Seizing the opportunity, capital arbitrage, casting a wide net, and striking down from a lower dimension—Jane Street's four major tricks.

Written by: Maher, Foresight News

In May of this year, a 13F holdings report from Jane Street made the cryptocurrency market explode.

This mysterious quantitative giant on Wall Street suddenly reduced its holding of BlackRock’s Bitcoin spot ETF IBIT from 20.31 million shares (worth $790 million) by 71% to about 5.9 million shares (worth $225 million), with its FBTC holdings also declining by 60%. Its strategy holdings were directly cut down by about 78%. At the same time, it was quietly increasing its holdings in Ethereum ETFs totaling about $82 million.

A month prior, this company, "with no CEO, relying on mathematical models and extremely low latency," had just reported a quarterly trading revenue of $16.1 billion and a net profit of $10.3 billion—an average employee compensation of $2.68 million, nearly seven times that of Goldman Sachs. What does this mean in the crypto space? In 2024, Tether, the most profitable company in the crypto sector, is expected to make only $13 billion in net profit for the year. Hyperliquid's revenue per employee of $7.8 million ranks first globally, yet its total revenue for all of 2025 is merely $908 million.

What is it really aiming for in the cryptocurrency market? The answer lies hidden in years of systematic planning.

Wall Street's Mysterious Player, Behind-the-Scenes Operator of Major Crypto Figures

Jane Street was founded in 2000; it never manages client assets but only uses its own capital to trade on over 200 exchanges globally. It has no CEO and lacks a traditional hierarchy. Each trading desk and business unit is managed by one of the equity holders, but no single person holds ultimate decision-making power. Co-founder Rob Granieri (who is also one of the defendants in the Luna lawsuit) is regarded internally as "the top peer," but major decisions are made collectively by a broader leadership group.

Rob is the only founding partner still active among the four co-founders. Interestingly, it was Rob who personally recruited SBF, who later left to found Alameda Research and FTX.

Jane Street Co-Founder Robert Granieri

The earlier mentioned 13F document is just the tip of the iceberg. Over the past five years, it has already established itself as the invisible operating system of the liquidity infrastructure in the cryptocurrency market through its AP positions in spot ETFs, a ten-minute advance before the Luna collapse, suspected anonymous arbitrage addresses on-chain, and its widespread equity spreads across exchanges and DeFi protocols.

In 2017, Jane Street officially entered the cryptocurrency market, led by veteran Thomas Uhm, who had served for 22 years. In 2018, it launched an institutional-grade OTC trading platform JCX, supporting 24/7 trading of mainstream tokens, beginning to provide stable liquidity for institutional counterparties.

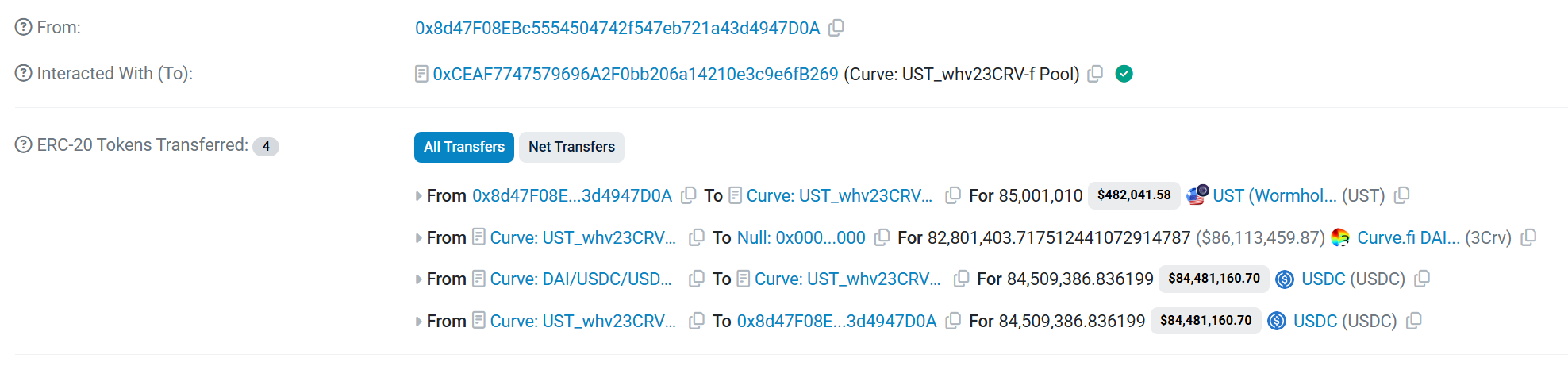

In May 2022, Terraform Labs quietly withdrew $150 million UST from Curve 3pool, and ten minutes later, a wallet associated with Jane Street withdrew 85 million UST from the same pool, triggering a death spiral with a market cap of $40 billion.

