The distribution table decides who can see the opportunity, the allocation table decides who truly owns the opportunity.

Written by: Yacht

On June 13, SpaceX, known as the "strongest IPO on the planet," completed its initial public offering (IPO), unexpectedly becoming a major test for various cryptocurrency IPO subscription platforms. The platforms involved faced a fundamental yet daunting question:In the world's most proficient market for gathering liquidity, when faced with the world's scarcest stock quotas, who truly has the ability to turn funds into shares?

In recent years, the cryptocurrency market has proven its ability to connect stablecoins, wallets, exchanges, and global users into a single distribution network. An event can attract funds from different regions in a short time; users do not need to understand the complexities of cross-border remittances anew, nor do they have to adapt to the account systems of traditional brokers. In terms of "organizing demand," cryptocurrency platforms have already taken a seat at the distribution table.

However, the outcome of the SpaceX IPO illustrates that entering the distribution table does not equal entering the allocation table. Multiple platforms can receive funds, display subscription pages, and promise to strive for quotas, yet may not control the actual stock supply within the underwriter and licensed broker system. The front end can expand infinitely, but the underlying quotas cannot be created through oversubscription, segmentation, or technical packaging.

After a brief information explosion, according to summaries from existing industry media, cryptocurrency trading platforms Kraken and Gate ultimately distributed limited shares to some users, while Binance Wallet, Bybit, and Bitget Wallet ended the activity with refunds and various forms of compensation, but specific allocation ratios, compensation standards, and upstream relationships still showed divergences.

This uneven "Starship launch" exposed the gap between the imaginative tokenization of on-chain stocks and the reality of allocation capabilities. After cryptocurrency platforms brought global funds to the IPO doorstep, what is still lacking for them to transition from being asset distributors to effective participants in scarce shares?

In the most crowded IPO, what is truly scarce?

SpaceX is not a company that gains valuation solely from future stories. Rocket launches and recoveries, satellite internet, and the long-accumulated engineering system give it the attributes of a technology company, an infrastructure company, and a space contractor simultaneously. What it represents is not merely a listing, but a moment where years of private market value enters into public market pricing.

Because of this, the SpaceX IPO has been widely described as a historic capital market event. Many figures surround issue size, company valuation, Musk's wealth, and employee ownership, with discrepancies still existing among different public materials; but it is confirmed structural fact that market demand far exceeds the quotas that ordinary retail channels can reliably acquire.

Hot IPOs have never been publicly available products that can be bought simply because one has money. After a company goes public, it enters a continuous trading market, where qualified investors can buy when prices allow; however, the issuance shares before listing must first go through the allocation to underwriters, institutional clients, licensed brokers, and retail channels. Public trading resolves price discovery, while IPO allocation resolves how scarce resources enter different accounts.

This is also where SpaceX holds its appeal for the crypto industry. Crypto users lack neither risk appetite nor liquidity; what they lack is the identity, channels, and stable relationships of traditional primary markets. When exchanges and wallets place the SpaceX IPO entry next to stablecoin accounts, they offer not just a new product, but a ticket indicating that "crypto funds can also participate in top-tier IPOs."

The issue, however, is that the ticket is primarily a channel commitment, not the stock itself. Only when the upstream party genuinely obtains shares can subsequent tokenization, segmentation, on-chain operation, and secondary trading rest on an underlying asset. The more crowded the asset demand, the easier it is to magnify the distance between the ticket and the real seat.

What is scarce is not the stock symbol, but the issuing price

On the surface, a group of individuals who have long discussed decentralized finance suddenly starts competing for the stocks of a traditional company, seemingly forming a narrative regression. However, this understanding is overly simplistic. Crypto users have not left the on-chain world by purchasing stocks; they have merely begun to require on-chain accounts to accommodate more types of assets.

The development of stablecoins has changed the entry of funds. In the past, cross-regional investors entering the U.S. stock market had to navigate multiple frictions such as bank accounts, cross-border remittances, broker accounts, settlement times, and trading hours.Now, stablecoins allow purchasing power to first enter a globally liquid account system, later connected to securities exposure via trading platforms, broker API, or tokenized products..

