Author: Oluwapelumi Adejumo

Translation: Deep Wave TechFlow

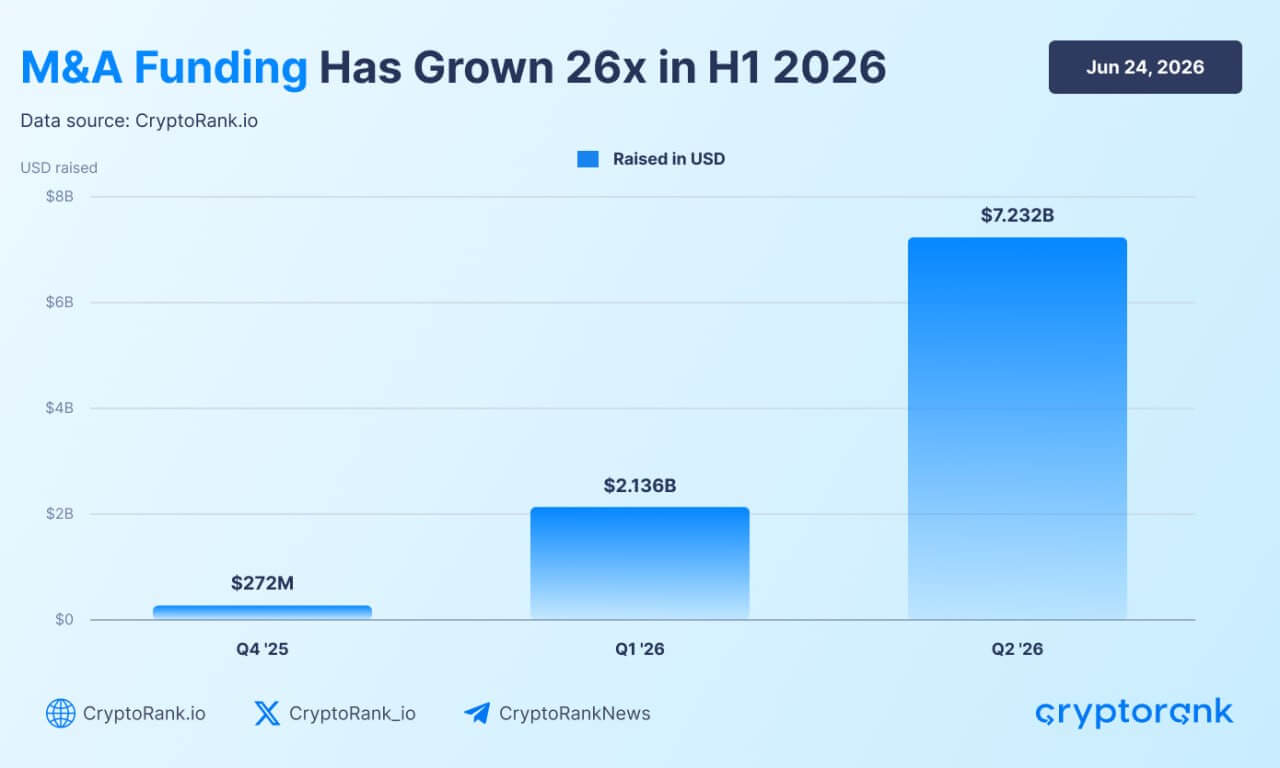

Deep Wave Introduction:The continuous decline of BTC is forcing crypto companies to lay off workers on a large scale, but it is also giving rise to the most aggressive merger and acquisition wave in the industry's history — the transaction volume reached $9.4 billion in the first half of 2026, which is 26 times that of the same period last year. Traditional financial institutions are no longer building infrastructure themselves but are instead directly purchasing licenses, custody, and payment rails, revealing the real flow of capital during this bear market.

The long-term decline of Bitcoin is compelling cryptocurrency companies to lay off employees, automate more tasks, and abandon the expansion plans set during the previous bullish market. At the same time, this has also created one of the busiest acquisition periods in the history of the industry.

In the second quarter of 2026, cryptocurrency merger and acquisition transactions reached $7.23 billion, up from $2.14 billion in the first quarter.