In January 2024, the Bitcoin spot ETF was approved. Jane Street became a core authorized participant (AP) for BlackRock’s IBIT, Fidelity’s FBIT, and WisdomTree ETFs. This means that behind every retail ETF subscription, there is Jane Street’s involvement.

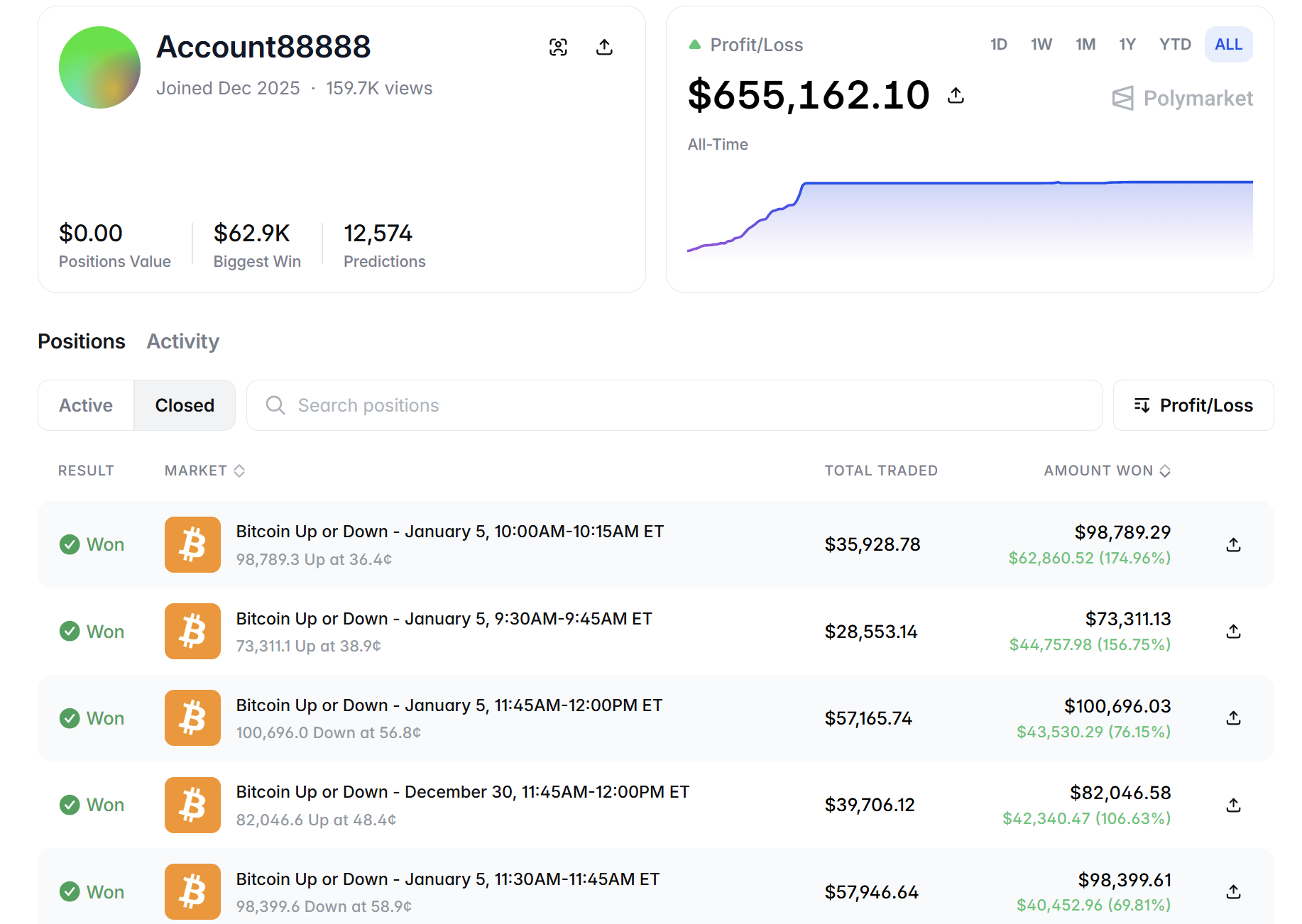

In December 2025, an address named “JaneStreetIndia” appeared in the “15 Minutes Bitcoin Price Guessing” market on Polymarket. This address employed a strategy of simultaneous betting on both rise and fall (locking in risk-free profits), earning nearly $360,000 within 25 days.

