The prediction market and perpetual contracts have taken a share of the cake from investment banks.

Written by: Prathik Desai

Translated by: Luffy, Foresight News

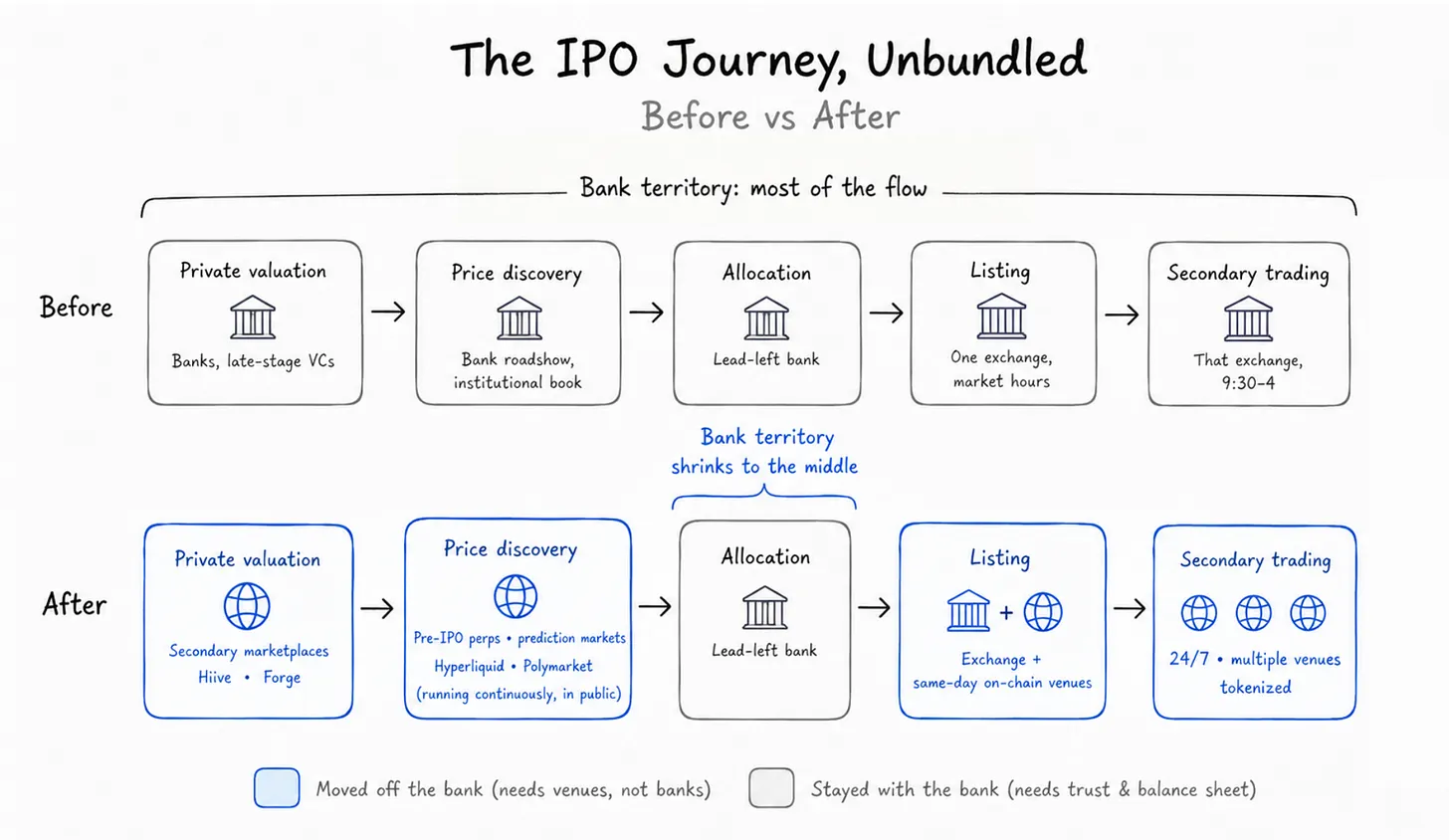

Going public is an important ritual in the capital society system. Company executives embark on a roadshow for several weeks, presenting business plans to major fund managers in order to attract institutional investment. Investment banks play the role of underwriting intermediaries, summarizing market subscription demand, assessing company valuations, finalizing issue prices, and completing share distribution. When the bell rings on the day of listing, private companies officially turn into public ones. Subsequently, buy and sell orders in the secondary market engage in continuous games, completing price discovery within hours or even days of opening.

