Author | Azuma, Odaily Planet Daily

Strategy's preferred stock STRC is in a continuous "de-pegging" situation.

The U.S. stock market shows that, since May 15, STRC has gradually deviated from the target face value of $100, with the discount widening significantly recently, reaching a low of $83.26 during trading on Thursday, closing at $88.59, more than 11% away from the target face value.

For a regular stock, an 11% drop may not be a big deal, but for STRC, the continuous deviation from the target face value of $100 means that the core design goal of the product is facing severe challenges.

This is because in the initial design of Strategy, STRC was intended to be a yield-bearing security operating close to the face value of $100, rather than a high-volatility speculative asset. Now, the increasing divergence between market price and target face value has led more and more investors to reassess the logic behind this product.

More importantly, as Strategy continuously expands its Bitcoin reserve scale, STRC has gradually become the company's most important financing channel. In a sense, the market's pricing of STRC reflects not only investors' attitudes toward a preferred stock but also reflects the market's confidence in Strategy's entire capital operation model.

STRC: The Engine of Strategy's Capital Flywheel

To understand the seriousness of this de-pegging, it is first necessary to clarify the product structure of STRC and its unique anchoring mechanism.

STRC is an innovative financial derivative tool launched by Strategy in 2025. Unlike Strategy's common stock MSTR, STRC is positioned as a perpetual preferred stock with a fixed target face value ($100) and relatively stable dividend yields, making its nature closer to that of a fixed-income security.

- Note from Odaily: Strategy founder Michael Saylor recently revealed that STRC was designed with AI assistance.

In the closed loop of Strategy's balance sheet expansion, STRC is not just a regular financing tool, but the strongest engine of Strategy's current capital flywheel.

Prior to launching STRC, Strategy mainly relied on issuing convertible notes and directly increasing the issuance of common stock to raise funds to purchase Bitcoin. However, both models have limitations -- convertible bonds are constrained by maturity dates and the maximum debt leverage ratio, while frequent issuance of common stock dilutes existing shareholders' equity.

The emergence of STRC perfectly solves this pain point, with its core utility in Strategy's strategy mainly reflected in two dimensions:

- Unlimited "At-the-Market" (ATM) issuance plan: As long as STRC's market price stabilizes at $100 or above, Strategy can continuously issue new STRC shares in the secondary market through the ATM (At-the-Market) mechanism, raising fiat currency.

- Zero dilution of purchasing power: As a perpetual preferred stock, STRC has no statutory pressure to repay the principal and does not have the voting rights and residual asset distribution rights of common stock. This means that Strategy can create tens of billions in purchasing power without diluting MSTR shareholders' equity or increasing rigid debt interest, and invest all of it into increasing Bitcoin holdings.

By following the closed loop of "Issuing STRC ➡️ Raising fiat currency ➡️ Purchasing BTC ➡️ Enhancing company net assets ➡️ Boosting STRC trustworthiness," Strategy has successfully built a seemingly limitless capital flywheel.

However, the key prerequisite for this flywheel to operate smoothly is that STRC must maintain its value close to $100. Once the market price falls significantly below $100, according to ATM fundraising terms and market arbitrage logic, Strategy will be unable to effectively absorb funds from the market through discounted preferred stock, and its entire capital magic will effectively come to a halt.

At the design stage, to ensure that STRC's secondary market price always aligns closely with the target face value of $100, Strategy introduced a "monthly dynamic adjustment of the dividend rate" mechanism. In simple terms, when STRC's market price falls below $100, Strategy can increase the dividend rate to enhance product attractiveness; when the price exceeds $100, the dividend rate can be lowered -- theoretically, by continuously adjusting the dividend rate, STRC should be able to operate around $100 for a long time.

But now, even though Strategy has raised the dividend to a high of 11.5% and changed the payment frequency from monthly to bi-monthly, STRC's "de-pegging" status has not been effectively repaired... why is this?

