Written by: Bao Yilong

Following a record-setting IPO, SpaceX's massive $25 billion bond issuance faced intense sell-offs in the secondary market. The aggressive pace of financing for this long-loss-making rocket and artificial intelligence company quickly undermined investor confidence, causing its bond spreads to widen significantly, approaching speculative grade (i.e., "junk") levels.

As of Friday, SpaceX corporate bonds transitioned from "hot demand" on the books to a full-blown collapse within just 48 hours of pricing.

The sell-off pressure on SpaceX's bonds across various maturities led to a cumulative book loss of approximately $400 million compared to U.S. Treasuries, erasing the narrowing gains made by underwriters during the subscription phase due to the declines in long-term bonds.

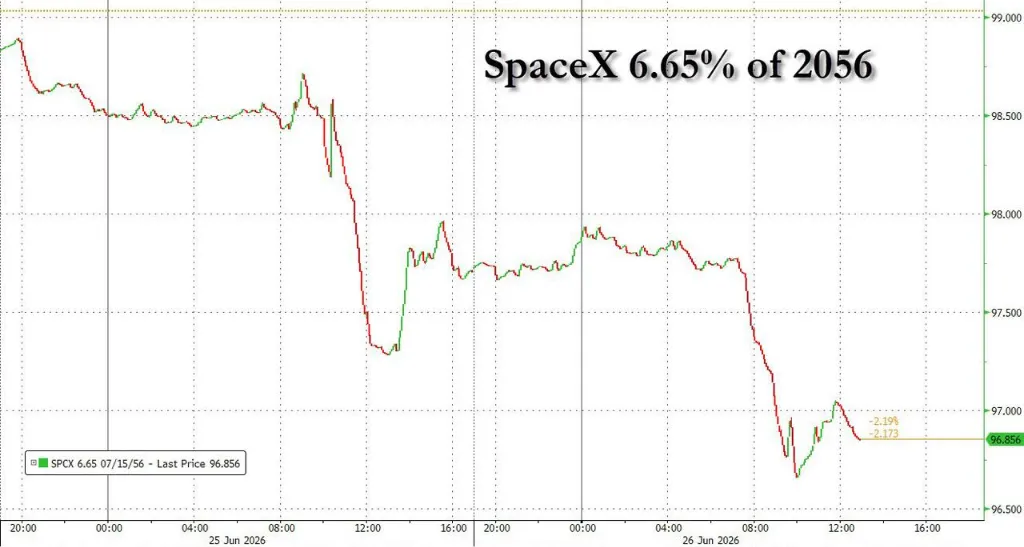

According to MarketAxess data, the yield on SpaceX's 10-year bonds rose to nearly 6%, with spreads over U.S. Treasuries widening to more than 1.6 percentage points. The spreads on its long-dated bonds maturing in 2046 and 2056 soared to 1.93 and 2.01 percentage points, respectively.

According to Ice Data Services, the average spread pricing for BB-rated "junk bonds" in the market is currently 1.67 percentage points, indicating that SpaceX, which has a Baa1/BBB investment-grade rating, is trading significantly worse than some junk-rated issuers.

The magnitude and speed of the collapse shocked traders in the fixed-income market. Market participants pointed out that in recent large bond issuances, there have been nearly no precedents for spreads to widen to such an extent so quickly.

"Perfect Storm" Hits the Secondary Market

The initial book data for SpaceX's bond issuance temporarily masked potential risks.

According to Bloomberg, the deal initially received close to $90 billion in subscription orders, nearly four times oversubscribed, leading to an expansion of the issuance scale from $20 billion to $25 billion.

However, traders revealed that this frenzy was mainly driven by fast money seeking short-term arbitrage, rather than traditional buy-and-hold investors. When these funds attempted to quickly take profits in the secondary market, selling pressure surged.

Tony Trzcinka, portfolio manager at Impax Asset Management, indicated that the market had anticipated a widening of SpaceX's spreads, but the current magnitude is nothing short of a "perfect storm."

He pointed out that this stems from the significant shrinkage of the company's market value since its IPO, the technical pressure from the enlarged issuance size, and the confusion among investors on how to price its unique risk profile.

