The retail investors' money runs faster than Wall Street's roadshows

While global retail investors are still waiting for the official IPO of SpaceX tomorrow, crypto retail investors have been playing with SpaceX's equity for three months.

As of June 10, over 15 crypto exchanges and platforms in the crypto space have already offered Pre-IPO products of SpaceX to retail investors. Binance, OKX, Bitget, Hyperliquid, Coinbase, Bybit, Kraken, and others have all entered the market, rolling out a complete line of products from perpetual contracts to SPV tokens (which hold SpaceX shares indirectly through a specially established holding company and tokenize the shares for retail investors), to tokenized IPO allocations.

According to Coin Metrics, as of June 9, just in perpetual contracts alone, the total open interest across platforms has exceeded 385 million dollars, with peak daily trading volume over 250 million dollars, and cumulative trading volume reaching 2.7 billion dollars.

Additionally, Bitget created a product with 61 million dollars in holdings, which was entirely sold to retail investors, and platforms like Gate.io, MEXC, and BitMart together totaled over 35 million dollars; the total distribution of Pre-IPO tokens is close to 100 million dollars. At the same time, Kraken opened a subscription quota of 400 million dollars for SpaceX through the xStocks framework, and Bybit IPO Express allocated 100 million dollars.

From IPO allocations, SPV shares to perpetual contract holdings, the actual capital investment and risk exposure of crypto retail investors in SpaceX have surpassed 1 billion dollars.

What exactly are crypto retail investors buying with SpaceX?

In April, Pre-IPO perpetual contracts were still a niche product existing only on Hyperliquid, with an average daily trading volume of just a few million dollars. Two months later, Binance, OKX, and Coinbase all entered the market, a speed of spread rarely seen in the history of crypto derivatives, faster than the rollout of contract trading and meme coin categories.

The catalyst was the IPO of an AI chip company. On May 14, Cerebras listed on Nasdaq, with underwriters pricing it at 185 dollars per share, which opened directly at 350 dollars. In the last hour before the opening, the VWAP for CBRS perpetuals on Hyperliquid was 354.54 dollars, with a deviation of only 1.3%, while traditional private placement trading platforms Forge and EquityZen had deviations as high as 35%. On-chain contracts provided the closest price to the opening price without the involvement of underwriters, and every product manager at CEX saw the same thing.

The race to enter the market started quickly in May, with OKX first launching Pre-IPO perpetual contracts, followed by Trade.xyz on Hyperliquid, with a first-day trading volume of 33 million dollars. On May 21, Binance entered the market, marking a turning point. According to CoinDesk data, the average daily trading volume for the entire Pre-IPO perpetual market was around 20 million dollars before Binance launched; after Binance's entry, there were four days in the following seven with daily turnover breaking 100 million dollars, accumulating to 400 million dollars. On June 4, Coinbase launched SPCX-PERP, with the last arriving giant filling in the last piece.

Apart from perpetuals, Bitget distributed 61.1 million dollars of SPV tokens through Republic, followed by Gate.io, MEXC, BitMart, and others. In early June, Kraken and Bybit opened tokenized IPO allocations through xStocks, with a cumulative quota of 500 million dollars. The three product lines were fully rolled out within two months.

