Written on the eve of SpaceX's IPO.

Written by: EXIO Research Institute

The soon-to-be-listed SpaceX has brought the pre-IPO token to the forefront, but what is truly important is not "who can let users buy SpaceX early," but rather how private equity is being repackaged by virtual asset exchanges, tokenization platforms, and compliant securities infrastructure. The market is transitioning from "can we trade exposure on a popular company" to "who can prove the underlying assets actually exist."

This is also the core judgment of this article: the next round of competition for pre-IPO tokens will not be about traffic but about layers of trust. Platforms that can prove the existence of underlying assets, custody structures, investor rights, and compliance with sales boundaries will gradually push out gray products that only sell stories, lack real underlying assets, or only provide vague economic exposure from the mainstream market.

In the past few weeks, multiple routes have appeared in the market: Kraken / xStocks and Bybit / xStocks focus on tokenized IPO access; Coinbase launched pre-IPO perpetual futures for non-U.S. users; Bitget / Republic launched products like preSPAX that are linked to SpaceX's future IPO or acquisition economic returns; Binance, Hyperliquid, and others have also provided pre-IPO or synthetic exposure related to SpaceX. EX.IO itself is also advancing a matrix of tokenized securities / RWA products under a compliant framework in Hong Kong. This indicates that pre-IPO tokens are no longer just a marketing move by a single platform but are part of a differentiating new market.

1. First, clarify the concepts: pre-IPO tokens do not equal "having bought stocks"

The market currently refers to several types of products as pre-IPO tokens, but their legal and economic implications are completely different.

The first type is tokenized equity / tokenized IPO access. The platform claims that qualified investors can submit subscriptions, and if they receive an allocation, on the listing date they will receive a tokenized representation backed 1:1 by the underlying stock. Kraken's SpaceX IPO Access page states that qualified users can submit non-binding intentions and will receive SPCXx after successful allocation; it also clearly states that xStocks provides price exposure without voting rights or dividend rights, allocations are not guaranteed, and it is not accessible to certain jurisdictions such as the U.S., U.K., Canada, and Australia.[1]

The second type is pre-IPO perpetual / synthetic exposure. Coinbase's pre-IPO markets are perpetual futures settled in USDC, tracking SpaceX's pre-IPO valuation; these products deal with price exposure, not stock equity.[2] SpaceX related pre-IPO or synthetic exposures seen in markets like Binance, Hyperliquid, are also closer to valuation trading, rather than equity holdings.[3]

The third type is economic rights / note / proxy token. For example, Bitget's IPO Prime has launched preSPAX, which is described in market reports as a product issued by Republic, linked to SpaceX's future IPO or acquisition economic returns.[4] It is closer to structured economic exposure than pure perpetuals, but investors still need to be clear: what exactly is the underlying asset, who holds it, whether there are real shares, SPV rights, note rights, or just some kind of revenue calculation formula.

The fourth type, which is also the riskiest, is the "story-type token" without proof of the underlying assets. It may use the names of popular companies like SpaceX, OpenAI, and Anthropic but cannot prove the underlying shares, custodians, legal rights, redemption arrangements, and investor suitability. This type of product is most prone to fraud or misleading sales risks.

Therefore, the first principle of pre-IPO tokens is not "can it be traded," but "what exactly are you buying."

2. Why will SpaceX become a tipping point?

SpaceX is an ideal pre-IPO token asset: the brand is strong enough, the IPO expectations are high enough, global investors can understand, and ordinary investors have long found it difficult to access its private equity market.

Traditional pre-IPO equity is not inherently retail-friendly. It typically relies on private equity funds, secondary equity platforms, SPVs, family offices, brokerages, and institutional relationships, resulting in high investment thresholds, numerous transfer restrictions, and opaque information. For global non-U.S. retail investors, the opportunity to participate in the allocation of U.S. star company IPOs before is even more limited.

