Written by: Chao Xiang Research

As a 175-year-old glass company, Corning has recently made waves in the market.

On June 24, 2026, the day Glass Bridge technology was announced, the A-share CPO sector plummeted over 6%. Funds fled from midstream manufacturers like Zhongtian Technology, FiberHome Technologies, and Yongding Co., Ltd., rushing towards glass substrate concepts. The market identified this as a disruptive technology.

Two months prior, Corning's Q1 financial report showed optical communications revenue of $1.85 billion, a year-on-year increase of 36%, with net profit soaring 93%. The numbers were good, yet the stock price plummeted nearly 9% post-report. The reason was simple: the Q2 guidance was "in line with expectations," not "exceeding expectations."

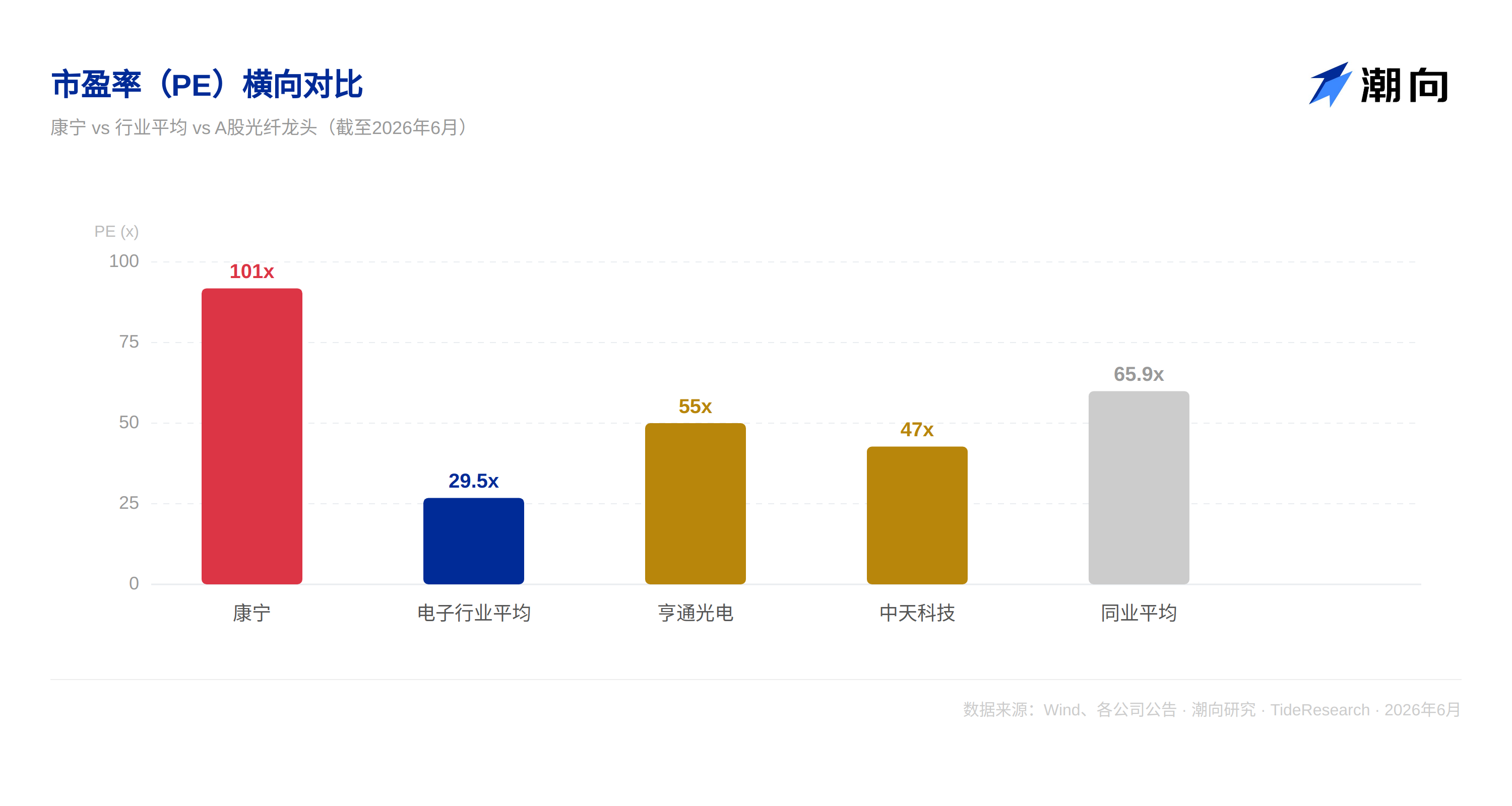

On one side was the frenzy of "disruption," while on the other was the stampede of "meeting expectations." Corning's stock price has risen about 200% from its low at the beginning of the year, with a price-to-earnings ratio exceeding 100 times.

Most people's misunderstanding lies in viewing Corning as an optical module company or a fiber manufacturer, then applying the industry average valuation. The real problem is far more complex than that.

After sorting through public information, we found that it can be explained in three layers.

1. What role does Corning play in the AI industrial chain?

First, let's clarify Corning's position: it is neither an optical module company nor a small fiber manufacturer.

