Galaxy's research executive warns of deadly flaws hidden in Coinbase's tokenized US stocks, with the lessons from SpaceX's failure still fresh in mind.

Written by: Alex Thorn, Research Director at Galaxy Digital

Translated by: Saoirse, Foresight News

Editor’s Note: The process of merging cryptocurrency with traditional finance is accelerating. Recently, Coinbase launched multiple cross-asset products, including tokenized US stocks aimed at overseas users, which has sparked much discussion in the market. Alex Thorn, Research Director at Galaxy Digital, has released an in-depth analysis directly pointing out significant doubts regarding the platform's claim of 'true ownership rights for stocks'. The article combines the past case of xStocks' failure in SpaceX asset redemption to dissect the structural risks of third-party packaging models while also clarifying the hidden compliance and asset security risks associated with tokenized stocks in light of the uncertainties posed by the SEC's innovation exemption policy and the CLARITY Act for industry investors.

This week, Coinbase announced its plans regarding tokenized stocks but did not disclose the legal structure behind it. This structure has a critical impact on regulatory compliance, user experience, and the competitive landscape of the industry.

At the 'System Update' launch event held on June 16, Coinbase introduced a total of 21 new products and features covering four major areas: trading, lending, payments, and on-chain infrastructure. Among these, the tokenized stock business has caught our attention. Coinbase stated that next month it will launch tokenized US stocks for non-US users, with assets achieving 1:1 full reserve; the platform claims that these tokens allow holders to enjoy complete shareholder rights, receive dividends, and lend tokens for profit or use them as collateral, while US residents are unable to participate in this service.

Although Coinbase claims that these tokens represent 'true ownership rights for stocks', it has not disclosed the legal structure supporting this assertion. Accompanying the product launch is the B20 token standard deployed on the Base public blockchain, which is a layered, policy-controlled compliance toolset, benchmarked against Uniswap v4 hooks. However, Coinbase has not specified how it will integrate the B20 standard into its tokenized stock system.

Another highlight of this launch is Coinbase Advisor, an AI investment tool embedded within the app. This tool has completed SEC registration as a Registered Investment Advisor (RIA) and has filed with the National Futures Association as a commodity trading advisor, initially available only to Coinbase One members in the US. The new products also include cryptocurrency and stock options trading, real-world assets (RWA) and IPO pre-target perpetual contracts (with the first target being SpaceX), a privacy platform for enterprise compliance on-chain trading, and Bitcoin-backed loans launched in collaboration with Better.

Our Perspective

Currently, a deep integration of traditional finance and the cryptocurrency industry is indeed unfolding.

Like other native cryptocurrency exchanges, Coinbase's ambition to expand into traditional financial products is quite clear, just as traditional financial institutions are also continuously laying out in the cryptocurrency field. The two markets are both merging and competing for each other's customer resources. Coinbase is not simply integrating stock trading functions into its app; the company plans to launch options and perpetual contracts for a full range of asset classes. It is not difficult to foresee that tokenized stocks will also eventually introduce corresponding options and perpetual contracts.