In terms of crypto infrastructure, Jane Street has marked its presence across crypto infrastructure: Kraken, 1inch (Series B at $175 million), Arbitrum, ZetaChain, Euler Finance, Kaito, among others. It also holds equity in mining stocks such as Hut 8, Bitfarms, and Cipher Mining.

Its core logic is to deeply embed itself in the liquidity infrastructure layer of the cryptocurrency market through methods like seizing opportunities, capital arbitrage, and striking down from a lower dimension, thereby stabilizing the extraction of “toll fees” and profits from information asymmetry.

The birth of the Bitcoin spot ETF marks the moment Jane Street steps into the spotlight.

Biggest "Pipeline" of Bitcoin Spot ETF

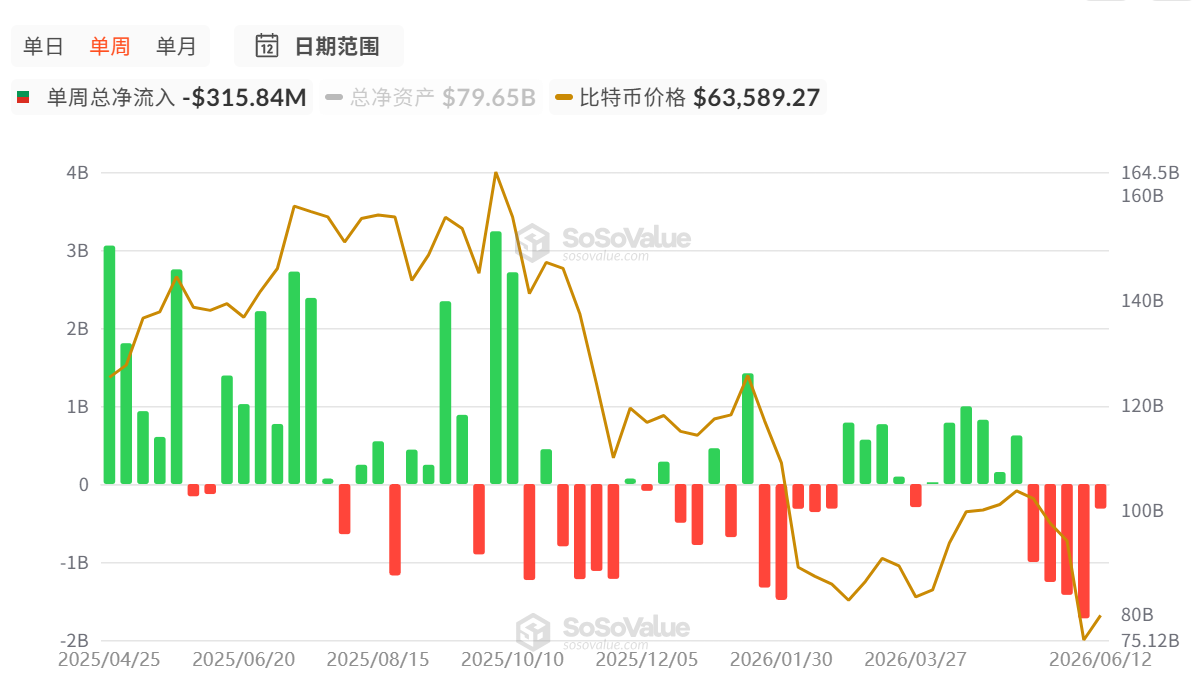

In January 2024, the U.S. SEC approved several Bitcoin spot ETFs. After the ETF approval, the influx of institutional funds exceeded expectations. According to SoSoValue data, as of June 16, there has been a total net inflow of $53.49 billion, and its inflow-outflow indicators have significantly impacted BTC prices.

