market has generally entered a stage of zero-commission or low-commission competition, which means that even if cryptocurrency exchanges successfully enter, they are unlikely to replicate their high trading fee models from the cryptocurrency market. At the same time, they must share revenue across multiple levels with brokerages, clearing agencies, and asset issuers, compressing profit margins significantly.

More importantly, this competition is not a one-way infiltration. While cryptocurrency exchanges expand into the US stock market, brokers like Robinhood, Fidelity, and Charles Schwab are beginning to "counterattack" the crypto world, quickly enhancing their crypto capabilities through spot trading, ETFs, custody services, and prediction markets, to capture a new generation of users and incremental funds.

After the era of high commissions ends, brokerage competition enters the asset retention era

Although cryptocurrency exchanges continue to penetrate traditional brokerage businesses, the underlying business logic of both is different.

After bidding farewell to the era of high commissions, mainstream US stock brokerages have generally shifted to a diversified, asset-driven revenue structure, evolving from traditional trading intermediaries into comprehensive financial platforms, thus enhancing their resilience to economic cycles and user stickiness in their profit models.

Taking the latest quarterly report from representative US brokerages Charles Schwab, Interactive Brokers, and Robinhood as an example, the importance of trading commissions is declining, with client assets and the time funds remain becoming the new cores of profitability. In other words, the competition among brokerages has shifted from "who can bring more trades" to "who can retain more assets".

Charles Schwab

The core of Charles Schwab is no longer trading, but asset management and interest income. In the first quarter of 2026, it achieved revenue of $6.5 billion, a year-on-year increase of 16%; net profit reached $2.5 billion, showing significant growth.

Q1 revenue is mainly derived from three segments: net interest income, asset management fees, and trading business. Among them, net interest income reached $3.14 billion, accounting for about 48% of total revenue. This part mainly comes from client cash deposits, margin financing, bank loans, and interest income generated from investment securities portfolios; asset management and administrative fees amounted to $1.76 billion, a year-on-year increase of 15%, accounting for about 27% of total revenue, covering ETF, mutual fund management fees, wealth management service fees, and investment advisory business; trading-related income was about $1.09 billion, accounting for about 17% of total revenue, mainly from trading in stocks, ETFs, options, and fixed-income products; in addition, income from related banking deposit accounts also rose to about $290 million, accounting for about 4.5% of total revenue.

It can be seen that trading income is no longer the core, but has been surpassed by income from asset retention.

In terms of asset retention scale, as of the end of the first quarter of 2026, Charles Schwab's total client assets reached $11.77 trillion, a year-on-year increase of 19%, setting a historical high. The large client assets have brought steadily growing management fee income and also provided a stable source for net interest income. In terms of asset allocation targets, about 52% of client assets are allocated to funds such as ETFs and mutual funds, about 6.6% to fixed-income securities, and stocks and other securities account for about 39%. Diversified asset allocation helps to disperse market volatility risks, thus enhancing the business's cyclical resilience.

It can be said that today’s Charles Schwab resembles an integrated financial institution that combines wealth management platform, bank, and brokerage. Its growth logic is not limited to relying on frequent client trading but instead leans towards relying on long-term asset allocation and asset retention by clients. Even in a sluggish market, management fees and interest income can still provide stable cash flow.

Interactive Brokers

The competitive advantage of Interactive Brokers comes from its trading capabilities covering global markets and the efficient allocation and utilization of funds.

In the first quarter of 2026, Interactive Brokers achieved net operating revenue of $1.669 billion, a year-on-year increase of 17%; pre-tax profit reached $1.288 billion, a year-on-year increase of 22%, with a pre-tax profit margin of as high as 77%.

From the revenue structure perspective, Interactive Brokers' revenue is mainly composed of net interest income and non-interest income. Among them, net interest income was $904 million, a year-on-year increase of 17%, accounting for about 54% of total revenue, making it the company's largest source of income, mainly from client margin financing interest, idle client funds interest, and cash management services. Non-interest income totaled $765 million, a year-on-year increase of 16%, primarily including trading commissions, market data service fees, account service fees, and other business income. Notably, trading commissions amounted to $613 million, accounting for 37% of overall revenue, marking the first instance of surpassing $600 million in a single quarter, and it is the second-largest source of revenue for Interactive Brokers. Other fees and service income (market data subscriptions, bank deposit clearing services, and other account services) and investment and business income (investment gains, forex-related income, and other financial operations) account for about 5% and 4% of total revenue, respectively.

Overall, despite trading commission revenue accounting for 40% of Interactive Brokers' total revenue, net interest income is Interactive Brokers’ most core revenue source, accounting for more than half of total revenue. This indicates that Interactive Brokers' business model is gradually evolving from "trading platform" to "asset management platform," with competitive advantages increasingly coming from a continuously expanding client asset base, gradually retained platform funds, and the resulting stable interest income, leading to a stronger ability to withstand economic cycles.

