At the age of 100, Alan Greenspan passed away, leaving behind the "put option" myth and the principle of "don’t fight the Fed," which dominated the market for thirty years. Just days before his passing, the newly appointed Chairman Kevin Warsh quietly initiated a comprehensive rewrite of the Federal Reserve's DNA - an era characterized by "central banks providing a safety net for the market" is coming to an end.

Written by: Yan Waizhi Yi

Source: Wall Street Journal

On June 22, 2026, NBC reported a piece of news that was not unexpected: Former Federal Reserve Chairman Alan Greenspan passed away due to complications from Parkinson's disease at the age of 100.

He had long been out of the public eye. However, what he left behind had never left the market for a moment.

Today, more than half of the pricing logic in the global financial market still bears his fingerprints. That phrase "the Fed will provide liquidity" after "Black Monday" in 1987, the question posed during the "irrational exuberance" remarks in 1996 that triggered turmoil in global stock markets, and the mantra recited by traders for 30 years - "Don't Fight the Fed." These are not history; they are codes that are currently operational.

Just days before Greenspan's death, current Federal Reserve Chairman Kevin Warsh had just begun a complete reassessment of how the Federal Reserve operates. The timing of this coincidence almost feels like a deliberately arranged metaphor: as one person takes a bow, the rules he personally wrote are being dismantled and rebuilt by another.

The Birth of the "Greenspan Put"

To understand what Warsh is changing, it is necessary to first understand what kind of system he is taking over - a system that is almost entirely the work of Greenspan.