The total transaction volume for the two quarters reached $9.37 billion. According to CryptoRank, the overall growth for the first half of the year is 26 times that of the same period last year, highlighting that even as spot market conditions deteriorate, trading activity is accelerating sharply.

This acceleration occurs against the backdrop of Bitcoin trading prices nearing a two-year low, and some of the industry's largest employers continue to lay off employees.

This divergence shows the direction of capital flows during a downturn — companies are reducing spending on broad hiring and speculative growth.

In contrast, traditional financial institutions, banks, card networks, trading companies, and crypto firms with ample funding are acquiring payment systems, regulatory licenses, custody services, and market infrastructures that would take years to build internally.

The result is that a bear market has weakened many crypto companies, but it has not eliminated institutional demand for their technology.

Traditional Finance Drives Wave of Crypto Infrastructure Acquisitions

Traditional financial institutions are driving the wave of crypto acquisitions by opting to purchase fully mature digital asset infrastructures rather than building compliant and technological systems from scratch.

Banks, payment processors, and fintech companies are actively targeting startups that already possess custody solutions, payment rails, and regulatory approvals.

This acquisition frenzy is largely driven by stabilizing global policies. The EU's Markets in Crypto-Assets (MiCA) framework establishes unified licensing standards, while ongoing U.S. stablecoin legislation gives corporate giants confidence to make long-term bets.

Legal and consulting experts note that this policy support is a major catalyst. According to Architect Partners' first-quarter crypto M&A financing report, the banking and securities industries are fully embracing blockchain and repositioning the technology as the foundational layer of traditional financial markets.

Mastercard's $1.8 billion acquisition of the stablecoin company BVNK is a typical example. This acquisition allows the card network to acquire the technology and licenses needed to process stablecoin payments immediately, bypassing years of internal development.

Other Wall Street giants are also ensuring strategic positions through targeted investments. Intercontinental Exchange backs the prediction platform Polymarket, Citadel Securities invests in brokerage service provider Alpaca, and Standard Chartered's venture arm funds market maker Keyrock.

Asset management firms are also capturing institutional demand through direct acquisitions. Franklin Templeton, managing $1.7 trillion in assets, recently launched a dedicated digital asset department called Franklin Crypto.

This initiative was achieved through the acquisition of 250 Digital, which absorbed the company’s investment team and the liquidity crypto strategies previously managed under CoinFund to provide actively managed cryptocurrency products directly to Franklin Templeton's global client base.

Overall, private capital is heavily favoring businesses that connect blockchain to the broader financial system. First-quarter financing data shows that investors clearly prefer the practicality of stablecoins, such as foreign exchange, corporate payments, and cross-border settlements, over speculative native crypto projects.

In this environment, regulatory qualifications have become a key competitive barrier. Acquisition targets with broker-dealer capabilities, federal banking licenses, or registered investment advisor qualifications, including Alpaca, Anchorage, and Superstate, attract stronger buyer interest because they provide immediate legitimate operational licenses for acquirers.

As traditional finance showcases its balance sheet strength, blockchain networks are quietly becoming a new class of aggressive buyers.

Historically, layer one and layer two networks relied on independent developers to build applications on their chains. Now, faced with fierce user competition, these networks are directly purchasing consumer-facing applications.

Polygon's recent acquisitions of Coinme and Sequence highlight this shift. By acquiring payment channels and wallet infrastructure, the blockchain is ensuring its end-to-end user experience and locking in transaction volume, indicating that mere technical capability is insufficient to maintain market share.