The reason this set of procedures of roadshow, pricing, and ringing the bell for listing has existed for a long time is primarily that the outside world cannot access the real operational data of private companies and can only rely on investment banks for pricing. In the past, all companies had to fully complete this process to list on the exchange.

However, recently, SpaceX, which listed on the US stock market, charted a completely different path to going public. Elon Musk directly finalized the issue price before the investment banks estimated the pricing and conducted the roadshow.

Traditional IPOs would package the three core tasks of price discovery, finding investors, and share delivery for investment banks to complete uniformly, paying them a bundled service fee. In contrast, SpaceX's listing thoroughly split the three stages and allowed different channels to complete them independently. Before the investment banks officially initiated the listing work, the market had already given the company a fair valuation, with a large number of investors lining up to subscribe in advance.

This article will dissect how SpaceX changed the way companies go public and the role changes of investment banks in the new listing environment.

The Origin of Investment Bank Underwriting Service Fees

Investment banks charge underwriting service fees to companies planning to go public. For almost a century, this fee has typically been charged as a percentage of the total amount raised by the company.

The complete underwriting process includes: the investment bank organizing a global roadshow, collecting intention subscription orders from institutions and retail investors at different price ranges, finalizing an issue price acceptable to the market, and ensuring the smooth delivery of shares. In a full underwriting model, the investment bank takes on all the issued shares and then distributes them to all subscribing investors.

The three core functions of price discovery, distribution allocation, and share delivery have been long bundled due to the limitations of early market infrastructure. Investment banks are the only institutions that can master complete market information, making them the most suitable to judge market demand. They can access the company's complete financial data and development plans in advance to accurately calculate the stock price. They have a vast and diverse client resource base and cross-industry collaboration channels, allowing them to distribute shares to leading institutions and retail investors; at the same time, they provide a mature clearing and settlement system to ensure normal share delivery.

Therefore, companies planning to go public have no choice but to purchase these services in a bundled manner and pay the service fees.

The split IPO has completely broken the monopoly of investment banks. Before the investment banks initiated the listing preparations, public channels such as perpetual contract trading platforms, prediction markets, and quasi-primary markets had already fully displayed the market's real demand. Companies can negotiate their own underwriting fee rates and choose the most efficient service channels for each stage of the listing.

The average underwriting fee rate for medium-sized IPOs in the United States is about 7% of the total amount raised, while large projects see a significant reduction in rates. In 2014, Alibaba raised $25 billion and had an underwriting fee rate of only 1.2%. This time, SpaceX's underwriting fee rate was as low as 0.67%. The fact that this largest IPO in history can secure such a low rate can be attributed to many reasons, among which breaking down the listing process and weakening the traditional functions of investment banks is undoubtedly one of them.

Price Discovery: Investment Banks Lose Pricing Power

SpaceX broke traditional IPO rules from the preparation stage. The traditional process is defined by investment banks determining a price range, gradually probing market acceptance, and ultimately finalizing the issue price; however, Musk directly announced a fixed issue price of $135, leaving investors only to choose whether to subscribe or give up.

SpaceX can skip the investment bank pricing stage because the market had already spontaneously completed the valuation and pricing a few weeks before the IPO.

Three types of public markets provided different dimensions of price signals for SpaceX:

- Quasi-primary and secondary markets like Hiive and Forge: Company employees and early investors traded private shares, with the transaction price in SpaceX remaining stable around $150, close to the opening price on the first day of listing;