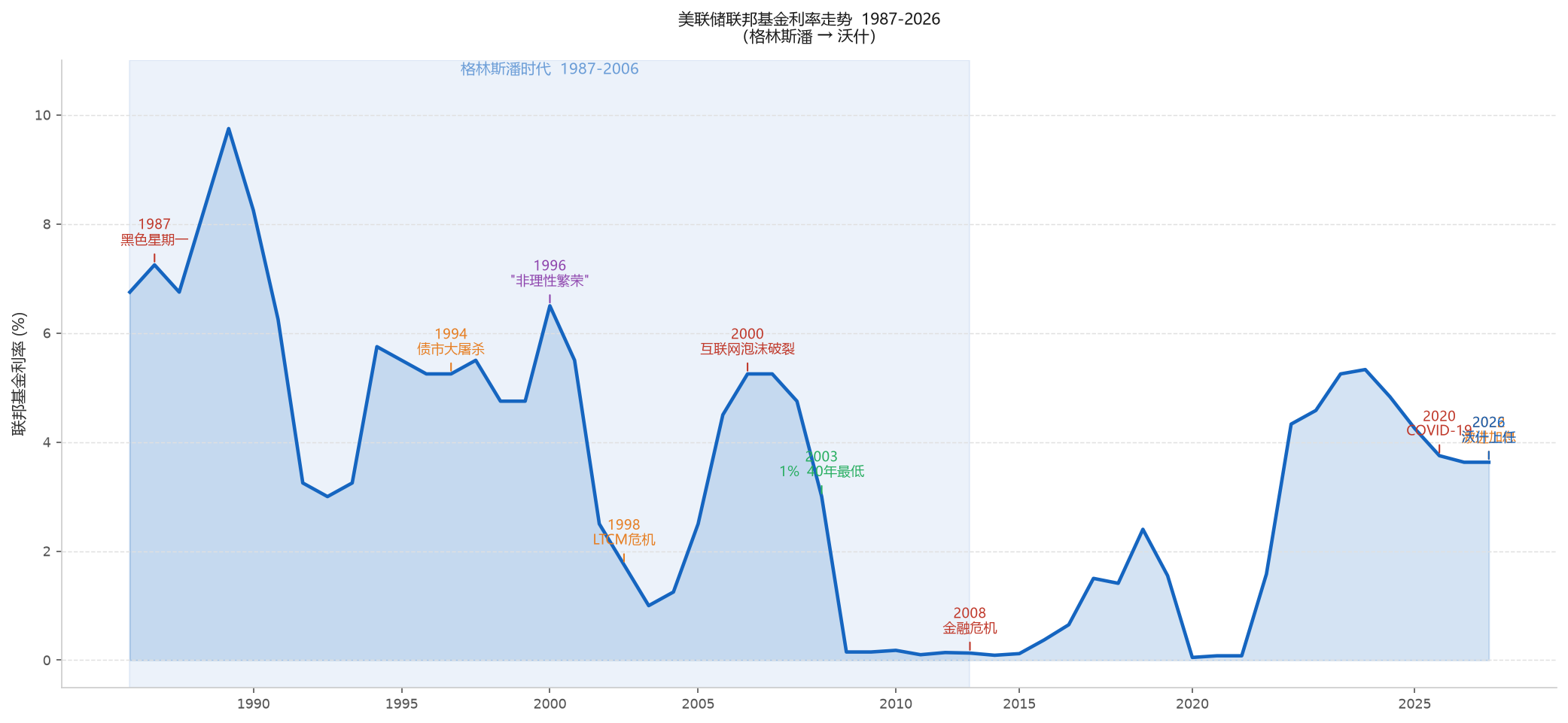

On August 11, 1987, 61-year-old Greenspan was nominated by President Reagan to replace Paul Volcker as Chairman of the Federal Reserve. This was a rather unexpected appointment. Greenspan was not an academic economist; it took him decades to complete his doctoral dissertation (he received his doctoral degree from New York University in 1977 at the age of 51). His background was as a Wall Street consultant - in 1954, he co-founded Townsend-Greenspan & Co. with lawyer Nathan Wolff to provide economic forecasting services to businesses and financial institutions. His intuition for data and business cycles was honed in the process of making money for clients, not derived from chalkboard theory.

This experience profoundly influenced his 19-year tenure at the Federal Reserve.

Only 69 days after taking office, on October 19, 1987, "Black Monday" struck. The Dow Jones Industrial Average plunged 22.6% in a single day, marking the worst single-day drop in the history of the American capital market. Programmatic trading triggered a liquidity black hole, and no one knew where the bottom was.

Greenspan's response defined the behavioral paradigm of the Federal Reserve for the next 30 years. He did not wait for the market to clear itself - that would have been the classical economics textbook answer - but instead quickly issued a statement: the Federal Reserve would "provide liquidity to support the economy and the financial system" and tacitly allowed banks to expand lending to brokers. This statement stabilized the market.

This logic later became condensed into one term - the "Greenspan Put." It means that when the market drops deep enough, the Federal Reserve will certainly step in to provide support, equivalent to giving all market participants a free put option. Once this expectation is formed, it can never be undone.

"Irrational Exuberance" and the Power of Language

Greenspan's shaping of the market was not only through action but also through language.

On December 5, 1996, during a speech at the American Enterprise Institute (AEI), he casually posed a rhetorical question: "How do we know when irrational exuberance has unduly escalated asset values?"

This question itself had no policy implications. However, the market's reaction was almost instantaneous: the Tokyo stock market opened the next day with a 3% drop, which was followed by declines in global markets.

This is the power of "Fedspeak." He later proudly summarized his style of language as a form of "purposeful ambiguity" - using four or five increasingly obscure sentences to evade unwanted questions, making the questioning Congressman think they received answers, then contentedly moving on to the next topic.

However, "irrational exuberance" was not ambiguous language; it was precise like a scalpel. It transmitted a signal: I think the stock market is too expensive. Just that alone was enough to trigger global turmoil. The market soon realized that this statement in itself did not change any policies - interest rates remained unchanged, and liquidity had not tightened. After a brief drop, the stock market continued to rise, reaching its peak in March 2000 during the internet bubble.

This, in turn, reinforced the credibility of the "Greenspan Put": even when he warned verbally, he was reluctant to truly tighten monetary policy, which led to the belief that he must be on the side of the bulls.

1994: The Forgotten "Hard Hand"

Today, people remember Greenspan mostly because of the "put" - believing he always stood on the market's side. But the events of 1994 tell a completely different story.

In early 1994, Greenspan judged that inflationary pressures were building and decided to act preemptively. Contrary to market expectations of a moderate stance, he quickly raised the federal funds rate from 3% to 6% within a year. This action was not communicated sufficiently to the market in advance, and was referred to as a "sneak attack."

The result was disastrous - a "bloodbath" in the bond market, with bond portfolios losing as much as $1.5 trillion, Orange County in California declaring bankruptcy due to massive losses from bond derivatives, and Greenspan's approval rating in the financial market plunging to rock bottom.

However, the outcome of this event actually solidified Greenspan's credibility in the market. Because he proved that he was not afraid to offend the market. His real priority was to control inflation, rather than to please Wall Street. This credibility enabled him to maintain low interest rates without triggering runaway inflation expectations in the late 1990s - the market believed in him, believing he would act when necessary.