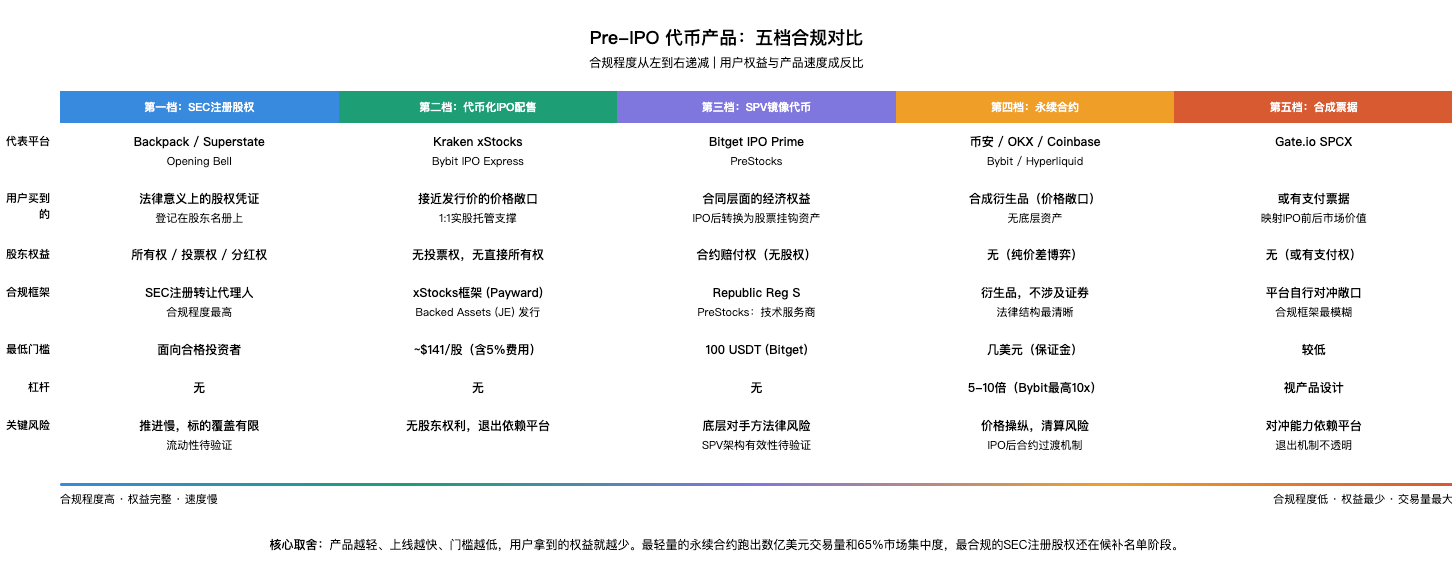

If categorized by compliance level, the Pre-IPO token products currently available on the market can be roughly divided into five tiers, with significant disparities between them. The 1 billion dollar capital scale is distributed among these five product tiers, showing very high concentration.

Perpetual contracts allow users to buy a price bet. Perpetual contracts are the most traded categories with the most participating platforms, and currently, all major trading platforms have listed SpaceX perpetuals, with leverage up to 10 times, and pricing determined by market speculation, having no legal relation to the underlying equity. Retail investors buy a price exposure and receive no shareholder rights. This tier contributed the largest portion of the 1 billion dollars, with total open interest on all platforms at 385 million dollars and cumulative trading volume at 2.7 billion dollars, with Binance holding 65% of that.

SPV mirror tokens, on the other hand, offer users a contractual economic interest. SPV mirror tokens have the most diverse means of participation, including PreStocks accessed through Binance's Web3 wallet, Bitget IPO Prime, etc. The compliance backbone that enables Bitget IPO Prime is Republic, a U.S. compliant crowdfunding platform established in 2016, whose core practice is embedding SPVs into its private placements and crowdfunding ecosystem. While taking the SPV path, different platforms have fundamentally different methods. Ken, the product manager for Bitget IPO Prime, provided a concrete comparison during an interview with Foresight News, explaining that Bitget IPO Prime directly acquires old shares of SpaceX through Republic to issue tokens, with a shorter underlying asset chain. Some platforms participate as technology service providers, not holding underlying assets directly, with asset pools involving multiple counterparties; the longer the chain, the higher the difficulty in validating the legal structure.

According to him, Bitget chose to sign an exclusive cooperation with Republic for 1 to 2 years, creating a special pool for preSPAX to directly acquire the corresponding number of old shares on a 1:1 basis according to the public offering scale, while completing legal due diligence on the authenticity of the assets and counterparty reliability before the acquisition.

A Hong Kong SFC-licensed digital asset trading platform provided another window to observe how the SPV path operates. In May 2026, this platform collaborated with a Singapore MAS licensed institution to complete Asia's first compliant tokenized distribution of SpaceX equity-linked depository receipts. The platform's head told Foresight News that this product structure is divided into three layers: the first layer consists of original shareholders such as early VCs of SpaceX, the second layer comprises SPV holding the shares, and the third layer is the frontend trading platform facing users. The total distribution of SPV tokens is close to 100 million dollars, providing users with contractual economic rights, but whether these can be fulfilled depends on the authenticity of the underlying assets and whether the SPV legal structure holds up.