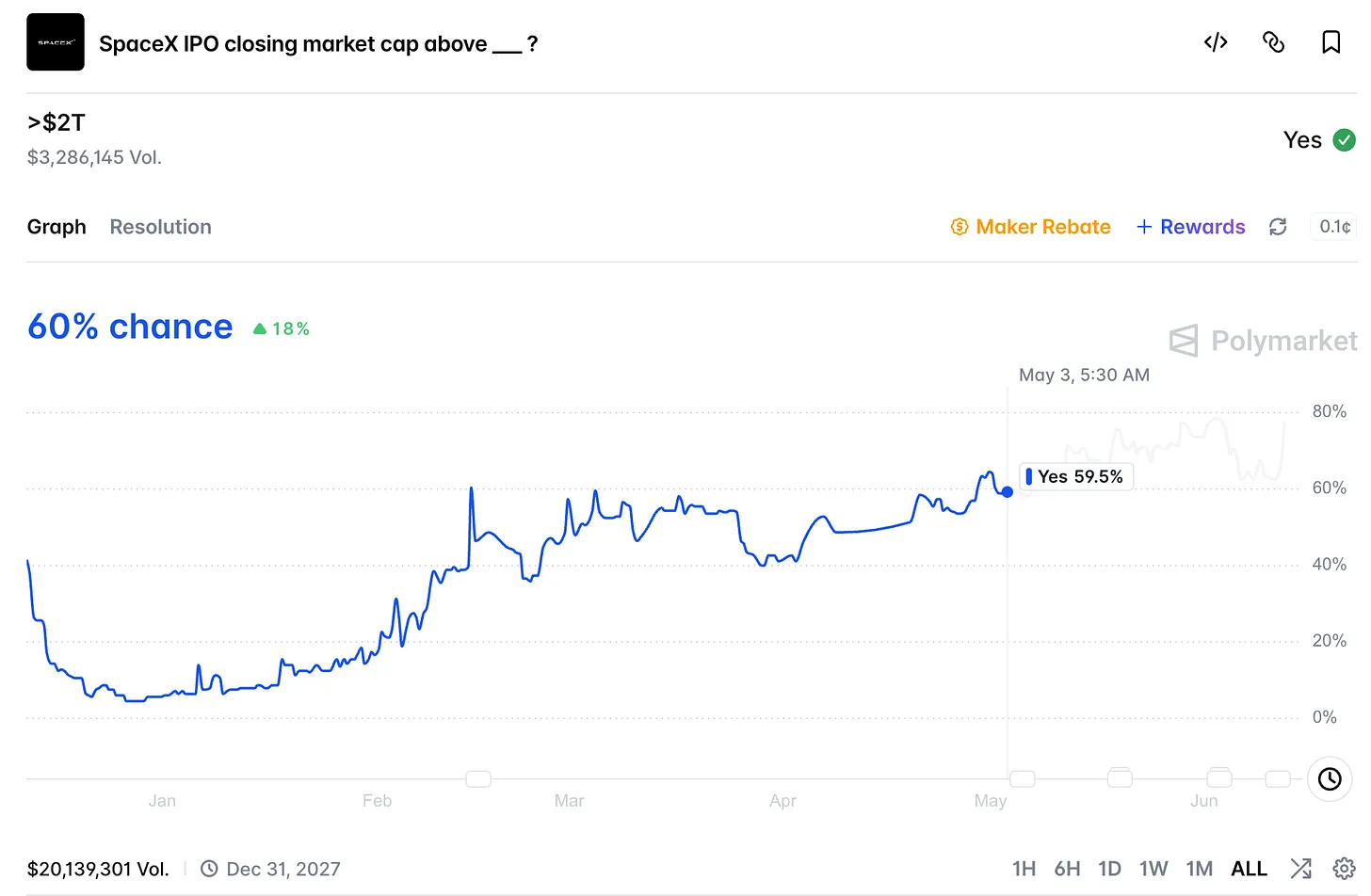

- Prediction market Polymarket: Users bet on the closing price on the first day of listing, with the maximum betting amount corresponding to a company valuation exceeding $2 trillion; On Friday, June 12, SpaceX officially went public, with the first day's closing price at about $161, up 20% from the issue price, bringing the total company valuation to $2.1 trillion;

- Hyperliquid perpetual contract platform: 24/7 trading of synthetic perpetual contracts for SpaceX, reflecting the market's valuation expectations for the stock in real-time.