This is the premise for the establishment of the "Greenspan Put": the market believed Greenspan was capable of controlling inflation, so they believed he would step in during crises. The two were two sides of the same coin.

1998: LTCM and the Precedent of "Too Big to Fail"

In 1998, two crises almost simultaneously broke out: the Russian sovereign debt default and the near bankruptcy of Long-Term Capital Management (LTCM), a hedge fund staffed by Nobel Prize-winning economists.

Greenspan's response once again shaped market expectations. He decisively cut interest rates and personally led the effort to organize Wall Street investment banks to privately rescue LTCM (the Federal Reserve did not directly provide funds but coordinated private sector intervention).

The historical significance of this event is often underestimated. It is one of the important sources of the modern financial market's "too big to fail" logic - when the failure of an institution could lead to systemic collapse, whether it is a bank, investment bank, or hedge fund, there will be someone (central banks or government) to organize a rescue.

From then on, the "Greenspan Put" expanded from the stock market to the entire financial system. The market began to systematically anticipate that the risks of systemically important institutions would ultimately be backed by monetary authorities.

Greenspan himself was not averse to this role. He wrote in his memoirs, "The job of a central banker is not to prevent every bubble from forming, but to ensure that the financial system does not collapse when the bubble bursts." This statement sounds cautious, but the market's understanding is: "So I can stay in the bubble a little longer, because the Fed will manage it when it bursts."

The Dark Side of the Legacy: 1% Interest Rates and Questions in 2008

After the internet bubble burst in 2000, the 9/11 terrorist attacks followed in 2001. Greenspan's response was to drop the federal funds rate from 6.5% in mid-2000 to a staggering low of 1% by mid-2003 - the lowest federal funds rate in over 40 years, maintained for a whole year.

Cheap money flooded into the real estate market. From 2000 to 2006, U.S. home prices cumulatively rose by over 80%. Subprime mortgages - loans issued to borrowers with very weak repayment abilities - wildly expanded during this period. Wall Street repackaged the subprime loans into CDOs (collateralized debt obligations) and used complex mathematical models to convince themselves that these products were "safe."

In 2008, everything collapsed.

Critics pointed their fingers directly at Greenspan: you kept interest rates at 1% for an entire year starting in 2003, inflating the real estate bubble with cheap money. You are the culprit behind the 2008 financial crisis.

Greenspan's defense was equally forceful. In a 2007 interview with USA Today, he stated, "On this one, I’m innocent." He shifted the blame to the "global savings glut" in his memoir "The Age of Turbulence" - emerging markets, represented by China, investing huge trade surpluses in dollar assets had depressed long-term interest rates, which was the fundamental source of monetary ease, rather than the Federal Reserve's short-term interest rate policy.

This debate remains unresolved. In 2016, a working paper from the Bank for International Settlements (BIS) found through quantitative analysis that Greenspan's maintenance of excessively low interest rates in his late tenure indeed significantly inflated home prices. However, there were also economists pointing out that the inflation levels in the U.S. from 2003 to 2005 were actually quite low, and the "neutral interest rate" itself was declining, so Greenspan's rate cuts were not entirely without reason.

Regardless, the 2008 crisis fundamentally questioned the logic of the "Greenspan Put": when the market firmly believes that the central bank will provide support during every downturn, moral hazard can accumulate to a level of systemic risk. This is precisely the legacy that the three generations of Federal Reserve Chairmen - Bernanke, Yellen, and Powell - had to confront - how to provide crisis support without further reinforcing the market's moral hazard expectations.

Later Years: From "Economic Tsar" to Controversial Figure

On January 31, 2006, Greenspan ended his 19-year tenure as Chairman of the Federal Reserve. Upon leaving, his popularity was at its peak - the U.S. economy had experienced one of the longest expansion cycles in history, inflation was kept at low levels, and the stock market underwent an epic bull market in the 1990s.

But the financial crisis came two years later, and Greenspan's reputation collapsed with it. In October 2008, he attended a Congressional hearing where he admitted to being "shocked and unable to believe" that the free market could fail so dramatically. This statement was interpreted by the media as "Greenspan's public confession of his faith in the free market," and became a seminal moment marking the decline of his public image.

