SpaceX is a great company, there is no doubt about that; however, great companies also need to be bought at the right price to make a proper investment.

Introduction: Starting with the chaos in the cryptocurrency world

On June 12, 2026, Eastern Time, SpaceX officially landed on the Nasdaq, with the stock code SPCX. Despite the company's reported net loss of about $4.9 billion for the entire year of 2025, the stock did not open below the issue price on the first day, contrary to many expectations. The issue price was set at $135, jumped to $150 at opening, continued to rise during the trading day, reaching a peak of $176.52, and finally closed at about $161, up approximately 19% on the first day.

The company's market capitalization reached $2 trillion, making it the sixth largest publicly traded company in the United States by market value, and this issuance also set a record for the largest IPO in human history.

Data source: Nasdaq Exchange

In stark contrast to the excitement of traditional markets, voices of complaint echoed from the cryptocurrency world. Multiple exchanges previously launched massive promotions to attract users through tokenized IPOs, but almost all failed to deliver on the day of the listing, with the core reason being: the quotas for the underlying shares were not received in time.

Upon analysis, platforms that connected through Kraken's xStocks channel almost universally failed to secure adequate shares.

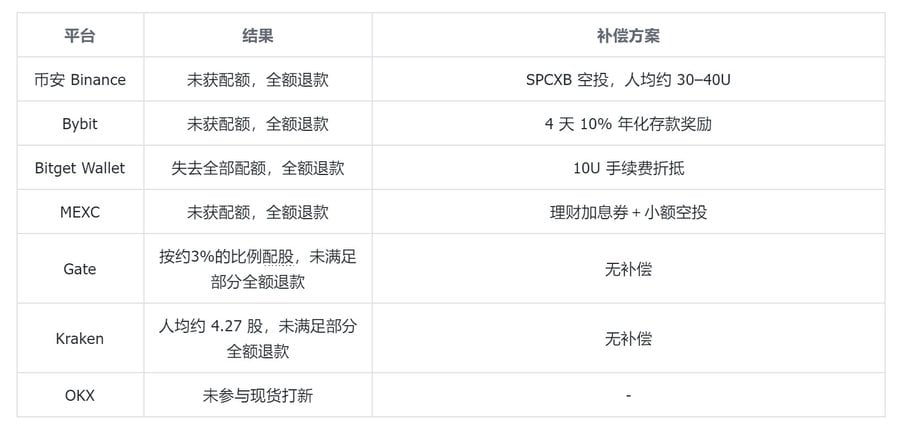

Data source: announcements from various exchanges on Twitter

Specifically:

- Binance canceled its tokenized IPO activity and issued full refunds, in addition to airdropping SPCXB tokens worth approximately $1 million as compensation, with an average value of about $30 to $40 per user;

- Bybit also issued full refunds and provided an additional deposit incentive of 10% annualized for 4 days;

- Bitget Wallet lost all its quota due to its connection with xStocks, ultimately offering full refunds to users and providing around $10 as a fee offset;

- Kraken utilized a proprietary brokerage channel, distributing fixed small shares to all subscribing users, averaging about 4.27 shares, with any unmet portions receiving full refunds.

In other words, the results of the IPO offered by several platforms generally fell below users' initial expectations.

The common failure was clear: platforms that bet on the xStocks channel collectively fell short, as SpaceX was oversubscribed by about four times, and the underwriters provided very limited shares to the cryptocurrency channel. The supply bottleneck actually originated from Kraken's own acquisition of the tokenized stock business xStocks at the end of 2025.

It is worth mentioning a platform called MSX (MaiTong MSX). During the SPCX IPO, MaiTong behaved differently from other exchanges, as it continued to open quotas to users at full value or even below the issue price—this raised concerns within the community—MaiTong explained that this was due to the quotas obtained through Republic.

However, Bitget's CEO Gracy pointed out that Bitget had an exclusive partnership with Republic, implying that MaiTong did not have a cooperation agreement with Republic.

Subsequently, there were numerous doubts in the community, leading to speculation about whether its quota sources were "electronic plate," and concerns about the platform's ability to fulfill obligations and potential concentrated withdrawals.