Crypto Layoffs Intensify, AI and Compliance Reshape Workforce

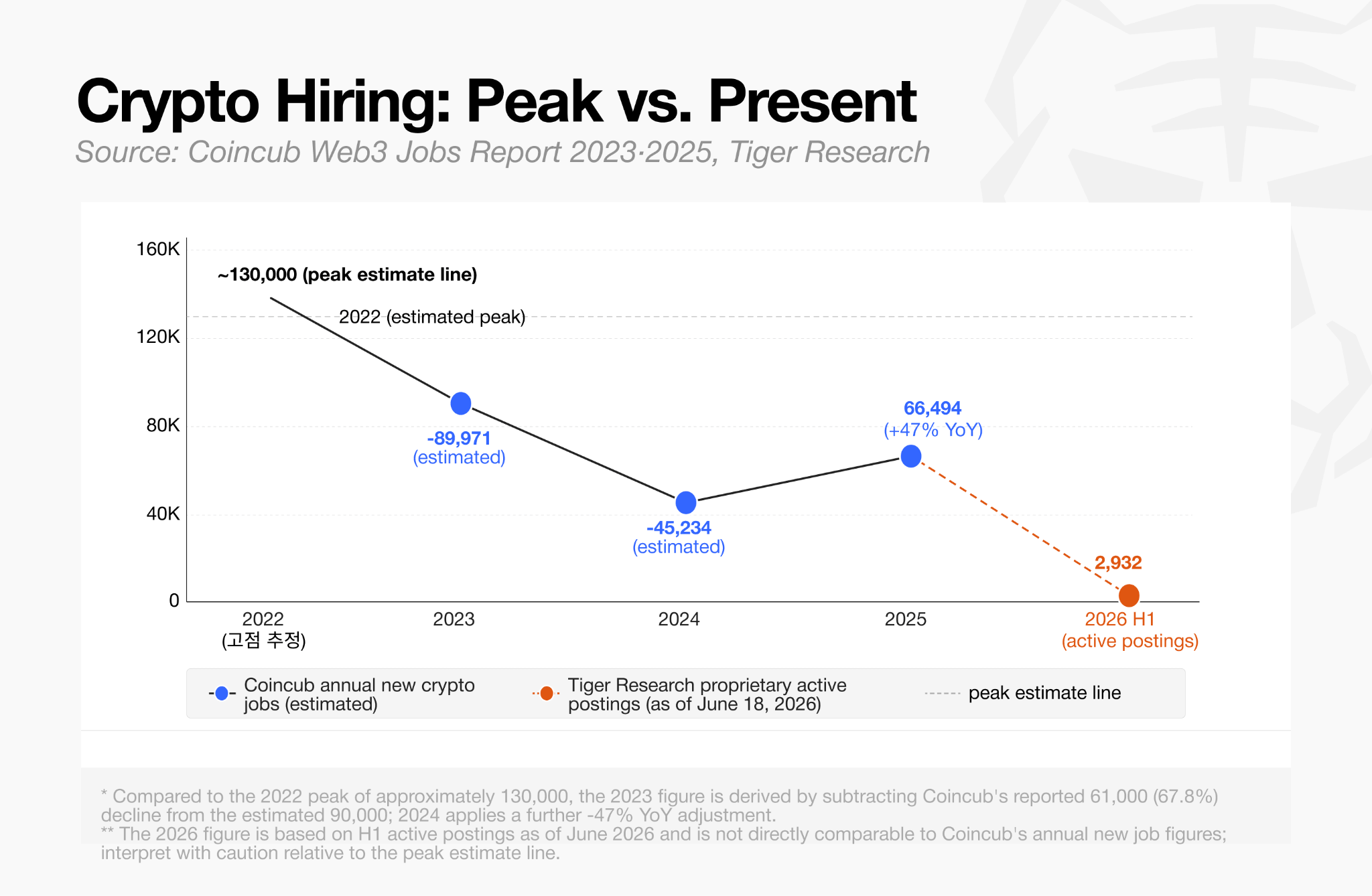

The pace of corporate acquisitions stands in stark contrast to the continuing shrinkage of the digital asset labor market.

According to June 2026 data compiled by Tiger Research, there are currently only 2,932 active job vacancies globally in the industry.

This number is far below the aggressive hiring spree seen in early 2021 and 2022 when trading platforms, decentralized finance protocols, and NFT markets were all expanding their workforce simultaneously.

Job shrinkage began during the market downturn in 2022 and accelerated after the FTX collapse, resulting in a nearly 40% decline in vacancies in North America and Europe. The market has yet to rebound to previous highs.

In fact, layoffs have been steadily ongoing in the first half of this year. Major platforms including Gemini, Coinbase, Kraken, Algorand, Crypto.com, and most recently, the Ethereum Foundation have all initiated a new round of layoffs.