After stepping down, Greenspan did not completely fade from the public eye. He founded a consulting firm, Greenspan Associates, continuing to provide economic advisory services to financial institutions. He occasionally voiced his opinions in the media - in 2018, he warned investors to "run for cover" on CNBC, as the U.S. Treasury yield curve inverted, which he considered a strong signal of an impending recession. In 2024, he, along with other former Federal Reserve and Treasury officials, issued a statement condemning the criminal investigation against Federal Reserve Chairman Powell as an "unprecedented attempt to undermine the independence of the Federal Reserve through prosecutorial attacks."

His personal life was also quite notable. His first marriage (to painter Joan Mitchell) ended in divorce after less than a year. In 1997, 71-year-old Greenspan married NBC Chief Foreign Affairs Correspondent Andrea Mitchell, with the ceremony officiated by Justice Ruth Bader Ginsburg. This marriage lasted until his death.

Greenspan also had a little-known early identity: a jazz saxophonist. As a youth, he attended the Juilliard School of Music and even played in Woody Herman's jazz band. This experience may explain his natural preference for "improvisation" and "ambiguity," whether in dealing with monetary policy or responding to reporters' questions.

What is Warsh Changing After Greenspan's Death?

When the news of Greenspan's passing was announced, current Federal Reserve Chairman Kevin Warsh's five task forces had just been launched less than a week earlier.

Warsh is not an outsider to the Federal Reserve. From 2006 to 2011, he served as a Federal Reserve Governor, witnessing the early years of the Bernanke era after Greenspan stepped down. After leaving the Federal Reserve, he went to the Hoover Institution at Stanford University, where he began systematically criticizing the Federal Reserve's increasingly "ultra-loose monetary path" post-crisis - notably the expansion of its balance sheet from less than $900 billion before 2008 to a peak of over $9 trillion. He believes that such a scale of asset purchases distorted asset pricing and created a pathological dependence of the market on central bank intervention.

This is the very first thing he intends to address upon taking office.

On June 17, 2026, Warsh chaired his first FOMC meeting. Maintaining the current interest rates was expected, but the format change in the post-meeting statement was noteworthy: Warsh placed "interest rate decisions" at the forefront of the statement, rather than discussing economic assessments first as had been the practice since 2009. This detail aligns more closely with the statement formats in the later period of the Greenspan era.

A bigger move is the establishment of five special task forces: to reassess the Federal Reserve's communication strategy, data framework, inflation theory, balance sheet size, and the impact of new technologies like artificial intelligence on the transmission mechanism of monetary policy. Warsh's directive for these task forces is to "start from first principles" - in other words, do not assume that any existing framework is a given.

Most intriguingly, it seems that "forward guidance" may be weakened or even eliminated. Warsh is not in agreement with the Federal Reserve's long-standing communication practice of "clearly telling the market what we plan to do next." He deleted all guiding language regarding the future policy path from the post-meeting statement. Former Cleveland Fed President Loretta Mester provided a precise analogy for this: the Federal Reserve has long had a "Hotel California problem" - once a statement is written into the minutes, it can never be erased. Warsh is doing a long-overdue "clearing."

If this indeed happens, the "Greenspan Put" would lose its most vital conduit for communication. For the past 15 years, the main source of information on "when the Fed will step in to save me" relied on the FOMC statements and the forward guidance in the chair's press conferences. If this information is deliberately obscured or even removed, the meaning of "don't fight the Fed" will fundamentally change - the Fed may not show up when you expect and may not do so in the manner you expect.

Conclusion: The End of a Paradigm

Greenspan lived for 100 years, long enough to witness the legacy he left being questioned by the 2008 financial crisis, amplified by quantitative easing, and distorted by the average inflation targeting regime.

He represented an era of confidence in "the Fed can manage the market."

During his 19 years in office, the United States experienced one of the longest economic expansions in history, inflation was kept at low levels, and "don't fight the Fed" became a mantra for all traders. He himself was referred to by Fortune magazine as "In Greenspan We Trust," and Bob Woodward's biography hailed him as a "Maestro."

Warsh faces a skeptical era of "whether the Fed can still control inflation expectations." Global supply chain disruptions, geopolitical fragmentation, challenges to the U.S. dollar's credibility - these issues far exceed what monetary policy alone can address. And his chosen response is to rewrite the very DNA of the Federal Reserve.

On June 22, 2026, Greenspan passed away. The playbook he left behind - the "Greenspan Put," his vague yet powerful artistry of language, and the expectation management that provided a safety net for the market through central bank credibility - has officially become history at this moment. The Federal Reserve is now facing a world far more complex than that of 1987 without the guidance of a "Maestro."

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。