Before the official listing, these pre-IPO perpetual contracts did not have real stocks as underlying assets; essentially, they were leveraged bets on the stock price on the first day of listing. The vast majority of positions on the Hyperliquid platform were concentrated in SpaceX contracts. On the day of the listing, the price range for the perpetual contract was between $174 and $185, showing a premium of 30%-35% over the $135 issue price; SpaceX stock peaked at $176 during trading. After the stock formally landed on the exchange, the perpetual contract price quickly converged toward the $150 opening price.

Is this merely a coincidence? There have been precedents proving that this type of new pricing channel has reference value. A few weeks ago, when chip company Cerebras went public, the IPO perpetual contract price on the Hyperliquid platform had only a 1.3% discrepancy from the actual opening price on NASDAQ; once the stock opened, the price difference nearly vanished. At that time, the company had not even finalized the issue price, and the market had preemptively forecast the opening price.

By relying on various public trading markets, SpaceX circumvented the first core task that investment banks were responsible for: price discovery.

Share Delivery: Tokenization Track Exposes Underlying Custody Vulnerabilities

After determining the pricing, the second core task for traditional investment banks is distributing shares and matching investors. We will skip the distribution process for now and break down the investment bank's third function: share allocation and delivery.

On the day of SpaceX's listing, stock trading was dispersed across multiple platforms, significantly different from traditional IPO models. Tokens were issued on the Solana chain via Backpack, products corresponding to them were launched by compliant agency Kraken, Ondo issued tracking tokens, and Hyperliquid launched synthetic perpetual contracts, all based on SPCX as an underlying asset; centralized exchanges like Bitget, Bybit, and Binance also opened IPO subscription channels.

On the day of listing, completely different outcomes appeared on different platforms.

Products that directly hold real shares or connect shares through compliant brokerages opened on time, with prices mirroring those of the underlying stocks. The Backpack Solana tokens correspond to the real shares held by custodial brokerages on a 1:1 basis; Kraken's US segment connects stocks via Payward Securities; Ondo issues asset custody proof daily to ensure the tokens adequately correspond to the underlying assets; Hyperliquid perpetual contracts do not require ownership of stocks, and stock prices automatically synchronize after the stocks are listed.

Binance, Bybit, and Bitget launched tokenized subscription activities, and the xStocks platform promised that tokens would fully correspond to real stocks. However, in the end, the platform was unable to secure adequate allocated shares, resulting in a full refund; the refund scale for Binance alone reached $557 million.

The root of the problem is not the blockchain technology itself; compliant custody channels completed the delivery normally. SpaceX's subscription was oversubscribed, with market demand reaching 3.5 to 4 times the $75 billion fundraising amount. Centralized exchanges, relying on third-party intermediaries to allocate shares, ultimately faced delivery failures, forcing the platform to issue full refunds.

When price discovery is completely public and freely accessible, pricing is no longer a scarce, high-value stage in the IPO process. The core of industry competition has shifted to whether shares can be fully delivered.

The challenge of share delivery is not a novel issue. Wall Street faced a similar crisis 60 years ago and built supporting infrastructure to solve it thoroughly.

In the late 1960s, the explosion of stock trading volume in the United States was hindered by the fact that stock certificates were paper, requiring search, verification, and manual delivery for each transaction, which inundated back-office departments with piles of documents. Exchanges directly closed every Wednesday for settling accumulated paperwork. Ultimately, the entire industry found a solution, which was to avoid the circulation of paper documents.

In 1968, a central securities custody institution was established, which was reorganized in 1973 into the American Depository Trust Company. All paper stocks were centrally deposited in a custodial treasury, and ownership changes only through ledger records. All assets are stored with a trusted third party, eliminating delivery risks; the custodial institution can guarantee that sellers hold adequate shares and buyers complete transfers smoothly.

This is also the core issue that custody infrastructure needs to address: whether sellers genuinely hold the underlying assets and whether asset transfers can be completed.

The tokenization model faces this risk as well. Tokens can be issued in advance, but the underlying stocks may not necessarily be simultaneously deposited in compliant custody institutions. If the stocks corresponding to the tokens are adequately deposited by the brokerage, the delivery is secured; if the tokens are issued first, but the underlying shares have not been actualized, the promise of fulfillment loses its support. The incident of 2026 arose precisely because the platform was unable to obtain real stocks corresponding to the tokens issued.