This type of demand is not mysterious. When the crypto market enters a downturn, or when some users wish to diversify asset risk, they naturally seek assets with more mature business models and stronger market consensus. The growth of stocks, government bonds, money market funds, and other real-world asset (RWA) products essentially reflects crypto accounts shifting from "only holding crypto assets" to "managing multiple assets."

The differentiation between SpaceX's IPO and ordinary stock token transactions lies in one fundamental aspect. Users are not just competing for the SPCX price symbol that can be bought at any time after listing, but for the possibility of obtaining limited shares during the issuance phase. Whether they get allocated directly determines if users can share in the potential gains between primary issuance and subsequent market pricing, making refunds more easily interpreted as "missed opportunities" rather than just unsuccessful orders.

Therefore, the real significance of on-chain U.S. stocks is not merely converting stocks to a token symbol. It attempts to redo asset distribution: users still utilize stablecoins, wallets, and an interface that operates 24 hours, but underlying value comes from regulated securities, custody accounts, and traditional market price discovery. On-chain provides programmable settlement and global access, while off-chain provides asset rights, legal registration, and corporate actions.

IPO is the most difficult hurdle for stock tokenization

Stock tokenization is often described as a technical engineering task: placing stocks in custody accounts and then issuing products on-chain that correspond to their value. However, the truly difficult aspect often lies not in "how to mint," but in "who is qualified to buy, hold, and dispose of the underlying stocks."