This round of debate in the cryptocurrency world can be put aside for now. Regardless of whether the IPO channels are trustworthy, what truly determines the profit and loss of an investment is the intrinsic value of the company and the price paid for entry. Therefore, the following will return to the company SpaceX, sequentially addressing three questions: Is it worth buying at the current price level? Does its valuation logic hold up? What are the likely price movements post-IPO?

1. SpaceX: A prospectus with a celestial tone

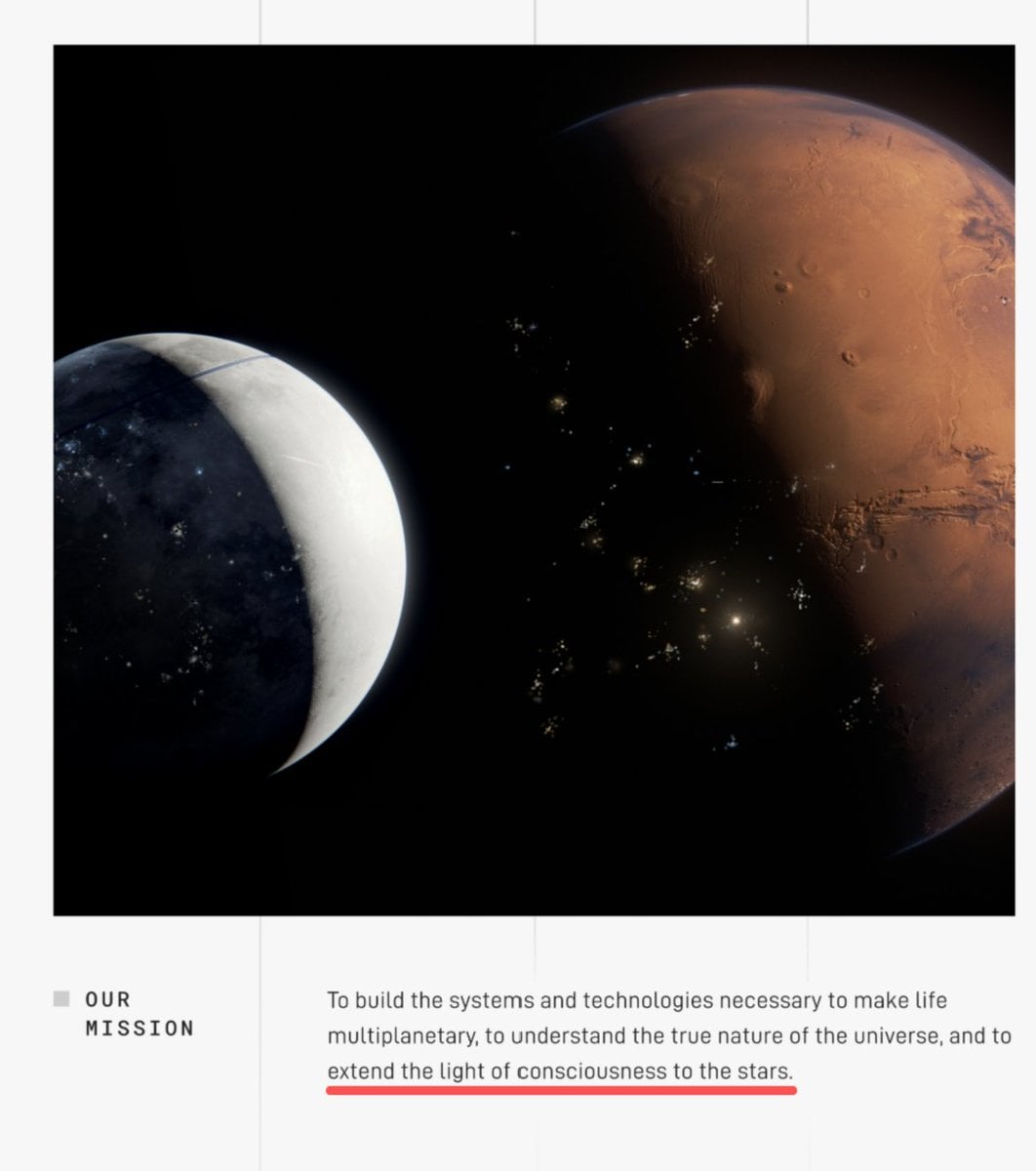

Space Exploration Technologies Corp. (SpaceX), to understand this company's opening, one might start by reading the first page of its prospectus. In the S-1 document submitted to the U.S. Securities and Exchange Commission (SEC), SpaceX's mission is expressed in a sentence that hardly reads like a financial document:

The mission of the company is to build systems and technologies necessary to make life multiplanetary, to understand the true nature of the universe, and to extend the light of consciousness to the stars.

Source: SpaceX Form S-1, SEC EDGAR (Original text: “to make life multiplanetary, to understand the true nature of the universe, and to extend the light of consciousness to the stars”)

The prospectus goes on to explain that xAI was established in 2023 and acquired by SpaceX in early 2026, now serving as a pillar in the company's vertically integrated system; the company plans to deploy AI computing satellites in orbit as early as 2028.

A rocket-making company mentions the sun, computing power, and consciousness in the first paragraph of its prospectus; this narrative strength is part of the pricing itself and also the starting point for all subsequent debates.

Source: SpaceX pricing announcement, CNN, NPR, The Motley Fool, June 2026

On the listing day, the stock opened at $150, peaked at $176.52 during the day, retreated at the close, and finished at about $161, up approximately 19.3% from the issue price. Based on the closing price, the company’s market capitalization surpassed $2 trillion, and Musk's personal net worth also crossed the trillion-dollar mark for the first time. The table below summarizes the key numbers.

The significance of this day is not just the increase, but structurally, it was a fine supply-demand imbalance. The issued Class A shares accounted for only about 4% of the company's equity; the rest remained locked up; approximately 30% of the issuance (about $22.5 billion) was allocated to retail investors. In other words, the entire $17.5 trillion company was priced through about 4% of its circulating shares, with most sellers locked out of the market—this point will recur in the following discussions, explaining both the strength on the first day and laying the groundwork for future volatility.

2. Valuation Breakdown: Why dare to value at $2 trillion?

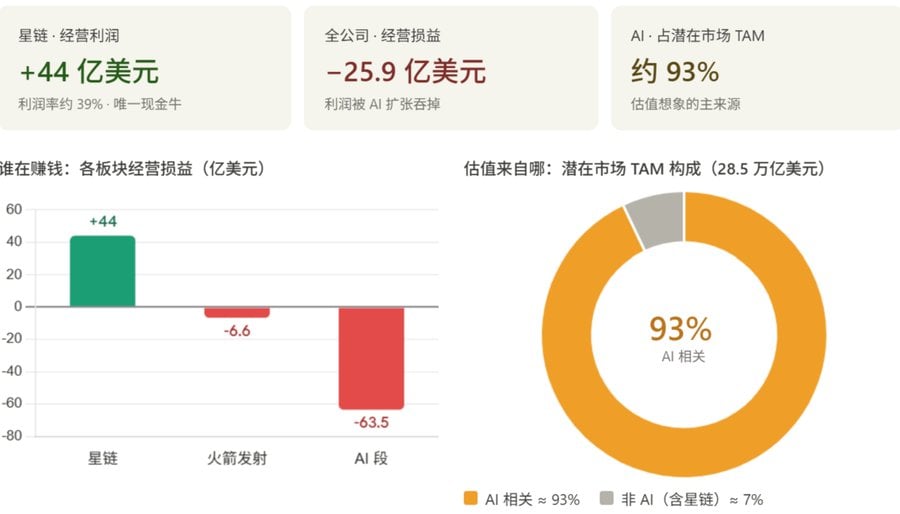

To understand the $2 trillion pricing, it is necessary to break down SpaceX into three business segments, as their profitability status and valuation logic are completely different. According to the S-1 disclosure, the company had a consolidated revenue of $18.674 billion in 2025, an operating loss of $2.589 billion, and an adjusted EBITDA of $6.584 billion; the net loss was about $4.9 billion.