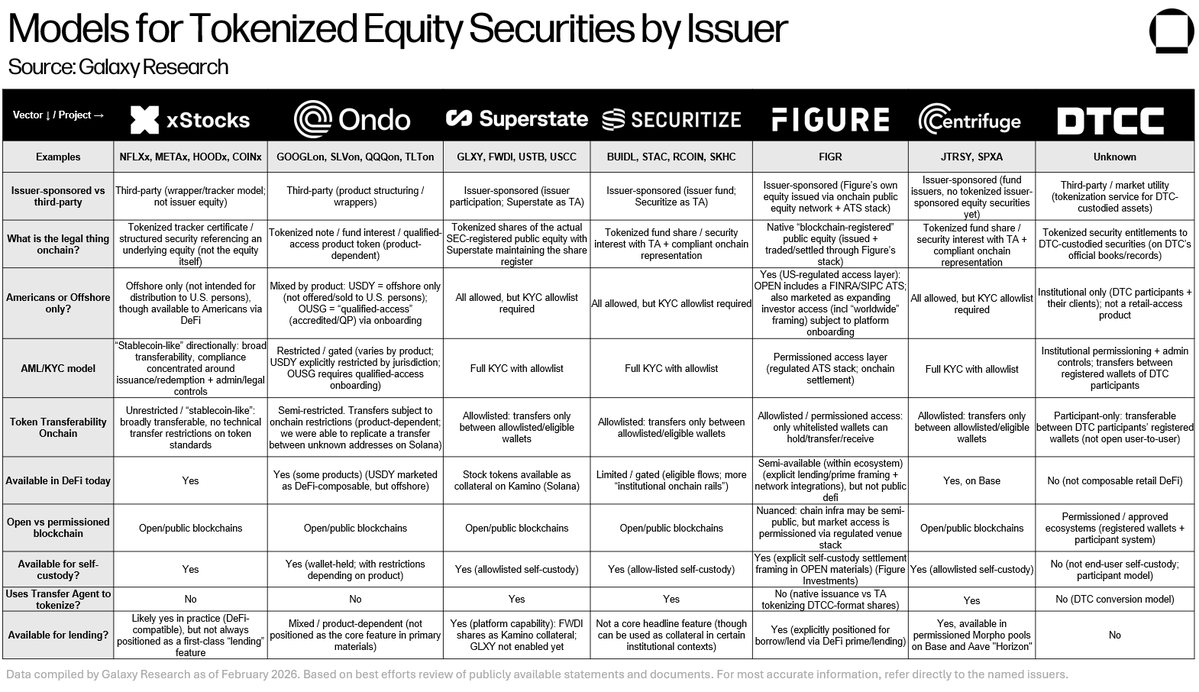

Speaking specifically about the tokenized stock sector, we have previously published a large number of analyses and comments. Based on our comprehensive judgment, Coinbase is likely adopting the third-party issuer 'wrapper' model, and currently only operates in offshore markets, open only to non-US users. This structural logic is highly similar to that of xStocks: underlying stocks are stored in a third-party investment vehicle, and then the shares of that vehicle are tokenized; the generated tokens can circulate in offshore trading venues and can also be withdrawn to self-custody wallets for various DeFi scenarios. This structure is completely different from the issuer-direct connection models promoted by Galaxy and Superstate. The chart below is an effort we made to compile, based on publicly available information, an industry map of tokenized stock issuers as of February (Note: The industry has continued to expand since then, for example, GLXY is now available as collateral for the Kamino platform, and Backpack launched the tokenized stock business earlier this month, but this chart still holds a high reference value).

Note: This chart was created in February, and relevant facts and data may have changed since; all data comes from public channels, compiled as best as possible. Please consult the respective issuers for accurate information.

It is precisely this wrapper model that makes Coinbase's phrase 'true ownership rights for stocks' full of contradictions. If there is a third-party packaging entity in between, the promises of dividends, shareholder voting rights, and other rights are not derived from the listed company of the underlying stock; the related rights constraints exist only in the service agreement between token holders and the packaging entity. Essentially, there is no direct legal association between token holders and the enterprises issuing the stocks. Currently, the industry does not have a mature compromise solution that can balance the issuer-direct connection model and the third-party packaging model. Perhaps a certain stock rights mechanism could achieve a balance? But key structural details have not yet been disclosed by Coinbase.

The third-party packaging model has recently exposed operational risks multiple times, with last week's SpaceX primary market share incident being a typical warning case. Multiple platforms, including Binance Wallet, Bybit, and Bitget, had listed shares obtained through xStocks channels for SpaceX IPO reservations, which were ultimately cancelled and refunded to users due to the inability to deliver the underlying stocks. Bybit informed users that xStocks was unable to deliver the underlying assets, and the platform did not obtain any shares of SpaceX; Kraken and xStocks' own users also received only a small portion of the subscription shares. Minting tokens has a very low technical threshold, but the real challenge lies in the collection, custody, and on-chain confirmation of the underlying assets. This is also the inherent structural risk of all third-party packaging products: lacking the official cooperation of the listed company, there is no guarantee that intermediary institutions adequately hold the real stocks.

All of the above business layouts are built upon two major unresolved regulatory policy backgrounds:

The SEC's originally planned 'innovation exemption policy' for tokenized stocks has been postponed. According to reports, the core of the policy disagreement lies in whether the exemption scope includes third-party packaged tokens or only permits direct connection tokens from issuers. The focal point of the dispute is a provision allowing the trading of third-party tokens — these tokens correspond to digital certificates of stocks whose issuance process was not disclosed or did not obtain the permission of the underlying listed company. SEC Commissioner Hester Peirce has publicly stated that she believes the exemption policy should only cover primary market native stock digital certificates, rather than all kinds of synthetic assets.

The CLARITY Act remains stalled in the US Senate, with no progress made in the past two weeks, and the remaining review window in Congress continues to tighten. The core value of this Coinbase product entirely depends on whether the third-party packaging entity can have compliance efficacy equivalent to directly holding stocks from issuers, but currently, there is no clear conclusion from the regulators on this.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。