Reasons for De-Pegging: Confidence, Confidence, and More Confidence

The failure of the dividend adjustment effect means that the risks being priced by the market have exceeded the yield of STRC itself. From the current market discussions, the market's risk concerns are mainly reflected in two aspects.

First, there are superficial technical factors. Some market participants believe that the recent decline is largely due to concentrated sell-offs by arbitrage funds during deleveraging.

Over the past year, STRC has traded close to $100 for a long time, thus attracting substantial yield-driven arbitrage funds to participate. These funds often amplify returns through leverage, earning dividend income while capitalizing on price returning to the face value. However, as STRC fell below $100 and continued to weaken, some leveraged accounts began to trigger risk control lines, forced to sell their positions; while the price drop further triggered more leveraged funds to liquidate, ultimately creating a chain reaction. In this process, the selling pressure continually reinforced itself, causing STRC's decline to far exceed normal supply and demand changes.

But merely explaining the current market performance with leveraged sell-offs seems insufficient. For many investors, deeper concerns lie in Strategy's liquidity reserve situation.

Earlier this month, JPMorgan released a research report stating that Strategy has an annual dividend payment obligation of about $1.7 billion, and based on the current cash reserve levels, the cash on hand is only sufficient to cover about 6.3 months of preferred stock dividend expenditures. This has raised market concerns regarding Strategy's promised future liquidity coverage abilities.