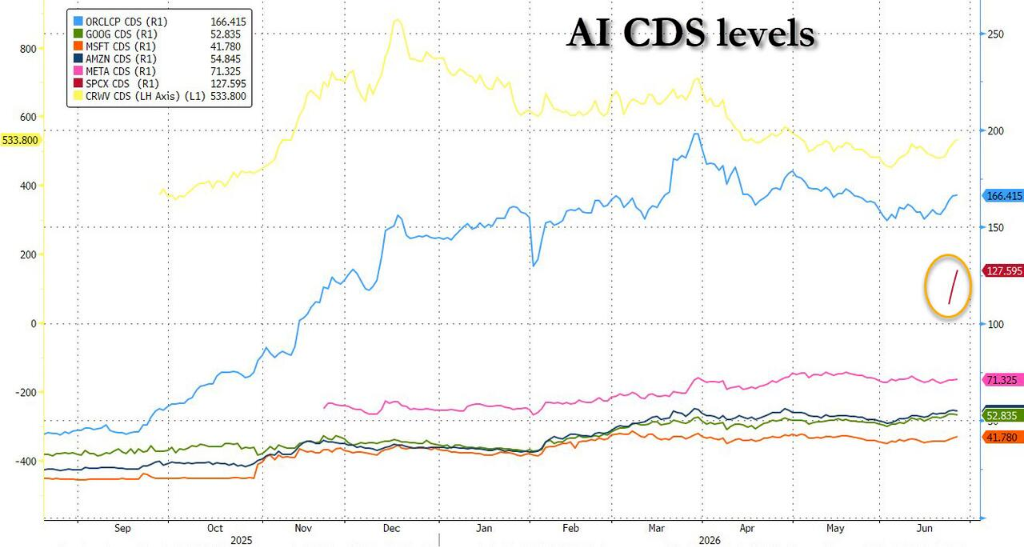

In contrast, Nvidia, which recently completed a $25 billion bond issuance, only saw its long-dated bond spreads widen by 11 to 12 basis points, while Alphabet's long-dated bond spreads even narrowed.

Furthermore, SpaceX's credit default swaps (CDS) also widened significantly after trading began, further confirming the market's defensive stance on its credit condition.

Cash Flow and Governance Risks Raise Immediate Concerns

There is a fundamental divergence in the evaluation logic between equity and bond investors regarding SpaceX.

The company raised $86 billion through its IPO earlier this month, with its valuation peaking at nearly $3 trillion before falling back to $2 trillion, largely based on expectations of a future surge in its AI revenues.

However, for creditors, the core fact is that while SpaceX is projected to achieve $18.7 billion in revenue by 2025, it will still post a net loss of $4.9 billion. PGIM portfolio manager Michael Campion stated:

In the investment-grade bond market, we focus on whether a company can repay its debts, as we are accustomed to lending based on actual cash flow rather than projections.

Allianz Chief Investment Officer Ludovic Subran also candidly noted:

Bond investors are different from equity investors. Equity investors might follow you to Mars, but bond investors will only ask, 'Where's my coupon?'

Additionally, the extreme reliance on Musk's personal leadership has become a core concern for rating agencies and investors. Fitch Ratings views this as a "critical rating constraint."

London Business School professor James Dow pointed out that SpaceX is currently overly reliant on Musk and lacks a succession plan, with its corporate governance being exceptionally weak, which significantly diminishes the attractiveness of its long-term debt.

The Wave of Bond Issuance from Tech Giants Approaches "Bubble" Limits

SpaceX's chilly reception is not an isolated incident; rather, it exposes the systemic risks of debt expansion among tech giants.

As tech companies compete to raise massive sums to fund AI projects, investors face a large-scale bond supply shock.

According to Morgan Stanley data, the volume of debt issuance related to AI has reached $236 billion this year, a 357% increase year-on-year, and is expected to double to $570 billion by year-end.

The borrowing frenzy is rapidly driving up the industry's leverage ratio. Data shows that the total leverage ratio of mega-cap tech companies has doubled from 0.9 times to 1.8 times in just over two quarters, surpassing the total leverage ratio of the entire energy sector.

This enormous supply is weighing down market structure; Bloomberg calculations show that as of Wednesday, the investment-grade bond supply in the U.S. for June has reached $180 billion, setting a historical high.

Oversupply has begun to drag down broader credit spreads. Morgan Stanley noted that spreads for super-large issuers are widening overall, with the bonds of Oracle and Meta confirming this trend.

Mark Dowding, Chief Investment Officer of Fixed Income at RBC BlueBay Asset Management, stated in a report that bondholders are clearly concluding that as this loss-making company finances its path to future profitability, there may be a significant amount of debt issuance ahead.

Analysis suggests that if this pace of debt expansion continues, credit spreads will ultimately explode further, thereby imposing substantial constraints on tech companies' capital expenditure cycles.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。