Tokenized IPO allocation allows users to buy a price exposure close to the issue price, supported by a 1:1 actual share custody, but without shareholder status. Kraken and Bybit opened IPO subscription applications for SpaceX to users in over 110 countries worldwide through the xStocks framework under Payward. Each token is backed 1:1 by an actual share held by a custodian, but Kraken's documentation clearly states that holders have no voting rights and do not constitute direct ownership of the underlying shares. Together, the two platforms allocated 500 million dollars, the largest single sector out of the 1 billion dollars.

On-chain equity registered with the SEC provides users with actual shares. The Opening Bell initiative, launched by Backpack in collaboration with SEC-registered transfer agent Superstate, offers legally recognized SpaceX shares that users obtain actual shareholder status. This is the path with the highest compliance level but also the slowest to advance; it has not yet officially launched as of early June.

The final tier is Gate.io's SPCX, which provides users with a financial contract. An industry insider also pointed out that Gate.io's SPCX is a type of contingent payment note, and the underlying hedge exposure disclosure is extremely limited, while the compliance framework lacks unified standards in traditional finance.

The structural trade-offs among these five product tiers are very clear: the higher the level of compliance, the more complete the user rights, the slower the product advancement speed, and the smaller the covered user scale. The most compliant SEC-registered shares are still waiting in line, while the lightest perpetual contracts have already generated hundreds of millions in trading volume and 65% market concentration.

Interestingly, the inverse relationship between trading volume and user rights applies to pricing capability as well; the perpetual contracts, which offer the least user rights, have the most accurate pricing. There is no positive correlation between complete rights and accurate pricing; retail investors have chosen the lowest threshold and fastest product, which also happens to provide the most effective price discovery.

The same SpaceX has four different prices across four markets

Interestingly, the SpaceX quotes retail investors see on different platforms vary so greatly that they seem like completely different assets.

On June 10, Bitget's preSPAX (SPV token) was priced at about 156 dollars, Binance's SPCX perpetual at about 174 dollars, and OKX's SPACEX perpetual at about 191 dollars. Meanwhile, on Hyperliquid, which had not executed a Rebase, SPACEX-USDH was still quoted at about 1982 dollars, with a price difference exceeding 10 times from other platforms.

The root of the price difference lies partly in the differing original prices obtained by each platform before pushing products, as well as varying subscription prices; some Pre-IPO perpetuals are priced on a "per share price" basis, while SpaceX has never disclosed the exact total number of shares before submitting its S-1. Each platform can only estimate.

Moreover, there is no effective arbitrage channel between platforms. The preSPAX on Bitget cannot be converted into the PreStocks SPACEX and cannot directly hedge with the old shares on Forge. Each platform's holders are effectively locked in by a single issuer until the day SpaceX goes public. When liquidity suddenly dries up on a smaller platform, retail investors face slippage and liquidation risks far exceeding those in mainstream platforms.

On June 1, SpaceX submitted the S-1A amendment, disclosing fully diluted shares of about 13.08 billion, which deviated from previous estimates by most platforms. Platforms began to adjust their capital bases in succession and Rebase their SpaceX-related products' prices.

OKX was the first to execute a Rebase on June 2, adjusting its capital from 1 billion to the 12.52 billion shares disclosed in the S-1, with an adjustment ratio of 12.52 times, bringing contract prices down from above 2000 dollars to the range of 150 to 200 dollars. Binance's SpaceX (SPCX) Pre-IPO perpetual had reserved a Rebase clause upon launch, specifying that a deviation above 3% in equity would trigger an adjustment; after the S-1A was published, the deviation far exceeded the threshold, and on June 8, it officially announced a 1.1 times Rebase, executed on June 10. Trade.xyz explicitly stated that it would not execute any Rebase, hence its price remains around 2000 dollars.

After the completion of successive Rebases, prices began to converge across platforms. Coin Metrics data indicates that as of June 8, the VWAP for SPCX perpetuals across all platforms had converged to 155 dollars, a premium of about 15% over the issue price of 135 dollars, with an implied valuation of about 1.94 trillion dollars. However, short-term arbitrage opportunities arose during the convergence process; after Binance confirmed its Rebase, the cross-platform price difference peaked at 10%, allowing institutions and market makers to establish long positions on Binance and equal short positions on Trade.xyz, locking in certain profits once the Rebase was executed and the prices converged.

