Written by: David, Chaoxiang Research

Chaoxiang Guide: SanDisk's stock has increased about 40 times since its IPO 16 months ago, and Jiangbolong's net profit in the first quarter of 2026 increased 26 times compared to the same period last year... Storage is the hottest sector in 2026, without a doubt. However, since June, the three giants AMD, NVIDIA, and SanDisk have done the same thing almost simultaneously:

Finding ways to use less expensive memory (DRAM) and shifting tasks to cheaper flash memory (NAND). This "flash memory substitution" hidden line has seen leading stocks soar, and the real opportunities that have yet to be priced may be hidden in its upstream and downstream.

Understanding the current situation of AI being constrained by the "memory tax"

The momentum of this storage market so far can be seen in a few numbers.

SanDisk (SNDK) was spun off from Western Digital and went public in February 2025 at an offering price of about $38, and by mid-June 2026 had reached about $2000, increasing nearly 40 times in 16 months, with a P/E ratio of about 69 times; let alone Micron.

On the A-share side, Jiangbolong's net profit in the first quarter of 2026 was 3.862 billion yuan, an increase of 2644% year-on-year; Zhaojie Innovation's net profit increased by 522% year-on-year, and on June 17, it directly hit a daily trading limit, closing at a historic high. The previous consensus in the entire market seems to have been summed up in one sentence:

AI is desperately lacking storage, shortages are expected to last until 2028, and buying storage stocks will lead to gains.

But while everyone celebrates the "shortage," several of the most authoritative companies are quietly laying mines in this story.

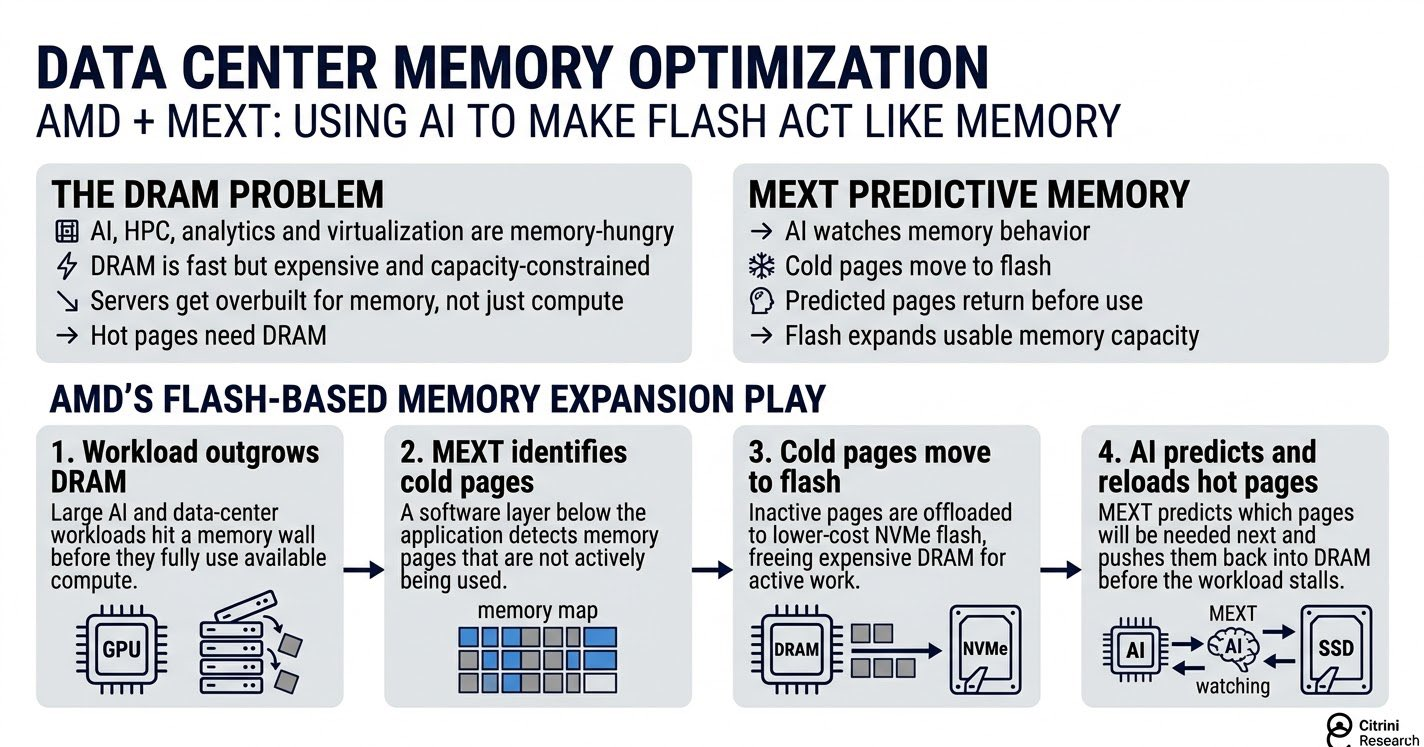

On June 15, AMD announced the acquisition of a company called MEXT, whose core technology is to use AI to "disguise" flash memory as memory;

