The Federal Reserve's hawkish tone continues to suppress market sentiment for gold. Following an initial fall below $4,000 per ounce on June 24, spot gold once again fell below the psychological threshold on June 25. Since reaching a historic high of nearly $5,600 per ounce at the end of January this year, gold prices have retraced about 29%.

The market generally attributes the current downturn to the more hawkish policy signals released by the Federal Reserve. Against the backdrop of rising expectations for prolonged high interest rates, the attractiveness of dollar assets has increased, significantly squeezing the allocation value of gold as a non-yielding asset.

However, Asymmetric Research offers a different perspective, arguing that it is inaccurate to simply equate interest rate hikes with weakening gold prices. The institution points out that historical experience shows that the key variable determining gold's mid- to long-term trend is not the absolute level of nominal interest rates, but whether the Federal Reserve can effectively control inflation and whether the economy has the foundation to return to strong growth.

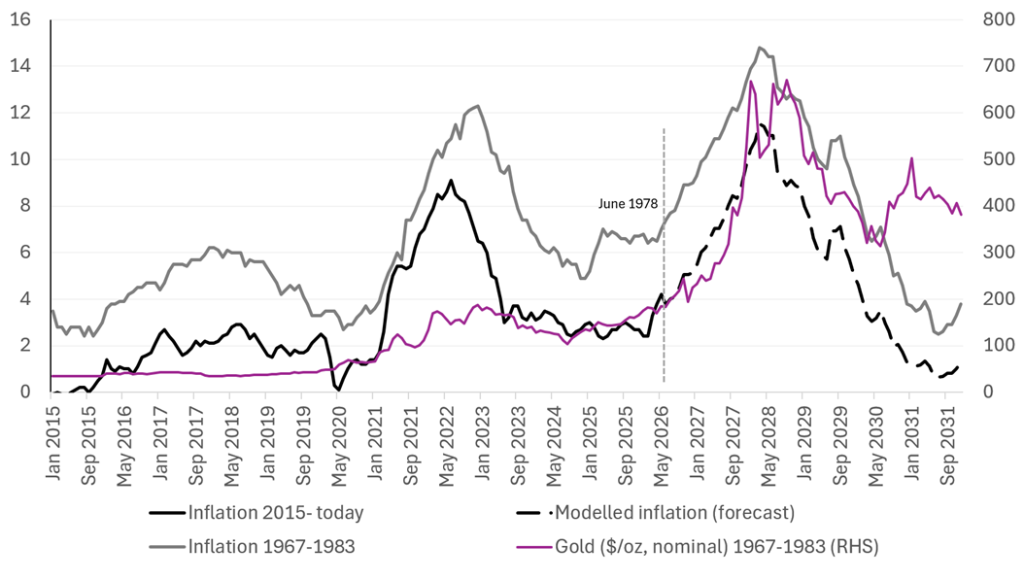

Within its analytical framework, the current macro environment is closer to 1978—the eve of the last inflation cycle escalation in the 1970s and the opening of a new bullish trend for gold. Anchoring to this historical coordinate provides an important reference for assessing the current trend in gold prices.

1970s Experience: Gold Rose in Sync with Interest Rates

For a long time, investors have widely believed that rising interest rates increase the opportunity cost of holding gold, thereby suppressing gold prices.

However, Asymmetric Research points out that the history of the 1970s does not support this view. During that time, while U.S. interest rates consistently rose, gold prices remained on an upward trend for most of the time.

The agency analyzes that the periods during the 1970s when gold experienced significant pullbacks primarily occurred after the Federal Reserve's interest rate hikes led the economy into recession. Even so, gold's average pullback was about 19%, and it typically resumed upward movement around four months later.

The two phases that truly ended the gold bull market occurred from 1975 to 1976 and after 1983. Both of these periods shared a common background: the market believed the Federal Reserve had successfully defeated inflation, and the economy entered a strong expansion phase. For example, U.S. GDP growth exceeded 5% in 1976; from 1983 to 1993, the average growth rate of the U.S. economy was over 4%.

Current Environment More Similar to 1978, Not the Start of a Gold Bear Market

Asymmetric Research believes that the current U.S. economic environment bears a high similarity to the late 1970s.

The agency's report indicates that the current U.S. Consumer Price Index (CPI) trend may be replicating the pathway of the late 1970s. If historical correlation continues to hold, the current phase may be similar to 1978, just before the final round of accelerating inflation and the subsequent rise in gold prices.

In this scenario, gold is not in a long-term bear market, but may be in an adjustment phase before the next round of increases. The research firm believes that the current market is overly focused on changes in interest rates, while underestimating the persistent nature of inflation and the fiscal pressures that may limit future monetary policy.

In the Era of High Debt, the Federal Reserve's Rate Hike Space is More Limited

Asymmetric Research notes that compared to the 1970s, the current U.S. financial system has a significantly lower capacity to withstand high interest rates. The reason lies in the fact that the ratio of U.S. federal debt to GDP has now reached 3 to 4 times that of the 1970s, while the ratio of fiscal deficit to GDP is also higher.

This means that even if the Federal Reserve wishes to control inflation through continued interest rate hikes, the pressure of high rates on government financing costs, economic growth, and financial market stability has become more pronounced. The research institution believes that the current environment does not possess the conditions, unlike the early 1980s, for a thorough end to the inflation cycle through drastic tightening policies.

Gold Pullbacks May Provide Buying Opportunities

Despite the recent rapid decline in gold prices, Asymmetric Research maintains a bullish outlook. The institution's baseline scenario suggests that further downside for gold prices is limited, and the recent market sell-off may present a buying opportunity for long-term investors.

Based on historical retracement data for gold over the past 30 years and over 50 years, the agency believes that the price bottom for gold may be around $4,000. Specifically, calculating from the median of the largest pullbacks in the past 30 years, a reasonable bottom for gold is about $4,030 per ounce; if referencing the past 50 years, in extreme cases, it may decline to $3,640 per ounce.

In other words, even if gold continues to adjust, the space for further declines may now be relatively limited.

The Next Gold Market Cycle Depends on Inflation and the Dollar's Direction

The previous bull market for gold was mainly driven by central bank purchases, geopolitical risks, and inflation concerns. Recently, the rebound of the dollar and the Federal Reserve's shift to a hawkish policy have put pressure on gold. However, Asymmetric Research believes that if inflation proves hard to subside quickly in the future and the Federal Reserve is constrained by the high debt environment, then gold may still see the onset of a new upward cycle.

In the agency's view, the current market is repeating the critical juncture of 1978: investors are selling gold under pressure from short-term interest rates, but what truly determines the long-term trend is whether U.S. inflation will spiral out of control again and whether U.S. monetary credit will continue to be challenged.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。