Financial comparison of SpaceX's three major business segments (Source: SpaceX Form S-1)

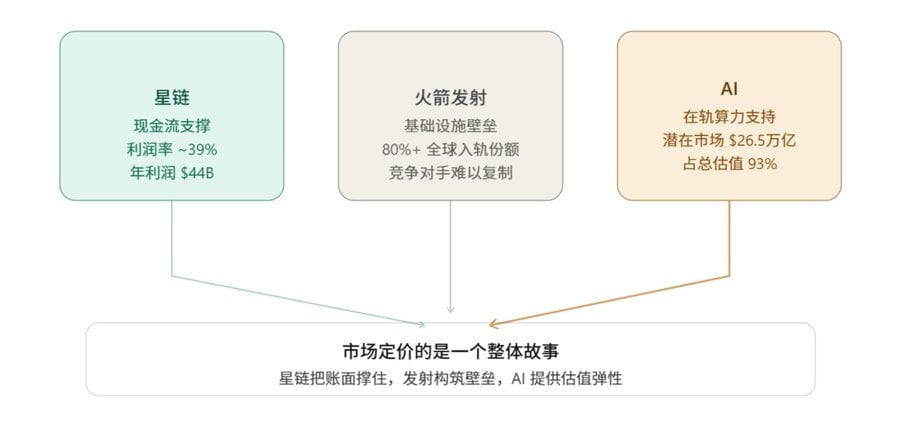

The first segment is rocket launches (the Space segment). This is SpaceX's core business and the most familiar part to the public, but it does not actually make money on its financial statements. In 2025, this segment generated about $4.1 billion in revenue, a year-on-year growth of only about 8%, while it recorded an operating loss of about $657 million, mainly dragged down by R&D investments in the next-generation Starship—just the R&D expenditure for Starship in 2025 was nearly $3 billion.

The second segment is Starlink (classified under Connectivity), which is the actual profit-maker and the engine supporting the company’s cash flow. In 2025, this segment generated about $11.4 billion in revenue, accounting for about 61% of the company’s total revenue, and generated about $4.4 billion in operating profit, with an operating margin close to 39%. As of the end of March 2026, Starlink had approximately 10.3 million users, covering over 160 countries and regions, with around 9,600 satellites in orbit. The key to its business model lies in the scale effect: once established, the marginal cost of adding a subscriber is very low, meaning the more users, the more room for profit margin expansion.

The third segment is the AI business, which has the greatest valuation imagination while also consuming the most capital. This segment, incorporated from xAI in February 2026, includes the Grok large model, X platform advertising and subscriptions, and Colossus data center computing power. In 2025, this segment generated approximately $3.2 billion in revenue but recorded an operating loss of about $6.35 billion—essentially consuming the profits earned by Starlink.

Source: SpaceX prospectus

Based on the above information, we can draw two conclusions:

- The greatest driving force behind SpaceX's IPO is actually AI, rather than "rocket launches" themselves. Therefore, SpaceX also belongs to an important layout within the AI narrative—this is also a significant manifestation of the concerns about the "AI bubble."

- What SpaceX is truly selling to investors is not the current financial reports, but a blueprint: using Starship to send data centers into orbit to directly collect solar energy to power AI, bypassing the constraints of terrestrial power grids. What the company is actually selling is the concept of a "cosmic-grade AI data center," not the rocket itself or the AI large model—while the prospectus marked the company’s potential addressable market (TAM) at $28.5 trillion, with about 93% tied to AI-related sectors.

Looking at these three segments together clarifies the valuation logic of SpaceX: the market is not pricing a rocket company or a satellite broadband company; rather, it is packaging the cash flow from Starlink, the moat built by launches, and the long-term vision for on-orbit AI computing power into a single story for pricing: Starlink is responsible for sustaining cash flow on paper, rocket launches are responsible for creating irreplicatable capability barriers, and AI is responsible for providing upward elastic space.

However, the question is: how much is this elastic space really worth?

3. Valuation Support Points: Two Power Contracts and a Cash Flow Base

High valuations require verifiable profit anchors. In SpaceX's S-1 prospectus, there are indeed a few clues that support the narrative: two signed computing power lease agreements, plus the subscription-based cash flow continuously generated by Starlink.