Earlier, in early 2026, NVIDIA launched CMX at CES and GTC, relocating the portion of data in AI runtime that occupies the most memory to the flash memory layer; looking back further, SanDisk and SK Hynix teamed up in February to initiate a new standard called HBF to cram flash memory into packages originally designed only for high-end memory (HBM).

Looking at these three things together, the direction is completely consistent:

Adding a layer of "cheaper than memory, faster than hard drives" intermediate memory for AI, paying less for expensive DRAM. An overseas thematic investment research organization, Citrini Research, even named this phenomenon "The AI Tax."

To understand this term and follow the investment targets, you first need to distinguish between the two types of "memory" in AI.

One type is memory, namely DRAM, as well as its highest-end form HBM (High Bandwidth Memory, specifically used with GPUs). It is fast, and GPUs can easily access data, but it is extremely expensive and has a small capacity.

The other type is flash memory, or NAND, which is what your computer's solid-state drive uses. It is cheap, has a large capacity, but is slow. Here's a not-so-precise but sufficient analogy: DRAM is like files on your desk that you can easily grab, while NAND is like goods in a warehouse downstairs; it’s cheap and plentiful, but accessing it takes longer.

Over the past two years, as AI has developed, it has become clear that desk space is insufficient and excessively expensive.

TrendForce data shows that the contract price of DRAM increased by over 90% quarter-on-quarter in Q1 2026; Citi predicts that the average DRAM price will increase by 88% throughout 2026, while NAND will rise by 74%. The root of the price increase lies in AI:

NVIDIA's GPUs need to be fed data, HBM is both fast and expensive, thus HBM has consumed more and more DRAM capacity.

A set of data cited by Citrini indicates that HBM's share of total DRAM wafer production rose from 2% in 2020 to about 21% in 2025, and is expected to be 25% in 2026... This means that one-quarter of memory capacity is occupied by HBM, naturally making it tighter and more expensive for others.

This is the origin of the "memory tax."

AI wants to run fast but is forced to pay an increasingly high "tax" for both expensive and scarce memory. The tax is too heavy, naturally, there are those who want to avoid it. The only way to avoid the tax is to shift some of the tasks originally based on DRAM onto the cheaper NAND flash memory.

The three things mentioned earlier that AMD, NVIDIA, and SanDisk are doing essentially represent different paths of "tax avoidance." But the effect is to add a layer of "cheaper than memory, faster than hard drives" intermediate memory for AI.

The significance for investment lies in this "shifting" term. Every task moved to flash memory is adding another layer of demand to the NAND industry chain. Storage leaders have already experienced a round of price increases due to "shortages," while "flash memory replacing DRAM" is the second layer of logic on top of price increases.

It doesn't necessarily point to the already crazily priced leaders, but rather to those segments in this chain that have not yet been priced within this layer of logic. This is what we should dig further into.

Dissecting the flash memory industry chain: upstream earns profits, main control sells shovels

The flash memory business, from wafers to the hard drives in your hands, can be roughly divided into three layers, with the further upstream being more profitable and monopolistic.

- The most upstream is the NAND original factory, those who produce wafers themselves:

Samsung, SK Hynix (after the merger with Kioxia), Micron, and SanDisk spun off from Western Digital. They control capacity and earn the most during price increase cycles.

- The middle layer consists of module manufacturers, who buy wafer chips from original factories and package them into SSDs and memory bars to sell to end-users:

They do not produce wafers and earn money through processing and branding, often exhibiting even more exaggerated performance elasticity than the original factories. When chip prices rise, their low-cost inventory instantly appreciates.

Jiangbolong, Baiwei Storage, and Demingli from A-share are all part of this layer. Jiangbolong’s net profit in Q1 2026 was 3.862 billion yuan, an increase of 2644% year-on-year; Baiwei Storage grew 1567% during the same period.

But elasticity can also be a double-edged sword. Once chip prices drop, the inventory can backfire, and module manufacturers are usually the first to feel the pressure during a cycle.