Virtual asset exchanges see a structural gap: users want to buy popular private companies; traditional brokerage accounts may not provide access; crypto users are used to 24/7 trading and small participation; tokenization can make shares, settlements, and transfer experiences more like digital assets. This explains why exchanges like Kraken, Bybit, Coinbase, Bitget, Binance, and Hyperliquid are all making moves around SpaceX.[5][6]

However, this does not mean they offer the same thing. On the contrary, the SpaceX frenzy exposes the biggest confusion in this market: products referred to as SpaceX exposure could be a 1:1 backed tokenized representation, perpetual futures, economic return-linked tokens, or simply customized price games on platforms. This is why the article cannot be written as a product introduction for a single exchange. The real analysis should focus on how the whole market is layered.

3. Platform Landscape: Five Routes Competing for Entry

3.1 xStocks Route: Connecting the Exchange Front End to Regulated Securities Structure

xStocks is one of the core infrastructures in this discussion. It is not a single exchange, but a framework for tokenized equities under the Payward / Backed related system. The related products from Kraken and Bybit all use xStocks as a foundational framework to varying degrees.[1][5]

xStocks officially states that its IPO access framework will aggregate user demand from partner platforms and collaborate with the underwriting syndicate to obtain allocations; in the process it describes, shares will be tokenized after the allocation is finalized on the public listing date and will be supported 1:1 by underlying shares held in custody by a regulated entity. However, xStocks also clearly states: it is not open to U.S. persons or entities, there are geographic restrictions, and it does not constitute an offer to sell U.S. securities; Kraken's page also clearly states that xStocks offers price exposure without voting or dividend rights, allocations are not guaranteed.[1]

This indicates that the advantage of xStocks lies in its attempt to structure tokenized equity with custody, frameworks, and qualified investor restrictions rather than casually issuing a "SpaceX token." But its limitations are also clear: this is not a direct IPO by the issuer, not backed by the issuer, does not guarantee allocation, and does not equate to complete shareholder rights in a traditional stock account.

3.2 Coinbase Route: Providing Valuation Exposure through Pre-IPO Perpetuals

Coinbase's pre-IPO markets resemble innovations in derivative markets. Cointelegraph reports that Coinbase launched pre-IPO markets starting with SpaceX, providing USDC-settled perpetual futures for qualified users outside the U.S. that track the pre-listing price of private companies.[2]

The advantage of this route is high trading efficiency and a clear structure: it is a contract, not disguised as stock. The downside is also straightforward: investors are obtaining price exposure, not underlying shares; risks come from leverage, margin, funding rates, index pricing, liquidity, and liquidation mechanisms. If users believe they have "bought SpaceX stock," that is a serious misunderstanding.

3.3 Bitget / Republic Route: Packaging Pre-IPO Rights as Economic Return Tokens

Bitget launched IPO Prime in April, debuting preSPAX, issued by Republic, which market reports say is linked to SpaceX's future IPO or acquisition economic returns.[4] This route is positioned between tokenized equity and synthetic perpetuals: it is not purely transactional like perpetual futures, nor is it necessarily equivalent to direct stockholdings.

The professional issue lies in structural disclosure: investors need to know whether the underlying holds SpaceX equity, who holds it, whether it is through SPVs, what legal rights token holders have regarding the SPV or returns, if it is redeemable, whether there is a lock-up period, and how to handle scenarios like IPOs, mergers, delays, or failures. Such products may have value, but they must clearly communicate this in the documentation. Otherwise, they risk being misinterpreted by the market as "buying SpaceX stock early."

3.4 Binance / Hyperliquid Route: Synthetic Speculation Under High Liquidity Narrative

Binance, Hyperliquid, and others are leaning towards trading-type scenarios. They provide contracts or synthetic markets focused on the valuation of SpaceX pre-IPO. The advantage is speed, liquidity concentration, and ease of understanding for crypto-native users; the risk is that it is closer to high volatility speculation.[3]

The key risk of such products does not lie in whether a transaction can be quickly established, but whether the pricing anchors, leverage, margin, market depth, and liquidation mechanisms are sufficiently transparent. They are not cases of underlying asset fraud, but they illustrate one fact: in a pre-IPO synthetic market without enough depth, mature market-making, and a clear underlying asset anchor, prices can rapidly distort, and retail users can easily bear actual market structure risks within the "star asset narrative." On May 28, 2026, contracts on Hyperliquid linked to SpaceX's pre-IPO experienced a 45% flash crash, resulting in approximately $1.51 million being liquidated.[7]