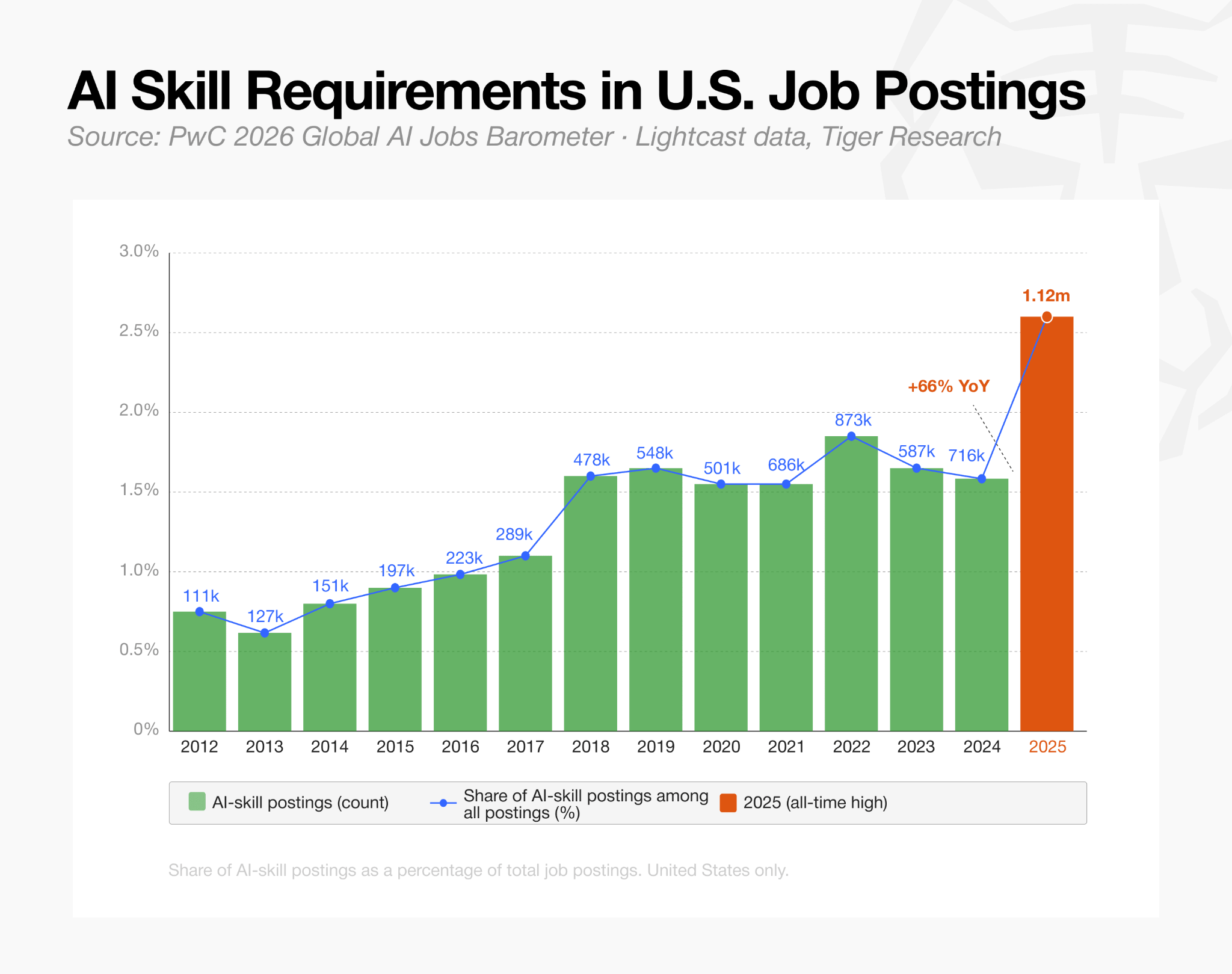

Executives attribute the layoffs to low token valuations, broader macroeconomic pressures, and AI-driven operational efficiencies. Specifically, Coinbase has explicitly framed its restructuring as a transition to an "AI-native" operating model.