Main profit support points for SpaceX (Source: SpaceX Form S-1, DatacenterDynamics, Markman Capital Insight)

Anthropic's $15 billion computing power contract: According to the S-1, Anthropic is indeed continuously paying SpaceX monthly for computing power, which amounts to $1.25 billion per month for the computing power in the Colossus data center located in Memphis. The contract states it runs until May 2029, with an annualized total of about $15 billion and a total amount exceeding $40 billion over the contract period.

Google's $11 billion computing power lease: Google signed the second computing power lease, paying about $920 million monthly for around 110,000 GPUs and supporting computing power, effective from October 2026 to June 2029.

Cash flow base and pricing shift: Apart from the above two large contracts, Starlink itself is the most stable source of revenue for the entire company. In the first quarter of 2026, the Connectivity segment's operating profit reached $1.188 billion, with the number of subscription users as of the end of March being 10.3 million. In May 2026, SpaceX raised prices on all Starlink service plans, with increases of up to $10 per month, marking a shift in company strategy from exchanging price cuts for scale to monetizing its massive user base.

Adding up the above three sources of certain income, SpaceX is expected to earn at least about $40 billion in a year—this figure itself significantly surpasses its total revenue of $18.7 billion for 2025.

4. Questions: Small Print in Contracts, Ridiculous Multiples

After outlining the support points, it is also essential to examine its valuation weaknesses: for SpaceX to fulfill this valuation, the difficulty is indeed very high, for three reasons.

Contracts written through 2029 can be terminated at any time

The two computing power contracts appear to secure years of revenue; however, there is a crucial line in the terms: either party may terminate the agreement with 90 days' notice. Furthermore, Musk clarified publicly on X that Anthropic's arrangement is essentially a 180-day lease; thereafter, both parties have rolling 90-day cancellation rights. Similarly, the Google contract can likewise be exited 90 days ahead of December 2026.

This means that treating about $26 billion in annual computing power revenue as a definite contract reserve for valuation is unfounded: a lease that can be canceled in 90 days corresponds to completely different cash flow certainty than a long-term contract locked until 2029. Any valuation model treating it as a certain backlog will be undermined by this line of small print.

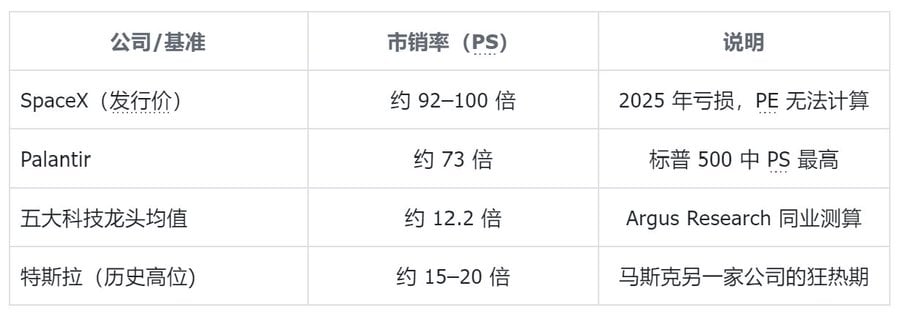

Price-to-sales ratio nearing a hundred times: How ridiculous compared to history

From the perspective of multiples:

First, the company is currently operating at a loss, making price-to-earnings (PE) calculations impossible.

Second, if calculated using the widely adopted price-to-sales (PS) method for tech companies, the company's $1.75 trillion issuance value corresponds to about $18.7 billion in revenue for 2025, leading to a PS ratio of about 92 to 100 times.

Horizontal comparison of price-to-sales ratios (Source: Investing.com)

For reference, the average price-to-sales ratio of the top five tech giants in the U.S. stock market is around 12.2 times; the highest price-to-sales ratio in the S&P 500 is about 73 times for Palantir. This means that upon its listing, SpaceX's price-to-sales ratio was about 30% higher than the most expensive stock in the S&P 500.

Historical experience does not support it either:

- According to data from Jay Ritter of the University of Florida, of 14 IPOs that had revenue exceeding $100 million and a price-to-sales ratio over 40 times, 12 underperformed the market in the three years following their IPOs.