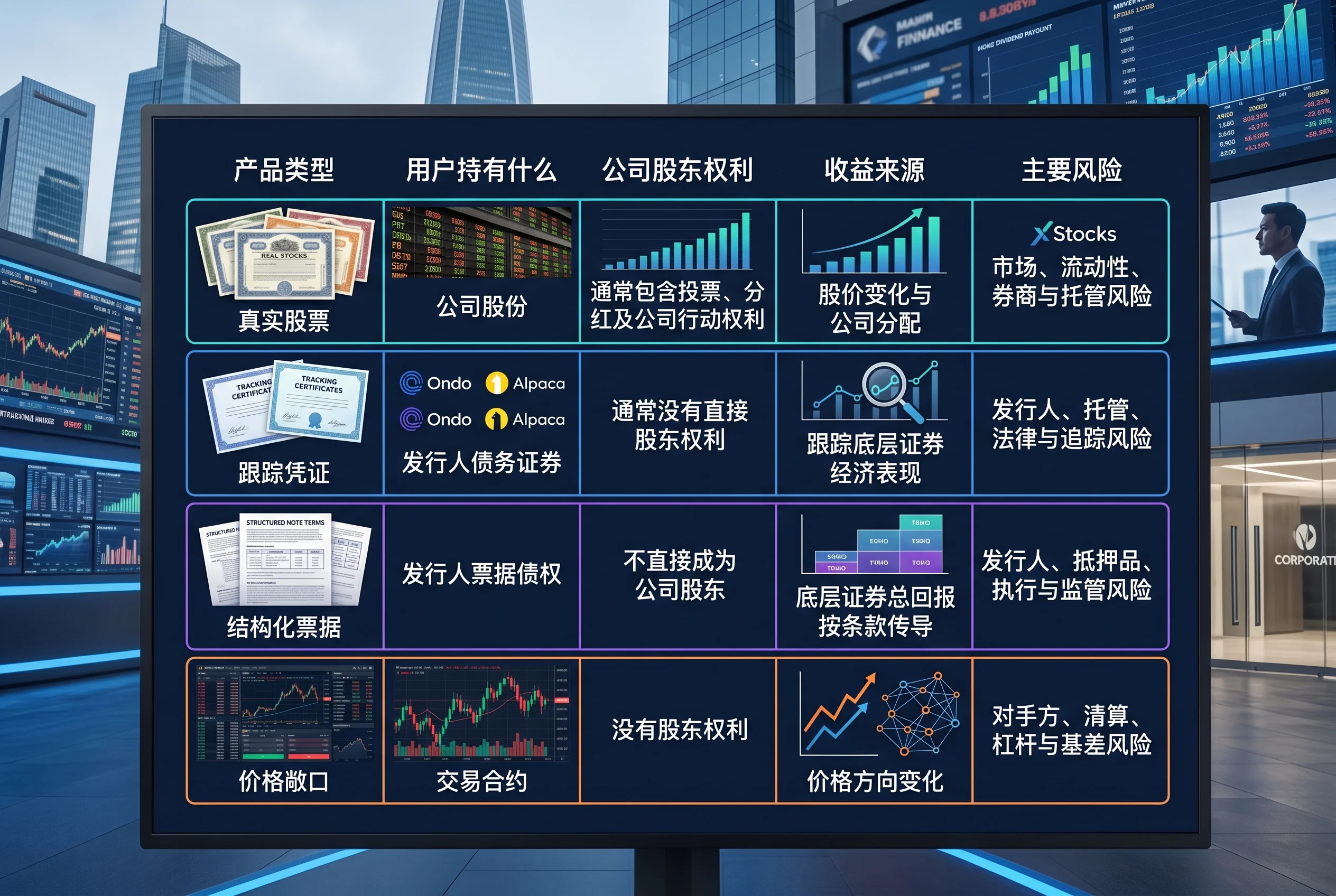

Taking xStocks as an example. xStocks is a system that packages the economic exposure of traditional securities as on-chain tokens, and its public documents define the related products as tracker certificates provided by independent issuers. Users obtain economic exposure that tracks the performance of the underlying securities, rather than directly becoming registered shareholders of the underlying company. Similarly, Ondo Global Markets is a product platform under Ondo that connects on-chain funds with traditional securities exposure, with products structured as notes tracking total returns from the underlying securities. Products can have underlying asset support and can also have custody, verification, and guarantee arrangements, but these arrangements do not equate to users directly holding stocks in traditional securities accounts.

Comparison of rights structures for real stocks, tracker certificates, structured notes, and price exposure

It is essential to distinguish between two types of capabilities. The first is asset conversion capability, which means packaging acquired stocks into products that are divisible, transferable, or can be settled on-chain; the second is asset acquisition capability, which means obtaining the real shares that the underwriting chain is willing to deliver when the IPO allocation occurs. The former can be continuously optimized through technology and product structures, while the latter depends on licenses, capital, compliance capability, and long-established market relationships.

From this perspective, there is a simple constraint in the primary market: it is difficult for scarce assets, non-discriminatory access, and full allocation to coexist. If the assets are sufficiently scarce and do allow global users to apply without discrimination, there will inevitably be proportional allocation, priority, or lotteries; if a channel can guarantee full allocation, it often means that the channel has pre-controlled sufficient shares, or the asset itself is not scarce.