Robinhood

Unlike Charles Schwab and Interactive Brokers, "retail's stronghold" Robinhood has younger users, higher trading frequencies, and a richer product ecosystem, still primarily focusing on trading income but gradually strengthening its positioning in asset retention business.

In the first quarter of 2026, Robinhood achieved total revenue of $1.067 billion, a year-on-year increase of 15%; net profit was $346 million, up about 3%. Compared to the fourth quarter of 2025, due to the cooling of crypto trading enthusiasm and reduced market volatility, revenue dropped by 17%, and net profit decreased by 43% quarter-on-quarter, yet overall maintained a net profit margin of over 30%.

Robinhood's revenue for the quarter mainly comprises trading revenue, net interest income, and other revenue across three major segments.

Trading revenue was $623 million, accounting for about 58% of total revenue, remaining the largest source of income. Among these, options trading revenue reached $314 million, accounting for about 50% of trading revenue, forming the absolute core profit source; cryptocurrency trading revenue was $134 million, accounting for about 21%, but showed a noticeable decline compared to the previous quarter; stock trading revenue was only $82 million, accounting for about 13%, relatively small. Other trading-related income (including prediction markets, futures, and instant withdrawal services) totaled about $147 million, accounting for about 24%, further enriching the sources of trading income.

This quarter, net interest income reached $359 million, a year-on-year increase of 24%, becoming one of the fastest-growing core businesses for Robinhood. Major sources include interest on idle cash from clients, interest from margin financing, securities lending income, interest on segregated funds, and investment income from the company's own funds. Among these, the cash accounts of users are the largest contributing source, and as the client asset size expands and the interest rate environment supports it, interest income continues to rise, becoming an important stabilizer to hedge trading fluctuations.

Other income this quarter was $85 million, accounting for about 8% of total revenue, mainly from Robinhood Gold subscription, wealth management services, credit cards, and other financial service income. Although relatively small in scale, it has stability and continuous subscription attributes, making it an important part of Robinhood's expansion into comprehensive financial services.

Overall, while trading income still dominates, Robinhood's business model has diversified: on one hand, relying on high-volatility trading products centered around options and crypto assets to obtain traffic and transaction fees; on the other hand, relying on the growth of client cash and margin scale to bring about net interest income, achieving a relatively stable cash flow supplement. In addition, the continuous expansion of new businesses also provides more long-term growth space for the future. However, compared with traditional brokerages, Robinhood's trading income proportion remains relatively high, and the user structure leans more towards short-cycle, high-frequency trading behaviors, thus leading to profitability volatility higher than traditional asset retention brokerages.

The battle for financial gateways, a misalignment in different business paths

Although cryptocurrency exchanges and traditional brokerages compete for the same type of retail user gateway, they fundamentally operate on completely different business paths and profit logic.

At this stage, the core income of cryptocurrency exchanges still concentrates on crypto trading business, with platform attributes still favoring high β trading-type financial intermediaries, whose profitability is highly correlated to market risk appetite and transaction activity.