- Another analysis reviewed over a hundred popular tech stocks and found that only about 8 had price-to-sales ratios that broke 100 times historically, and without exception, they all saw significant declines after peaking, averaging a drop of over 50% from highs to lows.

Thus, purely from the perspective of valuation and pricing analysis, there can be no doubt that SpaceX's valuation is excessively high.

What magnitude does doubling imply?

To take a reverse check from another angle: if someone expects SpaceX's stock price to double several times, they need to first understand what scale that corresponds to.

The current market cap already exceeds $2 trillion, ranking sixth in the nation.

- If the market cap doubles to about $4 trillion, it would be close to or exceed Nvidia, the highest valued company globally;

- If the stock price increases five or six times from the issue price, the corresponding market cap would reach the $10 trillion level, which would be equivalent to combining the market caps of several of the largest tech companies in the U.S. stock market.

Given that the company is still in a loss phase, its core profits rely solely on Starlink, and the computing power contracts can be canceled within 90 days, the difficulty of achieving such magnitude in the foreseeable future is evident.

This also accounts for the saying from many bears and institutions: while they scramble for quotas at $135, they write in their models: this price doesn’t hold up.

5. Short-term perspective: Index Inclusion and Timeline for Passive Buying

Sorting out the long-term valuation doesn’t necessarily mean there will be a short-term decline. On the contrary, due to modifications to an index rule, SpaceX is likely to experience support from forced buying of passive funds (ETFs) for a period after its listing.

Nasdaq indeed changed the rules "for him"

Historically, new stocks typically go through a stabilization period (seasoning) of three months to a year before qualifying for inclusion in major indexes; this window allows the market to complete price discovery and protects passive investors.

However, Nasdaq officially launched the "Fast Entry" mechanism in March 2026, effective from May 1: newly listed companies that rank in the top 40 by market cap can be included in the Nasdaq-100 within just 15 trading days after their IPO, waiving the previous requirement of at least a three-month stabilization period and restrictions—this is even seen as a modification specifically for SpaceX.

At the same time, the Nasdaq-100 also waived the minimum requirement of 10% for free float—this directly corresponds to SpaceX's merely about 4% extremely low liquidity ratio; otherwise, it would not qualify at all.

Other index providers have varying attitudes:

- FTSE Russell shortened the waiting window after an IPO to just 5 trading days—SpaceX has already qualified.

- Morningstar's CRSP index has introduced liquidity screening for mega IPOs—SpaceX can be included early.

- However, S&P Dow Jones announced on June 4, 2026, after a formal consultation, that it would maintain its 12-month stabilization period and GAAP earnings threshold—this means SpaceX will likely not enter the S&P 500 until at least mid-2027.

SpaceX's main stock index inclusion timeline (Source: SpotGamma, Morningstar, CNBC, ETF Stream, June 2026)

The core value of index inclusion lies in forced passive buying

This point is worth explaining separately: the essence of index inclusion is not an honor, but rather the triggering of "passive buying."

Once SpaceX is included in an index, all passive funds tracking that index—regardless of fund managers' opinions on its valuation—must unconditionally buy according to weight. This buying pressure is rule-driven and does not rely on active judgment, therefore it has high predictability and enforceability.

Inclusion in the Nasdaq-100 will directly trigger forced buying from the following major ETFs:

- QQQ (Invesco QQQ Trust, approximately $495.7 billion in size)

- QQQM (Invesco Nasdaq-100 ETF, approximately $98.5 billion in size)

SpotGamma analysts estimate that merely Nasdaq-tracking funds will need to purchase approximately $7 billion in SpaceX stock as forced buying on the inclusion day.

If we combine the QQQ, FTSE Russell, and Russell 1000 tracking funds, the recent mechanical buying scale ranges from approximately $22 billion to $27 billion—this figure already includes the passive funds resulting from early inclusion, and will flow in batches over the weeks following the listing, providing phased support for the stock price. If S&P 500 inclusion occurs in 2027, an additional $8 to $12 billion in passive buying will be added.