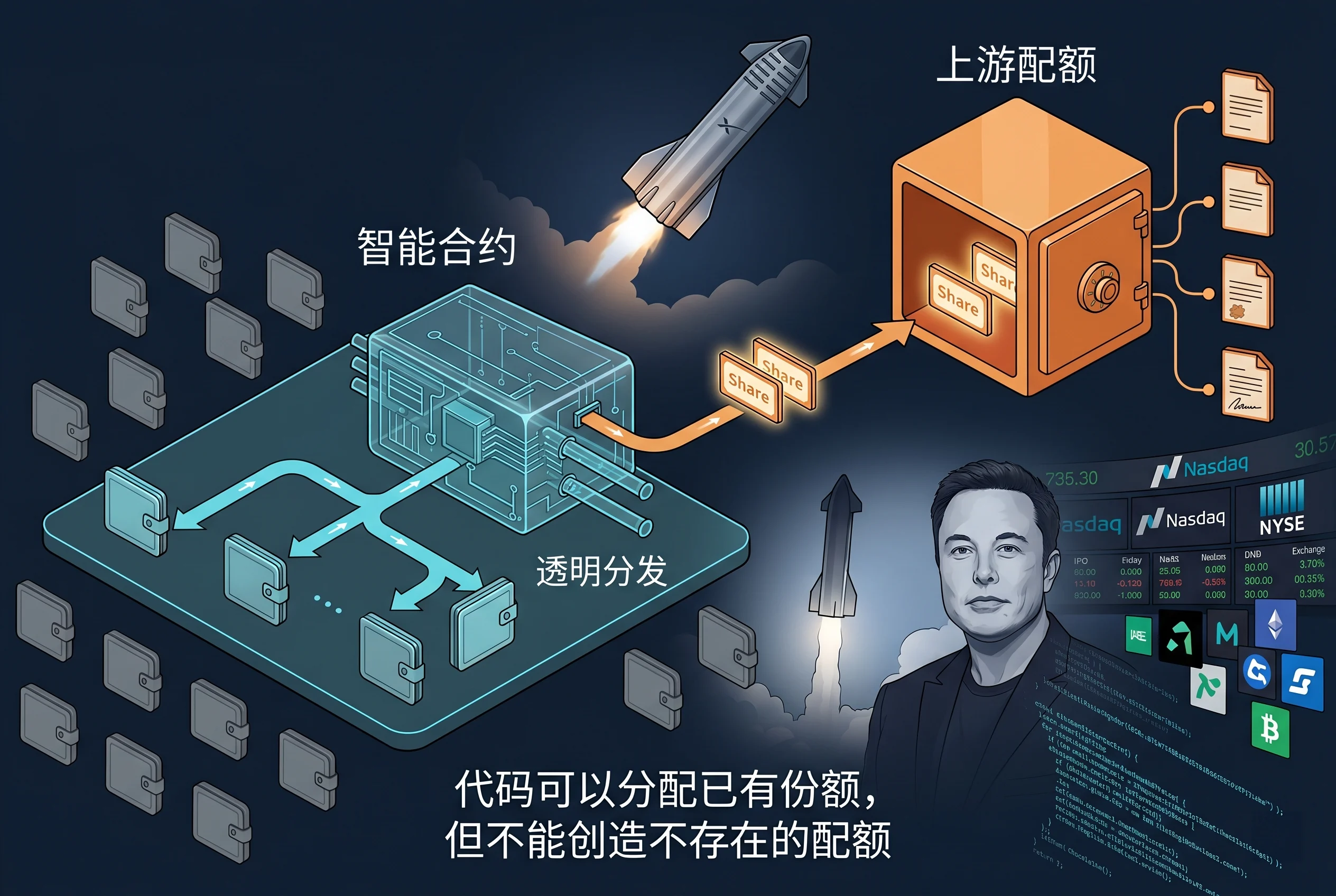

Blockchain can make distribution formulas public, ensure each fund's entry and exit is traceable, and can automatically execute proportional distribution after receiving total quotas. But code cannot mandate underwriters to deliver more stocks. Smart contracts can faithfully allocate "existing ten," but cannot create another ninety real shares just because there is a hundred share demand on-chain.

Thus, this pressure test does not signify a failure in stock tokenization on the engineering front. It proves that once tokenization enters the IPO stage, technical issues will yield to supply issues, and supply issues will ultimately revert to traditional finance's allocation structure.