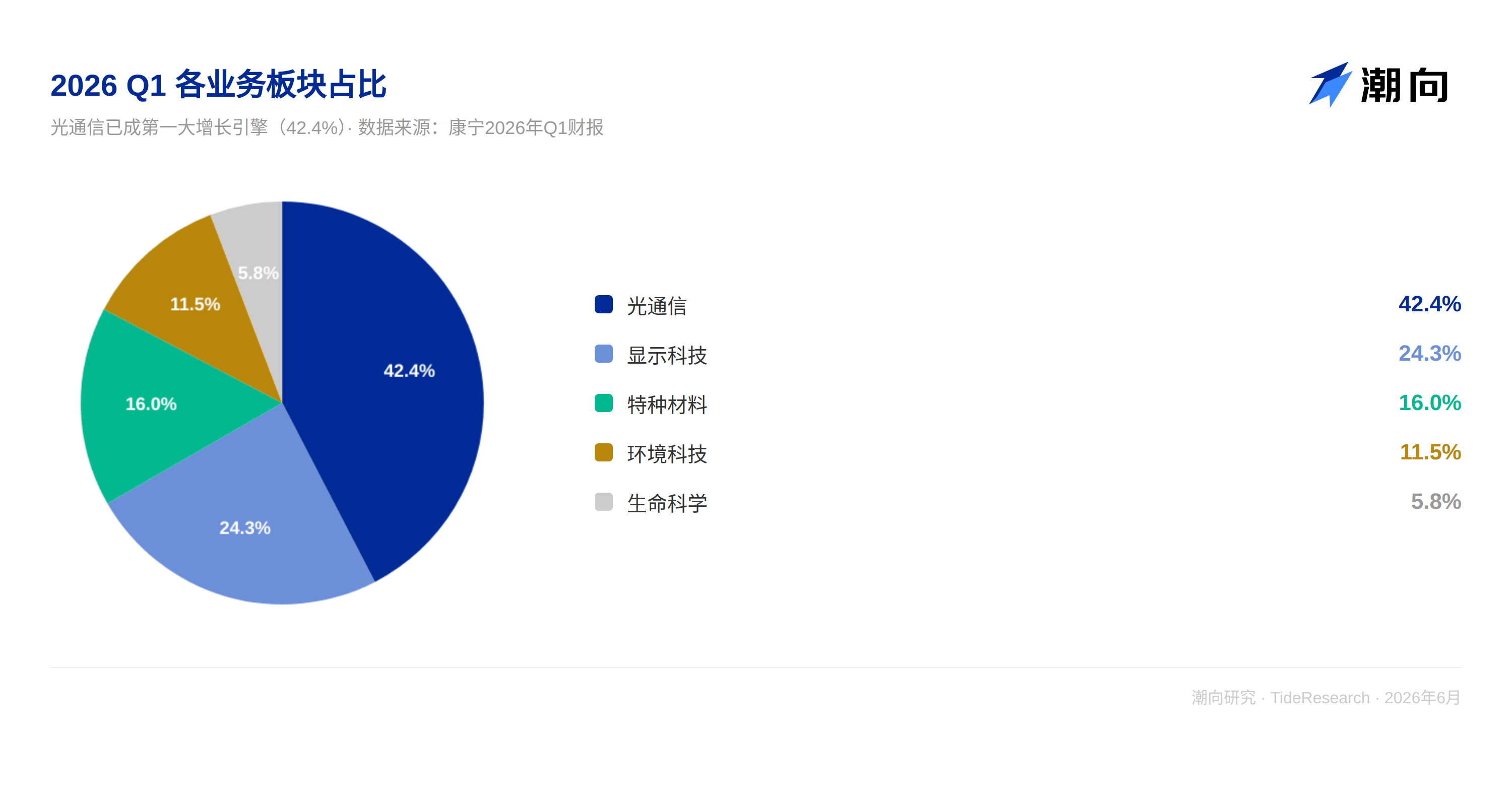

Corning's core role is as the general contractor for the optical fiber infrastructure of AI data centers. As AI models evolve from hundreds of billions of parameters to trillions, the hundreds of thousands of GPUs inside data centers must exchange vast amounts of data over very short distances. Traditional copper cables have become inadequate in terms of bandwidth and energy efficiency. As the inventor of low-loss optical fibers, Corning is centrally positioned in this irreversible technological trend of "optics over copper."

What makes Corning unique is that it doesn't just sell optical fibers; it offers a complete optical connection solution. From optical fibers to optical connectors, from internal data center interconnections to intercity trunk lines, from traditional optical fiber array units to the latest Glass Bridge wafer-level optical interconnects. Management has stated in calls: "We are transforming from a materials company into a systems solution provider."

However, this "system solution provider" faces a set of sharp contradictions. The most certain aspects have already been priced in, while the most valuable aspects have yet to be realized. To clarify this, we divide Corning's value into three layers. The demarcation line is simple: has this money been recorded in the financial reports?

2. First layer: Profits already reflected in the financial reports

Open the Q1 financial report and you can see:

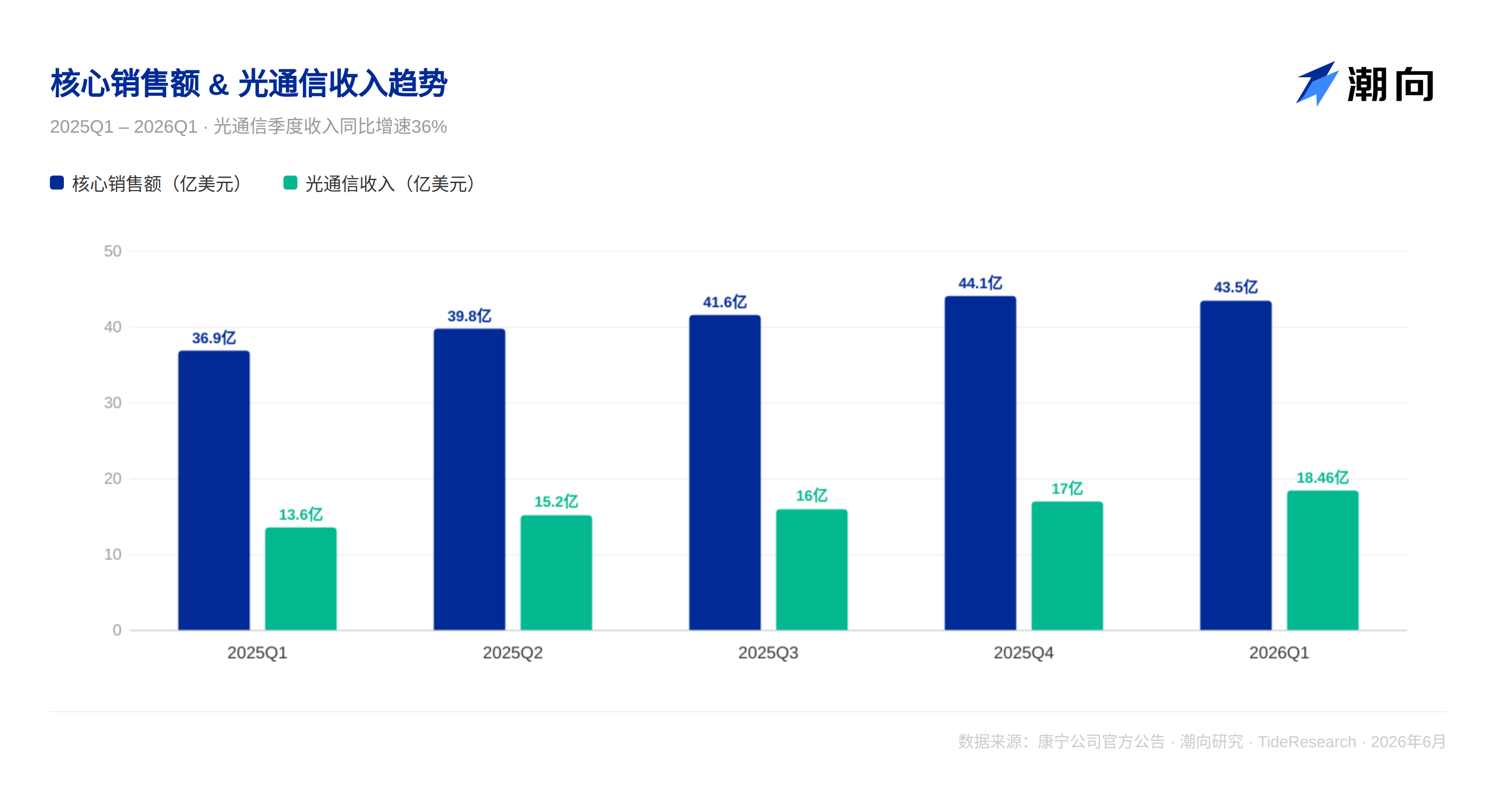

Optical communications are the absolute engine. Revenue of $1.85 billion, a 36% year-on-year increase, with net profit of $387 million, soaring 93% year-on-year. Corporate networks and carrier lines grew simultaneously by 36%, with demand not concentrated on a single customer. Core operating profit margin expanded from 16.3% at the Springboard plan's kickoff to 20.2%. Profit growth far outpaced revenue growth, releasing significant operational leverage.

Customer retention is exceptionally fierce. In Q1, Corning signed a multi-year optical fiber supply agreement with Meta worth up to $6 billion and added two super-scale customers of similar scale to the Meta agreement. On the carrier side, Corning signed and extended a long-term cooperation agreement with Lumen.

The Springboard plan has exceeded expectations. Since its launch in Q4 2023, core revenue has cumulatively increased by 33%, EPS has increased by 79%, and the core operating profit margin has expanded by 390 basis points.

This layer is very solid, and the market has fully priced this part. In fact, it may have been overvalued.

However, no matter how certain the first layer may be, it cannot support a price-to-earnings ratio of 100 times. The real divergence lies in the two layers below.

3. Second layer: Locked in but not yet accounted for

This layer is the most contentious part of Corning's current valuation and the fundamental reason the market is willing to assign a high premium.

NVIDIA strategic partnership. On May 6, 2026, NVIDIA and Corning announced a multi-year strategic partnership. Corning will build three advanced manufacturing plants in the U.S., increasing optical connection capacity tenfold and expanding optical fiber capacity by over 50%, creating more than 3,000 jobs. This is capacity expansion, but more importantly, a shift for Corning from materials supplier to core partner of AI infrastructure.