This enforced building of positions means that investors holding the QQQ ETF globally will automatically hold SpaceX, without making any active decisions.

Chip Structure: Heavily Locked and Low Circulation, Limited Short-term Selling Pressure

Passive buying describes the certainty on the demand side; looking at the supply side, the current chip structure is also tight, with limited selling power of circulating shares in the short term.

SpaceX's issued Class A shares account for only about 4% of the total equity, while Musk holds about 42% of the shares and 85% of the voting rights. Under such narrow liquidity conditions, even a modest scale of passive buying could produce an outsized effect on the stock price.

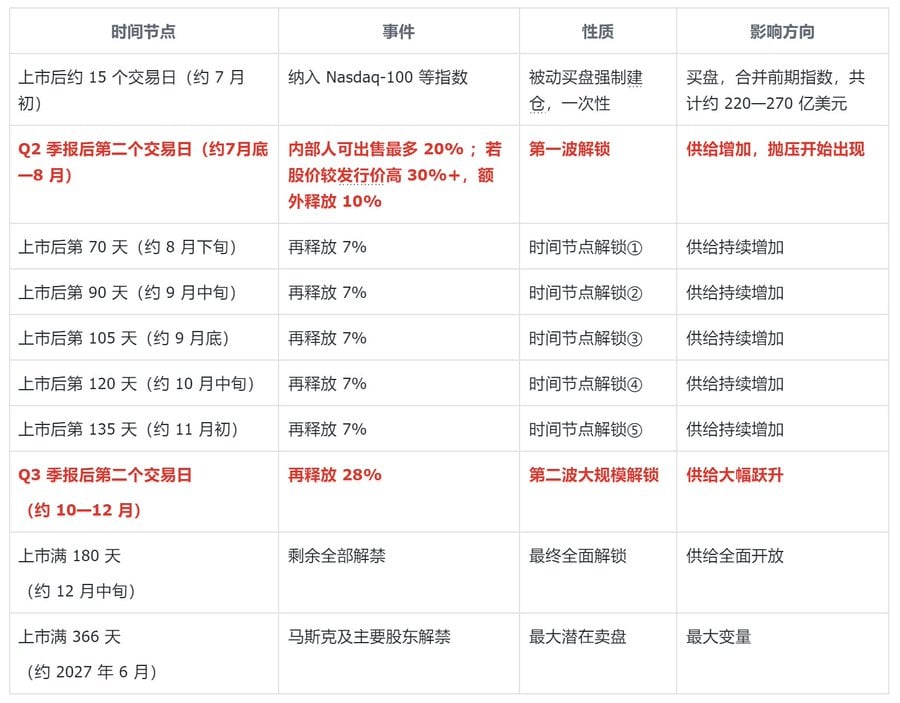

The lock-up period is designed to be stricter than conventional IPOs because SpaceX uses a tiered unlocking mechanism:

- Two days after the Q2 financial report is released, insiders can sell 20% of their shares; if at this time the stock price exceeds the issue price by more than 30%, an additional 10% can also be unlocked.

- Subsequently, about 7% will be released every roughly 15 days across five nodes (on days 70, 90, 105, 120, and 135 post-listing);

- After the Q3 financial report is released, an additional 28% will be unlocked, with the remaining portion opened fully after 180 days post-listing (around mid-December 2026).

- Musk and some major shareholders face separate restrictions, with a lock-up period lasting up to 366 days.

This structure means that large-scale sell-offs will not occur in the early days of listing but will be released gradually over time.

During the lock-up period prior to the Q2 financial report at the end of July, the shares that can be freely traded will be limited to that approximately 4% of circulating shares issued during the IPO phase. All insiders who held shares prior to this— including early employees and venture capitalists—must wait until the end of the lock-up period to sell.

Combining both supply and demand perspectives, the logic becomes relatively clear: in the weeks following listing, the demand driven by passive buying is time-constrained and regulated; meanwhile, the supply side is constrained by the lock-up period, with almost no conditions for large-scale selling in the short term. When these two directions overlap, it forms a more bullish chip structure for SpaceX at the start of its listing. The crucial time node to watch is the second half of 2026, when the lock-up period begins to expire in batches—at that time, supply will gradually unfreeze, and the market structure will experience a transition.