3.5 EX.IO Route: A Hong Kong Sample of Compliant RWA/tokenized Securities

EX.IO has expanded its regulated tokenized securities product matrix under a compliant framework in Hong Kong, including products like GNIT-LPF2, STBL, TBILL / OpenEden, and has been reported by PR Newswire APAC as one of the leading platforms offering compliant tokenized securities products in licensed virtual asset trading platforms in Hong Kong.[8] (For the information regarding specific targets or products, please refer to EX.IO's official announcements and publicly disclosed documents.)

4. The Biggest Risk is Not "Price Drops," but "The Underlying Does Not Exist at All"

The most dangerous aspect of pre-IPO tokens is not their volatility, but that investors may not know whether the underlying assets exist at all.

The SEC's investor education website Investor.gov has a straightforward warning about pre-IPO scams: scammers often claim that investors can buy pre-IPO shares of upcoming public companies, using high-yield promises, social media marketing, professional-looking websites, and phrases like "the IPO is coming soon" to attract investors. Common red flags for this type of scam include unregistered investment professionals, aggressive sales, social media solicitation, and claims that the company is in a hot tech or emerging industry.[9]

Placing this reminder into the tokenized pre-IPO market amplifies the risks. Because the presence of tokens can make products appear more "tradeable" and "real," having a token on-chain does not mean there are underlying stocks.

To professionally assess pre-IPO tokens, at least eight questions should be asked:

As long as these questions remain unanswered, the more popular the product, the greater the risk.

5. Why are Disclosure and Regulatory Chains More Important?

The issue is not a simple "compliant platforms are more reliable," but whether the platform can clarify the asset chain, disclose clearly, and accept verifiable constraints. A credible pre-IPO token / tokenized equity product needs at least four layers of proof: asset proof (where the underlying shares, SPV rights, or economic rights come from); custody proof (who holds the underlying assets, whether there is bankruptcy isolation, and whether it is auditable); rights proof (what legal rights token holders have over the underlying assets or cash flows); sales proof (which jurisdictions and investors it is aimed at, whether there are suitability restrictions and risk disclosures).

This is why infrastructure companies like Securitize deserve to be included in this discussion. Securitize's announcements with Cantor Equity Partners II show that it operates in the U.S. through SEC-registered broker-dealers, SEC-regulated ATS, SEC-registered transfer agents, etc., and provides relevant infrastructure for tokenized funds for institutions like BlackRock, Apollo, BNY, Hamilton Lane, KKR, and VanEck.[10] It is not a provider of SpaceX pre-IPO products, but it illustrates what is needed for tokenized capital markets to go mainstream: broker-dealers, ATS, transfer agents, fund administration, custody, disclosure, rather than an isolated token.

Kraken/xStocks' disclosures provide an observant case for public disclosure: it clearly states geography restrictions, no voting or dividend rights, allocation not guaranteed, and value may go down as well as up. These seemingly "conservative" words are exactly the dividing line between professional products and gray products. In contrast, if a platform only emphasizes "buying SpaceX early," "striking it rich before the IPO," "global accessibility," "no qualifications required," yet does not discuss custody, rights, restrictions, and risks, that is not innovation, it is a dangerous signal.

6. What are Wall Street, Exchanges, and Issuers Thinking?

6.1 Wall Street: Not Opposing Tokenization, But Wanting to Incorporate It Into Regulated Rails

Wall Street is not simply against tokenization. Judging from publicly available information, Securitize has served institutions like BlackRock, Apollo, Hamilton Lane, KKR, and VanEck with tokenized funds / tokenization projects; its announcements also mention collaborations with NYSE supporting tokenized securities infrastructure and digital transfer-agent standards.[10] This indicates that traditional finance is not rejecting on-chain record and settlement efficiency but rather hopes to incorporate them into regulatory, auditable, and custodial market infrastructures.