NVIDIA has the right to invest up to $3.2 billion in Corning, including a $500 million prepaid subscription for 3 million shares and an additional $2.7 billion to subscribe for up to 15 million shares at $180 per share. Corning's CFO explained at the Morgan Stanley conference: "NVIDIA provides billions of dollars in prepayment to support capital deployment and has made equity investments."

Customers are funding the capacity expansion for you. This completely changes the risk structure of capital-intensive expansion. Orders are already locked in, so Corning does not need to build factories first and wait for customers to place orders.

Springboard target upgrade. At the Investor Day on May 6, Corning significantly raised its Springboard target: annual sales of $30 billion by the end of 2028 and $40 billion by the end of 2030. This implies that Corning must more than double over the next 4 to 5 years. Management defines the range of $35 billion to $40 billion as a "high-confidence target."

The COO explained: When the scale of the AI cluster exceeds 130,000 GPUs, a third layer of switching will be added, and Corning's growth will increase by another 50%. The growth rate of corporate business is expected to be 1.3 to 1.5 times that of GPU growth.

This layer supports the core of Corning's valuation premium. However, it’s important to note that the targets of $30 billion and $40 billion are not contracts; a considerable portion of these figures still depends on customers that are "in negotiation" rather than "signed orders."

The market has already baked in a good deal of expectations for the second layer. However, the real shift for Corning from being a "larger optical fiber company" to a "completely different valuation species" lies in the third layer.

4. Third layer: Still being validated, not yet contracted

Returning to the initial scene. On June 24, Corning announced Glass Bridge, and the A-share CPO sector plummeted 6%. What was the market afraid of? What were they excited about?

Glass Bridge forms optical waveguides in glass through wafer-level ion-exchange waveguide technology, enabling direct optical connections between optical fibers and photonic chips. Traditional solutions require precise active alignment of optical fiber array units, while Glass Bridge achieves passive alignment. A single connector supports 24 optical fiber channels, with coupling loss controlled to within 1.5 dB, deeply binding with GlobalFoundries’ silicon photonics platform.

If this technology is mass-produced, the business of traditional optical fiber array unit suppliers will shrink for the long term. This is the reason for the plummet in the CPO sector. Funds voted with their feet, asserting that this marks the beginning of a value restructuring in the industrial chain.

But let’s calmly review several facts.

First, Corning officially positions it as a complement to existing solutions, not a disruption. Traditional optical fiber array units remain effective in current applications, and Glass Bridge caters to incremental demand in scenarios with extremely high fiber counts. The two can coexist in the long term; it’s not a replacement relationship.

Second, mass production and validation will take at least 1 to 2 years. The wafer-level mass production and validation cycle with leading cloud manufacturers will dictate that from 2026 to 2027, mainstream computing hardware will still rely primarily on traditional solutions. Corning is also advancing the research and expansion of the next generation of optical fiber array units.

Third, Glass Bridge is not Corning’s exclusive bet. Chip-level optical coupling involves multiple competing paths, and companies like NVIDIA, Broadcom, and Intel each have differentiated photonic chip solutions, with no unified standard yet. Corning’s Glass Bridge must fit GlobalFoundries’ platform to be effective.

The second layer determines Corning’s revenue growth over the next two to three years, while the third layer determines whether Corning’s valuation system can be rewritten. If Glass Bridge merely sells more connectors within the existing optical module supply chain, it cannot sustain a PE of 100 times. But if it can upgrade from "selling connectors" to "selling optical packaging solutions," the market’s pricing logic for Corning will be completely different. This is the true value of Glass Bridge, as well as its greatest uncertainty.