When will selling pressure emerge?

Understanding the rhythm of selling pressure first requires clarifying the true structure of SpaceX's lock-up period. From the end of July until the Q2 financial report in August, the first wave of unlocking has already started, with new chips gradually entering the saleable state every few weeks, thus pressure will be released progressively throughout the second half of the year rather than concentrated all at once in December. The lock-up period remains 180 days, but insiders (employees, early investors) can sell at multiple nodes during these 180 days in batches. In other words: selling pressure has actually begun since the Q2 report at the end of July, continuing throughout the second half of the year, not concentrated in December.

Key time nodes for SpaceX post-listing (Source: SpaceX Form S-1; CNBC; Darrow Wealth Management)

To summarize the above table in one sentence: buying pressure is one-off, but selling pressure is continuous.

The $22–$27 billion of passive buying resulting from index inclusion is a time-defined, measurable singular event; once completed, it ends—index funds will have bought what they needed and will not continue to increase purchases.

In contrast, the unlocking nodes start immediately after the Q2 report, with a new release window appearing approximately every two weeks, continuing throughout the second half of the year until the total release in December—each node represents a new supply release, and potential sellers merely need to choose a good window to sell during their respective periods, thereby making the pressure progressive and ongoing.

Institutions in the shareholder list include Andreessen Horowitz, Founders Fund, Sequoia, Alphabet, etc., among which Founders Fund and Valor Equity Partners have paper profits exceeding $60 billion; any behavior of exit by any institution, even if it's a small proportion, will be significantly impactful.

In summary, the trading structure in the second half of 2026 is essentially a confrontation between the time difference of buying and selling pressure: passive buying is concentrated within the first three weeks, while supply release from the selling side starts from the seventh or eighth week and extends until the end of the year.

- The window with the least overlap of the two (i.e., just before and after the Nasdaq inclusion) may represent the most bullish phase for the chip structure;

- Once entering the Q2 reporting period, the market will have to digest not only exhausted passive buying but also the continuous influx of unlocking selling pressure; that is the truly critical pressure range to watch.

6. Conclusion: A Great Company Does Not Equal the Right Price at This Moment

No one will deny that SpaceX is a great company.

It has monopolized global commercial launches, made Starlink a truly profitable satellite broadband network, and is attempting to move data centers into orbit—this level of integration is unmatched by any other company on Earth. The phrase written on the first page of the prospectus, “to extend the light of consciousness to the stars,” matches its engineering achievements.

However, a great investment is not simply about buying a great company. Buffett once wrote a repeatedly quoted phrase in his 1989 letter to Berkshire shareholders: to buy an outstanding company at a fair price. The key word in this statement is “fair price,” not “any price.” No matter how exceptional a company is, if the entry price is wrong, it simply does not constitute a proper investment.

Returning to SpaceX. Its nearly hundred-fold price-to-sales ratio, ongoing overall losses, reliance solely on Starlink for profits, and the two computing power contracts that can be canceled within 90 days, all indicate that the current valuation is already embedded with extremely optimistic future assumptions.

- In the short term, benefitting from an extremely low circulating price of about 4%, a 180-day lock-up period, and the enforced influx of passive buy orders from indexes like Nasdaq-100, the stock price has the potential to be supported or even to continue rising;

- However, this support, built on scarcity and one-off buying, is not strong—when the lock-up period expires and passive buying diminishes, the valuation is likely to undergo a correction toward its fundamentals.

Thus, adopting an investment mindset rather than an emotional one, a more prudent approach is to acknowledge its greatness while waiting for a more reasonable price. —Of course, from a speculative perspective, betting on its massive passive buy orders from index funds two weeks later makes sense. But one worry remains: is it possible that this valuation expectation has already been included in the $15 jump at opening?

Since most people in the market can discern that the current valuation is high and that a return to value will eventually occur, there is no need to rush in at the hottest narrative and tightest chips, but rather to wait for a pullback to present a true entry opportunity.

SpaceX is undeniably a great company; however, great companies also need to be bought at the right price to achieve a correct investment.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。