This technological shift is evident in hiring data: the proportion of crypto jobs requiring AI skills has more than doubled in a year, soaring from 23% in early 2025 to over 53% by March 2026.

While overall hiring remains sluggish, the composition of the workforce is undergoing a fundamental change. Companies are not implementing a broad hiring freeze. Instead, they are actively narrowing their focus to technology and regulatory expertise.

According to Tiger Research, engineering roles account for about 34% of active vacancies, while legal and compliance positions make up about 10%. This shift is even more pronounced in centralized exchanges, where compliance roles account for 16% of vacancies, over twice as much as sales and business development roles.

This indicates that these companies are prioritizing staffing for licensing, risk management, and maintaining core infrastructure while reducing spending on marketing and community growth.

Moreover, the limited hiring that is taking place is heavily concentrated in a few heavyweight firms rather than spread across early-stage startups. Centralized exchanges generate nearly a third of all job vacancies.

Stablecoin and payment sectors account for another significant portion, but this activity is highly concentrated; Tether and Ripple alone account for over 80% of the listings in this category.

Ultimately, the data paint a picture of targeted corporate restructuring and a defensive stance rather than a broad recovery in the labor market across the industry.

Struggling Crypto Firms Become Acquisition Targets

Blockworks' recent acquisition of Messari perfectly illustrates the intersection of mass layoffs and accelerated consolidation.

The crypto analytics firm Blockworks acquired the analytics provider for about $10 million, a significant drop from its $300 million valuation following financing in 2022. Prior to this sale, the research company experienced three separate rounds of layoffs starting in 2023.

Shorter funding runways and slow revenue growth are forcing smaller businesses to the negotiating table, allowing well-funded buyers to absorb specialized talent, proprietary data, and distribution channels at a fraction of their former private market valuations.

Industry analysts expect these financial pressures to soon extend to the digital asset treasury sector. Throughout 2025, many publicly traded treasury entities successfully raised funds by trading at a premium relative to their cryptocurrency reserves.

Meanwhile, the acquisition wave may ultimately also encompass decentralized autonomous organizations, aided by a maturing legal framework.

Recent legislative advances, such as Wyoming's decentralized nonprofit association (DUNA) structure, provide DAOs with a recognized legal mechanism to hold off-chain assets and intellectual property.

With clearer governance and ownership, protocol treasuries are better able to acquire complementary software projects or specialized development teams.

However, compared to the traditional, compliance-driven corporate acquisitions dominating the current market cycle, these decentralized mergers remain highly experimental.

Capital Remains Available but Has Become Selective

Despite cryptocurrency trading activity approaching $10 billion in the first half of 2026, capital allocation has become more selective.

A notable exception to this strict institutional focus is the prediction market space. Event betting platforms have received substantial financing commitments as they vie for mainstream dominance.

For context, Kalshi is reportedly negotiating a funding round that would value the federally regulated exchange at $40 billion, nearly double its previous $22 billion price tag. Polymarket has also attracted significant support as competition for prediction market dominance heats up.

However, outside of predictions, venture capital arguments have narrowed significantly. Capital overwhelmingly flows to companies that serve as bridges between digital assets and traditional financial systems.

Tokenization companies and institutional trading venues receive large checks as they promote sustainable, insulated revenue models: charging regulatory service fees to banks, brokerages, and asset management companies rather than relying on volatile retail crypto traders. Superstate recently closed a $82.5 million funding round to expand its blockchain-based securities issuance, while Alpaca leads in the settlement of tokenized U.S. stocks and exchange-traded funds.

This funding trajectory indicates that investors are shifting their bets from conceptual tokenization pilots to real-time, regulated financial products.

Notably, purely decentralized finance protocols and experimental layer one blockchains are entirely absent from this quarter's significant financing.

This selective deployment of venture capital reflects broader M&A trends. Liquidity is present, but it is earmarked for startups with regulatory licenses, institutional distribution channels, and tangible utility for traditional finance.

The bear market is effectively pruning the industry, forcing weaker models to consolidate or lay off workers, while richly rewarding those infrastructure providers that have been built to weather the crypto winter.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。