5. Putting the three layers together: What is the 100 times PE really pricing in?

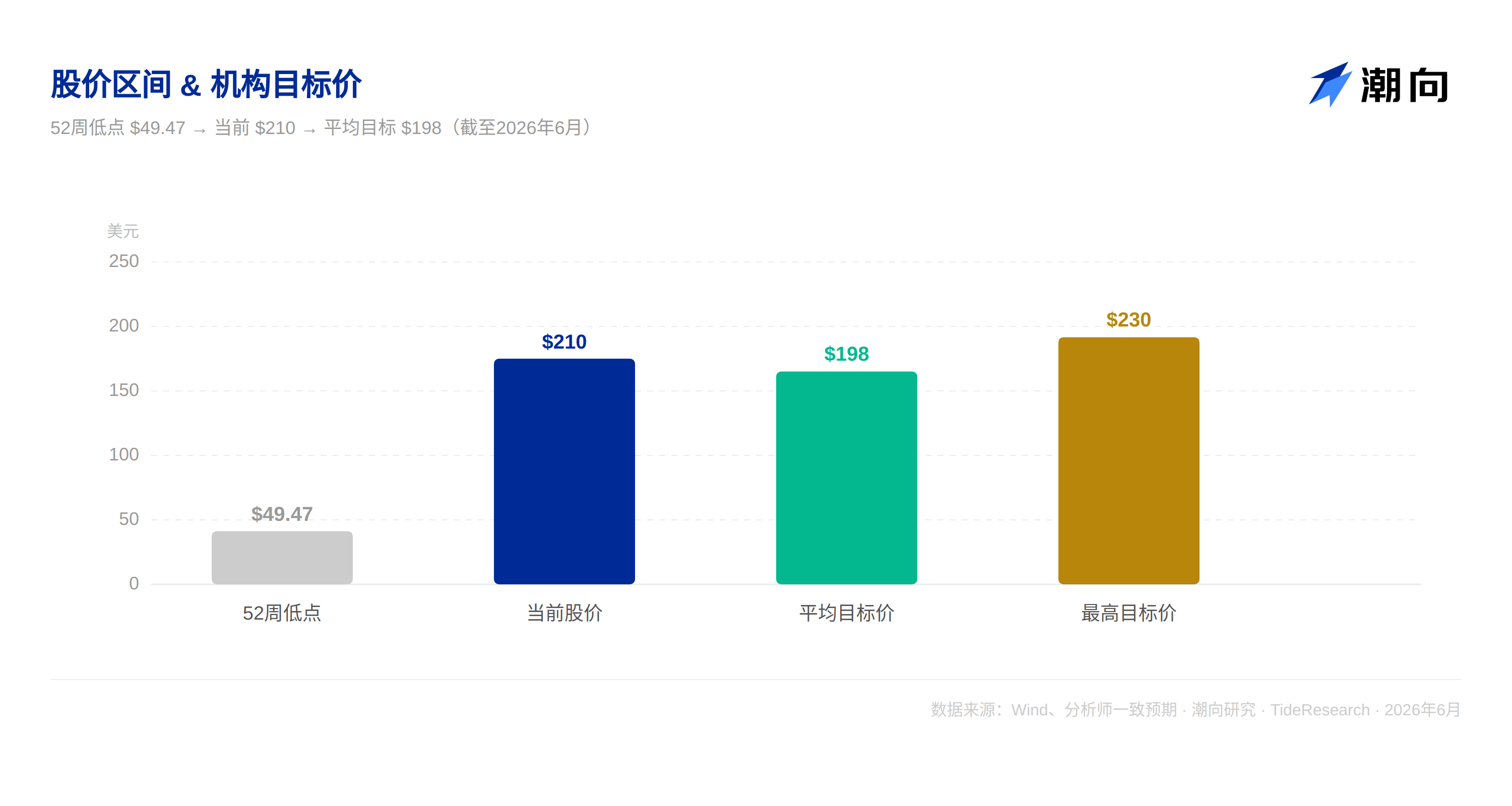

As of late June, Corning’s stock price was around $210, with a price-to-earnings ratio of about 100 times. This valuation level is usually associated with software companies, not capital-intensive manufacturers.