- The most easily overlooked is the third layer, the main control chip:

In SSDs, aside from flash memory chips, there's a "brain" responsible for managing data inbound and outbound, which is the main control. It does not directly benefit from rising chip prices, but as long as SSD shipments increase, the demand for main control rises.

Theoretically, this layer is the closest to the "water seller" position in this chain. The top two independent main controls globally are Silicon Motion (SIMO) from Taiwan, and Phison (8299.TW), with A-share's Lianyun Technology (688449) ranking third.

Currently, within these three layers, original factories and module manufacturers have been fully priced into the market by "the pricing logic," reflecting the current reality of shortages and price increase.

Meanwhile, "flash memory replacing DRAM" adds another layer of logic on top of price increases, benefiting not just from price rises, but also from the long-term expansion of SSD/flash memory shipments.

This layer of logic is most likely to benefit those segments driven by shipments that haven't yet been boosted by the price increase cycle, such as main control; as well as the newly created volume generated by the HBF specifically discussed in the next chapter.

Truly unpriced: the "valuation depression" of main control and the "new cake" from HBF

Segments driven by shipments that haven't yet been boosted by the price increases can be further explored in two areas.

The first area is the valuation gap of main control.

Lianyun Technology (688449) serves as a case study. It is the third-largest independent SSD main control manufacturer globally, just behind Taiwan's Silicon Motion and Phison, and its PCIe 5.0 main control is one of the few domestic companies that can mass-produce.

However, as of April 2026, its market value is still less than its IPO day, and its stock price has been significantly outpaced by the module stocks like Jiangbolong and Demingli during the same period... The reason likely isn't complex:

Main control doesn't directly benefit from rising chip prices, and during this past half year when chip prices have surged, capital has flocked to the most elastic module manufacturers, leaving main control sidelined.

But I believe this actually reflects the distinction between "price increase logic" and "shipment volume logic." When chip prices rise, those with inventory—the original factories and module manufacturers—benefit, but main control does not; however, the substitution of flash memory for DRAM leads to long-term amplification of SSD shipment volume. Every additional SSD sold requires an additional main control.

If this line holds, it benefits from volume rather than price; main control is a more pure target.

Three companies to watch in this layer:

Silicon Motion (SIMO) (US ADR): The largest independent main control globally; it holds over 30% market share in consumer-grade SSD main control.

Phison 8299.TW (Taiwan stock): The second-largest independent main control globally; custom main control for Kioxia comes from them.

Lianyun Technology 688449 (A-share): The third-largest independent main control globally; among domestic main controls, it has the most advanced technology and also the largest valuation depression.

However, risks also need to be clarified. Main control is not a high-monopoly segment; there are numerous domestic players competing and price wars have been ongoing; public data shows that Lianyun’s R&D expense ratio is as high as 36%-38%, profit is continuously diluted, and its "global third" share does not equate to high profits.

The second area is the "new cake" created by HBF.

First, let's explain what HBF is.

HBM is both fast and expensive and has consumed one-quarter of DRAM capacity. Thus, SanDisk and SK Hynix came up with a solution: to create a layer of high-bandwidth flash (HBF) similar in form to HBM, but with 8 to 16 times the capacity and only a fraction of the cost.

It doesn't compete with HBM; it acts as a "large-capacity warehouse" next to HBM, specifically addressing the needs of AI inference data that "cannot fit into HBM but are too valuable to throw into cold storage."

The process for producing HBF involves using TSV (through-silicon vias, creating vertical connections by drilling holes on the chip) to stack multiple layers of NAND and then bonding and packaging them, which shares origin with HBM. The related targets in technology include:

Changjiang Electronics Technology 600584 and Tongfu Microelectronics 002156 (A-share): The leading dual heads in domestic packaging and testing, capable of the stacking and bonding technology used in HBF.

Huahai Chengke 688535 (A-share): The only company in China that mass produces the core material GMC for HBM packaging; the technology used in HBF is extendable from the same source.

However, this segment feels more like unfulfilled expectations, and several points need attention.

First, HBF has not yet reached mass production. SanDisk's timeline targets late 2026 for sample rollout and early 2027 for the first batch of equipment, so currently, all "benefits" are merely expectations, with no revenue entering the financial reports.

Second, the market is not as large as imagined. According to predictions cited by SK Hynix, the HBF market is expected to reach about $12 billion by 2030, while HBM is predicted to be around $117 billion during the same period, meaning HBF is less than a fraction of that. It serves as a supplementary layer, not a disruptor.

Third, numerous "HBF concept stocks" have emerged in the A-share market, including Yishitong, Feikai Materials, Xinyuan Micro, and Kuaike Intelligent, which frequently get mentioned. Most of these companies are merely "theoretically relevant" without actual orders related to HBF or technological validation disclosed, exemplifying the typical concept hype.