In this $10 billion pipeline layer, Jane Street is the only name appearing in nearly all BTC ETF prospectuses—from BlackRock’s IBIT and Fidelity’s FBTC to WisdomTree, where it is either a core authorized participant (AP) or even the sole AP.

Retail investors buying IBIT on Robinhood can only trade at market price, while APs like Jane Street can directly knock on BlackRock's back door, exchanging a basket of Bitcoin spot for ETF shares, or return ETF shares to exchange for Bitcoin. This is what is commonly referred to as “creation” and “redemption.”

This "wholesale privilege" gives APs an arbitrage space inaccessible to retail investors: when IBIT's market price exceeds the net asset value of its underlying Bitcoin (premium), the AP buys spot Bitcoin → creates ETF shares → sells ETF on the market, pocketing the difference; when IBIT is at a discount, the reverse operation occurs. As long as there’s a deviation between ETF price and spot price, APs can engage in risk-free arbitrage.

What makes Jane Street unique is that it is not only an AP but also a market maker. It simultaneously exchanges shares with BlackRock at the "wholesale layer" while providing buy and sell quotes to retail investors at the "retail layer," thus profiting from the price difference on both ends. When the Bitcoin spot ETFs were approved in January 2024, all 11 applicants listed it as an AP in their prospectuses—Valkyrie even selected just two APs, one of which was Jane Street.

In the Q4 2025 13F document, Jane Street held approximately 20.31 million shares of IBIT, valued at about $790 million. In Q1 2026, it sharply reduced its holdings by 71% (IBIT down to about 5.9 million shares, worth about $225 million), further cutting it by 71% in Q1 2026 to 5.9 million shares. In just three quarters, the IBIT positions fluctuated wildly like a roller coaster. Interestingly, in Q1, they increased about $82 million in ETH ETF.

It is important to note: this is not the holding curve of “long-term value investment”; it reflects the inventory volatility of a high-frequency market maker—positions fluctuate back and forth with arbitrage opportunities; fill up when opportunities arise and withdraw when premiums converge. This is how they make money.

Former hedge fund manager Michael Green commented on this: "Seeing someone interpret Jane Street's 13F as a bullish signal makes me uneasy. These positions are almost certainly hedged with undisclosed options and futures; they are not building positions in Bitcoin, this is standard market making."

Additionally, besides Bitcoin and Ethereum, the SOL ETF has also been reported to have Jane Street as a market maker.

Compared to other market makers, Jane Street is particularly strong in complex or non-mainstream ETFs (like fixed income, international equities, commodities, and crypto ETFs). By combining quantitative techniques and fundamental/correlation analysis, they convert ETF demand into correlation signals and hedging strategies, willing to hold positions longer to realize structural arbitrage.

In contrast, Citadel and Jump Trading are more inclined towards ultra-low latency pure technical high-frequency trading, with speed as their core competitive advantage. Jane Street's speed is not the fastest, but its risk management systems and balance sheets allow it to hold positions longer amidst volatility, thus earning price differences that others cannot hold long-term.

When it simultaneously serves as the authorized participant for IBIT, FBTC, and several Ethereum ETFs, it collects not directional bets’ returns but rather the “toll fees” generated by the entire institutionalization process in crypto—every subscription, every redemption, and every arbitrage balance is completed through Jane Street's pipeline.

However, this model faced backlash in the Indian market.

In July 2025, the Indian Securities and Exchange Board of India (SEBI) issued a temporary ban against Jane Street-related entities on grounds of market manipulation, freezing around 48.4 billion rupees (approximately $566 million) in assets. SEBI's 105-page ruling accused Jane Street of systematically manipulating the Indian Bank Nifty index during 18 derivatives expiry dates from January 2023 to March 2025 by employing tactics of “lifting index constituent stocks in the morning, simultaneously establishing large short options positions, and then crashing the market in the afternoon to cash in on options profits,” recording a loss of about $7.5 million on the spot market while profiting roughly $89 million from the derivatives side.

This compliance giant hides its sharp tools, and insider front-running has landed it in considerable controversy.

The Critical 10 Minutes, "Igniter" of the Luna Crash

On February 23, 2026, Terraform Labs bankruptcy administrator Todd Snyder submitted an 83-page lawsuit in the U.S. Southern District Court of New York, with defendants including Jane Street Group LLC, Jane Street Capital LLC, co-founder Robert Granieri, and two employees, Bryce Pratt and Michael Huang.