The average target price from 16 analysts is $198, ranging from $149 to $230. UBS raised its target price from $223 to $228 on June 8, while Truist raised from $149 to $205. Morgan Stanley and Barclays provided a target price of $180. Analyst opinions are significantly divergent: 10 rated "buy," 5 rated "hold," and 1 rated "sell."

Looking at the three layers together: the first layer, the existing optical communications business and Springboard has yielded profits that are highly certain and fully priced. The second layer, the NVIDIA partnership for capacity expansion and Springboard targets, has moderate certainty and is partially priced. The third layer, the large-scale commercialization of Glass Bridge, has low certainty, and market sentiment has overreacted.

The conclusion is: if only the certainty of the first layer is considered, Corning is not worth this price. A considerable portion of the current valuation is paying for the second and third layers, and realizing these layers will take at least 2 to 3 years.

6. Don’t be blinded by Glass Bridge

Corning's story is enticing, but amid the optimism, the following risk factors need to be kept in mind.

Technology realization pace. Glass Bridge is a long-term option, not a near-term catalyst. This is the risk that the current market is most likely to misjudge. On the day when the A-share CPO sector dropped sharply, the market had already fully priced in the expectations of "disruption." But Corning has made it very clear: mass production validation will take at least 1 to 2 years. This means that in the financial reports of 2026 and 2027, the revenue contribution from Glass Bridge can almost be ignored. If customer verification progress by 2027 falls short of expectations, the current valuation may face a concentrated clearance of that "technology premium."

Customer concentration. Corning's performance growth heavily relies on a few large cloud manufacturers. If any customer turns to in-house development or seeks alternative suppliers, Corning's orders will face direct pressure. Cloud manufacturers are increasingly inclined to develop their own chips and network solutions. Amazon's Annapurna team, Microsoft's Maia, and Google's TPU are trends that are eating into the traditional supply chain and altering Corning's customers' procurement decision logic.

Geopolitics. Corning faces dual pressures in China. The U.S. may impose stricter controls on high-end technology exports, while local Chinese manufacturers are accelerating their catch-up. All of these threaten Corning's long-term competitiveness in the Chinese market.

Valuation itself. A static price-to-earnings ratio exceeding 100 times has already incorporated many optimistic expectations into the stock price. Following the release of the Q1 financial report, the performance numbers themselves were not bad, but simply because the Q2 guidance was "in line with expectations" rather than "exceeding expectations," the stock price dropped over 10% in pre-market trading and nearly 9% at close. This is the survival rule for high-valuation stocks: you must exceed expectations every time; any "in line with expectations" will be viewed as a negative signal.

7. The story is captivating, but the price is steep

Corning is a company with solid fundamentals and a clear strategic direction. Optical communications continue to grow at a high rate amidst the wave of AI computing infrastructure, NVIDIA's deep integration and Springboard's upgraded targets provide a narrative for long-term growth, and Glass Bridge's technological breakthrough represents a forward-looking industrial direction.

However, a good company does not equate to being a good investment at any time.

A price-to-earnings ratio exceeding 100 times has made Corning one of the most discerning companies in the U.S. stock market regarding "good news" and most sensitive to "bad news" in the AI infrastructure sector. The sharp drop following the Q1 report has already proven this, as a "meeting expectations" report can trigger a nearly 9% decline.

For long-term investors, Corning's positioning in the AI optical communication field, NVIDIA's capital binding, and the long-term option value of Glass Bridge are all worth attention. However, at the current valuation, waiting for a more secure entry point after a pullback may be a more prudent choice. If the stock price returns to the $150–$170 range, the risk-return ratio would improve significantly.

For short-term traders, it’s essential to closely monitor several key points: quarterly order announcements, substantial progress in customer verifications for Glass Bridge, and the phased fulfillment of Springboard targets.

Disclaimer: This article is for analysis reference only and does not constitute any investment advice. The stock market has risks; investors should be cautious. All data comes from public information, and the author bears no responsibility for the accuracy and completeness of the data.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。