Liquidity fragmentation is merely a surface issue; the underlying product risks are more substantial.

Research by Arkstream Capital has found that at a 1.2 trillion dollar valuation level, less than 10% of the Pre-IPO shares marked as SpaceX in the market can actually be executed for delivery, with multiple intermediary organizations repeatedly listing the same batch of shares, nominal supply vastly exceeding real holdings. The implied valuation of the Anthropic token on PreStocks once reached 1.5 trillion dollars, while the actual assets held by the underlying SPV amounted to only about 23 million dollars.

On May 13, Anthropic and OpenAI publicly stated that the transfer of shares via SPV is invalid under the company's bylaws, causing the tokens of the two companies on PreStocks to plummet by 34% to 39%. This was the largest single risk event for Pre-IPO crypto products thus far, directly exposing the legal vulnerabilities of the SPV path.

The compliance framework of Gate.io's SPCX is similarly doubted; "contingent payment notes" lack unified regulatory standards in traditional finance, and Gate.io has disclosed little about the specific arrangements for the underlying hedge exposure, making it difficult to assess the counterparty risks faced by users.

In addition to product-level risks, the profit structure that exchanges gain from Pre-IPO perpetuals is also noteworthy. The volatility of Pre-IPO targets is much higher than that of BTC and ETH, with retail investors overwhelmingly going long on these contracts, while the main participants in short positions are market makers and arbitrageurs. When the vast majority of positions align, longs need to continuously pay funding rates to shorts, which is structural. Exchanges themselves charge transaction fees on each deal and collect penalties during each liquidation. With 400 million dollars in trading volume over seven days, this category represents a new high-margin product line for exchanges. Retail investors pay a premium for the narrative of "participating in an unlisted giant," while exchanges and market makers stabilize their earnings on the other side.

Ultimately, Pre-IPO crypto products lower the threshold for entry but do not reduce underlying risks. Traditional finance filters participants with insufficient risk tolerance through accredited investor definitions and high thresholds; this mechanism has its brutal aspects but also its rationale. Crypto platforms have opened the door, but the risks behind that door—differences in product rights, the authenticity of underlying assets, uncertainties in IPO transitions, and liquidity fragmentation—have not disappeared due to the lowered barriers; they have merely shifted from the shoulders of institutional investors to retail investors.

SpaceX is just the first shot

SpaceX is the first super target for Pre-IPO crypto products; its immense IPO scale and high attention have pushed a previously marginalized experimental category into the industry's spotlight. But it is clear that this competition will not end with SpaceX's listing on Nasdaq on June 12.

OpenAI is valued at 852 billion dollars, aiming for an IPO in September, potentially surpassing a trillion in valuation; Anthropic confidentially submitted its S-1 on June 1, having just completed a 65 billion dollar Series H financing, with its latest valuation close to a trillion at 965 billion dollars, expected to IPO around October. With only these two plus SpaceX, a total market value exceeding 3.5 trillion dollars will successively enter the public market in the second half of 2026.

Currently, Nasdaq's Fast Entry rules took effect on May 1, and the S&P 500 is also proposing to shorten the quick inclusion waiting period from 12 months to 6 months. The cycle for large IPOs from listing to being allocated by index funds is sharply compressed, and passive buying from index funds will rapidly surge after listing, making the exit certainty for Pre-IPO positions higher and forming the underlying logic for this category's continued attractiveness. The advancement of each super IPO will bring a new round of demand pulse for Pre-IPO crypto products.

Pre-IPO perpetual contracts may just be transitional products; Binance's bStocks, Kraken's xStocks, and Coinbase's tokenization roadmaps all aim to trade U.S. stocks on crypto platforms. As long as the SEC’s innovative exemption framework is not in place, these plans cannot be formally advanced in the United States. The SpaceX Pre-IPO is the first stress test for this larger infrastructure plan, and the outcomes will directly impact exchanges' subsequent decisions in the tokenized stock arena.

From a longer-term perspective, the educational significance of Pre-IPO tokenized products may exceed their current trading volume. SpaceX, OpenAI, and Anthropic serve as an entry point, allowing global retail investors to first encounter concepts and tools previously reserved for accredited investors. Such products objectively play a role in financial equality, but issues such as product structure discrepancies, ambiguous rights boundaries, and regulatory vacuums are also laid bare.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。