The crux of the accusation is that before the May 2022 Terra collapse, Jane Street obtained early knowledge of the liquidity crisis through an insider information channel and completed a precise withdrawal of $85 million UST within ten minutes, thus avoiding over $200 million in losses and attempting to buy Luna at a significant discount after the collapse.

Bryce Pratt had interned at Terraform Labs and later joined Jane Street. He established a private group chat named “Bryce's Secret,” connecting Terraform's internal engineers with Jane Street’s trading desk. Through this channel, Jane Street learned the specific time and amount for the withdrawal from Curve 3pool before Terraform publicly announced it. For a quantitative trading company, this “time difference” represents an arbitrage opportunity.

At 17:44 on May 8, 2022, Terraform Labs withdrew $150 million UST from Curve 3pool, an operation that at the time was not publicly announced (transaction hash 0x18bd477f9beeff22b2ad0c6d48a9c0f02b542049789f0638f5ec50365f1d1de7).

Thirteen minutes later, a wallet identified in the lawsuit as being associated with Jane Street executed a redemption operation for 85 million UST from the same pool (transaction hash 0xaa23df48c53f221d0e8ac60ffc9e69340f3e8948fcdc936f3aee9c887d802abb). This was one of the largest single redemptions ever on the Curve platform.

The logic of the lawsuit is that if Jane Street had not been privy to Terraform's plan in advance, it would not have been able to execute such a precise and substantial reverse operation within ten minutes after Terraform completed a large withdrawal. Normal quantitative models require reaction time, yet this wallet responded in just ten minutes.

More crucially, after Terraform’s withdrawal, the liquidity of 3pool had been significantly weakened; withdrawing another 85 million at this point equated to giving a kick to a shaking table, directly shattering market confidence and triggering the UST depegging.

By withdrawing in advance, Jane Street avoided significant depreciation of its held UST and Luna-related positions in the death spiral. The specific figure given in the lawsuit is over $200 million. The plaintiffs made 13 legal claims, covering insider trading, securities fraud, violations of the Commodity Exchange Act, unjust enrichment, and breach of confidentiality obligations, seeking damages and recovery of all illegal gains.

On April 23, 2026, Jane Street submitted a 39-page motion to dismiss with three core defenses:

- Terraform itself committed fraud of billions of dollars, and the bankruptcy party cannot shift the disaster onto others;

- The on-chain operations of Terraform were itself publicly visible; the ten-minute window does not constitute non-public information;

- Its largest single transaction occurred after Terraform's liquidation rather than before. A company spokesperson described it as "a desperate lawsuit and baseless extortion."

The 2022 collapse, viewed by countless as a "black swan" in crypto, is gradually revealing another face under the legal scrutiny post-incident: while retail investors rushed to escape, institutions closest to core information may have already been standing at the exit long before.

Prediction Markets Don't Guess Up or Down, Only Collect Time Tax

If the aforementioned three dimensions represent Jane Street's overt layout in the crypto world, its potential impact in on-chain prediction markets constitutes a covert dimension that is increasingly worth noting yet harder to quantify.

As traditional quantitative giants extend their tentacles into native on-chain markets, attacks from a lower dimension occur. Polymarket—a prediction market platform that processed over $9 billion in transaction volume in 2024 and surpassed $13 billion in 2025—has become the latest target.

Ironically, Jane Street, which was heavily fined and expelled from the market by the Indian SEC in 2025, seems to have quickly found a new outlet in the anarchic prediction markets of crypto.

In December 2025, an address named JaneStreetIndia appeared in Polymarket’s 15-minute Bitcoin price guessing market.

According to on-chain statistical analysis, this account operates as a high-frequency trading bot, detached from the "predictions" of regular players, being purely mathematical and delay arbitrage.

This account primarily targets event contracts: it hardly touches long-term political elections or cultural events, focusing entirely on the “15 minutes cryptocurrency price up or down,” a market of extreme frequency, high volatility, and rapid result determination.

Transaction frequency and success rate: according to recent on-chain statistics, this account executed over 11,000 transactions within its first two months of operation. Even more terrifying, its success rate has consistently remained above 95%. In the earliest 25 days of exposed data, it made a profit on 23 out of those 25 days.

On-chain data statistics show that this address earned $360,000 in the first 25 days, and after two months of running, its total profit rapidly surged to about $645,000.