However, what Wall Street wants is not unbounded issuance but controlled issuance: KYC, investor suitability, custody, clearance, transfer agents, broker-dealers, information disclosure, and accredited investor rules must be within the system. In other words, Wall Street does not reject on-chain stocks but does not want "shadow stocks" without a regulatory chain.

6.2 Virtual Asset Exchanges: Transitioning from Crypto Venue to Multi-Asset Distribution Platform

For exchanges like Kraken, Bybit, Coinbase, Bitget, and Binance, the appeal of pre-IPO tokens is clear: they do not want to be just trading venues for BTC/ETH/SOL but want to become the gateway for global users to access popular assets. This is also why SpaceX is particularly important. SpaceX is an asset that can bring crypto users, traditional stock users, AI/ aerospace narrative users, and global retail users onto the same page. If exchanges can meet this demand, they may evolve from digital asset exchanges into multi-asset distribution platforms. However, there is a natural challenge for the exchanges: the larger the traffic, the greater the pressure for compliance and proof of underlying assets. Exchanges can serve as user gateways, but they cannot skip the chain of securities issuance and custody.

6.3 SpaceX / Issuers: The Core Attitude is Usually Cautious or Even Distant

From the issuer's point of view, third-party tokenized exposure is a double-edged sword. On one hand, it broadens market awareness; on the other, it may create misunderstandings among unauthorized investors, leading users to believe that the related tokens have official endorsements from SpaceX. Therefore, it is crucial to repeatedly differentiate: while SpaceX is popular, it does not mean SpaceX endorses every SpaceX token; the existence of pre-IPO exposure does not mean the issuer is involved, acknowledges, or guarantees the presence of underlying shares. The same logic applies to any trendy private company, including OpenAI, Anthropic, Stripe, etc. The rational attitude of issuers is usually that actual IPOs and stock transfers must go through formal securities documents, underwriting, transfer restrictions, and the company's articles of association; third-party tokens that cannot prove authorization and underlying asset chains cannot be considered issuer securities.

7. EXIO Research Institute's Judgment: Pre-IPO Tokens Will Persist, but Will Quickly Layer

Our judgment is clear: pre-IPO tokens will not just be a short-term fad; they will become an important branch of RWA / tokenized securities; but this market will rapidly stratify.

The first layer is the disclosure and regulatory chain level. These products will emphasize the real existence of underlying assets, 1:1 or clear proportional backing, custodians, SPV/notes/rights structures, investor suitability, judicial jurisdiction restrictions, risk disclosures, and audit-able documents. They will not promise returns and will not imply issuer endorsement. Platforms and infrastructures that place more emphasis on disclosure and regulatory chains are more likely to form a long-term market foundation around this layer.

The second layer is the trading exposure layer. Coinbase pre-IPO perps, Binance/Hyperliquid synthetic exposure are more suitable for high-risk traders. They can exist but must be clearly labeled as derivative/synthetic exposure, without being packaged as "buying stocks."

The third layer is the gray narrative layer. Such products rely on the names of popular companies, KOL promotion, and generate FOMO through "getting on board before the IPO," yet cannot prove the underlying assets, custody, and rights. They may have traffic temporarily, but in the long run, they will be squeezed by regulations, investor education, and market incidents. Therefore, the core opportunity of pre-IPO tokens does not lie in who shouts the loudest, but in who can most clearly answer one question: where are the underlying assets?