In the future, the difficulty of IPOs will no longer lie in price discovery, but in verifying the real existence of underlying assets and ensuring normal transfer.

What Irreplaceable Value Do Investment Banks Still Hold?

A comprehensive review of the new listing process shows that the three traditional functions have been diverted to external channels.

Price discovery in the primary market is no longer monopolized by investment banks. Weeks, if not months, before the listing, quasi-primary markets, prediction markets, and perpetual contract platforms continuously provide public valuations, and by the time SpaceX finalizes the issue price, multiple channels had already given a fair market price;

The trading channels for listing are no longer singular. As SpaceX landed on NASDAQ, multiple blockchain trading channels opened simultaneously. Blockchain supports 24/7 trading, and secondary market liquidity is no longer limited to a single traditional exchange;

The core threshold for share delivery is the qualification for asset custody. In the past, this capability was exclusively controlled by investment banks, relying on custodial institutions to complete delivery guarantees; today, any institution with compliant custody qualifications can undertake this business.

So, what still requires investment banks to resolve? Currently, investment banks retain four core intermediary functions that are hard to replace.

First is credit endorsement. The signature of the lead underwriter on the prospectus acts as a credit guarantee for the project, providing conservative institutional investors with safety endorsement. This reputation, built over decades in the industry, cannot be replicated by on-chain token platforms; investment banks charge service fees based on their credit endorsement. In this instance, SpaceX paid a total underwriting fee of $500 million, with Goldman Sachs and Morgan Stanley each receiving $100 million, even though both investment banks had virtually no involvement in the pricing stage.

Secondly, the authority for share distribution. The lead underwriter still controls the majority of the share allocation decisions, independently filtering which investors can participate in the subscription.

Next is risk bearing. SpaceX adopted a full underwriting model, with the investment bank signing a contract to take on all the issued shares for external distribution. If market demand collapses and subscriptions are insufficient, all unsold shares are assumed by the investment bank, and SpaceX does not need to bear the loss. On-chain platforms cannot take on such massive bottom-line risks.

Finally, market stability. During the initial period of listing, when stock prices are highly volatile, the lead underwriter can exercise the green shoe option to moderately oversell shares and then repurchase in the secondary market to curb price surges and drops. Following SpaceX's listing, Morgan Stanley is responsible for post-listing stabilization operations. This business requires a substantial balance sheet and a professional market-making team, which only investment banks can provide at this stage.

Aside from these, all other segments of the entire listing process have been taken on by new market channels that are more cost-effective, longer in trading duration, and completely transparent.

Blockchain pricing channels have validated their own value, capable of continuously calculating the valuation of companies planning to go public at all times, with efficiency far exceeding traditional investment banks. SpaceX's significantly oversubscribed amount resulted in a first-day price increase of nearly 19%, representing a textbook-level listing scenario, sufficient to prove the effectiveness of these new pricing channels.

The traditional IPO model has been thoroughly broken down, with each function handed over to the most efficient channel, and similar divisions of labor are occurring across various industries. The earlier article "Reconstructing Primary Market Valuation" mentioned that the market no longer waits for investment banks to provide valuations for private companies. Investment banks, which once monopolized two core businesses of pricing and share delivery, can no longer rely on these two standardized services to earn high fees in the new listing system.

Will Investment Banks' IPO Business Income Completely Shrink?

Not at all. SpaceX's underwriting fee rate of only 0.67% is not the core source of income for investment banks.

Based on the first-day price increase, SpaceX raised $75 billion, resulting in an unrealized profit of about $14 billion on that day. Most investors able to share in this profit are existing clients of the underwriting investment banks. Investment banks cannot directly stockpile shares, but they will strive to secure premium IPO allocations for clients to earn high trading commissions.

This is also the core reason why the low fee rate of 0.67% still attracted nearly twenty investment banks to compete for underwriting positions. The underwriting service fee has become a secondary income; share distribution rights, client-derived trading commissions, and long-term wealth management businesses are the core pursuits for investment banks in project competition.

The profit logic of investment banks is evolving from standardized, replaceable pricing services to scarce resources—IPO share subscription channels.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。