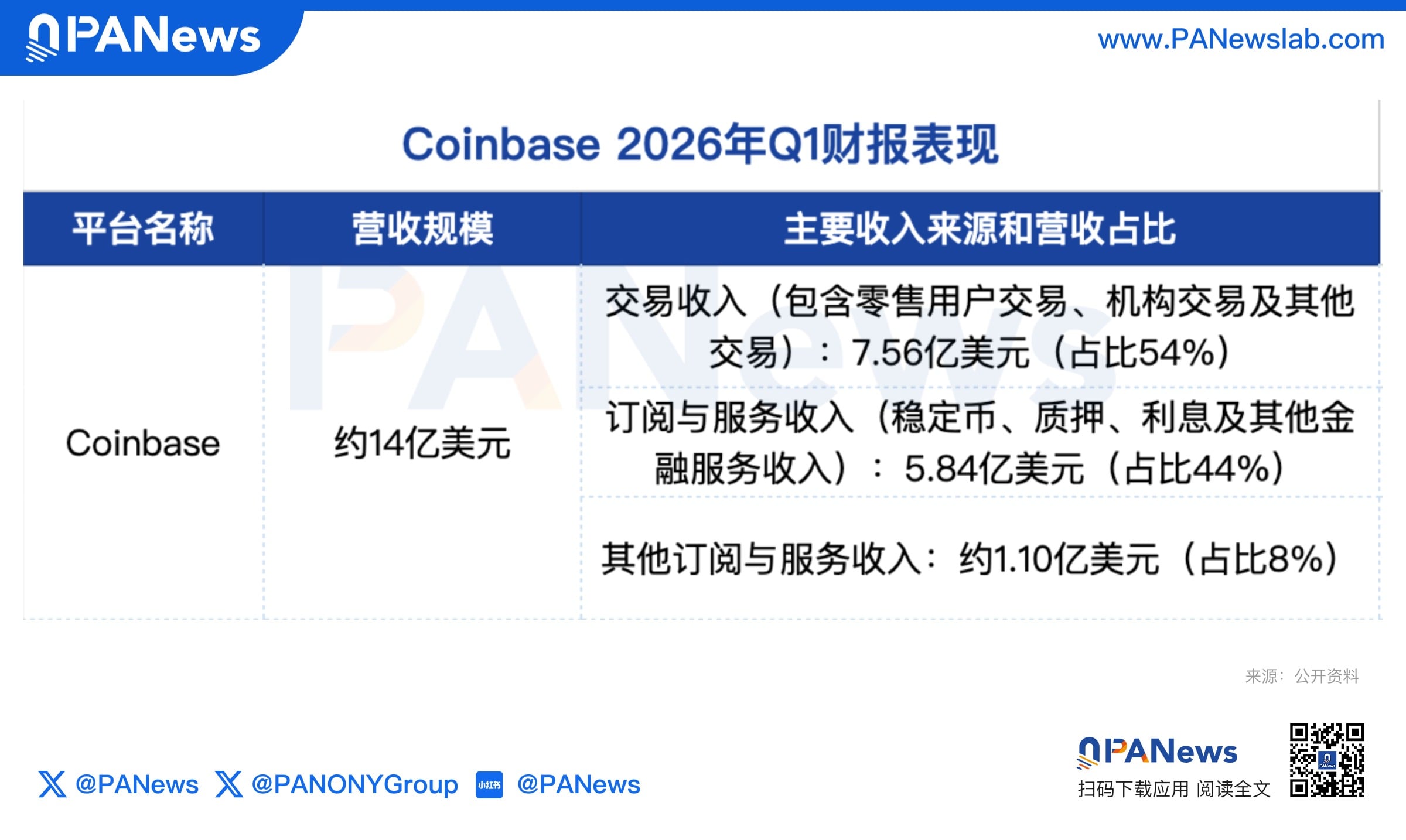

Taking Coinbase as an example, in the first quarter, Coinbase achieved total revenue of about $1.4 billion, a quarter-on-quarter decrease of 21%. Meanwhile, Coinbase recorded a net loss of about $394 million, mainly influenced by the market fluctuations in the cryptocurrency asset portfolio.

From the revenue structure perspective, Coinbase is still focused on trading income. In this quarter, Coinbase's trading revenue was about $756 million, accounting for about half of total revenue, still the core cash source. Among them, retail user trading contributed about $567 million, institutional trading was about $136 million, and other trades about $53 million. However, this portion of income decreased by 40% year-on-year, primarily affected by narrowed price fluctuations of crypto assets, an overall decline in trading volume, and reduced retail trading activity, confirming that its revenue still heavily relies on the cyclical trading behavior of the retail end.

However, subscription and service income is becoming a more stable growth source for Coinbase. In this quarter, this segment accounted for about $584 million, close to 44%. Among them, income related to stablecoins from fund custody and interest sharing was about $305 million, a year-on-year increase of 11%, making it the largest single non-trading income source; staking income was about $101 million, and interest and other financial services income was about $68 million. This segment of business is gradually nearing the scale of trading income, partially hedging against cyclical fluctuations. From a functional perspective, the income from stablecoins and fund custody has certain similarities in mechanism to traditional brokers' cash management and margin financing interest income, both relying on the retention of client funds and generating interest income.