8. A Judgment Framework for Readers: Look at Pre-IPO Tokens, Not Stories, but the Chain

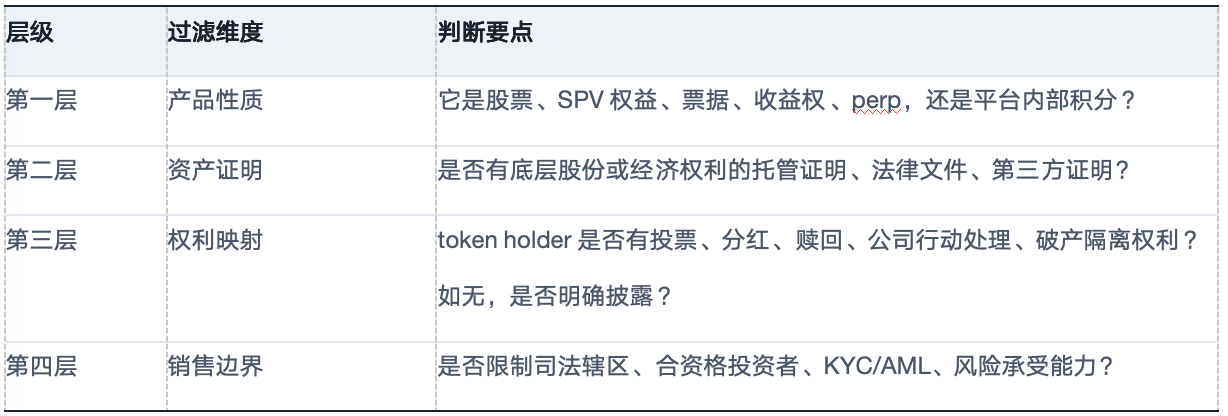

If you want to assess whether a SpaceX / OpenAI / Anthropic pre-IPO token is credible, you can filter it through four layers:

The more sufficiently disclosed platforms will write these restrictions clearly; the weaker the disclosure of products, the more they will only talk about "fast," "early," "scarce," and "getting rich." This is also our attitude toward this track: pre-IPO tokens are an important direction for RWA, but being more aggressive is not necessarily better. What is truly more likely to survive through cycles is not the narrative that generates the most FOMO, but the market infrastructure that can best prove the underlying assets and legal rights.

References

[1] Kraken Blog - SpaceX IPO access now available via xStocks

https://blog.kraken.com/product/xstocks/spacex-ipo-access

[2] Cointelegraph - Coinbase launches pre-IPO markets, starting with SpaceX

https://cointelegraph.com/news/coinbase-launches-pre-ipo-markets-amid-crypto-push-private-markets

[3] CoinDesk - Hyperliquid's pre-IPO SpaceX contracts suffer 45% flash crash

https://www.coindesk.com/markets/2026/05/28/hyperliquid-s-pre-ipo-spacex-contracts-suffers-45-flash-crash-liquidating-usd1-5-million

[4] Decrypt - SpaceX Nearing $1.75 Trillion IPO; Bitget Offers Pre-IPO Exposure

https://decrypt.co/363950/elon-musk-spacex-nearing-1-75-trillion-ipo-bitget-pre-ipo-exposure

[5] PR Newswire - Bybit Launches IPO Express with SpaceX

https://www.prnewswire.com/news-releases/bybit-launches-ipo-express-becoming-one-of-first-centralized-crypto-exchanges-to-offer-tokenized-ipo-access-starting-with-spacex-302793370.html

[6] CoinDesk - HYPE pops 7% as SpaceX pre-IPO lands on Hyperliquid

https://www.coindesk.com/markets/2026/05/18/hype-pops-7-beating-bitcoin-declines-as-spacex-pre-ipo-lands-on-hyperliquid

[7] Source [3]

https://www.coindesk.com/markets/2026/05/28/hyperliquid-s-pre-ipo-spacex-contracts-suffers-45-flash-crash-liquidating-usd1-5-million

[8] PR Newswire APAC - EX.IO Expands Regulated Tokenized Securities Product Matrix

https://www.prnewswire.com/apac/news-releases/exio-expands-regulated-tokenized-securities-product-matrix-solidifying-leadership-in-rwa-market-302727027.html

[9] Investor.gov / SEC - Pre-IPO Investment Scams

https://www.investor.gov/protect-your-investments/fraud/types-fraud/pre-ipo-investment-scams

[10] FT Markets - Securitize and Cantor Equity Partners II Announce SEC Declaration

https://markets.ft.com/data/announce/detail?dockey=600-202606051045PR_NEWS_USPRX____FL76813-1

[11] xStocks - Announcing Tokenized IPO Access for Retail Investors Across the Globe

https://xstocks.fi/news/

[12] RWA.xyz - Global Market Overview

https://app.rwa.xyz/

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。