Every Monday, Wednesday, and Friday, analyze the market with data reconstruction and seize opportunities with trends, covering macroeconomics, U.S. stocks, precious metals, crude oil, and cryptocurrencies, gaining insights into key global market changes, produced by PANews.

Macroeconomic Market

The United States and Iran reportedly have agreed to cease further military actions and plan to hold talks in Doha, Qatar, on June 30 to discuss navigation issues in the Strait of Hormuz. Just 11 days since the ceasefire agreement led by Trump became effective, the market has shifted back from the extreme scenario of "closing the Strait of Hormuz" to a trading logic of "oil prices returning to fundamentals."

WTI crude oil fell to $68.46, with a weekly decline of nearly 10%, dropping below $70 for the first time since the U.S.-Iran war; Brent crude oil also retreated to pre-war levels. Tariq Zahir, a member of Tyche Capital Advisors, warned that despite the rapid decline in oil prices, the ceasefire agreement remains fragile and the situation in the Strait of Hormuz still holds uncertainties. JPMorgan believes that this round of rapid oil price decline is not due to supply recovery, but rather because the contraction of demand in Asia, especially in China, is far exceeding market expectations.

Spot gold rebounded 1.36% to $4,096 on Friday, but last week it repeatedly fell below the $4,000 threshold, and was observed experiencing the first "death cross" of the "50-day moving average crossing below the 200-day moving average" since September 2023; the strength of the U.S. dollar and rising real interest rates remain the core logic suppressing precious metals.

Additionally, the U.S. Bureau of Economic Analysis (BEA) announced that it will adjust the methodology for three components of the PCE price index—computer software, portfolio management, and legal services—starting September, systematically reducing core inflation. UBS economist Alan Detmeister criticized this move, stating that it lacks transparency and carries risks of political manipulation, pointing out that the revised series appears to be entirely aimed at artificially lowering inflation by skewing the distribution of inflation contributions to the top. Goldman Sachs estimates that the new regulations may lead to a revision of the year-on-year core PCE for May, down by 0.2 percentage points to 3.2%, and a cut in the December 2026 core PCE forecast to 3.0%.

Next, attention should be paid to:

June 30: U.S. and Iranian delegations plan to hold high-level technical talks in Doha, Qatar; whether they can completely resolve the international shipping route dispute in the Strait of Hormuz will directly determine the lifeline of international oil prices.

July 1, 21:30 Beijing time: The European Central Bank's global central bank forum in Sintra, Portugal begins; Federal Reserve Chairman Waller will have his first overseas appearance since taking office, debating alongside Lagarde, Bailey, and McClem. The market should be wary of him releasing tightening and geopolitical risk premiums beyond inflation considerations.

September 30: The new PCE price index statistical methods from the BEA will officially take effect, and the "digital shrinkage" of the core inflation rate will fundamentally reshape the Federal Reserve's future monetary policy game path.