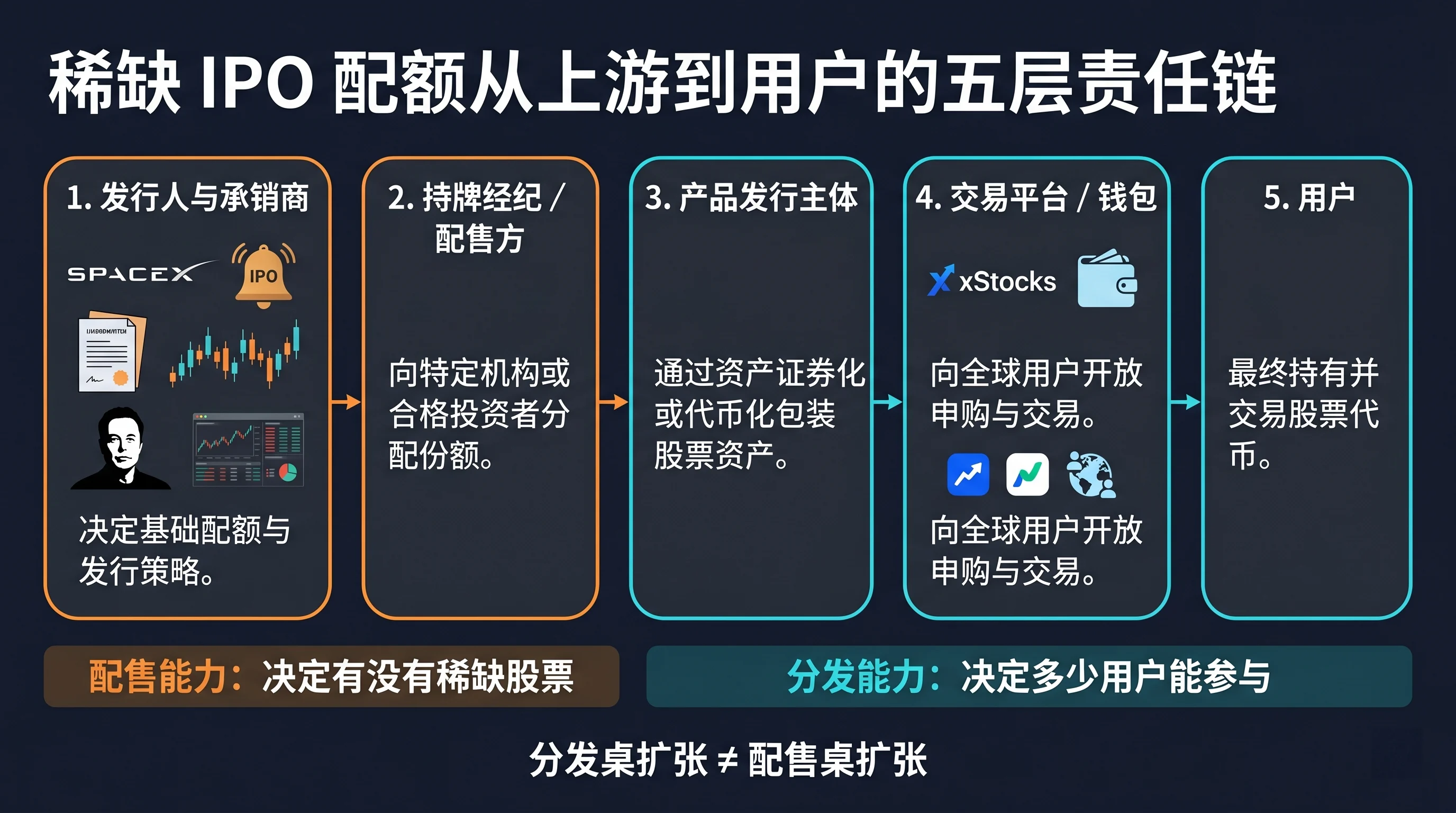

How many tables are there between SpaceX and users?

To understand the risks of crypto IPOs, it is necessary to break down the vague term "platform." The subscription button that users see in an application could connect to completely different entities behind the scenes.

Five layers of responsibility chain from issuer and underwriter to final user

The first table is the table between the issuer and the underwriter. SpaceX determines the issuance arrangements, and the underwriting system is responsible for pricing, sales, and share distribution. This level decides how many stocks are initially available in the market and which institutions and channels can acquire shares.

The second table is the table of licensed brokers and allocation participants. They can participate in securities transactions, account registration, clearing, and custody as regulated entities. Alpaca is a U.S. financial infrastructure provider offering securities trading, custody, and technology interfaces to fintech companies, with its securities business carried out by its corresponding licensed entities, while also providing infrastructure for wallets and tokenization platforms. The key point is not how fast a certain interface is but who records the securities, who clears them, and what rules apply in case of disputes.

The third table is the table of custody and product issuance. The issuer usually sets up special purpose vehicles (SPVs) to issue tracker certificates, structured notes, or other on-chain products based on the underlying securities, specifying how redemptions, transfers, corporate actions, and defaults will be handled. This level determines whether users receive stocks, debt securities, derivatives, or just price exposure.

The fourth table, then, is the distribution table of exchanges, wallets, and protocols. They have users, stablecoin balances, interfaces, traffic, and customer service systems, capable of packaging complex products into a nearly frictionless subscription experience. Users see the same brand, but the responsibility may fall on multiple legal entities.

In this chain, with each additional layer, efficiency may not decline, but information asymmetry increases. Users typically know which platform they are giving funds to, but may not know through whom the platform obtained quotas, who holds the underlying stocks, who issues the tokens, and who bears the obligation of refunds.

Therefore, judgment cannot stop at "Is there 1:1 support?" but must continue to question: Does the underlying asset already exist? Who verifies it? Who has the right to dispose of it? Can users redeem it? In case of bankruptcy of the issuer, who represents the holders in the claims, and does the front-end platform actually bear sales responsibilities or merely provide technical access?

Multiple answers, what kind of conclusion do we need?