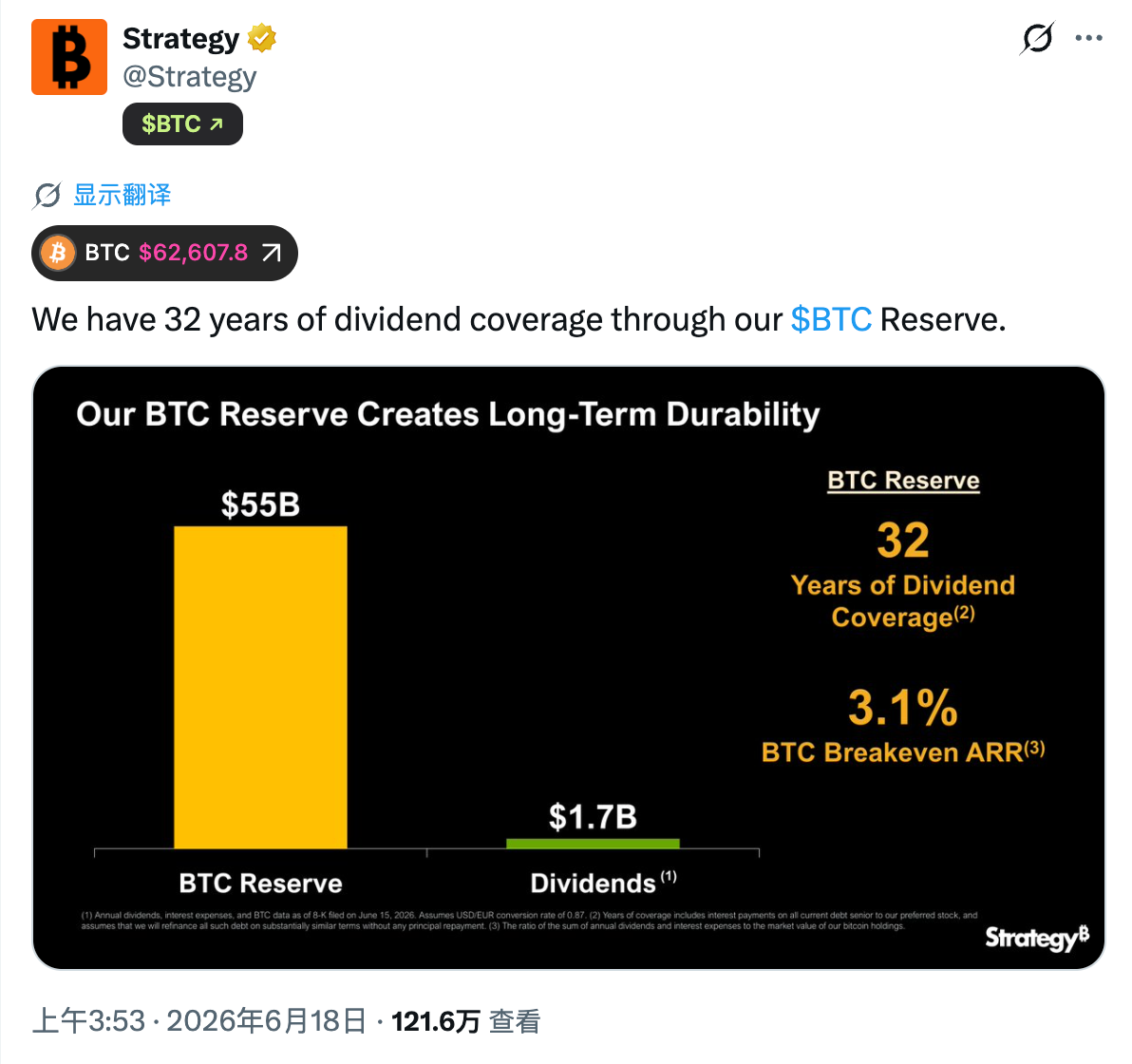

In response, Strategy provided a starkly different explanation, emphasizing in an official post on X that if its enormous Bitcoin reserves are taken into account, it would be enough to cover 32 years of dividend payments.

However, the problem is that these two statements are based on different premises. JPMorgan focuses on Strategy's cash attributes, while Strategy's calculations implicitly assume an important hypothesis -- that if necessary, the company can raise funds by selling Bitcoin.

This precisely touches on the most sensitive part of the market. Earlier this month, Strategy sold a portion of its Bitcoin holdings for the first time. Although the scale of this sale was only 32 coins, and the official described it as "actively conducting market desensitization tests" and mentioned that "more would be bought back later," the move still caused a severe impact on the market. The reason is that, over the past few years, Strategy and its founder Michael Saylor have consistently conveyed a core narrative to the market -- Bitcoin is a long-term strategic reserve asset, and the company will finance its operational funds through capital markets rather than relying on selling Bitcoin.

Therefore, when the market saw for the first time that Strategy actually sold Bitcoin, it inevitably raised greater concerns -- if the future financing environment tightens, will Strategy need to further rely on selling Bitcoin to fulfill its dividend obligations? If the answer is not an absolute no, then investors must reevaluate the risk levels of related securities.

From this perspective, the ongoing "de-pegging" of STRC actually signifies that the market is reassessing the robustness of the entire Strategy capital structure.

Strategy's Buying Pressure May Turn into Selling Pressure

For Strategy, the most significant impact of STRC's continued de-pegging lies in the weakening of its financing function.

In recent years, Strategy has been able to continuously expand its Bitcoin reserves, with the core logic being to obtain funds from the capital market through issuing stocks, convertible bonds, and preferred stock, and then use those funds to increase Bitcoin holdings. STRC is the most important financing tool for Strategy, and when it trades below the target face value of $100 for a long time, it means that the market is demanding higher risk compensation, and Strategy's financing ability is therefore likely to fall into a temporary stasis.

Going forward, STRC's re-pegging status may become an important indicator for the market to observe Strategy's risk situation. If STRC remains at a discount for an extended period, leading to sustained limitations on financing capability, while Strategy's cash reserves are continuously depleted, concerns will inevitably rise regarding Strategy's future need to sell more Bitcoin to meet dividend payment requirements.

Once this expectation is strengthened, its impact will no longer be limited to STRC itself. As one of the most important marginal buyers in the Bitcoin market over the past few years, Strategy's financing ability and pace of accumulation have always significantly influenced market supply and demand expectations; if Strategy's buying pressure turns into selling pressure, it could impose unimaginable downward pressure on Bitcoin.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。