U.S. Stock Dynamics

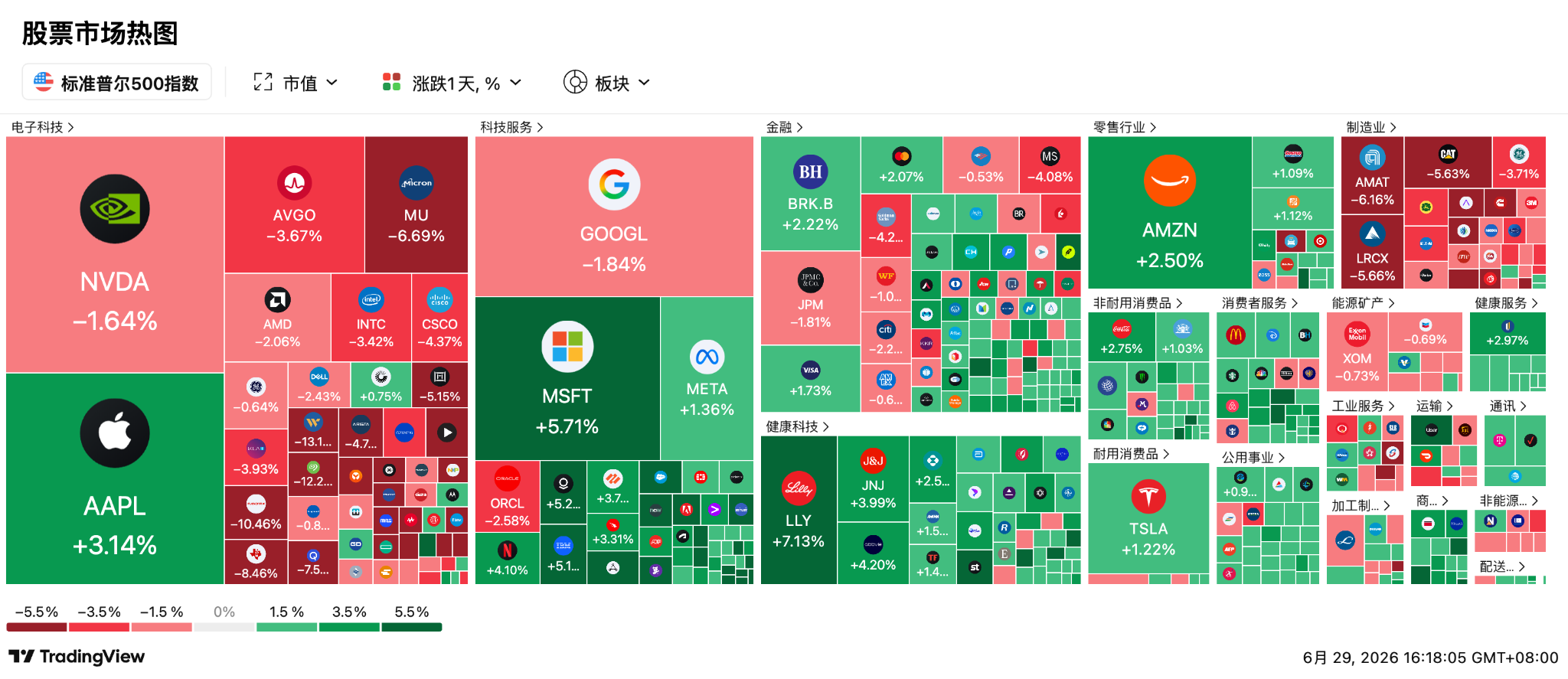

The U.S. stock market struggled to finish flat on Friday, with the S&P 500 index slightly down 0.05%, marking a record streak of five consecutive declines, the longest since August last year; the Nasdaq index fell 0.24%, marking its fifth consecutive trading day of decline, the longest streak since January this year.

The fervor for AI-driven premiums is facing unprecedented liquidity clearance, with hedge funds frantically unloading U.S. tech stocks at the most intense pace in a decade. Goldman Sachs' PB data shows that, for the week ending June 25, the information technology sector encountered extreme selling at a 4-standard deviation level, with a long-short sell ratio of 1.3 to 1; the semiconductor sector faced net selling for eight consecutive trading days, and the seven major tech firms have suffered continuous reductions for five weeks, collectively approaching a three-year low in positions. EPFR data also confirms that after a significant inflow into U.S. tech funds, there was a focused withdrawal of institutional funds last week.

The Philadelphia semiconductor index plummeted 5.3% on Friday, with all 30 constituent stocks declining, among which On Semiconductor fell sharply by 23%, and Qualcomm dropped by 7.57%. Micron Technology, although supported by strong earnings, rose over 4% for the week, but still could not escape a massive decline of 6.7% on Friday under the weight of the broader market, dragging down related memory stocks, with SanDisk falling 10.5%, Western Digital dropping 13.17%, and Seagate Technology decreasing 12.24%. Forex.com analyst Fawad Razaqzada noted that investors have become extremely sensitive to the inflated valuations of AI and the high infrastructure costs within this sector, and expectations seem to have significantly exceeded business realities.

Funds have surged into defensive sectors such as healthcare, utilities, and real estate, with healthcare ETFs and biotech ETFs leading the U.S. stock market. Nationwide's Mark Hackett stated that investor sentiment has weakened due to sharp rotations, but this seems more like a consolidation phase beneath the surface rather than the beginning of a major downturn cycle. Gabelli Funds manager John Belton also believes this is merely a pause rather than a sell-off, and the AI platforms built by major cloud service providers will continue to proliferate in the coming years.

SpaceX (SPCX) triggered Nasdaq's new rules less than a month after its listing and will be historically and rapidly included in the Nasdaq 100 index. JPMorgan estimates that this will lead to a concentration flow of approximately $4.3 billion in passive funds in a short time. However, Morningstar strategists have stated that the stock is significantly overvalued, and S&P Global has also clearly stated it will not follow the trend, waiting at least 12 months before considering inclusion. Additionally, the listing expectations for OpenAI and Anthropic are also heating up, with potential valuations exceeding $1 trillion.

Next, attention should be paid to:

After the close on July 6: $800 billion passive funds tracking the Nasdaq 100 index will begin to focus on allocating SpaceX stocks, which is expected to cause a violent fluctuation in the supply and demand for semiconductor and technology sectors.

Before the market opens on July 7: SpaceX will officially trade as a constituent of the Nasdaq 100.

All of July: The U.S. stock market is entering the "July window," the strongest seasonal period of the year; since 2015, the average return of the Nasdaq 100 in July has reached as high as 4.4%, with a very high historical win rate, likely welcoming a strong reallocation after pension funds readjust.

Cryptocurrency

Bitcoin is experiencing its worst monthly performance since 2022, with less than two days left in June, but the cumulative decline has reached 18.42%, marking one of the largest monthly declines since the bear market of 2022.

Currently, the BTC price is fluctuating around the $60,000 mark, with the market focusing on its rebound potential in July. Since dropping from $120,000, BTC has failed to recover the 200-week moving average (approximately $62,600) for the first time, and has turned that key support level into a resistance level, further increasing the risk of falling to $55,000.