These are not the same as Changjiang Electronics and Huahai Chengke, where the "process can genuinely connect"; they need to be viewed separately.

Therefore, these two segments can be seen as part of the same investment theme, representing both current and long-term narratives.

Main control represents the "current shipments but valuation has yet to reflect substitution logic" valley, which is tangible; while the new increments from HBF represent "sexy stories but payouts are to wait until after 2027" long-term options, which are intangible and the concept stocks are quite inflated.

A single chart to understand the entire market: where the targets lie along the industry chain and whether they are expensive

Summarizing the segments previously dissected into a single map.

According to actual geographic distribution, this chain is concentrated in four markets: NAND original manufacturers are in the US, Japan, and Korea; the main controls are distributed in US ADRs and Taiwan stocks; modules, packaging and testing, and materials are mostly in A-shares. There are no corresponding pure flash memory targets in the Hong Kong stock market, so we won’t force any combinations here.

When reading this chart, remember one coordinate:

The further upstream (original manufacturer), the more monopolistic and profitable, but also priced higher, with the most expensive valuations; the further down to midstream (modules, main control, packaging, materials), the elasticity and certainty vary, with some not yet priced under the "substitution logic."

Risks and variables: short-term is favorable, long-term is a sword hanging over DRAM

The most commonly misunderstood aspect of the "flash memory substitution" line is confusing short-term and long-term factors. Their directions are actually opposite.

In the short term (from 2026 to 2027), substitution hasn't yet scaled to landing where the storage super cycle is still being fulfilled. The NAND contract price in Q2 is still rising by over 70% quarter-on-quarter, with original factories and module manufacturers continuing to explode in performance.

During this phase, the "memory tax" presents a pure tailwind for the flash memory chain: as AI grows more desperate for memory, it will increasingly shift towards flash, hence driving demand for NAND.

The short-term risks do not lie in the logic but in the positioning. The valuations of leaders already encompass a lot of optimistic expectations; SanDisk has a P/E ratio of 69 times, and A-share module stocks have generally doubled, with Micron, AMD, and SanDisk experiencing collective pullbacks of 6%-7% on June 17, as high-positioned funds reacted instinctively to "too much too fast" rises.

Pursuing high bets from this position is a gamble on whether sentiment can continue.

In the medium to long term (after 2027), true variables will emerge. If HBF achieves mass production, and solutions like CMX and MEXT are validated as effective, the narrative that "flash memory can replace some of DRAM's tasks" will transition from theory to reality.

At that point, the narrative of DRAM being "forever in shortage, scarcity premium never diminishing" will be shaken, which is the sword hanging over pure bullish positions in DRAM.

Note that this sword cuts against DRAM’s scarcity premium, which may actually be a boon for the NAND/flash memory chain (as demand is redirected). Hence, the same event poses a risk for DRAM bulls but presents an opportunity for the flash memory chain.

Transforming ambiguous long-term variables into trackable elements, I believe three signals can be monitored:

- HBF sample rollout progress (late 2026): The yield and cost of the samples will determine whether this technology path is genuinely landing or just another empty promise.

- NVIDIA CMX actual shipments (starting from late 2026): Whether downstream cloud manufacturers are willing to pay for the "flash layer," CMX's shipments are the most direct votes.

- Turning point for NAND contract prices from Samsung and SK Hynix: A shift from rising to flat, then to falling contract prices is the earliest evidence of loosening supply-demand logic, as well as a signal for the "super cycle" retreat.

Before these three signals appear, the short-term prosperity remains; once they do, the narrative should transition from "price increase tailwinds" to "substitution disproof of DRAM scarcity" in a new phase.

Chaoxiang Judgment:

Short-term prosperity in this chain remains, but valuations have already accounted for optimistic expectations; pursuing storage leaders is a gamble on sentiment. It is better to look for segments like main control (Silicon Motion, Phison, Lianyun) that have not yet been priced under this level of "substitution logic," where asymmetry is better than those upstream original factories already priced at 40 times.

The new increments in HBF are directionally enticing, but before 2027 they remain long-term options, and concept stocks are mixed; they are suitable for tracking but not for significant investment at this moment.

In short: I am optimistic about the long-term logic of this industrial chain, but the cost-effectiveness at this moment does not lie with the hottest leading stocks.

Note: This article is a collection of information and analysis of viewpoints. The stocks, ratings, and target prices involved are sourced from public information and are time-sensitive, not constituting any investment advice. The market has risks, and decisions should be made based on personal judgment.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。