According to existing industry media summaries, various platforms have roughly provided three types of answers: limited allocation, refunds while bearing the cost of capital occupation, and refunds followed by future rights offerings. They cannot be ranked solely based on compensation amounts, as different handling corresponds to different responsibilities.

Limited allocation, refunds while bearing capital costs, providing future rights post-refund

Kraken and Gate represent the first type of result: the platform indeed secured some allocatable shares, but user demand far exceeded the final allocation. Kraken's activity rules indicated the possibility of full, partial, or no allocation in advance, with unallocated funds returned to the usable balance; Gate performed proportional distribution based on the final limited quota obtained. Both completed the delivery from upstream shares to downstream users, but it also shows that even in a relatively forward distribution position, crypto users can still receive only a small portion.

Binance Wallet and Bybit represent the second type of handling. Neither ultimately delivered SpaceX shares to users but refunded subscription funds, bearing customer relationship costs in different ways. Binance Wallet used additional token airdrops; Bybit defined compensation as capital occupation rewards and automatically returned funds. The evaluation focus should not be on which provided "more," but on whether the announcement was timely, what rights the compensation actually entailed, and whether the platform fully transferred upstream failures to users.

Bitget Wallet is more aligned with the third type of route: beyond refunds, it also offers fee-related processing, on-chain fee vouchers, and future tokenized IPO whitelist eligibility. Such schemes can reduce some direct friction but also delay partial compensation to the next activity. Future rights only hold value if users continue to participate, the next activity truly occurs, and upstream performance is fulfilled, thus they should not be equated with cash refunds or actual stocks.

These varying answers expose that crypto IPO subscription is still in its early stages: the product structures adopted by platforms, upstream channels, and boundaries of responsibility are inconsistent, thus post-failure treatments are naturally difficult to standardize. However, one thing is certain: clear and consistent rules protect users better than compensation amounts. Regardless of the product structure adopted, platforms need to provide more mature examples in terms of transparency, normativity, and front-end responsibility.

Full refunds, why is it still not a return to the starting point?

From an accounting perspective, a complete return of principal seems to imply that the transaction did not occur, and users did not incur losses. However, refunds do not fully restore users to the state before the subscription. Not receiving an allocation does not necessarily constitute an investment loss that the platform should compensate, yet it cannot be simply understood as "users bore nothing."

The first type of cost is capital occupation. Users lock stablecoins in the activity to subscribe, giving up other returns and trading opportunities during that period. Even if the funds are eventually returned, the opportunity cost still exists. Bybit calculates additional rewards based on a fixed interest rate, which essentially acknowledges that the occupation of funds carries a cost.

The second type is transaction friction. Subscriptions may involve currency exchanges, cross-chain transactions, on-chain fees, platform fees, and bid-ask spreads. If the refunded currency, chain, or receipt method changes, users may also incur additional conversion costs. Whether the platform auto-refunds, whether it processes fees, and whether it requires users to perform additional actions are more indicative of service quality than the compensation figures presented on a promotional poster.

The third type is strategic risk. Some users might anticipate "receiving the spot" and establish hedge positions in advance. If the spot does not arrive, the hedge turns into a one-sided risk. Such losses may not belong to the platform's legal responsibility, but they illustrate that activity rules, quota uncertainties, and the timing of outcome announcements directly affect user decisions.

The fourth type is trust cost. What users participate in is not a segment that they can independently audit via a smart contract, but a chain of agents comprising underwriters, brokers, issuers, and platforms. When the results are opaque, the market naturally generates doubts about "where the shares went." Even if such doubts lack evidence, platforms need to eliminate them with more thorough information disclosures rather than simply demanding user trust.

Where do profits come from, and who bears the risks, is now very clear: the profits for successful allocators come from repricing between the issuance price and secondary market prices; before stocks are genuinely delivered, users bear the risks of quotas, capital occupation, platform execution, and information asymmetry. Platforms that gain traffic, asset accumulation, and brand exposure cannot explain all failures as upstream problems.

Why do decentralized users still need to trust centralized institutions?

The most ironic aspect of this incident is that users, in pursuit of verifiable rules, still entrust their funds and outcomes to a series of commitments from centralized institutions when entering the real asset market.