Historically, July is one of Bitcoin's best-performing months, with an average increase of 7.6% since 2013; during midterm election years, the average increase even reaches 10.3%. If historical patterns repeat, the theoretical target for BTC is between $64,500 and $66,100, while an optimistic scenario may challenge $75,000.

Liquid Capital founder Yi Li Hua stated that this current phase is the last major drop of the cycle, predicting that July and August will usher in the most perfect bottom-fishing opportunity for the next three years, with a maximum drop range of $51,000 to $43,000. CrypNuevo pointed out that Monday's market performance is key; stabilizing above $61,000 will confirm a reversal, while breaking below $57,000 could lead to a continued drop to $52,000. The current market is showing extreme oversold conditions, and the daily RSI has appeared with a diverging bottom, making July's trend a critical moment to validate whether bulls can use seasonal effects to reclaim the 200-week SMA (approximately $62,445).

Today's highlights:

SharpLink will be included in the Russell 2000 and 3000 indices, effective June 29

Spain's CNMV issued an emergency warning before the MiCA transition period ends on June 30

0xPPL will stop trading functions from June 6 and fully shut down by June 30

Falcon Finance (FF) will unlock approximately 102 million tokens on June 29, worth approximately $6.9 million

Collector Crypt (CARDS) will unlock approximately 28.84 million tokens on June 30, worth approximately $6.7 million

Upbit 24-hour trading volume ranking: SLX, BTC, XRP, POWER, HUNT

Bitcoin spot ETF: Net outflow of $1.79 billion last week, marking the third-highest weekly net outflow in history

Ethereum spot ETF: Net outflow of $273 million last week, with seven consecutive weeks of net outflow

HYPE spot ETF: Net inflow of $111 million last week

XRP spot ETF: Net inflow of $22.99 million last week

Today's largest gainers among the top 100 cryptocurrencies: VELVET up 8.4%, JTO up 6.8%, 9BIT up 3.9%, NIGHT up 3.5%, FET up 3.3%.

Asia-Pacific Market

The South Korean stock market opened to harsh conditions as storage giants faced relentless pressure; due to a global AI-driven shortage in storage capacity, Aletheia Capital has significantly raised its DRAM price expectations, but the absolute leverage in the market has reached historical highs of 2x-5x. SK Hynix and Samsung Electronics opened under strong liquidation pressure, dropping nearly 5%, dragging the KOSPI index down over 3% during trading.

At a critical moment, the South Korean government and President Lee Jae-myung released positive news, announcing the largest industrial investment plan to date, designating semiconductors, physical AI, and AI data centers as the "three pillars" of industrial upgrade. President Lee Jae-myung announced an investment of approximately 800 trillion won to build four chip factories in the southwest, with each constructed by Samsung and SK Hynix, aiming to double DRAM capacity within five years. Additionally, South Korea plans to invest over 1,000 trillion won in AI data centers by 2035 and spend 81 trillion won to build advanced packaging clusters in the Chungcheong region.

Encouraged by this news, the KOSPI index, along with Samsung and SK Hynix share prices, rebounded simultaneously.

The Japanese market, on the other hand, is supported by consumer recovery. May retail sales grew by 5.3% year-on-year and 1.9% month-on-month, marking the third consecutive month of growth, while wage growth has begun outpacing inflation. Although the Nikkei 225 index ultimately fell by about 0.15%, the logic of consumer recovery remains solid.

The Chinese market has entered a phase of style rebalancing. The Shanghai index rose by 1.16%, the Sci-Tech Innovation Composite Index rose by 3.12%, the Shenzhen Component Index rose by 0.19%, and the ChiNext rose by 0.54%.

Innovative drugs emerged as the biggest winners. The CRO sector surged by 7%, with over 20 stocks hitting the daily limit; Beigene rose by over 10%, Bairi Tiangeng rose by 12%, WuXi AppTec rose by 6%, and Henlius rose by 8%. The National Medical Insurance Administration announced that 557 drugs passed the initial review for the medical insurance catalog, becoming a catalyst for the pharmaceutical market.

Consumer stocks also recovered simultaneously. Kweichow Moutai rose by over 3%, Dongpeng Beverage rose by 10%, and Bairun Co. hit the daily limit. Institutions believe that the stable price of Feitian Moutai indicates that the adjustment of channel inventories is basically over.

Hong Kong stocks notably benefited from the recovery of technology sentiment. The Hang Seng Index rose nearly 2%, the Hang Seng Tech Index soared by 3.23%, and the Hang Seng Biotech Index surged by 7%; Alibaba rose nearly 6%, while Meituan and Baidu rose over 7%, but Lenovo Group fell over 10% against the trend.

Next, attention should be paid to:

June 30, 09:30: NetEase will officially transition to a dual primary listing on the Hong Kong Stock Exchange, which will have far-reaching impacts on the funding structure and valuation system of the Hong Kong tech sector.

June 30: The 2026 China Intelligent Computing Industry Ecosystem Development Annual Conference will be officially held, focusing on the construction of GW-level Token factories, and guidance will be provided on the future direction of speculation regarding cutting-edge AI hardware such as glass substrates and CPO.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。