This approach starkly contrasts with the early scrappy individual traders on Polymarket. At the beginning of 2024, an anonymous developer named @defiance_cr operated a market-making bot on Polymarket with a $10,000 principal, earning $700 to $800 daily, with an annualized return of about 2700%. However, by early 2026, he chose to open-source his code and exit, citing that profit was no longer feasible under current market conditions—because institutional-level competitors had entered the arena.

It should be stated initially: as of now, no blockchain analysis platform has officially labeled this address, and Jane Street has never publicly acknowledged its relation to this address. All associations are based on on-chain behavior speculations. However, the following speculations most likely point to Jane Street.

This address earns using the disparity between the buy-up and down settlement prices. Essentially, it employs the same convergence arbitrage logic as the spot ETF, but adapted for different markets.

This address executed more than 11,000 transactions, boasting an almost 100% success rate. Human traders cannot maintain such discipline in 25 days; only those with institutional-grade computing power and low-latency infrastructure can continue harvesting in such a squeezed environment.

Furthermore, a change from identifiable institutional identifiers to completely meaningless digital strings typically leads to retail traders boasting or abandoning them once attention grows; however, opting for the most covert renaming path to continue operation aligns more closely with typical operational manuals of institutional compliance departments: no justification, just concealment.

Jane Street's core competitive advantage is its extreme low latency (FPGA hardware, microwave networks, optical fiber infrastructure). The 15-minute guessing market features an extremely short cycle requiring high demands on latency—while retail investors are still refreshing the page, the bot has already completed ordering, hedging, and settlement. The choice of a 15-minute short cycle instead of long-term predictions indicates that its strength lies in speed rather than judgment, which aligns closely with Jane Street's DNA.

So why is it unlikely to be other quantitative institutions, like Jump Trading or others?

In February of this year, Bloomberg reported that Jump Trading had secured shares in Polymarket and Kalshi through equity partnerships, forming a prediction market trading team of about 20 people; DRW recruited prediction market traders with a base salary of $200,000; SIG became Kalshi's first official market maker. These “regular troops” enter the market through compliance, equity, and team-building.

Conversely, Jane Street's entry method is anonymous, robotic, and zero-sum game-oriented. It does not seek platform cooperation but appears directly in the form of blockchain addresses, employing the most savage arbitrage strategies to harvest. This wild approach aligns more closely with how Jane Street acted during the Luna incident (information pre-positioning, discreet execution, denial afterward).

For Jane Street, Polymarket is not an experimental ground requiring belief in the "decentralized prediction market ideal" but rather a brand-new, illiquid, pricing-discrepant volatility surface—subsequently harvested.

What emerges here is a deeper structural problem: when an institution simultaneously possesses priced authority in the spot market, participation ability in the derivatives market, and potential liquidity influence in the prediction market, an information and capital closed loop forms between the three layers of markets, theoretically enabling highly synergistic profit acquisition.

Even if all operations remain within a legal framework, the information asymmetry stemming from such multi-layer penetration is sufficient to place ordinary retail investors at a significant disadvantage in trading decisions.

This is not a conspiracy theory; it is the reality of financial market structure.

Conclusion

Jane Street is not an institution investing in crypto. It does not bet on Bitcoin's price movements, does not care which public chain prevails, and is not concerned about whether decentralized ideals are realized.

Looking back on its multiple layouts, what it earns from the trillion-dollar doors of Bitcoin spot ETFs is not returns from Bitcoin appreciation but rather the tolls accrued from the basis between ETF shares and spot net asset value. Within the ten-minute window of the Luna collapse, it gained early knowledge of the collapse's coordinates, avoiding significant losses. At the infrastructure level, it casts a wide net over Kraken, 1inch, Arbitrum, and Bitcoin mining stocks—not betting on who wins; just ensuring it maintains the power of infrastructure discourse no matter who wins. In Polymarket's 15-minute guessing market, it has turned the prediction market into another volatility harvesting machine.

Operators never stand in the spotlight. When operators become the infrastructure itself, the market no longer needs operators.

It has become the market.

When top traditional Wall Street players comprehensively penetrate into DeFi, OTC, and even native on-chain prediction markets like Polymarket, is the “permissionless, retail-friendly” alpha space that the crypto world prides itself on being permanently erased? When so-called genius individuals have to open-source code and exit the game, has the crypto industry really matured, or has it entirely devolved into a new pool of flesh and blood for Wall Street?

Perhaps there is no universally recognized answer.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。