This does not mean that users are hypocritical, nor does it signify a failure of the decentralized narrative. Real-world assets have never been purely a chain-based system from the start: real stocks require verification from corporate law and securities law, need brokers to record them, need custodians to hold them, and require courts to execute in the case of bankruptcies and disputes. As long as the underlying assets exist off-chain, on-chain products will necessarily collaborate with centralized institutions.

The real question is not whether centralized institutions exist, but whether these institutions' commitments can be seen, verified, and held accountable. Traditional finance relies on licenses, capital requirements, audits, disclosures, and judicial systems to build trust; the crypto market is accustomed to using open code, on-chain balances, automated execution, and composable interfaces to reduce trust costs. The two systems need not be purely adversarial; they are more likely to divide labor in the realm of real-world assets.

If on-chain only issues a tradable symbol, while the underlying stocks, quotas, and capital flows remain invisible, then so-called decentralization only happens on the most superficial layer. Conversely, if platforms can publicly disclose upstream entities, quota limits, distribution rules, custody addresses, or asset proofs, and write refund conditions into automatic execution programs, then blockchain would truly enter into the accountability chain, rather than just remaining at the marketing interface.

What can "code is law" solve, and what can it not?

"Code is law" emphasizes constraining the execution process by public programs. The SpaceX incident reminded the market that what blockchain initially sought to reduce was precisely the unverifiable commitments of agents. If subscription funds, total demand, final quotas, and allocation formulas are all auditable, users at least do not need to guess whether the platform altered the rules temporarily.

Code can transparently allocate existing shares, but cannot create quotas that do not exist upstream

Code can record the time of fund entering, can fix subscription priorities, can automatically allocate proportionally after obtaining total quotas, and can automatically refund in case of zero quotas. It can also publicly prove how many underlying assets the issuer holds, limit unsecured issuance, and write conditions for triggering certain risks into smart contracts.

However, the boundaries of code are equally clear. It cannot compel underwriters to increase IPO quotas, cannot complete securities registration by itself, nor can it replace custodians in handling dividends, stock splits, and corporate actions. When the issuing entity goes bankrupt, custody assets are frozen, or cross-border regulations conflict, legal contracts, licensed entities, and judicial enforcement will ultimately be needed.

Therefore, a more realistic direction is not "replacing all institutions with code," but rather transforming institutional commitments into verifiable and accountable interfaces. The underwriting relationship does not have to be fully on-chain, but platforms can disclose the level they operate at; underlying stocks cannot be created by smart contracts, but already acquired shares can be audited; judicial rights cannot be granted by code, but product terms can more clearly tell users what they actually own.

This also explains why competition for U.S. stocks going on-chain ultimately does not occur only in terms of public chain performance and trading interfaces. The real barrier may come from who can connect licensed securities broker dealers, custodians, clearing entities, special purpose issuers, on-chain settlements, and global distributions into a clearly accountable chain.

Can crypto IPOs truly enter the mainstream?

Returning to the title, crypto IPOs have indeed "made it to the table" in some aspects. They can gather funds globally, package complex securities products into stablecoin accounts, and allow users who previously could not easily access traditional brokers to obtain new market entry points. This distribution table has formed and is likely to continue expanding.

However, in the face of scarce IPOs like SpaceX, most crypto platforms have still not stabilized their position at the allocation table.They have the demand but may not have the underwriting relationships; they have users but may not control the underlying supply; they can issue or distribute tokens but may not ensure that real stocks first enter custody accounts.

So, what will the next crypto IPO subscription look like? In an optimistic scenario, more platforms will connect directly with licensed brokers and reliable allocation channels, making quotas, funds, and user rights auditable. In a neutral scenario, crypto platforms will continue to play the role of the global retail distribution layer, accepting that popular IPOs can only receive partial allocations, and fully incorporating this uncertainty into their product rules. In a pessimistic scenario, platforms repeatedly absorb funds from hot assets, only to end with refunds, alternative tokens, and marketing rights, ultimately exhausting users' trust in the entire realm of on-chain stocks.

Therefore, true entry at the table is not merely randomly snagging a small portion of stocks from an IPO, nor simply offering a higher compensation after an activity fails. It means a platform can continuously answer three questions: where do the stocks come from, what do users actually receive, and who is responsible in case of failure.

The distribution table decides who can see the opportunity, the allocation table decides who truly owns the opportunity. SpaceX has clearly showcased the long-standing distance that existed between these two tables to the crypto market for the first time.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。