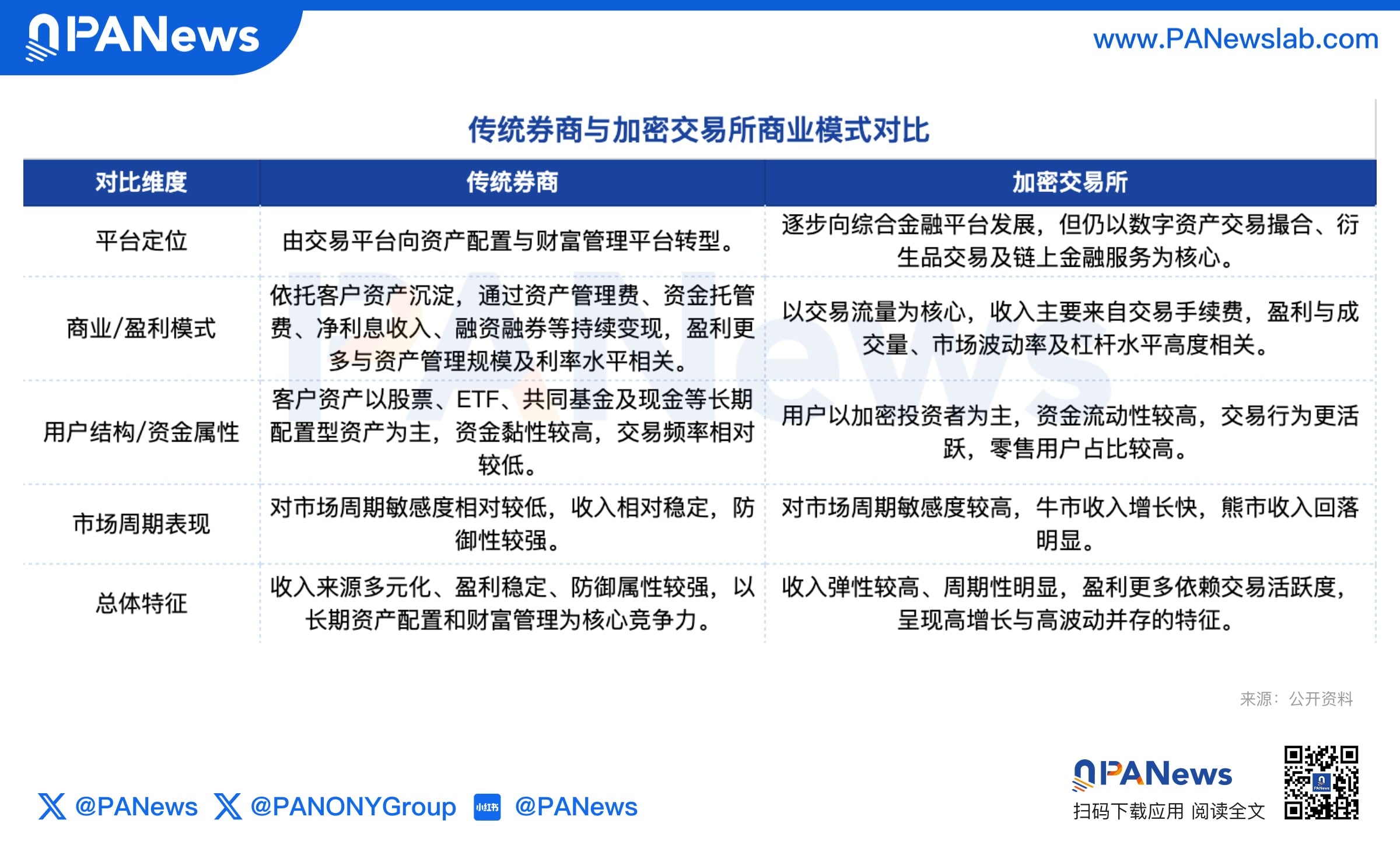

Although cryptocurrency exchanges are gradually aligning with traditional brokerage models, constructing one-stop trading and asset allocation platforms for various asset types, the two still exhibit essential differences in platform positioning, business models, user structures, and profit models, which determine their distinct performance paths in different market cycles.

From the perspective of platform positioning, traditional brokerages are gradually shifting from execution platforms to asset allocation and wealth management platforms, while cryptocurrency exchanges still primarily focus on trade matching and derivatives trading, leaning towards high-frequency trading infrastructure attributes.

From the revenue scale perspective, mainstream US stock brokerages' asset allocation centers around stocks, ETFs, mutual funds, and cash, fundamentally belonging to long-term allocation funds. Once clients complete asset retention, platforms can continuously realize income through asset management fees, fund custody, and interest income. The marginal impact of trading frequency on revenue is relatively limited, with overall profitability more related to asset size and interest rate levels rather than short-term trading activity. In contrast, cryptocurrency exchanges' business models center around trading traffic, with revenue highly reliant on market transaction volume, volatility, and leverage levels; trading behavior itself constitutes the primary source of income.

In terms of market cycle attributes, within a bull market environment, high-frequency trading and leverage expansion can drive cryptocurrency exchanges' revenues to exhibit significant elasticity and amplification effects; however, in bear or turbulent phases, trading activity rapidly contracts, resulting in a simultaneous sharp decrease in revenue. In comparison, the income structure of US stock brokerages is less sensitive to market cycles. Even in a sluggish trading environment, revenues can still rely on net interest income derived from client cash retention, as well as capital intermediary businesses such as margin financing, achieving relatively smooth income support.

Thus, from a business model perspective, traditional brokerages possess stronger defensive attributes, whereas cryptocurrency trading platforms exhibit higher cyclical elasticity and profit volatility.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。